Europe Cosmetic Products Third-Party Manufacturing Market - Outlook 2024-2034

Europe Cosmetic Products Third-Party Manufacturing Market is segmented by Type (Contract Manufacturing, Private Label Manufacturing, OEM Manufacturing, ODM Manufacturing, Others), Application (Skincare, Haircare, Color Cosmetics, Fragrances, Personal Care), End-User Channel (Luxury Brands, Mass Market Brands, Indie Brands, E-commerce Brands), Distribution Channel (Retail Stores, Online Platforms, Pharmacies & Drugstores, Specialty Stores), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Cosmetic Products Third-Party Manufacturing Market is characterized by the outsourcing of cosmetic production to specialized manufacturers who provide services such as contract manufacturing, private label production, OEM, and ODM solutions. This market serves a diverse range of cosmetic products including skincare, haircare, color cosmetics, fragrances, and personal care items. The third-party manufacturing model allows cosmetic brands to leverage advanced manufacturing technologies, regulatory expertise, and cost efficiencies while focusing on marketing and distribution. Market growth is driven by increasing demand for innovative formulations, clean and sustainable beauty products, and customization capabilities. The competitive landscape includes global and regional manufacturers emphasizing quality, compliance with stringent European cosmetic regulations, and agility in production. Key applications such as skincare and haircare dominate demand, supported by rising consumer awareness and premiumization trends. The market's strategic importance lies in enabling brands to rapidly respond to evolving consumer preferences and regulatory changes, fostering innovation and market expansion across Europe.

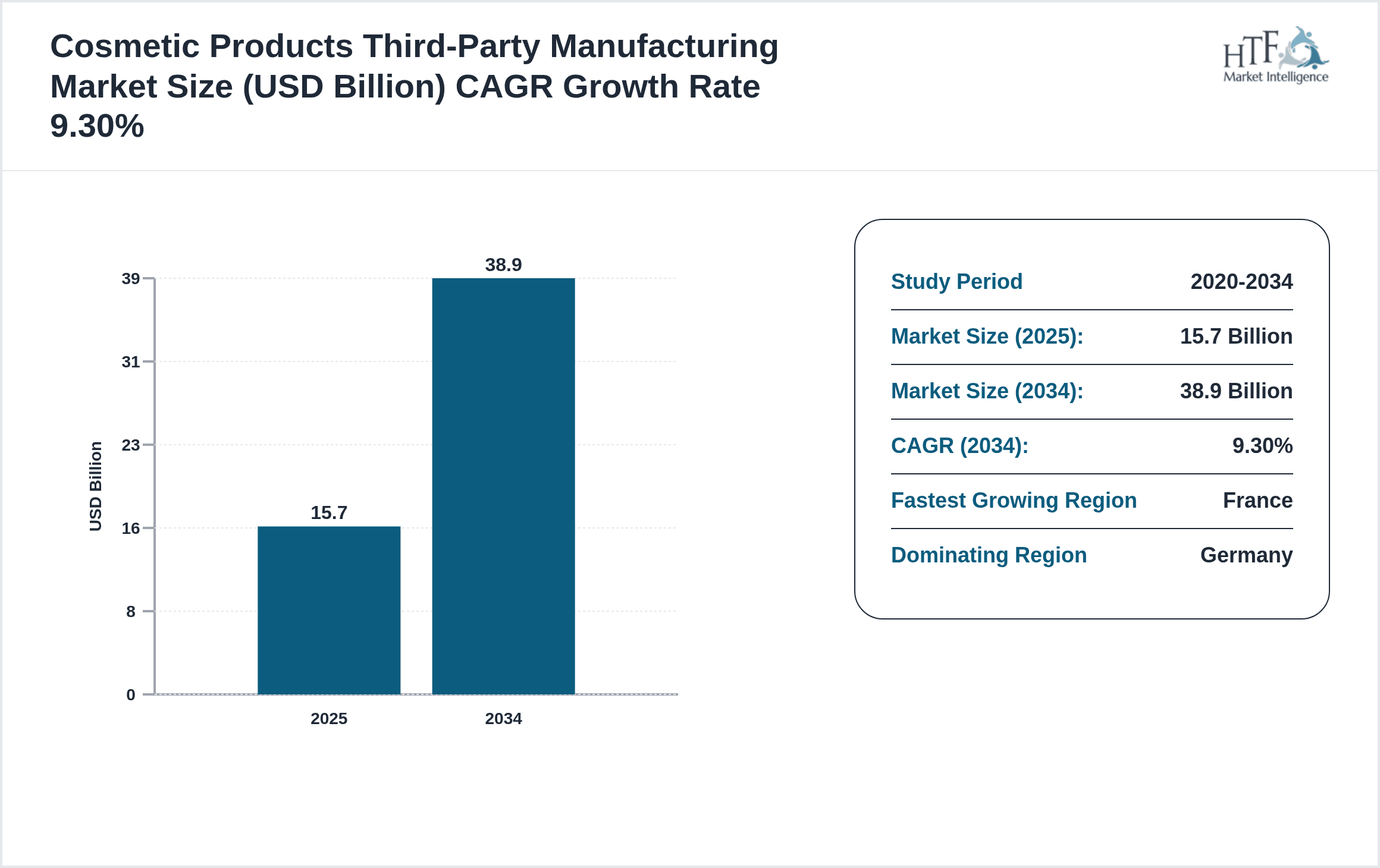

- •In 2024, the Europe Cosmetic Products Third-Party Manufacturing Market is valued at USD 15.7 Billion, with a forecast to reach USD 38.9 Billion by 2034, growing at a CAGR of 9.3%. Germany leads as the dominating country with a 25% market share, followed by France exhibiting the fastest growth at 11.2% CAGR. Contract manufacturing remains the leading product type, while private label manufacturing is the fastest growing segment, reflecting the increasing trend of branded products outsourcing production. Skincare applications dominate the market, with haircare as the second-largest segment, driven by consumer preference for wellness and natural ingredients. The market is witnessing rapid innovation and expansion driven by digital transformation, sustainability initiatives, and evolving consumer lifestyles in key countries including Germany, France, UK, Italy, and Spain.

- •The Europe Cosmetic Products Third-Party Manufacturing Market offers significant value propositions to brand owners, retailers, and manufacturers by enabling access to specialized production capabilities, regulatory expertise, and cost-effective scaling. This fosters innovation in product development, including clean and natural formulations, while maintaining compliance with stringent European cosmetic regulations. Outsourcing production reduces capital expenditure and operational risks for brands, allowing faster time-to-market and flexible production volumes. The strategic importance extends to sustainable manufacturing practices, supply chain optimization, and collaboration opportunities, positioning third-party manufacturers as critical partners in the cosmetic industry's growth trajectory across Europe. For stakeholders, this market represents a dynamic blend of technological advancement, consumer-driven innovation, and regulatory compliance shaping the future of the European cosmetic sector.

Competitive Landscape

The competitive environment of the Europe Cosmetic Products Third-Party Manufacturing Market is robust and dynamic, marked by the presence of established multinational manufacturers and agile regional players. Competition is driven by innovation in formulation technologies, adherence to stringent European cosmetic regulations, and the ability to provide customized solutions catering to diverse brand requirements. Leading manufacturers focus on strategic partnerships, technological advancements, and expanded service portfolios including R&D, packaging, and logistics to differentiate themselves. Pricing strategies balance cost efficiencies with quality assurance, while investments in sustainable and clean beauty manufacturing enhance competitiveness. The market exhibits moderate entry barriers due to regulatory complexity and high capital investment requirements, fostering a competitive advantage for incumbents. Regional competition varies, with Germany and France dominating in scale and innovation, while emerging markets in Eastern Europe offer growth opportunities. Future trends suggest intensifying rivalry based on digital transformation, eco-friendly processes, and faster product development cycles to capture increasing demand.

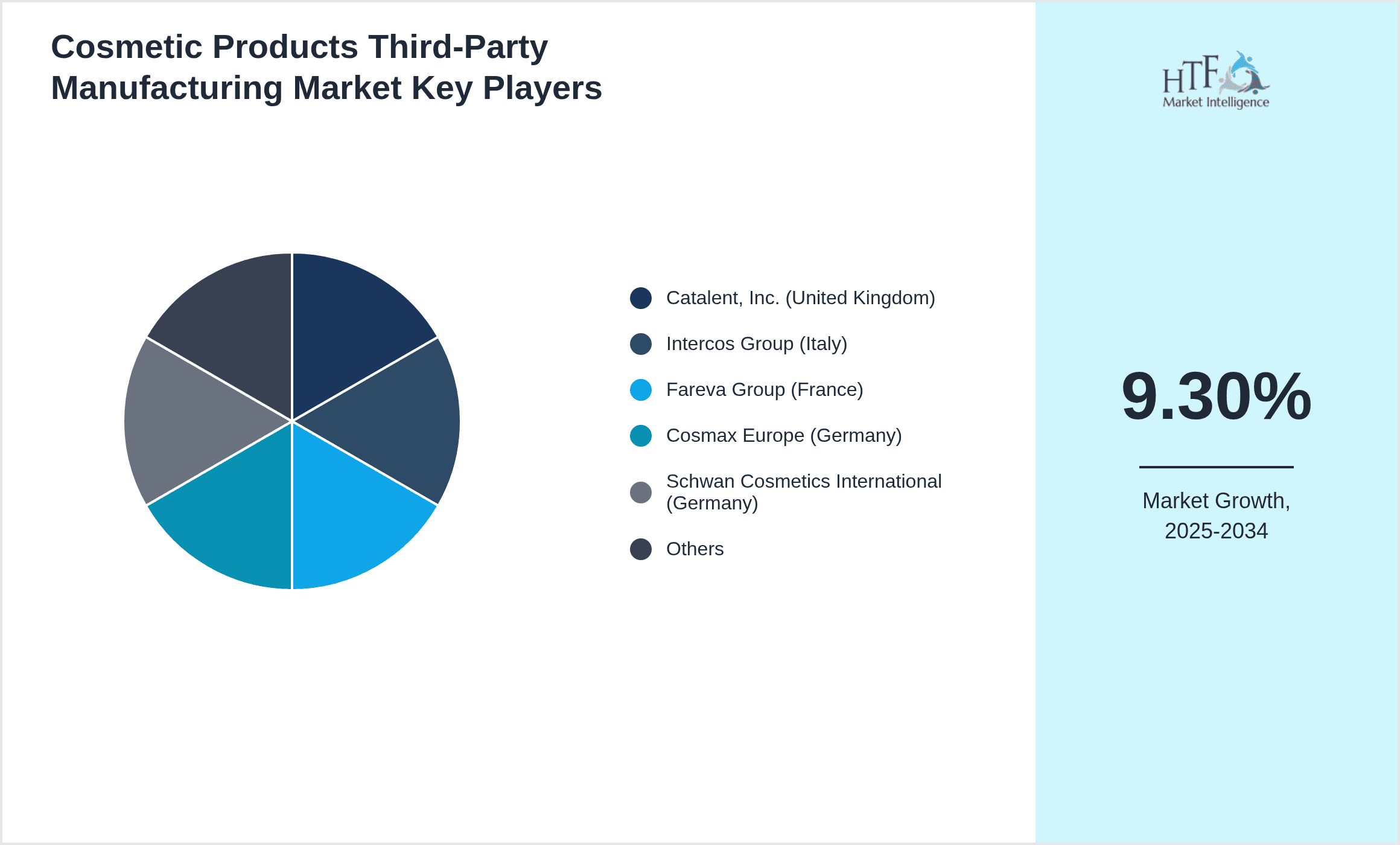

Leading Companies in Cosmetic Products Third-Party Manufacturing Market

- •Catalent, Inc. (United Kingdom)

- •Intercos Group (Italy)

- •Fareva Group (France)

- •Cosmax Europe (Germany)

- •Schwan Cosmetics International (Germany)

- •Sederma (France)

- •Mibelle Group (Switzerland)

- •HCT Group (France)

- •Cosmetica Swiss (Switzerland)

- •Azelis Group (Belgium)

- •BASF Personal Care and Nutrition GmbH (Germany)

- •Givaudan Active Beauty (Switzerland)

- •Mane SA (France)

- •Lubrizol Advanced Materials Europe (France)

- •Symrise AG (Germany)

- •Coptis (France)

- •L’Oréal Active Cosmetics Division (France)

- •Seppic SAS (France)

- •Brenntag AG (Germany)

- •Croda International Plc (United Kingdom)

- •Evonik Industries AG (Germany)

- •Lubrizol Life Science Europe (France)

- •KDC/ONE Europe (France)

- •Albea Group (France)

- •Tereos Syral (France)

Market Breakdown

- •By Type

- ◦Contract Manufacturing

- ◦Private Label Manufacturing

- ◦OEM Manufacturing

- ◦ODM Manufacturing

- ◦Others

- •By Application

- ◦Skincare

- ◦Haircare

- ◦Color Cosmetics

- ◦Fragrances

- ◦Personal Care

- •By End-User Channel

- ◦Luxury Brands

- ◦Mass Market Brands

- ◦Indie Brands

- ◦E-commerce Brands

- •By Distribution Channel

- ◦Retail Stores

- ◦Online Platforms

- ◦Pharmacies & Drugstores

- ◦Specialty Stores

Growth Dynamics

- •The Europe cosmetic products third-party manufacturing market is propelled by rising consumer demand for personalized and innovative cosmetic formulations, driving brands to outsource production to specialized manufacturers. Increasing awareness of clean and sustainable beauty significantly fuels market expansion, as third-party manufacturers invest in eco-friendly ingredients and green technologies to meet regulatory and consumer expectations. Moreover, the surge in e-commerce channels and indie brand emergence creates a growing need for flexible and scalable manufacturing solutions. Market growth is supported by stringent regulatory frameworks in Europe, which third-party manufacturers adeptly navigate, ensuring product safety and compliance. The increasing preference for premiumization and natural ingredients also encourages brands to collaborate with expert manufacturers to enhance product efficacy and appeal. Overall, the market benefits from technological advancements in formulation and packaging, enabling rapid innovation and reduced time-to-market for new cosmetic products.

- •Trends in the Europe cosmetic third-party manufacturing market highlight a shift towards sustainable and clean beauty practices, with manufacturers adopting biodegradable packaging and natural raw materials. Digital transformation, including Industry 4.0 technologies such as automation, AI-driven formulation, and smart manufacturing, is enhancing production efficiency and quality control. The rise of private label cosmetics, driven by retailer demand for exclusive products, is reshaping manufacturing portfolios. Additionally, the growing influence of social media and influencer marketing accelerates product lifecycle, requiring agile manufacturing responses. There is also an increased focus on transparency and traceability within the supply chain, promoting consumer trust. Furthermore, the market witnesses integration of biotechnology and novel active ingredients, reflecting innovation trends. These evolving consumer preferences and technological advancements are reshaping the third-party manufacturing landscape, fostering competitive differentiation and growth opportunities.

- •Restraints impacting the Europe cosmetic products third-party manufacturing market include stringent regulatory compliance requirements that increase operational complexity and costs for manufacturers. High capital investment in advanced manufacturing facilities and R&D limits entry for smaller players and constrains scalability. Supply chain disruptions, especially for natural and specialty ingredients, pose challenges to consistent production and timely delivery. Price sensitivity among mass-market brands pressures manufacturers to optimize costs without compromising quality. Additionally, intense competition among established players creates margin pressures and necessitates continuous innovation. Environmental concerns and sustainability mandates require ongoing adaptation of processes, which can incur additional expenses. Furthermore, geopolitical uncertainties and trade regulations within Europe may affect cross-border manufacturing and logistics. These factors collectively restrain rapid growth and demand strategic management by third-party manufacturers.

- •Opportunities in the Europe cosmetic products third-party manufacturing market are abundant, driven by the proliferation of indie and niche brands seeking specialized and flexible manufacturing partners. The growing demand for vegan, organic, and ethically sourced cosmetic products opens avenues for dedicated contract manufacturers focused on clean beauty. Expansion into emerging European markets with rising disposable incomes offers untapped potential. Technological advancements such as 3D printing and personalized formulation analytics provide innovative pathways for product differentiation. Collaborations between ingredient suppliers, technology firms, and manufacturers can accelerate product development cycles and enhance competitive advantage. Furthermore, increasing consumer preference for customization and on-demand production models creates opportunities for agile manufacturing solutions. Regulatory support for sustainability and safety compliance also encourages investment in green manufacturing technologies, fostering long-term growth prospects.

- •Challenges confronting the Europe cosmetic products third-party manufacturing market include navigating the complex and evolving regulatory landscape governing cosmetic safety, labeling, and environmental compliance, which demands continuous updates and certifications. The scarcity of skilled workforce specialized in cosmetic formulation and manufacturing technologies limits operational expansion. Managing supply chain volatility, particularly for rare natural ingredients, affects production reliability. Maintaining cost competitiveness while adhering to high-quality standards and sustainability expectations presents ongoing difficulties. The market also faces risks related to intellectual property protection and confidentiality, crucial for brands outsourcing innovation. Additionally, balancing customization demands with efficient mass production requires advanced manufacturing capabilities. Lastly, geopolitical tensions and economic instabilities in certain European regions may disrupt manufacturing operations and logistics, adding layers of uncertainty to market growth.

Market Trends

- •One prevailing trend in the Europe cosmetic products third-party manufacturing market is the accelerated adoption of sustainable manufacturing practices, including use of renewable energy, biodegradable packaging, and eco-friendly raw materials. This aligns with consumer demand for responsible beauty products and regulatory pressures. Manufacturers are increasingly investing in green chemistry and waste reduction technologies to minimize environmental impact while enhancing brand reputation. This trend is reshaping supply chains and operational priorities across the region.

- •Another significant trend is the integration of digital technologies such as automation, AI-driven quality control, and data analytics within manufacturing processes. These advancements improve production efficiency, reduce errors, and enable rapid customization, allowing manufacturers to meet the fast-evolving demands of cosmetic brands. Industry 4.0 adoption is fostering smart manufacturing environments, enhancing competitiveness in Europe.

- •The rise of private label and indie cosmetic brands is reshaping manufacturing demand, with third-party providers offering tailored services to support smaller volumes and niche formulations. This diversification drives innovation and broadens market accessibility. E-commerce growth further accelerates this trend, as direct-to-consumer brands seek agile production partners to maintain rapid product launch cycles.

- •Consumers’ increasing preference for transparency and traceability is leading manufacturers to implement advanced supply chain tracking systems. Blockchain and digital certification technologies are gaining traction, enabling verification of ingredient sourcing and manufacturing processes, which enhances consumer trust and regulatory compliance.

- •Emerging biotechnology applications in cosmetic ingredient development, such as fermentation-derived actives and synthetic biology, are influencing formulation innovation. Third-party manufacturers are collaborating with biotech firms to integrate these novel ingredients, offering differentiated, high-performance products aligned with clean beauty standards.

Market Opportunities

- •The growing demand for personalized and customized cosmetic products in Europe presents substantial opportunities for third-party manufacturers to develop flexible production capabilities. Brands are increasingly seeking bespoke formulations tailored to individual consumer needs, driving investments in modular manufacturing systems and advanced analytics to support personalization at scale.

- •Expansion into emerging European markets such as Eastern Europe and the Nordic countries offers significant growth potential. Rising disposable incomes and increasing beauty awareness in these regions are creating new consumer bases, encouraging manufacturers to establish localized production facilities and partnerships to better serve these markets.

- •Investments in sustainable and clean beauty manufacturing technologies open avenues for differentiation and compliance with stringent European regulations. Manufacturers adopting green chemistry, renewable energy, and waste reduction processes can capitalize on growing consumer preference for eco-friendly products and brand loyalty.

- •Collaboration with biotechnology companies to incorporate novel, bioactive ingredients into cosmetic formulations presents opportunities for product innovation. These partnerships enable manufacturers to offer cutting-edge solutions that meet consumer demand for efficacy and naturalness.

- •The surge in digital transformation and Industry 4.0 adoption allows manufacturers to enhance operational efficiency, reduce costs, and accelerate product development cycles. Embracing automation and data analytics can improve scalability and responsiveness to market trends.

- •The increasing popularity of private label cosmetics among retailers and e-commerce players creates demand for specialized manufacturing services. Third-party providers can leverage this trend by offering tailored solutions for small-batch and rapid-turnaround production.

- •Opportunities also exist in expanding service portfolios to include packaging, regulatory consulting, and logistics support, offering end-to-end solutions that attract a broader client base and enhance customer retention.

Market Challenges

- •Navigating the complex and evolving regulatory landscape governing cosmetic products in Europe remains a major challenge for third-party manufacturers. Compliance with regulations such as the EU Cosmetic Regulation (EC) No 1223/2009 requires continuous monitoring and adaptation, increasing operational costs and complexity.

- •The high capital investment required for state-of-the-art manufacturing facilities and R&D capabilities limits market entry for smaller players and constrains scalability for mid-sized firms. This financial barrier hampers innovation and market diversification.

- •Supply chain vulnerabilities, especially for sourcing natural and specialty ingredients, pose significant risks. Disruptions due to geopolitical tensions, climate change, and logistics challenges can lead to production delays and increased costs, affecting market reliability.

- •Maintaining cost competitiveness while adhering to stringent quality and sustainability standards is difficult amid intense market competition. Manufacturers must balance pricing pressures from mass-market clients with investments in eco-friendly and innovative processes.

- •Talent shortages with expertise in cosmetic science, formulation, and advanced manufacturing technologies limit operational expansion and innovation capacity. Attracting and retaining skilled professionals remains a persistent challenge.

- •Protecting intellectual property and maintaining confidentiality for proprietary formulations is critical but challenging, especially when collaborating with multiple brands and partners. Breaches can undermine competitive advantage and client trust.

- •Regional economic and political uncertainties within Europe, including trade policy shifts and regulatory changes, contribute to market instability and complicate long-term strategic planning for manufacturers.

Regulatory Framework

- •Between 2019 and 2024, the Europe Cosmetic Products Third-Party Manufacturing Market has been shaped by the ongoing enforcement of the EU Cosmetic Regulation (EC) No 1223/2009, which mandates rigorous safety assessments, ingredient restrictions, and labeling requirements. This regulation ensures consumer safety and product transparency but requires manufacturers to maintain detailed technical documentation and adhere to strict notification procedures. Compliance impacts formulation flexibility and manufacturing timelines, influencing market dynamics.

- •Additional regulations such as the Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) framework have imposed stricter controls on chemical substances used in cosmetics, compelling manufacturers to reformulate products and source safer alternatives. Enforcement mechanisms include regular inspections and penalties for non-compliance, affecting operational practices.

- •Environmental directives focusing on waste management, packaging recyclability, and emissions reduction have influenced manufacturers to adopt sustainable production methods and innovative packaging solutions. These requirements align with the European Green Deal objectives and consumer expectations for eco-friendly products.

- •Country-specific mandates, notably in Germany and France, have introduced additional labeling and ingredient disclosure norms, including mandatory notification of nanomaterials and allergen information. These regional regulations require localized compliance efforts by manufacturers operating in multiple European countries.

- •Government initiatives supporting innovation and sustainability in the cosmetic sector include funding programs for green technologies and research collaborations. These policies encourage the development of safe, natural, and sustainable cosmetic products, shaping manufacturing trends and investment priorities.

Market Intelligence

- •15th February 2024, Fareva Group announced the launch of a new eco-friendly production facility in France, designed to support sustainable cosmetic manufacturing with reduced carbon footprint and enhanced waste management systems. This state-of-the-art plant aims to meet rising demand for green beauty products in Europe and supports Fareva’s commitment to environmental responsibility. The facility incorporates advanced automation and quality control technologies to ensure product consistency and regulatory compliance, enabling faster time-to-market for client brands. Source: Fareva Official Press Release.

- •10th October 2024, Intercos Group unveiled its innovative AI-powered formulation platform that accelerates cosmetic product development by analyzing consumer preferences and regulatory constraints. This technology facilitates rapid prototyping and customization, allowing brands to quickly adapt to market trends. The platform integrates seamlessly with manufacturing operations to enhance efficiency and reduce development costs, positioning Intercos as a leader in digital transformation within the European third-party manufacturing sector. Source: Intercos Corporate News.

- •22nd January 2025, Catalent, Inc. expanded its European manufacturing footprint by acquiring a specialty cosmetics production facility in the United Kingdom. This strategic move enhances Catalent’s capacity to serve premium skincare and haircare brands with flexible contract manufacturing solutions. The acquisition includes advanced GMP-certified laboratories and pilot plants, facilitating innovation and quality assurance across product lines. This expansion supports Catalent’s growth strategy in the European market amid increasing demand for outsourced cosmetic production. Source: Catalent Press Release.

- •5th March 2025, Cosmax Europe partnered with a leading biotech firm to integrate fermentation-derived active ingredients into cosmetic formulations. This collaboration focuses on developing sustainable and high-efficacy skincare products, aligning with the clean beauty trend. The partnership leverages Cosmax’s manufacturing expertise and the biotech company’s innovative ingredient portfolio to accelerate product development and market entry in Europe. This strategic alliance enhances Cosmax’s competitive positioning in the rapidly evolving cosmetic sector. Source: Cosmax Europe Corporate Announcement.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 15.7 Billion |

| Forecast Year Market Size | USD 38.9 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.3% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Catalent, Inc. (United Kingdom), Intercos Group (Italy), Fareva Group (France), Cosmax Europe (Germany), Schwan Cosmetics International (Germany), Sederma (France), Mibelle Group (Switzerland), HCT Group (France), Cosmetica Swiss (Switzerland), Azelis Group (Belgium), BASF Personal Care and Nutrition GmbH (Germany), Givaudan Active Beauty (Switzerland), Mane SA (France), Lubrizol Advanced Materials Europe (France), Symrise AG (Germany), Coptis (France), L’Oréal Active Cosmetics Division (France), Seppic SAS (France), Brenntag AG (Germany), Croda International Plc (United Kingdom), Evonik Industries AG (Germany), Lubrizol Life Science Europe (France), KDC/ONE Europe (France), Albea Group (France), Tereos Syral (France) |

Europe Cosmetic Products Third-Party Manufacturing Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.