EMEA Integrated Visual Augmentation System Market - Europe Size & Outlook 2025-2034

EMEA Integrated Visual Augmentation System Market is segmented by Type (Head-Mounted Displays, Smart Glasses, Retinal Projection Systems, Contact Lens Displays, Handheld Devices), Application (Military & Defense, Healthcare, Industrial Manufacturing, Consumer Electronics, Automotive), Deployment Model (On-Premise, Cloud-Based, Hybrid), End-User Industry (Defense Forces, Hospitals & Clinics, Manufacturing Plants, Retail & Entertainment, Automotive OEMs), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

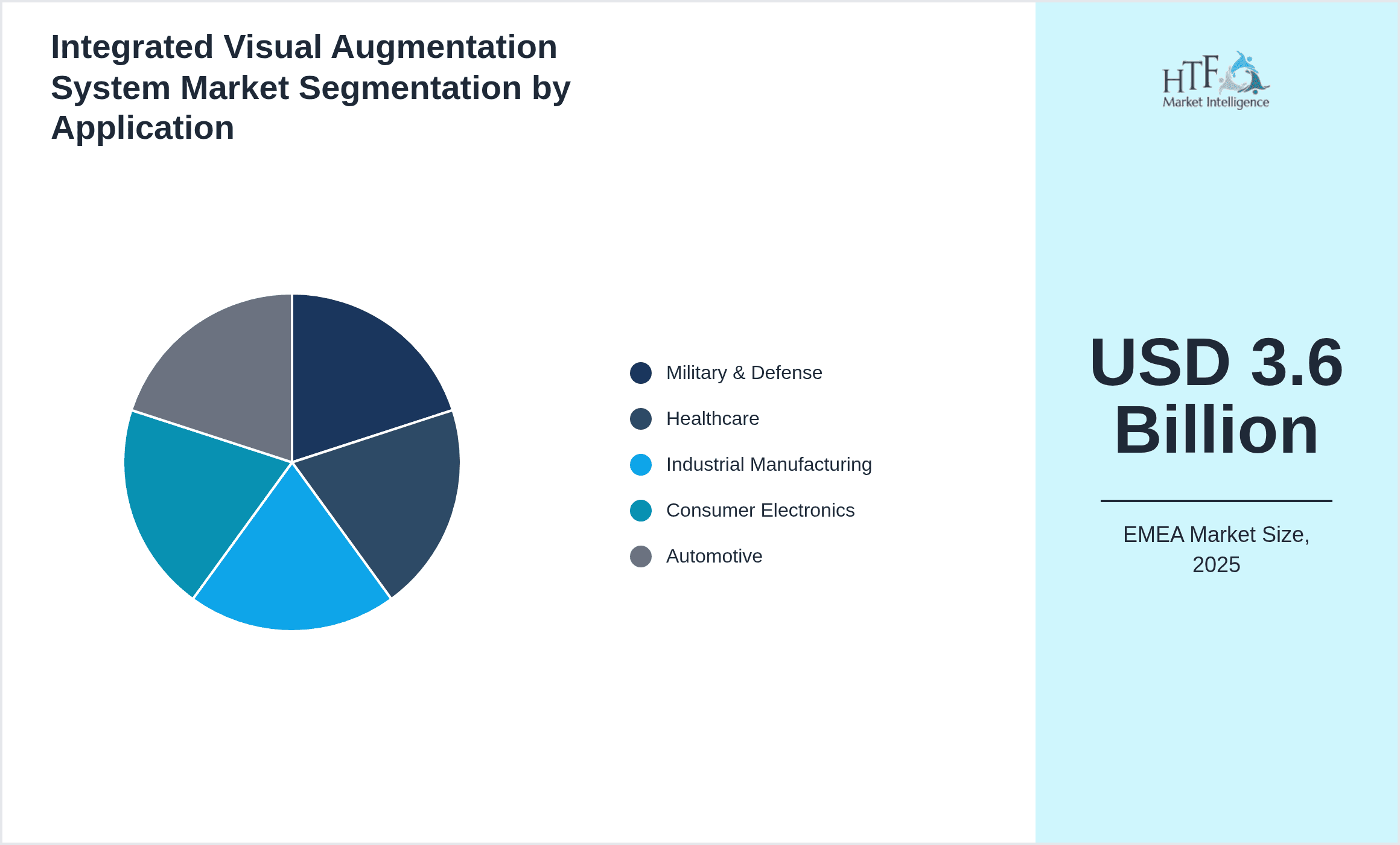

- •The EMEA Integrated Visual Augmentation System Market is a rapidly evolving sector focused on technologies that enhance user perception and interaction through augmented reality and visual overlay devices. These systems comprise a broad portfolio including head-mounted displays, smart glasses, retinal projection systems, contact lens displays, and handheld devices, all designed to deliver real-time enhanced visual inputs. Serving key sectors such as military & defense, healthcare, industrial manufacturing, consumer electronics, and automotive, the market integrates advanced hardware and software solutions for improved operational efficiency, safety, and decision-making capabilities. The demand is driven by technological advancements in AR, AI-powered image processing, and miniaturization, enabling diverse applications from battlefield situational awareness and surgical assistance to assembly line optimization and immersive entertainment. The EMEA region, with its strong industrial base and defense investments, represents a significant growth opportunity fueled by government funding, innovation hubs, and rising adoption across commercial sectors. Strategic collaborations and regulatory support further underpin the market’s expansion trajectory through 2034.

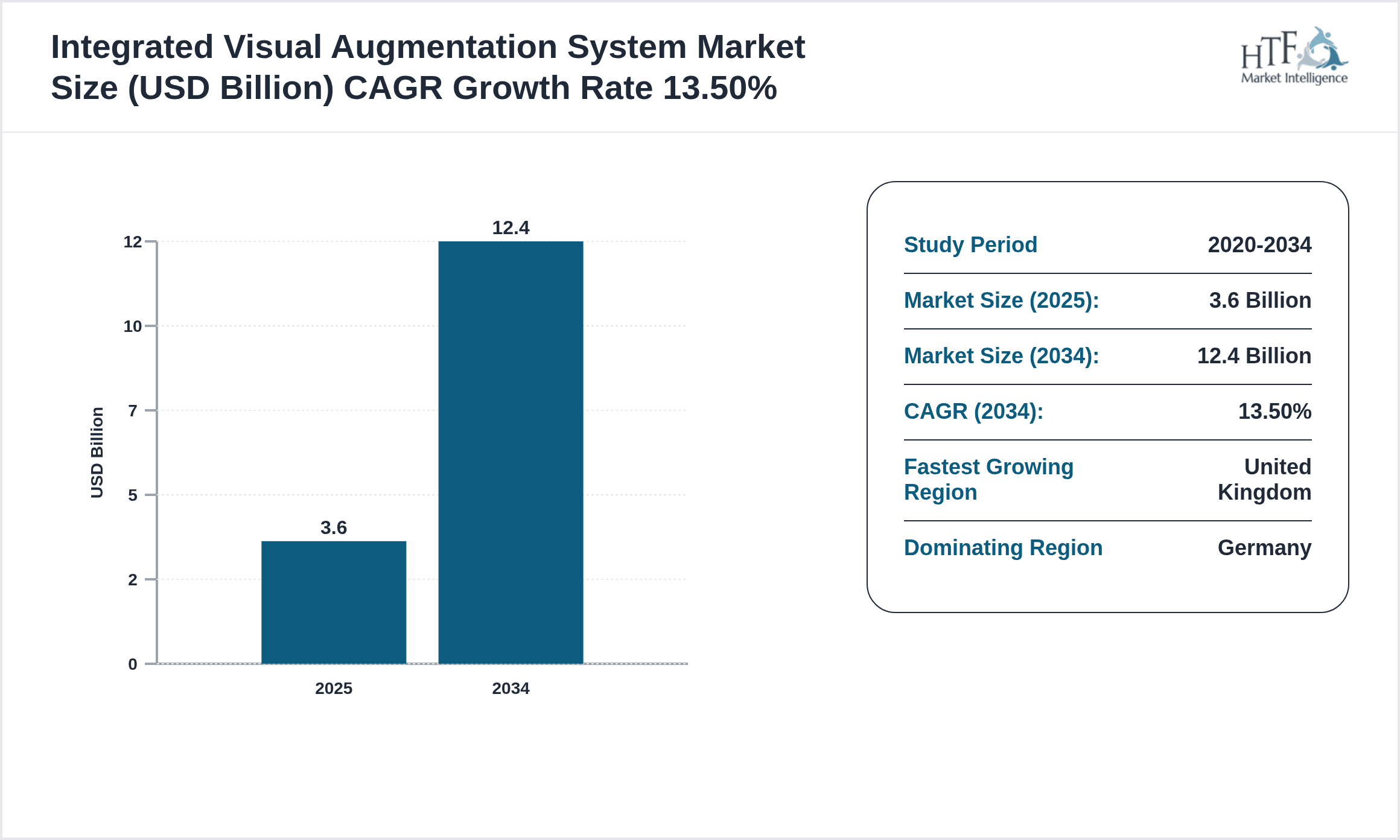

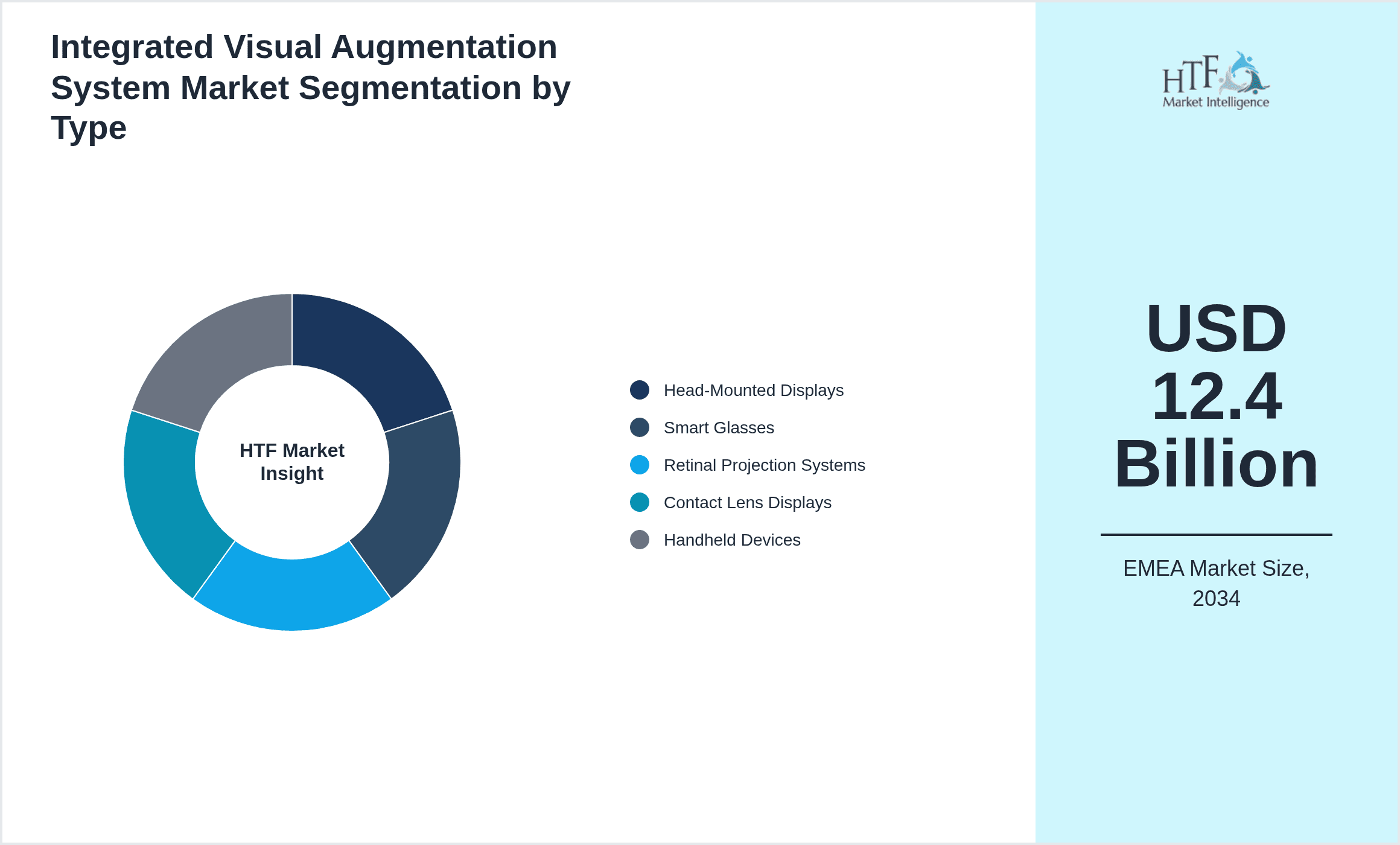

- •Key market highlights include a forecasted CAGR of 13.5% from 2025 to 2034, with the market size expected to increase from USD 3.6 Billion in 2025 to USD 12.4 Billion by 2034. Germany leads as the dominating country with a 25% market share, followed by the United Kingdom, which is the fastest-growing market with an 18% share and a CAGR of 16.2%. Head-Mounted Displays remain the leading product type, while Smart Glasses show the highest growth potential driven by consumer and industrial demand. Applications in military & defense and healthcare dominate the market, benefiting from substantial R&D investments and practical utility in mission-critical scenarios.

- •The market offers substantial value propositions by enabling enhanced situational awareness, precision, and productivity across industries. For stakeholders including device manufacturers, software developers, and end-users in healthcare, defense, and manufacturing, these integrated systems present strategic advantages in operational excellence and competitive differentiation. The convergence of AR, AI, and IoT technologies within these systems enables new business models, facilitates digital transformation initiatives, and supports sustainability goals. Investment in innovation, coupled with favorable regulatory frameworks within the EMEA region, positions this market as a strategic priority for both public and private sector participants aiming to capitalize on the evolving augmented reality landscape.

Competitive Landscape

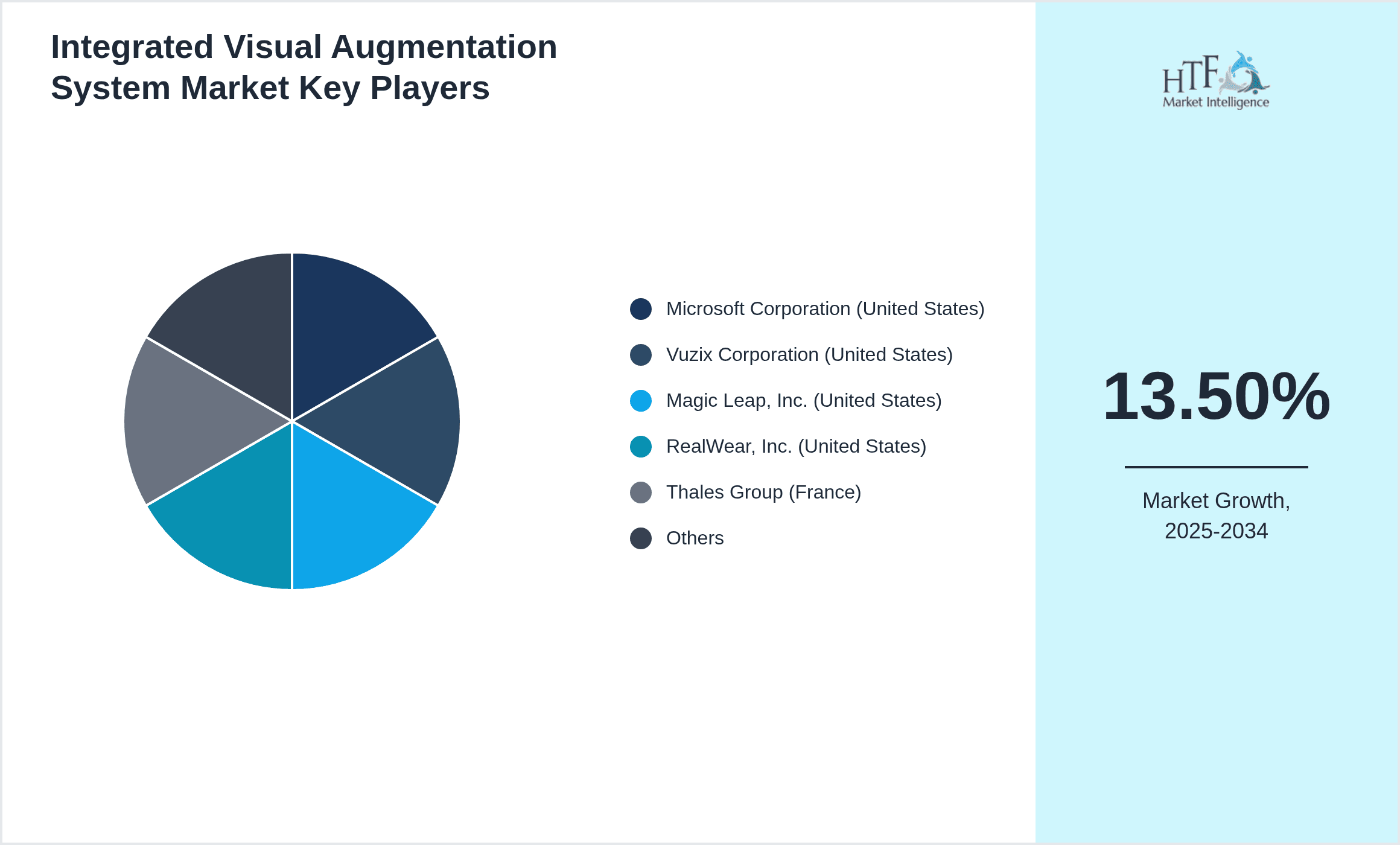

The competitive environment in the EMEA Integrated Visual Augmentation System Market is characterized by a mix of global technology conglomerates and specialized regional innovators. Companies compete on technological innovation, product differentiation, and strategic partnerships to secure market share and expand geographic reach. The rivalry is intense, with firms investing heavily in R&D to develop advanced features such as enhanced display resolution, ergonomic designs, and AI-driven contextual awareness. Strategic alliances and licensing agreements are common to accelerate product development and market penetration. Pricing strategies vary by application segment, with defense-focused products commanding premium pricing due to stringent performance requirements. Distribution channels are diversified, including direct government contracts, healthcare institutions, and industrial clients, as well as consumer retail for smart glasses. Market entry barriers include high capital expenditure, regulatory compliance, and the need for technological expertise, fostering competition among established players while limiting new entrants. Future trends point towards ecosystem development and integration with broader digital infrastructure to maintain competitive advantage.

Prominent Players in Integrated Visual Augmentation System Market

- •Microsoft Corporation (United States)

- •Vuzix Corporation (United States)

- •Magic Leap, Inc. (United States)

- •RealWear, Inc. (United States)

- •Thales Group (France)

- •Rokid Corporation (China)

- •Bosch Group (Germany)

- •Sony Corporation (Japan)

- •Epson Europe B.V. (Netherlands)

- •Meta Platforms, Inc. (United States)

- •Barco NV (Belgium)

- •HoloLens (Microsoft subsidiary) (United States)

- •Lenovo Group Limited (China)

- •Google LLC (United States)

- •DAQRI (United States)

- •Pico Interactive (China)

- •Magic Leap (United States)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Intel Corporation (United States)

- •Honeywell International Inc. (United States)

- •Nokia Corporation (Finland)

- •Meta Company (United States)

- •Zebra Technologies Corporation (United States)

- •Vuzix Corporation (United States)

- •Qualcomm Incorporated (United States)

Market Breakdown

- •By Type

- ◦Head-Mounted Displays

- ◦Smart Glasses

- ◦Retinal Projection Systems

- ◦Contact Lens Displays

- ◦Handheld Devices

- •By Application

- ◦Military & Defense

- ◦Healthcare

- ◦Industrial Manufacturing

- ◦Consumer Electronics

- ◦Automotive

- •By Deployment Model

- ◦On-Premise

- ◦Cloud-Based

- ◦Hybrid

- •By End-User Industry

- ◦Defense Forces

- ◦Hospitals & Clinics

- ◦Manufacturing Plants

- ◦Retail & Entertainment

- ◦Automotive OEMs

Growth Dynamics

- •The growing demand for enhanced situational awareness in military and defense sectors across EMEA is significantly driving the adoption of integrated visual augmentation systems. Governments are investing heavily in modernizing defense capabilities by integrating AR and VR technologies that improve tactical decision-making and soldier safety.

- •Advancements in healthcare technology, especially in minimally invasive surgeries and diagnostics, are fueling market growth. The integration of visual augmentation systems allows surgeons to access critical patient data in real-time, leading to improved precision and patient outcomes.

- •Industrial manufacturing is leveraging these systems to boost operational efficiency and reduce errors on assembly lines. By providing workers with real-time visual instructions and data overlays, factories in Germany, France, and the UK are enhancing productivity and safety.

- •The rising consumer interest in smart wearable devices, fueled by increasing digital literacy and lifestyle shifts, is expanding the market for smart glasses and handheld visual augmentation products in major urban centers across EMEA.

- •Technological innovations such as AI-driven image processing, 5G connectivity, and miniaturization of components are accelerating product development cycles and market penetration, enabling more versatile and user-friendly integrated visual augmentation systems.

Market Trends

- •The integration of AI and machine learning algorithms with visual augmentation systems is becoming a dominant trend, enabling context-aware enhancements and predictive analytics that improve user interaction and decision-making.

- •There is a growing movement towards lightweight, ergonomic smart glasses that cater to prolonged use in both industrial and consumer environments, reflecting increased user comfort and adoption.

- •Collaborations between technology firms and defense agencies in EMEA are leading to custom-tailored solutions optimized for complex operational environments, enhancing system reliability and performance.

- •Sustainability is influencing product design, with manufacturers focusing on energy-efficient displays and recyclable materials to meet regulatory requirements and consumer expectations.

- •Cloud-based deployment models are gaining traction, enabling scalable, remote updates and integration with enterprise IT infrastructure to support evolving operational needs.

Market Opportunities

- •Emerging applications in automotive heads-up displays and driver assistance systems offer substantial growth potential as vehicle manufacturers in EMEA increasingly embed visual augmentation technologies for enhanced safety.

- •The healthcare sector’s expansion into telemedicine and remote diagnostics creates opportunities for integrated visual systems to provide clinicians with enhanced virtual interaction capabilities.

- •Expansion into emerging markets within EMEA, such as the Middle East and Africa, represents untapped potential driven by increasing defense budgets and industrial modernization efforts.

- •R&D investments focused on contact lens display technology and retinal projection systems promise new product categories that could revolutionize wearable visual augmentation applications.

- •Strategic partnerships between hardware manufacturers and software developers can accelerate innovation and market penetration through integrated solution offerings tailored to specific end-user needs.

Market Challenges

- •High costs associated with developing and deploying advanced integrated visual augmentation systems limit accessibility, especially for smaller enterprises and emerging markets within EMEA.

- •Stringent regulatory requirements and certification processes in the medical and defense sectors pose significant hurdles, increasing time-to-market and compliance costs for new products.

- •Technical challenges including battery life limitations, display resolution constraints, and device ergonomics affect user adoption and satisfaction, requiring continuous innovation.

- •Data privacy and cybersecurity concerns around device connectivity and data transmission create trust barriers that manufacturers must address to ensure widespread adoption.

- •The fragmented nature of the EMEA market, with diverse regulatory landscapes and varying levels of technological infrastructure, complicates standardized market strategies and product rollouts.

Regulatory Framework

- •Between 2020 and 2025, the European Union introduced the Medical Device Regulation (MDR) which mandates rigorous safety and performance standards for visual augmentation devices used in healthcare, impacting product development timelines and compliance costs across EMEA.

- •The 2021 EU Cybersecurity Act established certification frameworks for connected devices, including augmented reality systems, ensuring enhanced data protection and device security in commercial and defense applications.

- •The General Data Protection Regulation (GDPR) continues to influence device manufacturers to implement robust data privacy measures, particularly for systems handling sensitive user and operational data.

- •National defense procurement regulations within EMEA countries have become increasingly stringent, with requirements for interoperability, durability, and secure communication protocols for integrated visual augmentation systems.

- •The European Commission's initiatives on sustainability and electronic waste management have led to stricter guidelines on component recyclability and energy efficiency for wearable technology manufacturing.

Market Intelligence

- •15th January 2025, Thales Group launched its latest head-mounted display system designed specifically for military applications, featuring enhanced night vision and augmented reality overlays to improve soldier situational awareness and mission success rates. The system integrates AI-driven threat detection and real-time data streaming capabilities, positioning Thales as a leader in defense-grade visual augmentation solutions across EMEA. This launch reflects the increasing defense sector demand for sophisticated wearable technologies to maintain tactical advantages in complex environments. Source: Official Thales press release.

- •10th March 2025, Bosch Group unveiled a new smart glasses platform for industrial manufacturing that incorporates gesture control, voice commands, and real-time analytics to optimize assembly line workflows. The product’s cloud-based architecture allows seamless integration with existing enterprise resource planning (ERP) systems, enhancing operational efficiency and reducing downtime. Bosch’s innovation responds to growing automation trends and the need for worker augmentation in factories across Germany and France. Source: Bosch corporate announcement.

- •22nd May 2025, Microsoft Corporation expanded its HoloLens product line with a lightweight variant tailored for healthcare professionals, enabling surgeons to overlay 3D anatomical models during procedures. This launch strengthens Microsoft’s position in the medical visual augmentation market and supports the growing adoption of AR-assisted surgeries in EMEA hospitals. Enhanced connectivity and improved battery performance are key features driving user acceptance. Source: Microsoft official news.

- •9th February 2025, Meta Platforms, Inc. announced a strategic partnership with several European automotive manufacturers to develop augmented reality heads-up displays aimed at improving driver safety and navigation. This collaboration leverages Meta’s AR expertise and automotive partners’ market reach to accelerate product adoption in key EMEA markets. The initiative is expected to drive innovation in connected vehicle ecosystems and enhance user experience. Source: Meta corporate press release.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Kingdom is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.6 Billion |

| Forecast Year Market Size | USD 12.4 Billion |

| CAGR | 13.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 13% |

| Scope of Report | Market is segmented by Type (Head-Mounted Displays, Smart Glasses, Retinal Projection Systems, Contact Lens Displays, Handheld Devices), Application (Military & Defense, Healthcare, Industrial Manufacturing, Consumer Electronics, Automotive), Deployment Model (On-Premise, Cloud-Based, Hybrid), End-User Industry (Defense Forces, Hospitals & Clinics, Manufacturing Plants, Retail & Entertainment, Automotive OEMs) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Microsoft Corporation (United States), Vuzix Corporation (United States), Magic Leap, Inc. (United States), RealWear, Inc. (United States), Thales Group (France), Rokid Corporation (China), Bosch Group (Germany), Sony Corporation (Japan), Epson Europe B.V. (Netherlands), Meta Platforms, Inc. (United States), Barco NV (Belgium), HoloLens (Microsoft subsidiary) (United States), Lenovo Group Limited (China), Google LLC (United States), DAQRI (United States), Pico Interactive (China), Magic Leap (United States), Samsung Electronics Co., Ltd. (South Korea), Intel Corporation (United States), Honeywell International Inc. (United States), Nokia Corporation (Finland), Meta Company (United States), Zebra Technologies Corporation (United States), Vuzix Corporation (United States), Qualcomm Incorporated (United States) |

EMEA Integrated Visual Augmentation System Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.