China Dental CBCT Market Size, Growth & Revenue 2024-2034

China Dental CBCT Market is segmented by Type (Stationary CBCT, Mobile CBCT, Handheld CBCT, Industrial CBCT, Hybrid CBCT), Application (Implantology, Endodontics, Orthodontics, Oral Surgery, Periodontics), End User (Dental Hospitals, Dental Clinics, Diagnostic Centers, Academic & Research Institutes), Distribution Channel (Direct Sales, Distributors, Online Platforms, After-Sales Service Networks), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Dental CBCT Market comprises sophisticated imaging modalities delivering high-resolution 3D visualization critical for dental diagnostics and therapeutic planning. This market includes diverse CBCT types such as stationary units primarily deployed in large dental hospitals, mobile and handheld devices increasingly favored for smaller clinics and remote areas, and hybrid solutions combining multiple technologies to enhance imaging accuracy. Applications span implantology, orthodontics, endodontics, oral surgery, and periodontics, reflecting the wide clinical utility of CBCT technology. The market is shaped by technological advancements, rising dental care expenditure, and a growing patient base seeking precise and minimally invasive treatments. Regional disparities within China, especially between developed zones like East China and emerging regions like Southwest China, influence market penetration and growth dynamics. The expanding dental healthcare infrastructure, coupled with government initiatives promoting oral health, propels demand. Competitive landscape features domestic manufacturers alongside global players adapting products to local needs. Regulatory frameworks ensure safety and quality compliance. Overall, the China Dental CBCT market is forecasted for robust double-digit growth fueled by innovation, increasing clinical adoption, and enhanced patient awareness.

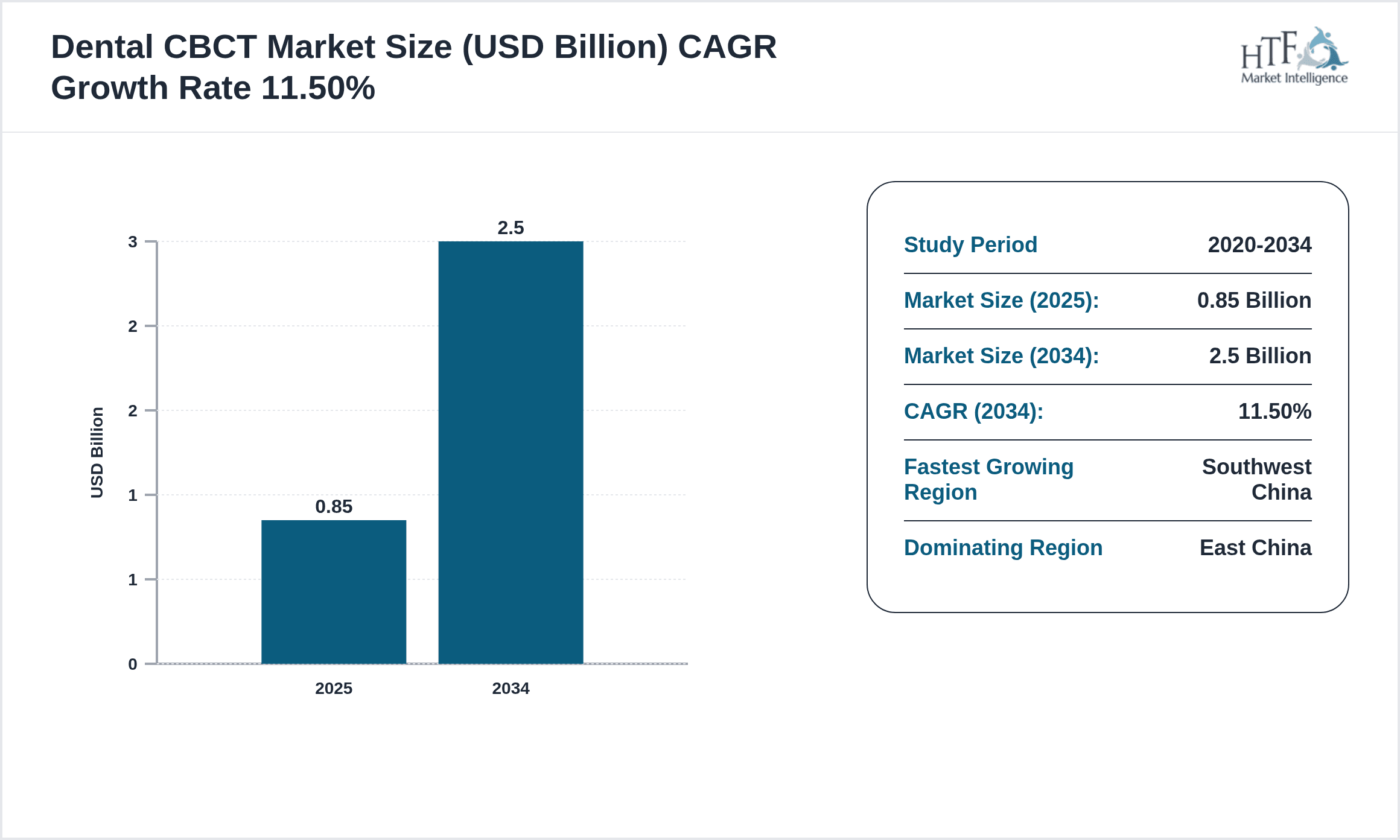

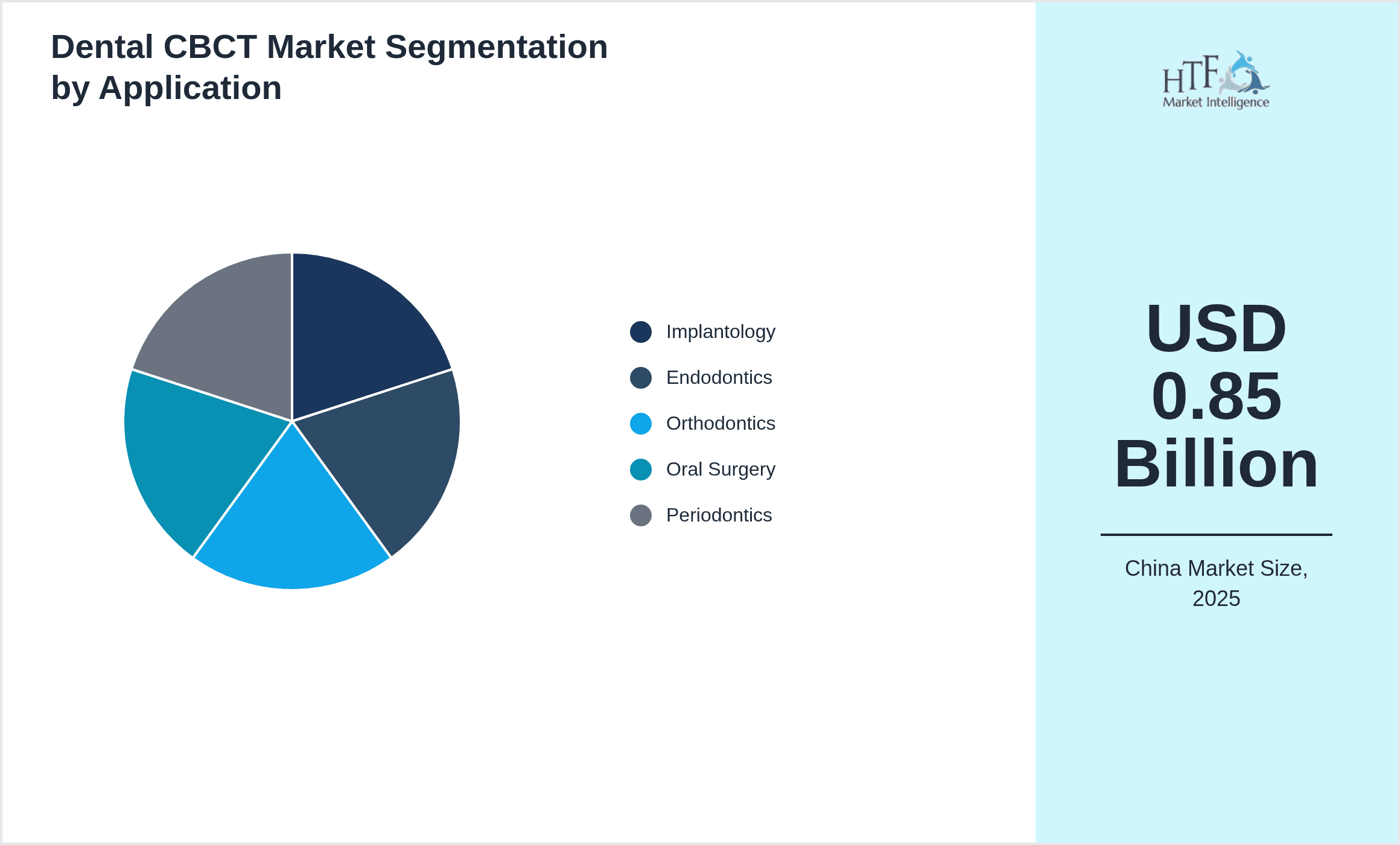

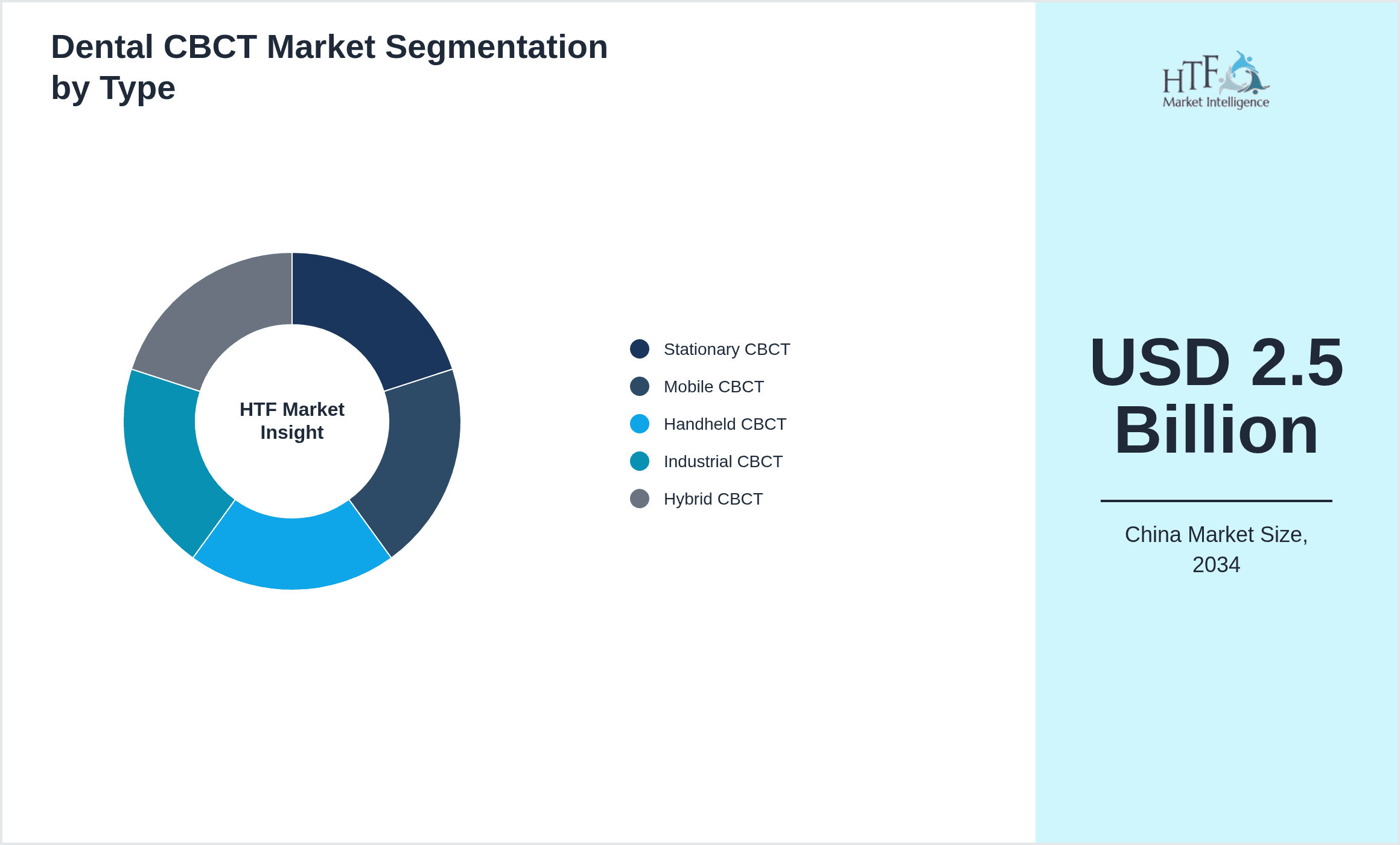

- •Key market highlights include a base market size of USD 0.85 billion in 2025, projected to reach USD 2.5 billion by 2034 at a CAGR of 11.5%. East China dominates with a 35% market share driven by advanced healthcare infrastructure and high patient volumes. Southwest China is the fastest-growing sub-region with a CAGR of 14.2%, reflecting rising investments in dental services. Stationary CBCT leads product segments due to its superior imaging capabilities, while mobile CBCT exhibits fastest growth owing to portability and flexible deployment. Implantology remains the largest application, followed by orthodontics, supported by increasing demand for dental implants and corrective procedures. Market growth is catalyzed by rising geriatric population, technological innovation, and increased dental insurance penetration. However, high costs and regulatory complexities pose challenges. Emerging trends include AI integration and digital workflow enhancement, unlocking new opportunities for service providers and device manufacturers.

- •This market offers significant strategic value to dental equipment manufacturers, healthcare providers, and technology innovators. Enhanced imaging accuracy translates to improved patient outcomes and operational efficiencies. The rising adoption of CBCT technology supports minimally invasive dentistry and precision treatment planning, essential for implantology and orthodontics. For stakeholders, the China Dental CBCT market provides avenues for product differentiation, regional expansion, and digital integration. Government-led oral health initiatives and increasing consumer awareness further augment market attractiveness. Strategic collaborations, localized manufacturing, and tailored service models are critical for capitalizing on regional growth pockets. As the market evolves, continuous innovation in imaging technology and compliance with regulatory standards will be pivotal for sustaining competitive advantage. Overall, the market represents a converging point of clinical need, technological advancement, and economic opportunity within China's rapidly expanding dental healthcare ecosystem.

Competitive Landscape

The China Dental CBCT market is characterized by intense competition among domestic manufacturers and international players striving to capture expanding demand. Market leaders emphasize innovation with continuous upgrades in imaging resolution, software integration, and user interface to differentiate their portfolios. Competitive strategies include strategic partnerships, localized production, and after-sales service enhancement to address diverse clinical and regional needs. Price competition is moderated by technological sophistication and regulatory compliance costs. Companies focus on developing portable and cost-effective solutions to penetrate tier 2 and 3 cities. Innovation extends to AI-enabled diagnostic capabilities and cloud-based data management, enhancing clinical workflows. Additionally, mergers and acquisitions are shaping market consolidation, enabling expanded product offerings and geographic reach. Distribution channels vary from direct sales to dental chains and digital platforms, influencing market penetration. Regulatory adherence and certification serve as competitive barriers, ensuring quality and safety. Overall, the competitive landscape reflects a dynamic interplay of technology leadership, customer-centric service, and regional market adaptation shaping future growth trajectories.

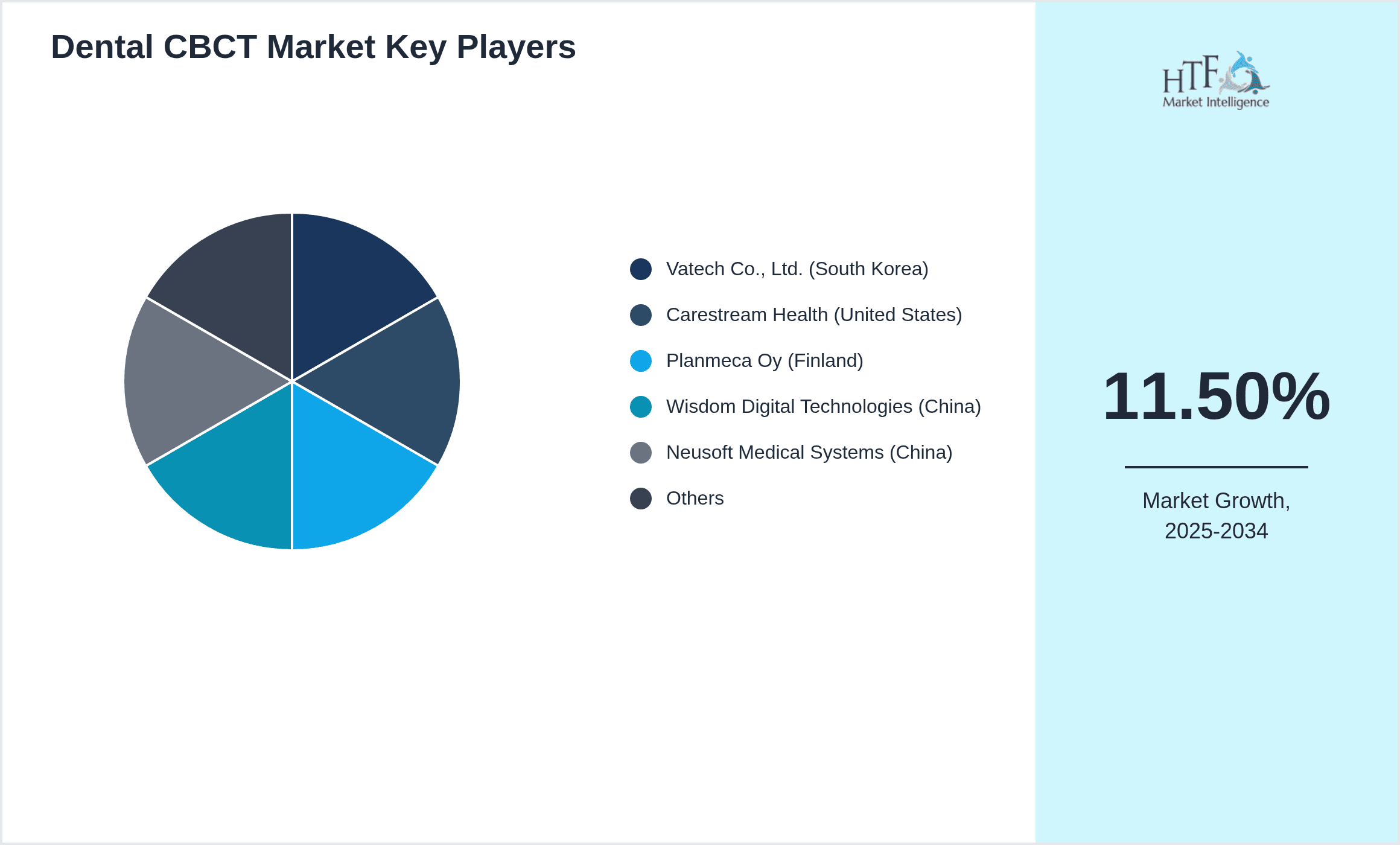

Leading Companies in China Dental CBCT Market

- •Vatech Co., Ltd. (South Korea)

- •Carestream Health (United States)

- •Planmeca Oy (Finland)

- •Wisdom Digital Technologies (China)

- •Neusoft Medical Systems (China)

- •Shenzhen Landwind Industry Co., Ltd. (China)

- •Soredex (Finland)

- •Sirona Dental Systems (Germany)

- •Morita Group (Japan)

- •Dentsply Sirona (United States)

- •Shanghai United Imaging Healthcare Co., Ltd. (China)

- •Zhejiang Hengtong Medical Equipment Co., Ltd. (China)

- •J. Morita Corporation (Japan)

- •RadiForce Company (Japan)

- •Anke Medical Corporation (China)

- •Perlove Medical Technology Co., Ltd. (China)

- •Shanghai Medicloud Technology Co., Ltd. (China)

- •Dürr Dental SE (Germany)

- •NewTom (Italy)

- •Imaging Sciences International (United States)

- •Gendex Dental Systems (United States)

- •Orangedental (China)

- •Wuhan Guide Infrared Co., Ltd. (China)

- •Beijing AUSS Technology Co., Ltd. (China)

- •Canon Medical Systems Corporation (Japan)

Market Breakdown

- •By Type

- ◦Stationary CBCT

- ◦Mobile CBCT

- ◦Handheld CBCT

- ◦Industrial CBCT

- ◦Hybrid CBCT

- •By Application

- ◦Implantology

- ◦Endodontics

- ◦Orthodontics

- ◦Oral Surgery

- ◦Periodontics

- •By End User

- ◦Dental Hospitals

- ◦Dental Clinics

- ◦Diagnostic Centers

- ◦Academic & Research Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

- ◦After-Sales Service Networks

Growth Dynamics

- •The China Dental CBCT market is propelled by escalating demand for precise dental diagnostics driven by the rising prevalence of oral diseases and growing geriatric population. Increasing patient awareness about dental health and advanced treatment options has elevated adoption rates among dental professionals. Expansion of dental healthcare infrastructure, particularly in urban centers like East China, augments accessibility to CBCT technology. Technological advancements, including enhanced image resolution and reduced radiation exposure, bolster clinical acceptance. Furthermore, government initiatives promoting oral health and reimbursement schemes incentivize investment in dental imaging equipment. The trend towards minimally invasive procedures requiring detailed 3D imaging also supports market growth. Collectively, these factors create a favorable environment for sustained double-digit growth, with emerging regions such as Southwest China witnessing accelerated adoption fueled by improving healthcare facilities and rising disposable incomes.

- •The China Dental CBCT market is witnessing a shift towards integration of artificial intelligence and digital workflow enhancements, revolutionizing diagnostic accuracy and treatment planning. Innovations include AI-powered image analysis facilitating automated anomaly detection, improving diagnostic speed and reducing human error. Portable and mobile CBCT devices are gaining traction, enabling flexible deployment in smaller clinics and remote locations, thus expanding market reach. Enhanced software interoperability with electronic health records and cloud-based platforms streamlines data management and collaborative care. Additionally, product developments focusing on low-dose radiation protocols address safety concerns, encouraging broader clinical adoption. These technological trends are complemented by increasing investments in dental research and development by both domestic and international players, fostering a competitive and innovative market landscape.

- •Market restraints include the high cost of advanced CBCT systems and associated maintenance expenses, limiting penetration in smaller dental practices and tier 3 cities. Regulatory complexities and stringent certification processes for medical imaging devices can delay product launches and increase compliance costs. Additionally, lack of standardized training for dental professionals on CBCT operation and interpretation hampers widespread adoption. Infrastructure limitations in rural and underdeveloped regions further restrict market growth. Concerns regarding patient radiation exposure, despite improvements, continue to influence cautious adoption among practitioners. Furthermore, competition from alternative imaging modalities like digital panoramic X-rays, which are more affordable, poses a challenge. Addressing these barriers requires strategic pricing, enhanced training programs, and regulatory streamlining to unlock full market potential.

- •Opportunities in the China Dental CBCT market arise from expanding dental healthcare coverage and increasing insurance reimbursement facilitating higher adoption. Emerging markets within China’s less developed regions present untapped potential driven by rising oral health awareness and infrastructure development. Integration of AI and machine learning technologies offers prospects for product differentiation and enhanced diagnostic capabilities. Strategic collaborations between technology providers and dental service chains can accelerate market penetration. Additionally, growing demand for personalized dental care and precision implantology procedures creates niches for innovative CBCT solutions tailored to specific clinical needs. The surge in dental tourism and cosmetic dentistry further expands the addressable market. Manufacturers investing in cost-effective portable CBCT devices can capitalize on the demand from smaller clinics and remote areas, ensuring inclusive market growth.

- •The China Dental CBCT market faces challenges including intense competition from global and local manufacturers driving price erosion and margin pressures. Complexity in navigating the evolving regulatory environment requires continuous compliance vigilance, increasing operational costs. Supply chain disruptions and component shortages can delay product availability. Variability in regional healthcare infrastructure leads to uneven market penetration, complicating nationwide commercialization strategies. Moreover, educating clinicians on the optimal use of CBCT technology remains a persistent hurdle, impacting utilization rates. Data security and patient privacy concerns associated with digital imaging storage and transmission necessitate robust cybersecurity measures. Sustaining innovation while maintaining affordability is critical for long-term success. Addressing these challenges demands coordinated efforts in regulatory alignment, training initiatives, and investment in resilient supply chains.

Market Trends

- •Integration of artificial intelligence in Dental CBCT systems is advancing rapidly, enabling automated detection of dental pathologies and improving diagnostic accuracy. Leading manufacturers are embedding AI algorithms that assist clinicians by highlighting anomalies such as root fractures or bone density variations, significantly reducing interpretation time and enhancing treatment outcomes. This trend is supported by increasing computational power and big data analytics adoption in China’s healthcare sector, positioning AI-enabled CBCT as a mainstream diagnostic tool.

- •The rise of portable and mobile CBCT devices is transforming the market by providing flexible imaging solutions for small clinics and remote areas. These compact units offer easier installation, lower costs, and enhanced mobility, addressing accessibility barriers in tier 2 and 3 cities. Growing demand for outpatient dental services and home healthcare further drives this trend, fostering decentralized dental imaging capabilities.

- •Digital workflow integration is a significant trend, with CBCT imaging increasingly connected to cloud platforms and electronic health records. This facilitates seamless data sharing among dental professionals, enhancing multidisciplinary collaboration and patient management. Companies are investing in interoperable software solutions to support this ecosystem, improving clinical efficiency and patient engagement across China’s expanding dental networks.

- •Safety-focused innovations such as ultra-low radiation dose protocols and improved shielding materials are gaining prominence. These advancements address patient and practitioner concerns about radiation exposure, promoting wider acceptance of CBCT technology. Regulatory emphasis on safety compliance accelerates adoption of these features, especially in pediatric and cosmetic dentistry applications.

- •Collaborative partnerships between dental CBCT manufacturers and healthcare providers are increasing to co-develop customized imaging solutions. These alliances enable tailored product features aligned with specific clinical workflows and regional market needs, enhancing user satisfaction and fostering long-term customer relationships. Such ecosystem development supports sustained innovation and market penetration.

- •Market segmentation based on patient demographics is evolving, with devices optimized for geriatric and pediatric populations becoming more prevalent. Customized scanning protocols and ergonomic designs cater to these groups, reflecting the growing focus on personalized dental care in China’s aging society and rising child healthcare awareness.

- •Future directions include the integration of 3D printing with CBCT imaging for precise surgical guides and prosthetic design, facilitating comprehensive digital dentistry workflows. This convergence is expected to revolutionize treatment planning and execution, positioning China at the forefront of dental technology innovation.

Market Opportunities

- •Expanding dental infrastructure in underpenetrated regions such as Southwest and Northwest China presents significant growth opportunities. Investments in modernizing healthcare facilities and increasing oral health awareness in these zones create demand for advanced imaging technologies like CBCT. Companies focusing on affordable, portable devices can capture these emerging markets effectively.

- •The integration of AI-powered diagnostic tools with CBCT systems offers avenues for product differentiation and enhanced clinical value. Developing proprietary algorithms tailored to common dental pathologies prevalent in China can provide competitive advantages and improve adoption rates among dental professionals.

- •Collaborations with dental service chains and academic institutions enable co-creation of customized CBCT solutions and training programs. Such partnerships can accelerate technology diffusion, improve clinician competence, and foster innovation aligned with evolving clinical needs and regulatory requirements.

- •Rising dental insurance coverage and reimbursement policies in China reduce financial barriers for patients and providers, stimulating CBCT adoption. Companies can leverage this by offering bundled service packages and financing options, enhancing market accessibility and customer loyalty.

- •Development of low-dose radiation protocols and safety-certified products addresses patient and regulatory concerns, unlocking wider acceptance particularly in pediatric and cosmetic dentistry segments. Investment in safety innovation can serve as a key market differentiator.

- •Digital transformation initiatives in China’s healthcare system encourage integration of CBCT imaging with tele-dentistry and remote diagnostics. Capitalizing on this trend through cloud-based platforms and mobile connectivity expands market reach and enhances patient care delivery in remote areas.

- •Emerging applications such as 3D surgical guides and integration with CAD/CAM technology present new revenue streams. Developing comprehensive digital dentistry ecosystems centered on CBCT imaging can position manufacturers as end-to-end solution providers.

Market Challenges

- •High acquisition and maintenance costs associated with advanced Dental CBCT systems limit penetration in smaller clinics and less affluent regions. Cost sensitivity among providers necessitates development of affordable yet clinically effective solutions to expand market reach.

- •Complex and evolving regulatory requirements for medical imaging devices in China pose challenges for timely product approvals and market entry. Navigating certification processes demands substantial investment in compliance and documentation, impacting time-to-market.

- •Limited availability of trained dental professionals proficient in CBCT operation and image interpretation restricts optimal utilization. The lack of standardized training programs and continuing education contributes to underutilization and suboptimal clinical outcomes.

- •Competition from conventional imaging modalities such as panoramic X-rays, which are more affordable and widely established, continues to hinder CBCT adoption in cost-sensitive segments. Demonstrating clear clinical and economic benefits remains essential to justify investment.

- •Supply chain disruptions including semiconductor shortages and import restrictions affect device manufacturing and availability, leading to delays and increased costs. Diversification of suppliers and localization strategies are required to mitigate risks.

- •Data security and patient privacy concerns associated with digital imaging storage and transmission necessitate robust cybersecurity measures. Compliance with data protection regulations is critical to maintain trust and avoid legal ramifications.

- •Balancing rapid technological innovation with affordability and ease of use remains a persistent challenge. Overly complex systems may deter adoption among smaller clinics lacking specialized staff, emphasizing the need for user-friendly designs.

Regulatory Framework

- •Between 2018 and 2025, China implemented the revised Medical Device Supervision and Administration Regulations mandating stricter quality control, clinical evaluation, and post-market surveillance for dental imaging equipment. Compliance with these regulations ensures product safety and efficacy, impacting market entry timelines and operational practices.

- •The National Medical Products Administration (NMPA) introduced updated certification requirements in 2022 focusing on radiation safety standards, mandating dose optimization and patient protection protocols for CBCT devices. These regulations have driven manufacturers to innovate low-dose technologies and enhance shielding features.

- •In 2021, China adopted the Digital Health Data Protection Guidelines setting stringent data privacy and security standards for medical imaging data storage and transmission. This regulation influences CBCT software design and cloud integration strategies, ensuring patient confidentiality and compliance with cybersecurity norms.

- •Regional mandates such as the Guangdong Province Medical Device Management Policies enacted in 2023 emphasize localized inspection and quality audits, reinforcing compliance at sub-national levels and fostering higher safety assurance for dental CBCT systems in key markets like East China.

- •Government initiatives under the Healthy China 2030 plan promote oral health awareness and infrastructure upgrades, indirectly supporting regulatory incentives for adoption of advanced diagnostic technologies including CBCT. These policies provide market support through funding and reimbursement facilitation.

Market Intelligence

- •15th January 2025, Vatech Co., Ltd. launched its next-generation Stationary CBCT system in China featuring ultra-low radiation dose technology combined with AI-based diagnostic software. The product targets major dental hospitals in East China, enhancing implantology and orthodontic treatment planning with superior image clarity and workflow integration. This launch aligns with growing regulatory emphasis on patient safety and digitalization trends in Chinese dental care. Vatech aims to consolidate its market leadership by expanding its service network and strengthening partnerships with dental service providers across key regional zones. Source: Official Vatech Press Release

- •10th March 2025, Wisdom Digital Technologies introduced a Mobile CBCT device tailored for tier 2 and 3 city clinics, emphasizing portability, affordability, and ease of use. The device integrates cloud-based data management and supports remote diagnostics, addressing accessibility challenges in Southwest China. This strategic product launch supports the company's objective to penetrate emerging markets with cost-effective solutions while complying with updated radiation safety regulations. The innovation received positive reception from dental practitioners seeking flexible imaging options outside major metropolitan areas. Source: Wisdom Digital Technologies Official Website

- •22nd May 2025, Shanghai United Imaging Healthcare Co., Ltd. announced a strategic partnership with leading dental chains to co-develop customized CBCT imaging solutions incorporating AI diagnostic features. This collaboration aims to accelerate technology adoption, improve clinician training, and expand coverage in Central China. The initiative leverages combined expertise to enhance clinical outcomes and operational efficiencies, positioning the company at the forefront of China’s dental imaging innovation landscape. Source: Shanghai United Imaging Healthcare Corporate Communications

- •5th August 2025, Neusoft Medical Systems completed the acquisition of a regional dental imaging startup specializing in handheld CBCT technology. This acquisition enhances Neusoft’s product portfolio with innovative portable devices designed for rural and remote healthcare delivery. The move supports the company's expansion strategy focused on integrating advanced imaging solutions with digital health platforms, targeting underserved markets in Northwest and Southwest China. This consolidation strengthens Neusoft’s competitive position amidst intensifying market rivalry. Source: Neusoft Medical Systems Press Announcement

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 2.5 Billion |

| CAGR | 11.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Type (Stationary CBCT, Mobile CBCT, Handheld CBCT, Industrial CBCT, Hybrid CBCT), Application (Implantology, Endodontics, Orthodontics, Oral Surgery, Periodontics), End User (Dental Hospitals, Dental Clinics, Diagnostic Centers, Academic & Research Institutes), Distribution Channel (Direct Sales, Distributors, Online Platforms, After-Sales Service Networks) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Vatech Co., Ltd. (South Korea), Carestream Health (United States), Planmeca Oy (Finland), Wisdom Digital Technologies (China), Neusoft Medical Systems (China), Shenzhen Landwind Industry Co., Ltd. (China), Soredex (Finland), Sirona Dental Systems (Germany), Morita Group (Japan), Dentsply Sirona (United States), Shanghai United Imaging Healthcare Co., Ltd. (China), Zhejiang Hengtong Medical Equipment Co., Ltd. (China), J. Morita Corporation (Japan), RadiForce Company (Japan), Anke Medical Corporation (China), Perlove Medical Technology Co., Ltd. (China), Shanghai Medicloud Technology Co., Ltd. (China), Dürr Dental SE (Germany), NewTom (Italy), Imaging Sciences International (United States), Gendex Dental Systems (United States), Orangedental (China), Wuhan Guide Infrared Co., Ltd. (China), Beijing AUSS Technology Co., Ltd. (China), Canon Medical Systems Corporation (Japan) |

China Dental CBCT Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.