China Computing Platform for Automated Driving Market Size, Growth & Revenue 2024-2034

China Computing Platform for Automated Driving Market is segmented by Computing Platform Type (Hardware Computing Platforms (High-performance Processors, GPUs, ASICs), Software Computing Platforms (Middleware, AI Frameworks, Operating Systems), Cloud Computing Platforms (Remote Data Processing and Storage), Edge Computing Platforms (On-vehicle Real-time Data Processing), Hybrid Computing Platforms (Integrated Hardware-Software Solutions)), Application Segment (Advanced Driver Assistance Systems (ADAS), Autonomous Navigation, Fleet Management Systems, In-vehicle Infotainment, Vehicle Safety & Security Systems), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Shared Mobility Vehicles), Deployment Model (On-vehicle Embedded Systems, Cloud-based Platforms, Edge Computing Deployment), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Computing Platform for Automated Driving Market is defined by its comprehensive offerings of computing solutions that facilitate the development and deployment of automated driving technologies. This market includes various platform types such as hardware computing units, software stacks, cloud and edge computing solutions, and hybrid platforms that combine these technologies to optimize performance. These platforms support applications including Advanced Driver Assistance Systems (ADAS), autonomous navigation, fleet management, in-vehicle infotainment, and vehicle safety systems. The market is bound within China’s automotive and technology landscape, focusing on meeting the country’s regulatory, technological, and consumer demands for intelligent and automated mobility. Key industry participants include OEMs, tier-1 automotive suppliers, semiconductor manufacturers, software developers, and cloud service providers, all collaborating to advance autonomous driving capabilities. The market's primary use cases revolve around enhancing driver safety, reducing traffic accidents, and improving vehicle operational efficiency, thus playing a strategic role in China’s smart transportation initiatives and automotive innovation ecosystem.

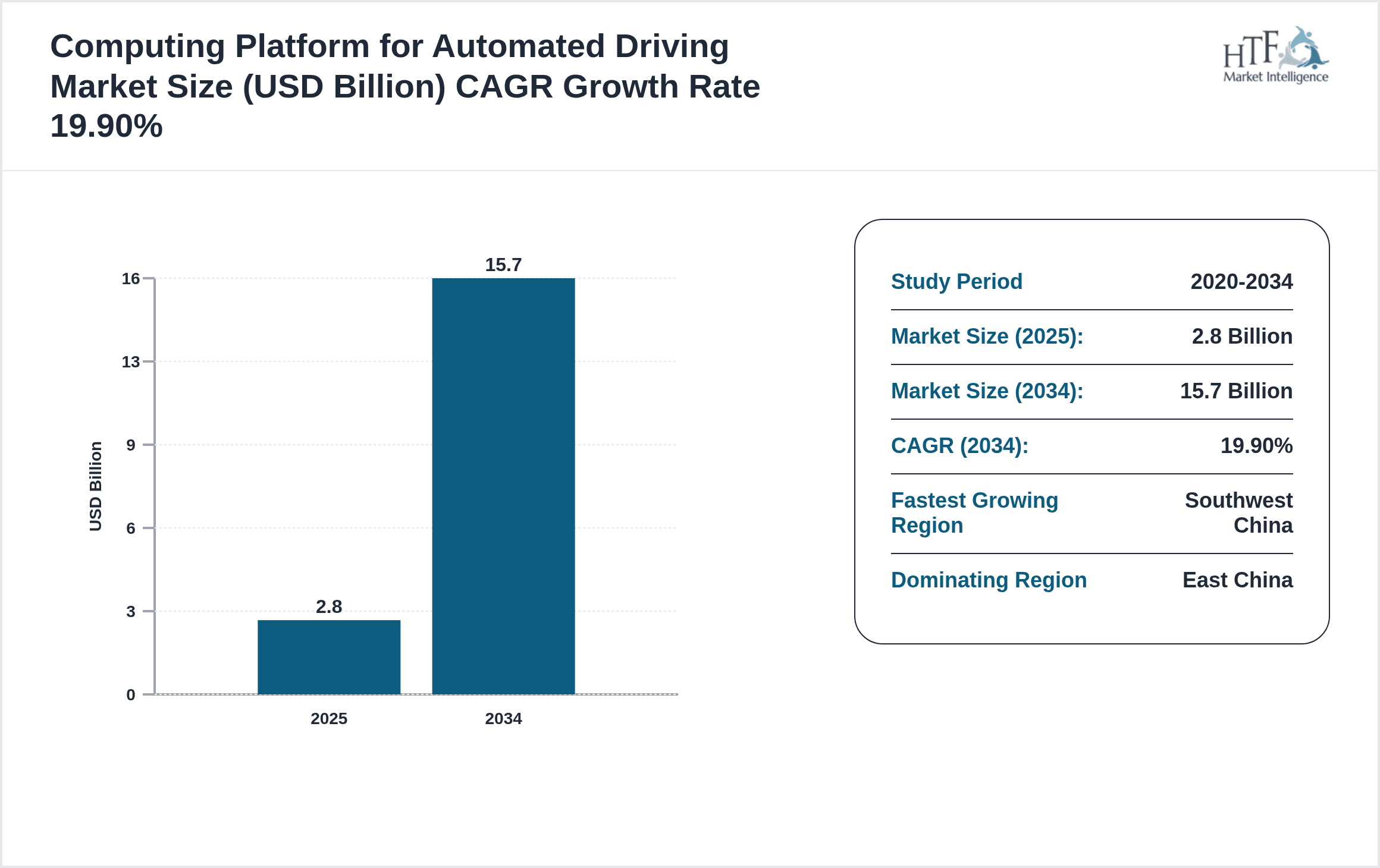

- •Key highlights of the market include a base size of USD 2.8 Billion in 2024, with projections reaching USD 15.7 Billion by 2034, reflecting a robust CAGR of 19.9%. The hardware computing platforms segment currently dominates, driven by demand for high-performance processors capable of real-time data processing. The East China region leads in market share due to its concentration of automotive manufacturing hubs and technology centers. Meanwhile, Southwest China emerges as the fastest-growing sub-region, fueled by regional government initiatives and growing adoption of edge computing solutions. The market growth is supported by increasing investments in AI, sensor integration, and 5G connectivity for vehicle-to-everything (V2X) communication, which enhance automated driving capabilities.

- •The value proposition of the China computing platform for automated driving market lies in its ability to enable safer, more efficient, and smarter vehicles, which appeal to automotive manufacturers, technology firms, and consumers alike. Its strategic importance is underscored by the Chinese government’s support through regulations, funding, and infrastructure development aimed at fostering autonomous vehicle adoption. The platforms provide critical computational resources that power AI algorithms, sensor fusion, and real-time decision-making, thereby transforming the transportation sector and contributing to urban mobility solutions. Stakeholders benefit from collaborations across automotive, semiconductor, and software sectors, creating a dynamic ecosystem that accelerates innovation and market penetration within China’s rapidly evolving automotive landscape.

Competitive Landscape

Competition in the China Computing Platform for Automated Driving Market is intensely driven by technological innovation, strategic partnerships, and a race to establish market leadership in a rapidly evolving industry. Established automotive suppliers and semiconductor companies leverage their expertise to develop high-performance hardware platforms optimized for automated driving workloads. Concurrently, software developers and cloud providers focus on scalable, AI-enabled computing solutions that support complex autonomous driving algorithms. Market rivalry is characterized by continuous R&D investments, aggressive patent portfolios, and collaborations between technology firms and automotive OEMs to co-develop integrated platforms. Pricing strategies balance between affordability and advanced feature sets, while regional players capitalize on local market knowledge and government incentives. Distribution channels increasingly emphasize direct OEM collaborations and ecosystem-based approaches incorporating sensor manufacturers and telecom providers. The competitive landscape also sees mergers, acquisitions, and joint ventures shaping market consolidation, with future trends likely to center on edge computing integration, AI acceleration, and the convergence of cloud and on-vehicle computing to meet real-time processing requirements.

Leading Companies in China Computing Platform for Automated Driving Market

- •Huawei Technologies Co., Ltd. (China)

- •Baidu, Inc. (China)

- •Tencent Holdings Ltd. (China)

- •Alibaba Group Holding Limited (China)

- •NVIDIA Corporation (United States)

- •Intel Corporation (United States)

- •Xilinx, Inc. (United States)

- •Mobileye N.V. (Israel)

- •Valeo SA (France)

- •Bosch Group (Germany)

- •Denso Corporation (Japan)

- •Continental AG (Germany)

- •Aptiv PLC (Ireland)

- •Renesas Electronics Corporation (Japan)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Xiaomi Corporation (China)

- •SenseTime Group Limited (China)

- •Pony.ai (China)

- •NavInfo Co., Ltd. (China)

- •Horizon Robotics (China)

- •Zhejiang Dahua Technology Co., Ltd. (China)

- •DeepRoute.ai (China)

- •AutoX Technologies (China)

- •Neusoft Corporation (China)

- •Inceptio Technology (China)

Market Breakdown

- •By Computing Platform Type

- ◦Hardware Computing Platforms (High-performance Processors, GPUs, ASICs)

- ◦Software Computing Platforms (Middleware, AI Frameworks, Operating Systems)

- ◦Cloud Computing Platforms (Remote Data Processing and Storage)

- ◦Edge Computing Platforms (On-vehicle Real-time Data Processing)

- ◦Hybrid Computing Platforms (Integrated Hardware-Software Solutions)

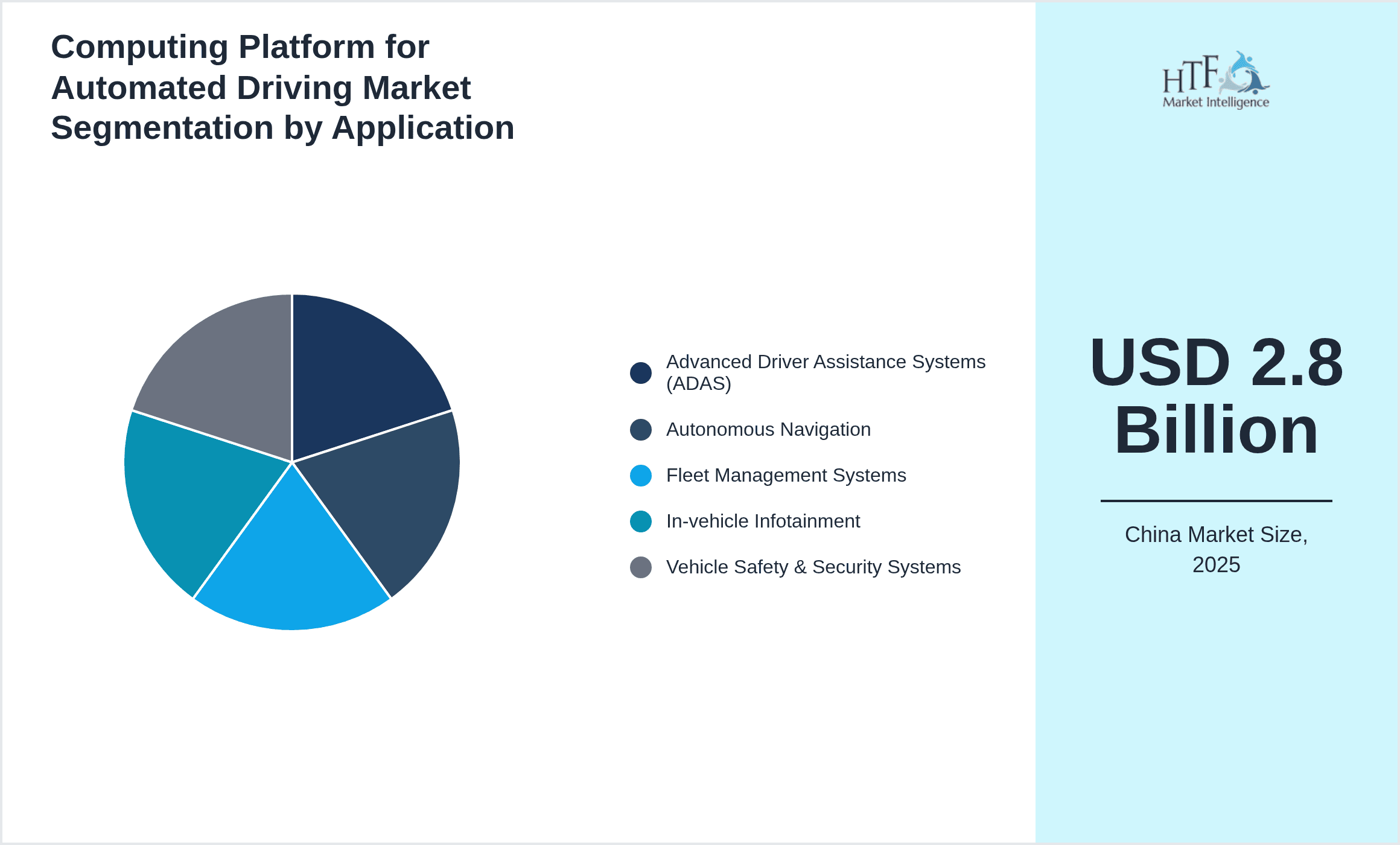

- •By Application Segment

- ◦Advanced Driver Assistance Systems (ADAS)

- ◦Autonomous Navigation

- ◦Fleet Management Systems

- ◦In-vehicle Infotainment

- ◦Vehicle Safety & Security Systems

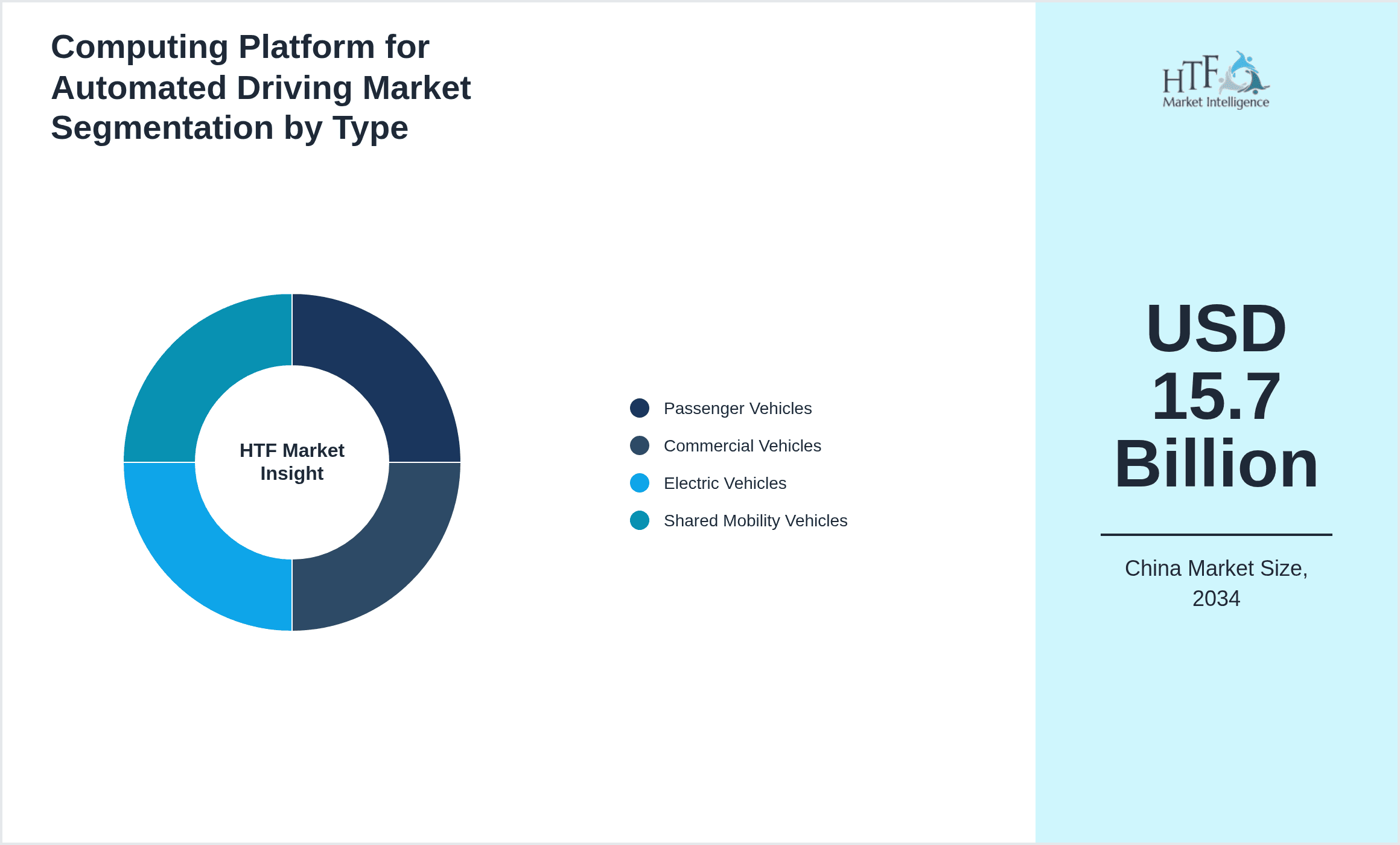

- •By Vehicle Type

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Shared Mobility Vehicles

- •By Deployment Model

- ◦On-vehicle Embedded Systems

- ◦Cloud-based Platforms

- ◦Edge Computing Deployment

Growth Dynamics

- •China’s expanding automotive industry, backed by governmental support for autonomous vehicle development, is a primary growth driver. Investments in infrastructure, AI research, and 5G connectivity enhance the capabilities and adoption rate of computing platforms. The rise in demand for safer, driverless cars across urban centers stimulates platform innovation. Furthermore, collaborations between tech giants and OEMs accelerate solution deployment, while consumer acceptance of smart mobility fuels market expansion. These combined factors significantly boost the computing platform market’s trajectory in China.

- •The increasing integration of AI and machine learning into computing platforms is driving market sophistication. Edge computing adoption allows real-time processing closer to vehicle sensors, reducing latency and improving safety. This trend is supported by advancements in semiconductor technology and cloud-edge hybrid architectures. Additionally, the need for processing vast sensor data (LiDAR, radar, cameras) strengthens demand for high-performance computing hardware and optimized software frameworks, further supporting market growth.

- •Rising regulatory emphasis on vehicle safety standards and autonomous driving testing frameworks in China incentivizes compliance through advanced computing platforms. Government mandates on data security and communication protocols foster development of secure, reliable platforms. These regulations encourage manufacturers to adopt certified computing solutions, enhancing market demand. Moreover, pilot programs in smart cities and designated autonomous zones provide practical deployment opportunities, accelerating market momentum.

- •Consumer preferences shifting towards connected and autonomous driving experiences underpin growth. The proliferation of electric vehicles (EVs) and shared mobility services necessitates robust computing platforms to manage complex operations and data flows. Increasing urbanization and traffic congestion drive demand for autonomous fleet management solutions, expanding market applications. This consumer-driven evolution encourages platform providers to innovate features enhancing user experience and operational efficiency.

- •Strategic partnerships among automotive OEMs, semiconductor manufacturers, and cloud providers catalyze market growth. Joint ventures and collaborative R&D initiatives enable integration of cutting-edge technologies into computing platforms. Government incentives for innovation and technology incubation further stimulate market activity. The establishment of industry standards and open platforms promotes interoperability, facilitating faster adoption and scalability of automated driving computing solutions across China.

Market Trends

- •The growing trend of AI-powered edge computing in automated driving platforms is transforming data processing by enabling real-time analytics directly on vehicles. This shift reduces dependency on cloud connectivity, improves response times, and enhances safety. China’s leading tech firms are pioneering edge AI chips tailored for automotive applications, driving market innovation.

- •Integration of 5G connectivity is becoming widespread, facilitating seamless vehicle-to-everything (V2X) communication. This advancement supports cooperative autonomous driving and remote diagnostics, creating new opportunities for computing platform providers to offer connected solutions aligned with smart city initiatives.

- •Collaborative ecosystems among automakers, technology developers, and telecom operators are emerging as a strategic trend. These partnerships focus on co-developing standardized computing platforms that reduce development costs and accelerate time-to-market, with notable pilots underway in major Chinese metropolitan areas.

- •There is increasing adoption of hybrid computing architectures combining cloud, edge, and on-vehicle resources to optimize performance and scalability. This trend enhances computational efficiency and supports complex autonomous driving functions requiring diverse data workflows.

- •Sustainability considerations are influencing platform designs, with a focus on energy-efficient processors and low-power computing modules. This aligns with China’s environmental policies and automotive electrification goals, driving innovation in computing hardware.

- •The rise of software-defined vehicles is reshaping platform development priorities, emphasizing modular, upgradable software computing stacks that support continuous feature enhancements and over-the-air updates, thereby extending vehicle lifecycle and enhancing user experience.

- •Increased consumer demand for personalized in-vehicle infotainment and safety features is pushing platform providers to integrate multi-modal sensor fusion and advanced AI algorithms, enabling richer user interfaces and predictive safety mechanisms.

Market Opportunities

- •Expanding autonomous taxi and shared mobility services in China present significant opportunities for computing platform providers to supply scalable, reliable platforms tailored for fleet operations. These segments require robust data management and real-time decision-making capabilities, offering substantial growth potential.

- •The development of regional autonomous driving pilot zones, especially in Southwest and Central China, offers fertile ground for platform testing, refinement, and commercialization. Providers can capitalize on government incentives and localized demand to accelerate market penetration.

- •Integration of AI with advanced sensor suites opens avenues for platforms that enable higher levels of vehicle autonomy. Investment in AI chip development and algorithm optimization tailored to China-specific driving environments is an emerging opportunity for technology leaders.

- •Partnerships with telecom operators to leverage 5G networks for enhanced V2X communication create new service models for computing platforms, including cloud-edge synergy and remote vehicle management, broadening revenue streams.

- •Growing demand for cybersecurity features within automated driving platforms presents opportunities for providers specializing in secure computing architectures, data encryption, and intrusion detection tailored to automotive applications.

- •The trend toward software-defined vehicles allows platform developers to offer subscription-based services and continuous software upgrades, creating recurring revenue models and deeper customer engagement.

- •Emerging markets within China’s tier 2 and tier 3 cities are underserved in automated driving platform deployment, representing untapped customer segments and growth potential for innovative, cost-effective solutions.

Market Challenges

- •High development and production costs for advanced computing platforms limit the accessibility for smaller automotive manufacturers, constraining widespread adoption across diverse vehicle segments within China. Balancing cost and performance remains a critical challenge.

- •Complex regulatory environment with evolving safety and data privacy standards creates uncertainty for platform developers. Ensuring compliance while maintaining innovation agility requires significant resource allocation and expertise.

- •The fragmented nature of China’s automotive supply chain, with multiple competing standards and proprietary technologies, complicates platform interoperability and integration, slowing down market consolidation and scalability.

- •Shortage of skilled talent in AI, semiconductor design, and automotive software development poses a bottleneck for rapid product development and deployment within China’s competitive landscape.

- •Security vulnerabilities specific to connected and autonomous vehicles expose platforms to cyber threats, requiring robust defense mechanisms that are still underdeveloped in many Chinese offerings.

- •Rapid technological obsolescence due to fast-paced innovation cycles pressures companies to continuously invest in R&D, increasing operational risks and financial strain, especially for emerging players.

- •Consumer skepticism and limited awareness about automated driving safety and benefits in certain regions of China slow adoption rates, impacting market growth projections and product acceptance.

Regulatory Framework

- •Between 2019 and 2024, China implemented the Autonomous Vehicle Road Testing Regulation, mandating stringent safety standards and obtaining government permits for autonomous driving trials. This framework ensures controlled deployment and guides platform development to meet national safety benchmarks.

- •China’s Cybersecurity Law, enforced from 2021, requires automotive computing platforms to adhere to strict data protection and network security protocols, compelling manufacturers to integrate robust encryption and threat detection capabilities within their systems.

- •The Ministry of Industry and Information Technology (MIIT) introduced guidelines in 2022 for vehicle-to-everything (V2X) communication standards, promoting interoperability and data exchange security between vehicles and infrastructure, influencing platform design requirements.

- •Regional governments, notably in East and South China, established pilot zones with localized regulations supporting autonomous vehicle testing and commercial deployment, providing regulatory clarity and incentives for platform providers in these sub-regions.

- •Ongoing updates to China’s National Intelligent Connected Vehicle Standardization framework, released periodically since 2020, set technical specifications for computing platforms, sensor integration, and AI algorithm transparency, fostering industry alignment and innovation.

Market Intelligence

- •15th January 2025, Huawei Technologies Co., Ltd. launched its latest edge AI computing platform optimized for autonomous vehicles, featuring enhanced processing power and energy efficiency. The platform supports complex sensor fusion and real-time decision-making, targeting passenger and commercial fleets within China. This launch underscores Huawei’s commitment to expanding its footprint in automotive computing and aligns with China’s push for autonomous driving adoption. The platform integrates 5G capabilities, enabling seamless V2X communication and cloud-edge synergy, positioning Huawei as a key innovator in the market. Source: Huawei Official Press Release

- •10th March 2025, Baidu, Inc. introduced an upgraded software computing platform for its Apollo autonomous driving system, incorporating advanced AI algorithms and enhanced cybersecurity features. This upgrade aims to improve navigation accuracy and system resilience against cyber threats, facilitating broader deployment across China’s urban and highway environments. Baidu’s initiative reflects growing emphasis on software-defined vehicle architectures and regulatory compliance within the market. The platform supports over-the-air updates, enabling continuous feature improvements and responsiveness to evolving regulatory requirements. Source: Baidu Corporate Announcement

- •22nd February 2025, NVIDIA Corporation announced a strategic partnership with Chinese automaker Xpeng Motors to co-develop high-performance hardware computing platforms for next-generation electric autonomous vehicles. The collaboration focuses on integrating NVIDIA’s AI acceleration technology with Xpeng’s vehicle systems to enhance autonomous capabilities and reduce processing latency. This partnership is expected to accelerate deployment of Level 4 autonomous vehicles in China, leveraging combined expertise in hardware and software. The initiative aligns with China’s objectives to lead in smart vehicle innovation and sustainable transportation. Source: NVIDIA Press Release

- •5th April 2025, Horizon Robotics unveiled a new hybrid computing platform combining edge and cloud processing tailored for commercial autonomous fleets. The platform emphasizes scalability, low latency, and AI-powered operational insights, addressing the needs of China’s rapidly growing logistics and transportation sectors. This launch positions Horizon Robotics as a significant player in the market by offering flexible deployment models and enhanced computational efficiency. The solution supports integration with existing fleet management systems, facilitating swift adoption. Source: Horizon Robotics Official Statement

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.8 Billion |

| Forecast Year Market Size | USD 15.7 Billion |

| CAGR | 19.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 19.3% |

| Scope of Report | Market is segmented by Computing Platform Type (Hardware Computing Platforms (High-performance Processors, GPUs, ASICs), Software Computing Platforms (Middleware, AI Frameworks, Operating Systems), Cloud Computing Platforms (Remote Data Processing and Storage), Edge Computing Platforms (On-vehicle Real-time Data Processing), Hybrid Computing Platforms (Integrated Hardware-Software Solutions)), Application Segment (Advanced Driver Assistance Systems (ADAS), Autonomous Navigation, Fleet Management Systems, In-vehicle Infotainment, Vehicle Safety & Security Systems), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Shared Mobility Vehicles), Deployment Model (On-vehicle Embedded Systems, Cloud-based Platforms, Edge Computing Deployment) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Huawei Technologies Co., Ltd. (China), Baidu, Inc. (China), Tencent Holdings Ltd. (China), Alibaba Group Holding Limited (China), NVIDIA Corporation (United States), Intel Corporation (United States), Xilinx, Inc. (United States), Mobileye N.V. (Israel), Valeo SA (France), Bosch Group (Germany), Denso Corporation (Japan), Continental AG (Germany), Aptiv PLC (Ireland), Renesas Electronics Corporation (Japan), Samsung Electronics Co., Ltd. (South Korea), Xiaomi Corporation (China), SenseTime Group Limited (China), Pony.ai (China), NavInfo Co., Ltd. (China), Horizon Robotics (China), Zhejiang Dahua Technology Co., Ltd. (China), DeepRoute.ai (China), AutoX Technologies (China), Neusoft Corporation (China), Inceptio Technology (China) |

China Computing Platform for Automated Driving Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.