United Kingdom Pro Audio Equipment Market Size, Growth & Revenue 2025-2034

United Kingdom Pro Audio Equipment Market is segmented by Application (Live Events, Studio Recording, Broadcasting, Installation, DJ Equipment), Type (Mixers, Amplifiers, Microphones, Speakers, Audio Interfaces), and Geography (England, Scotland, Wales, Northern Ireland)

Pricing

Report Overview

Executive Summary

- •The United Kingdom Pro Audio Equipment market comprises professional-grade audio devices including mixers, amplifiers, microphones, speakers, and audio interfaces. These products serve critical functions in live events, studio recording, broadcasting, fixed installations, and DJ performances. The market's scope extends to equipment sales, rentals, and after-sales services, integrating advanced audio technologies such as digital signal processing and wireless systems. The market supports the UK's dynamic entertainment, media, and event industries by enabling enhanced sound quality and operational efficiency. Increasing demand from music festivals, concert venues, broadcast studios, and corporate events drives growth. The market's significance arises from its role in enriching user experience and enabling creative audio applications. Continuous innovation and adoption of smart audio technologies further strengthen market prospects, making the United Kingdom a key hub for pro audio equipment usage and development.

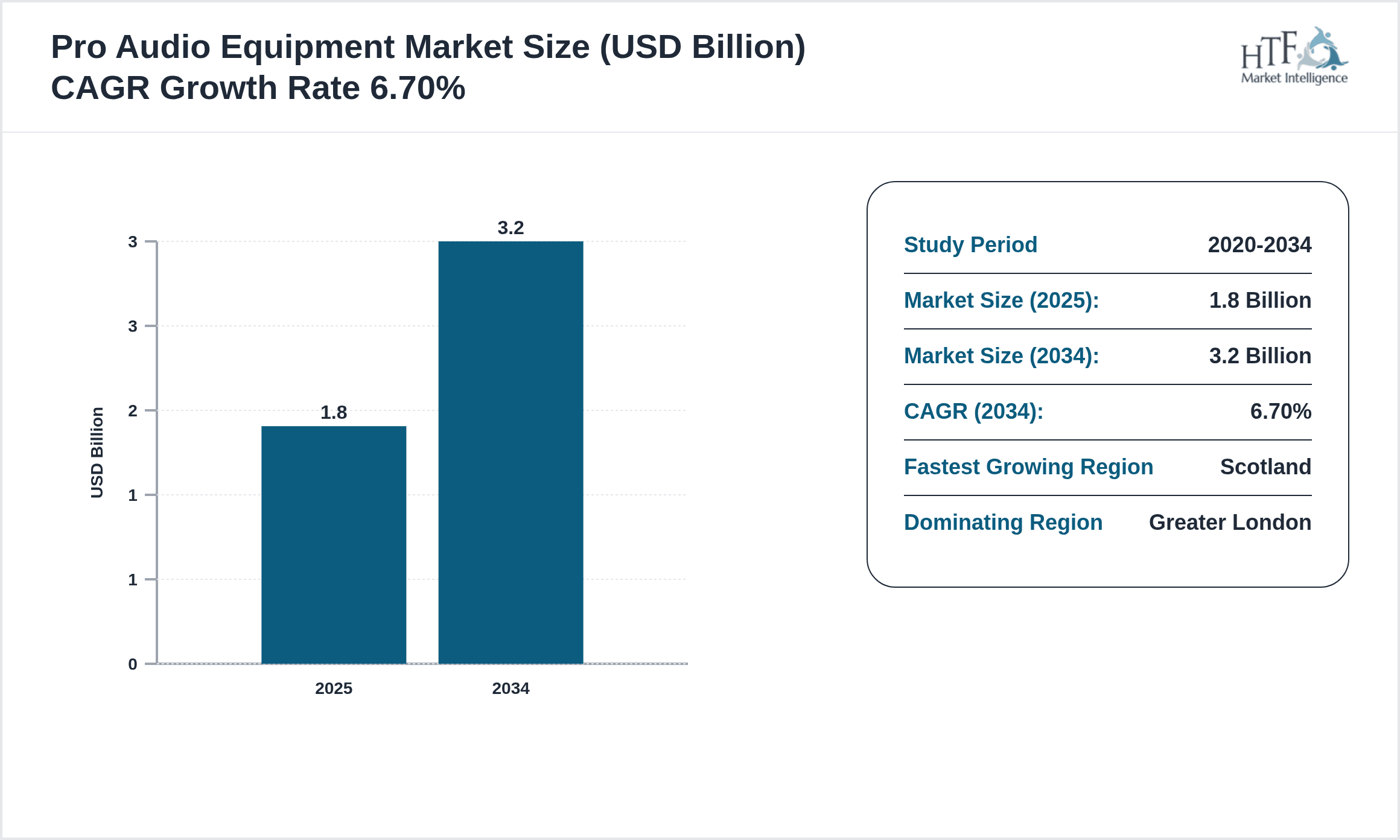

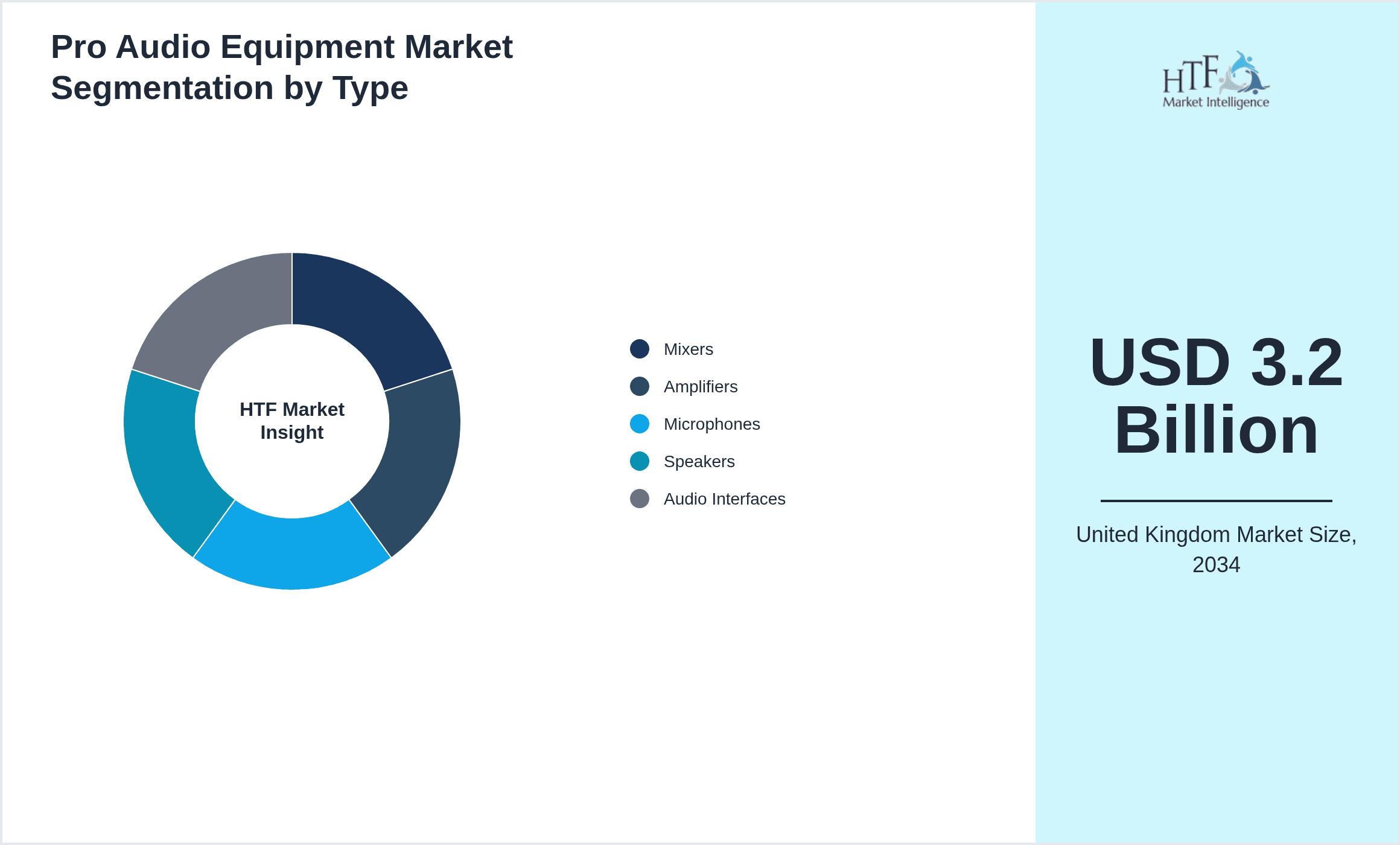

- •The market is projected to grow from USD 1.8 Billion in 2025 to USD 3.2 Billion by 2034, registering a CAGR of 6.7%. Greater London dominates the market with a 34% share, while Scotland exhibits the fastest growth at 8.2% CAGR. Mixers maintain leadership as the most demanded product type, whereas audio interfaces are the fastest growing segment. Live events and studio recording lead application demand. The market benefits from robust entertainment sector investments and technological advancements improving audio quality and integration. Year-on-year growth at 6.7% reflects steady expansion driven by rising event activities and digital media production. The market is strategically important to stakeholders across entertainment, broadcasting, and corporate sectors.

- •The United Kingdom Pro Audio Equipment market offers strategic value to manufacturers, distributors, event organizers, and broadcasters by enabling superior sound delivery and operational capabilities. Investment in R&D drives innovation in wireless and digital audio solutions, addressing evolving customer demands. The market supports the UK’s cultural and creative industries by facilitating immersive audio experiences. Stakeholders benefit from expanding applications in live entertainment, professional studios, and digital broadcasting. The market’s growth enhances employment opportunities in manufacturing, rental, and service sectors. Strategic partnerships among technology developers and event companies fuel competitive advantages. Overall, the market represents a vital segment contributing to the UK's audio technology ecosystem and entertainment economy.

Competitive Landscape

Companies operating in the United Kingdom Pro Audio Equipment market implement diverse strategies to sustain and grow their market presence. Product innovation focusing on digital audio processing, wireless connectivity, and integration with software platforms enhances competitive positioning. Many players engage in strategic partnerships with event organizers, studios, and broadcasters to secure long-term contracts and expand their footprint. Global expansion through localized service centers and distribution networks strengthens market reach. Adoption of eco-friendly manufacturing and energy-efficient products aligns with regulatory and consumer demands. Investment in after-sales support and rental services improves customer loyalty and recurring revenue streams. Firms leverage technological advancements such as AI-driven audio enhancement and cloud-based mixing solutions to differentiate offerings. Mergers and acquisitions create synergies, enabling resource sharing and accelerated innovation. Regional competition emphasizes customization for local music and entertainment culture, while future trends point to increasing digitization and automation enhancing operational efficiency and user experience.

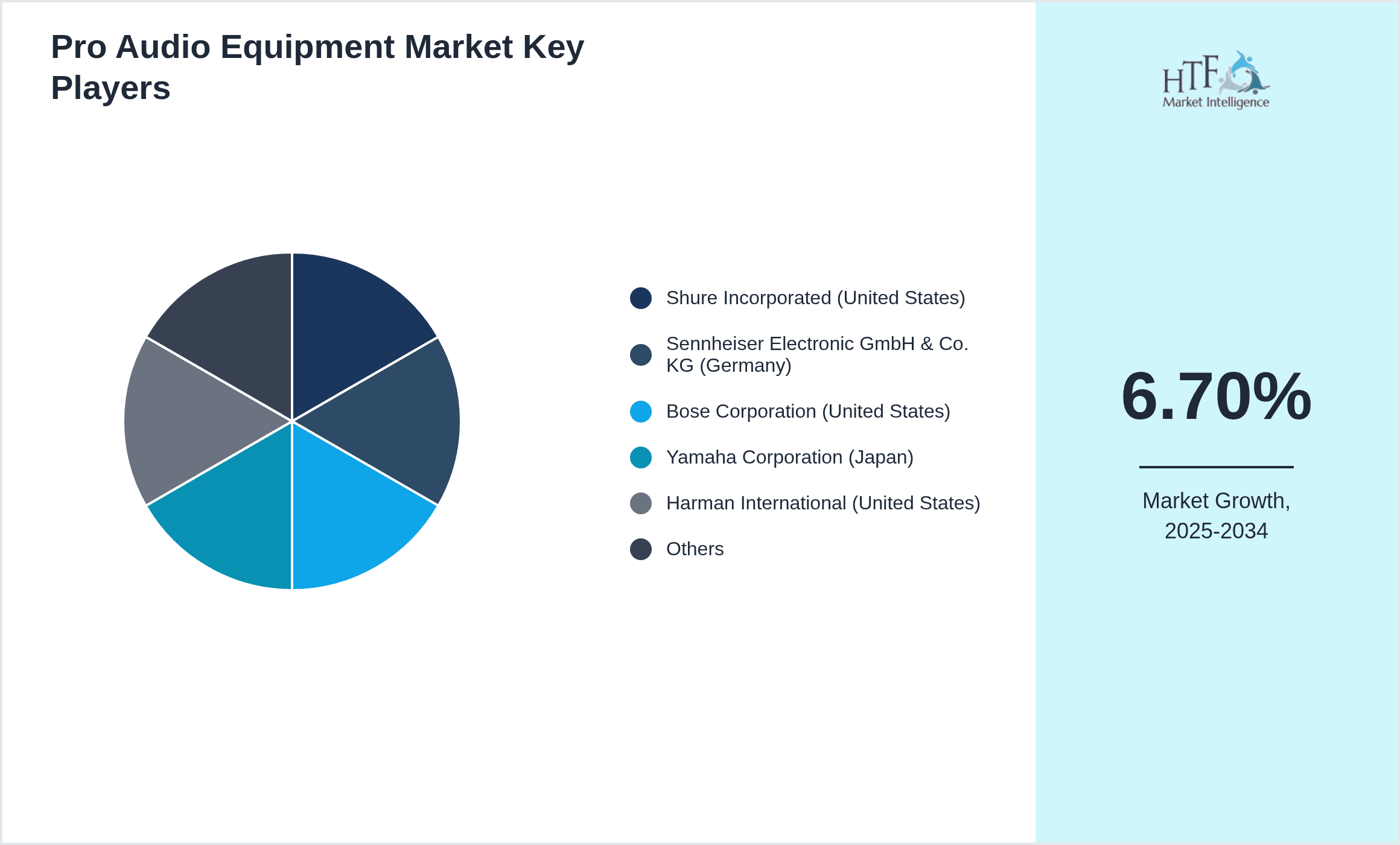

Leading Companies in Pro Audio Equipment Market

- •Shure Incorporated (United States)

- •Sennheiser Electronic GmbH & Co. KG (Germany)

- •Bose Corporation (United States)

- •Yamaha Corporation (Japan)

- •Harman International (United States)

- •Audio-Technica Corporation (Japan)

- •Electro-Voice (United States)

- •AKG Acoustics (Austria)

- •Mackie (United States)

- •QSC, LLC (United States)

- •Roland Corporation (Japan)

- •Behringer (Germany)

- •Neumann GmbH (Germany)

- •SPL Electronics GmbH (Germany)

- •TC Electronic (Denmark)

- •DiGiCo (United Kingdom)

- •Solid State Logic (United Kingdom)

- •Focusrite plc (United Kingdom)

- •Rode Microphones (Australia)

- •L-Acoustics (France)

Market Breakdown

- •By Type

- ◦Mixers

- ◦Amplifiers

- ◦Microphones

- ◦Speakers

- ◦Audio Interfaces

- •By Application

- ◦Live Events

- ◦Studio Recording

- ◦Broadcasting

- ◦Installation

- ◦DJ Equipment

- •By Distribution Channel

- ◦Direct Sales

- ◦Retail Stores

- ◦Online Sales

- ◦Rental Services

- •By Product Technology

- ◦Analog

- ◦Digital

- ◦Wireless

- ◦USB-Enabled

Growth Dynamics

The United Kingdom Pro Audio Equipment market experiences robust growth driven by increased live music events, cultural festivals, and corporate functions necessitating high-quality sound systems. Investments in event infrastructure and government support for arts and culture stimulate demand for advanced audio equipment. The rising popularity of home studios and online content creation expands the need for professional-grade audio interfaces and mixers. Technology adoption such as digital signal processing and wireless audio solutions enhances product appeal and operational efficiency. Collaborations between audio manufacturers and media production houses facilitate tailored solutions. Recent launches of compact and portable pro audio devices cater to mobility needs of professionals, further propelling market expansion. The surge in broadcast media and digital streaming platforms also contributes to increased equipment procurement, ensuring consistent demand. The market benefits from a skilled workforce and innovation ecosystem promoting product development aligned with evolving audio quality standards.

Market Trends

Emerging trends in the United Kingdom Pro Audio Equipment market include integration of artificial intelligence and machine learning to optimize sound engineering and mixing processes. Wireless and networked audio systems gaining traction enable flexible event setups and remote control capabilities. Sustainability considerations drive demand for energy-efficient and recyclable audio components. Modular and scalable audio solutions allow customization for diverse applications ranging from small venues to large concerts. Increasing use of immersive audio technologies such as spatial sound and 3D audio enhances audience experiences. The growth of virtual and hybrid events post-pandemic accelerates adoption of connected audio devices supporting streaming and remote participation. Companies invest in product designs focusing on portability without compromising audio fidelity. Recent industry collaborations focus on developing interoperable systems ensuring seamless integration across various platforms and devices, positioning the market for sustained innovation and growth.

Market Opportunities

The United Kingdom Pro Audio Equipment market presents opportunities in expanding rental services catering to event organizers seeking cost-effective solutions. Growth in independent music production and podcasting opens new customer segments requiring affordable yet professional audio equipment. Increasing government funding for cultural events and media production provides avenues for market penetration. Development of smart audio devices incorporating IoT technology offers potential for enhanced usability and remote diagnostics. Geographic expansion into underpenetrated regions like Wales and Northern Ireland supports market diversification. Collaborations with educational institutions promoting audio engineering curricula can foster brand loyalty and early adoption. The rising trend of hybrid events combining physical and virtual attendance demands integrated audio-visual solutions, creating cross-selling opportunities. Investment in after-sales service infrastructure and training centers strengthens customer retention. The market can leverage digital marketing and e-commerce channels to widen reach and improve customer engagement, capitalizing on shifting purchasing behaviors.

Market Challenges

The United Kingdom Pro Audio Equipment market faces challenges including high initial costs of advanced digital and wireless systems, limiting adoption among smaller event organizers and independent studios. Supply chain disruptions and component shortages during global crises impact timely product availability and increase production costs. Intense competition from low-cost imports pressures pricing and profit margins of domestic manufacturers. Rapid technological obsolescence demands continuous innovation, burdening companies with R&D expenses. Regulatory compliance costs related to electromagnetic compatibility and safety standards add complexity to product development. Skilled labor shortages in audio engineering and technical support hinder service quality. Market fragmentation and diverse customer requirements complicate standardized product offerings. Brexit-induced trade uncertainties affect import-export dynamics, influencing inventory management and pricing strategies. Examples include delayed shipments affecting product launches and increased tariffs leading to higher end-user prices. Addressing these challenges requires strategic planning, flexible supply chains, and investment in workforce development.

Regulatory Framework

The United Kingdom enforces compliance with the Electromagnetic Compatibility Regulations 2016, requiring pro audio equipment to meet stringent electromagnetic interference standards to ensure device safety and interoperability. The Electrical Equipment (Safety) Regulations mandate product safety certifications, protecting consumers and reducing liability risks for manufacturers. The UK’s adoption of the Restriction of Hazardous Substances (RoHS) Directive restricts use of specific hazardous materials in electronic products, promoting environmentally responsible manufacturing. The Wireless Telegraphy Act governs licensing and use of radio frequency spectrum for wireless audio devices, ensuring interference-free operation. Additionally, regulations on noise emission levels at public events are enforced to protect public health and comply with local authority requirements. These regulatory measures impact product design, testing, and market entry strategies, compelling companies to maintain rigorous quality control and certification processes aligned with UK standards introduced or updated within the last five years.

Recent Industry Insights

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Recent Merger and Acquisition

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Greater London currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Scotland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- England

- Scotland

- Wales

- Northern Ireland

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 3.2 Billion |

| CAGR | 6.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.7% |

| Regions Covered | England, Scotland, Wales, Northern Ireland |

| Key Companies | Shure Incorporated (United States), Sennheiser Electronic GmbH & Co. KG (Germany), Bose Corporation (United States), Yamaha Corporation (Japan), Harman International (United States), Audio-Technica Corporation (Japan), Electro-Voice (United States), AKG Acoustics (Austria), Mackie (United States), QSC, LLC (United States), Roland Corporation (Japan), Behringer (Germany), Neumann GmbH (Germany), SPL Electronics GmbH (Germany), TC Electronic (Denmark), DiGiCo (United Kingdom), Solid State Logic (United Kingdom), Focusrite plc (United Kingdom), Rode Microphones (Australia), L-Acoustics (France) |

United Kingdom Pro Audio Equipment Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.