Middle East Medical Waste Treatment Market - Outlook 2024-2034

Middle East Medical Waste Treatment Market is segmented by Type (Incineration Treatment, Autoclaving Treatment, Chemical Treatment, Microwaving Treatment, Landfilling Treatment), Application (Hospital Waste Management, Laboratory Waste Processing, Pharmaceutical Waste Disposal, Clinic Waste Handling, Research Facility Waste Treatment), End User (Public Hospitals, Private Hospitals, Diagnostic Laboratories, Pharmaceutical Companies, Research Institutions), Technology (Thermal Treatment Technologies, Chemical Disinfection Technologies, Mechanical Treatment Technologies), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

- •The Middle East Medical Waste Treatment market is a critical segment focused on the safe and effective management of medical waste generated by healthcare institutions such as hospitals, clinics, laboratories, pharmaceutical companies, and research facilities. This market covers a broad spectrum of treatment technologies including incineration, autoclaving, chemical treatment, microwaving, and landfilling, each designed to neutralize hazardous waste and mitigate environmental and health risks. The purpose of this market is to ensure compliance with stringent regional regulations and to facilitate sustainable disposal methods that protect public health and the environment. The scope extends across multiple countries within the Middle East, with varying adoption rates of advanced technologies driven by increasing healthcare infrastructure investments and rising awareness about biomedical waste hazards. This market's growth is further supported by government initiatives aimed at improving waste management infrastructure and encouraging eco-friendly treatment solutions to address the challenges posed by rapid urbanization and healthcare expansion.

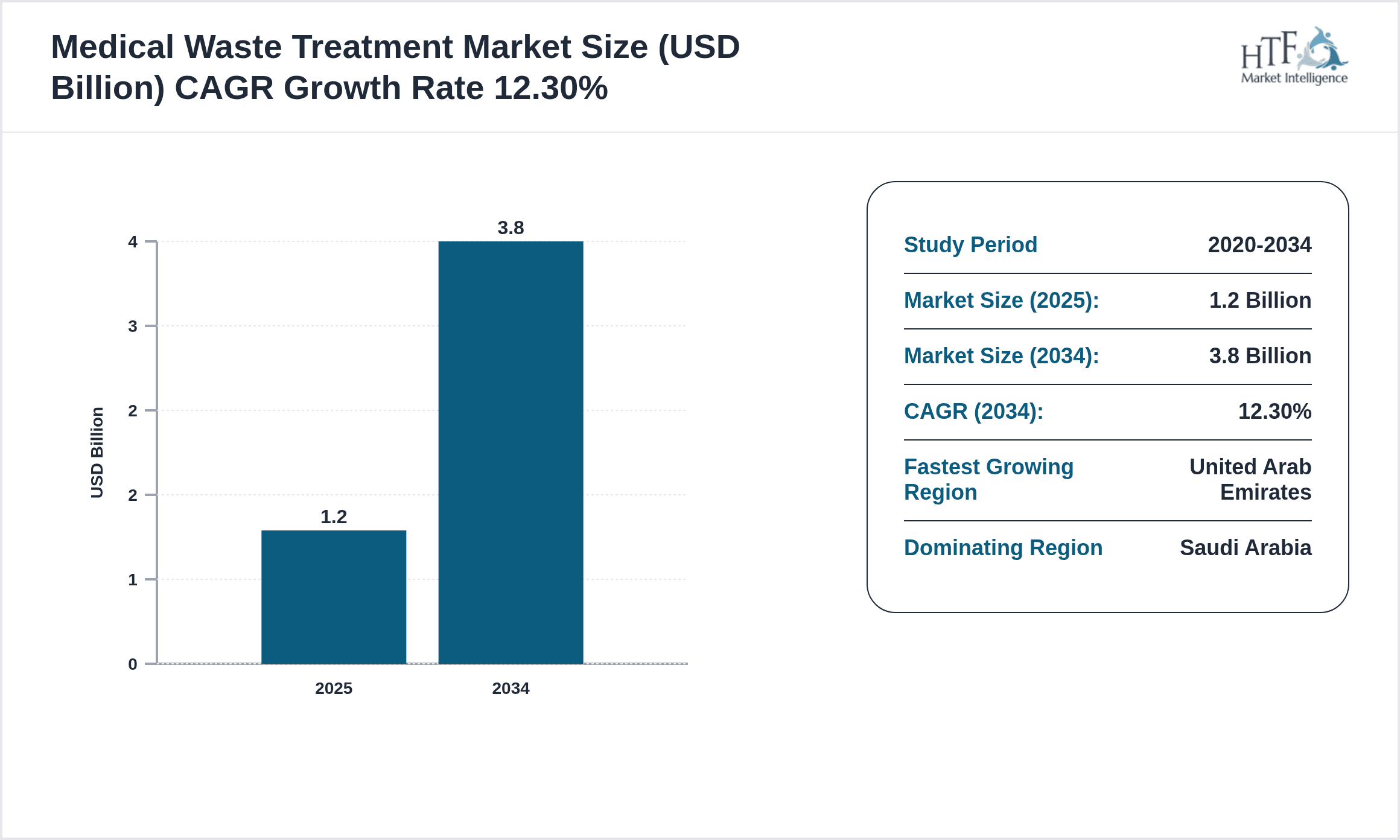

- •Key highlights of the Middle East Medical Waste Treatment market include a current valuation of USD 1.2 billion in 2024, with projections reaching USD 3.8 billion by 2034, reflecting a robust CAGR of 12.3%. Saudi Arabia dominates the market with a 35% share, driven by extensive healthcare infrastructure development and regulatory enforcement. The United Arab Emirates emerges as the fastest-growing country with a CAGR of 15.8%, fueled by innovative waste treatment technologies and increasing private healthcare investments. Incineration remains the leading treatment type, accounting for the largest market share due to its effectiveness in hazardous waste disposal, while autoclaving is the fastest-growing method given its environmental benefits. Hospital waste management is the foremost application segment, emphasizing the critical role of healthcare facilities in driving demand for efficient waste treatment solutions.

- •This market offers significant value propositions to healthcare providers, waste management companies, technology developers, and regulators by fostering sustainable and compliant waste disposal practices. It strategically supports public health protection through risk mitigation of infectious and hazardous waste, while enabling the healthcare sector to align with global environmental standards. Investments in advanced treatment technologies and infrastructure enhance operational efficiency and reduce environmental footprints, promoting long-term ecological sustainability. Stakeholders benefit from regulatory compliance, cost-effective treatment solutions, and improved community health outcomes. The growing emphasis on medical waste management as a critical environmental and health priority underscores the strategic importance of this market within the Middle East's evolving healthcare ecosystem.

Competitive Landscape

The Middle East Medical Waste Treatment market is characterized by moderate to high competition among regional and international players focusing on technological innovation, service diversification, and geographical expansion. Market leaders leverage advanced treatment technologies such as autoclaving and chemical treatment to differentiate their offerings while emphasizing compliance with evolving regional regulations. Competitive strategies include forming strategic partnerships with healthcare providers, investing in R&D to improve treatment efficiency, and adopting environmentally friendly solutions to address sustainability concerns. The rivalry is intensified by emerging local companies gaining traction through cost-effective services and tailored solutions for specific country regulations. Pricing strategies vary based on technology complexity and service scope, with premium pricing for advanced treatment methods balanced against cost-sensitive segments. Distribution channels typically involve direct contracts with hospitals and government healthcare agencies, supplemented by collaborations with waste collection and disposal firms. The market exhibits moderate entry barriers due to regulatory requirements and capital investment, ensuring a competitive yet stable environment with continuous innovation and consolidation trends shaping its future trajectory.

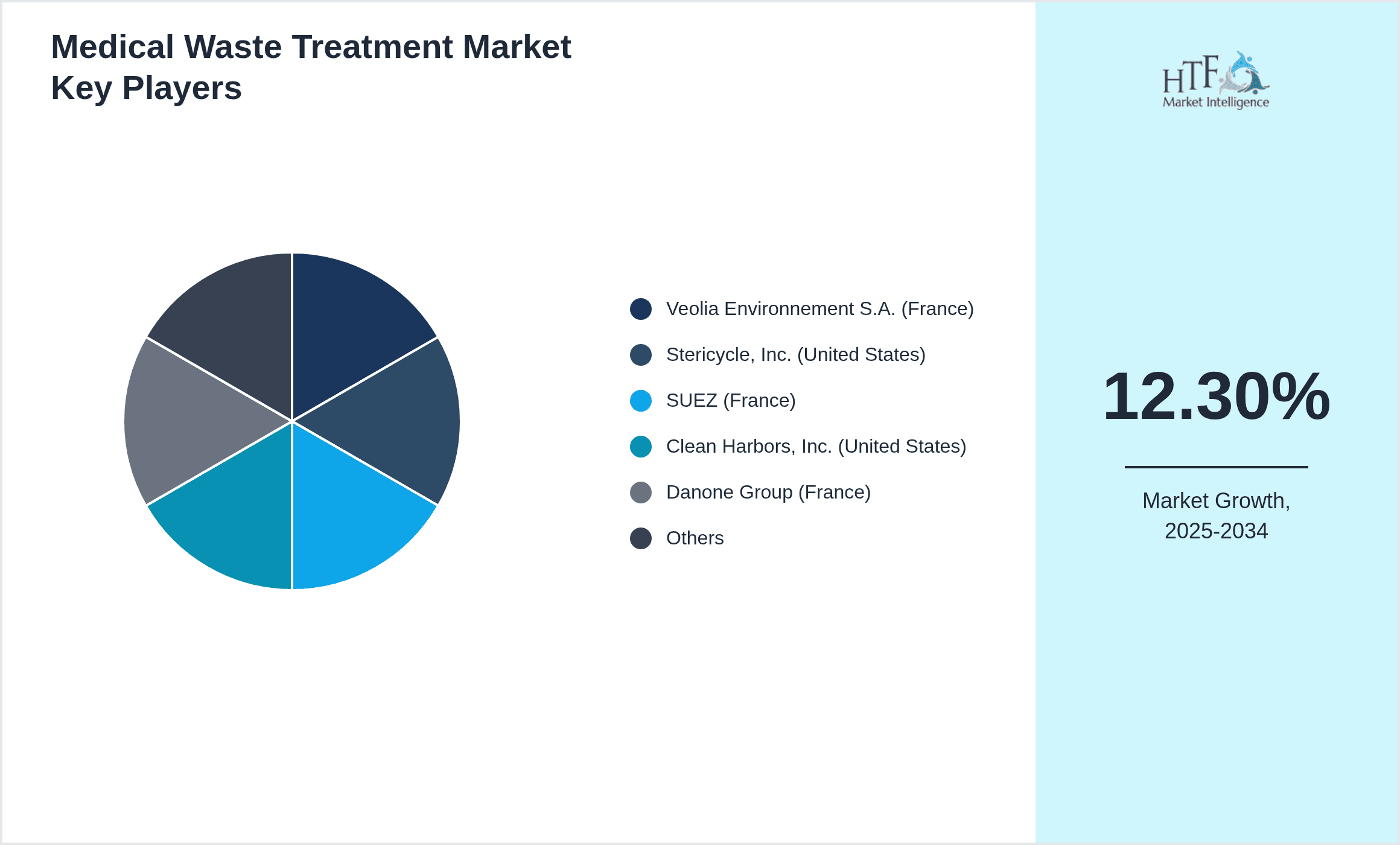

Prominent Players in Middle East Medical Waste Treatment Market

- •Veolia Environnement S.A. (France)

- •Stericycle, Inc. (United States)

- •SUEZ (France)

- •Clean Harbors, Inc. (United States)

- •Danone Group (France)

- •Transmed Waste Management (United Arab Emirates)

- •Buzwair Scientific & Technical Services (Saudi Arabia)

- •MedWaste Management LLC (United Arab Emirates)

- •Bio Medical Waste Management LLC (Saudi Arabia)

- •Environmental Waste Services LLC (Kuwait)

- •Gulf Medical Waste Solutions (Qatar)

- •Envirocare Waste Management (Oman)

- •Al Reyami Medical Waste Management (United Arab Emirates)

- •Apex Medical Waste Solutions (Saudi Arabia)

- •Al Jazeera Medical Waste Management (Qatar)

- •Arabian Environmental Solutions (Saudi Arabia)

- •Emirates Medical Waste Services (United Arab Emirates)

- •Zahra Medical Waste Management (Oman)

- •Meditech Medical Waste Services (Kuwait)

- •Al Nahda Medical Waste Management (Saudi Arabia)

- •Al Saqr Medical Waste Management (United Arab Emirates)

- •Al Fouzan Medical Waste Services (Kuwait)

- •BioSecure Medical Waste Solutions (United Arab Emirates)

- •MedPro Waste Management (Saudi Arabia)

- •Gulf Environmental Services (Qatar)

Market Breakdown

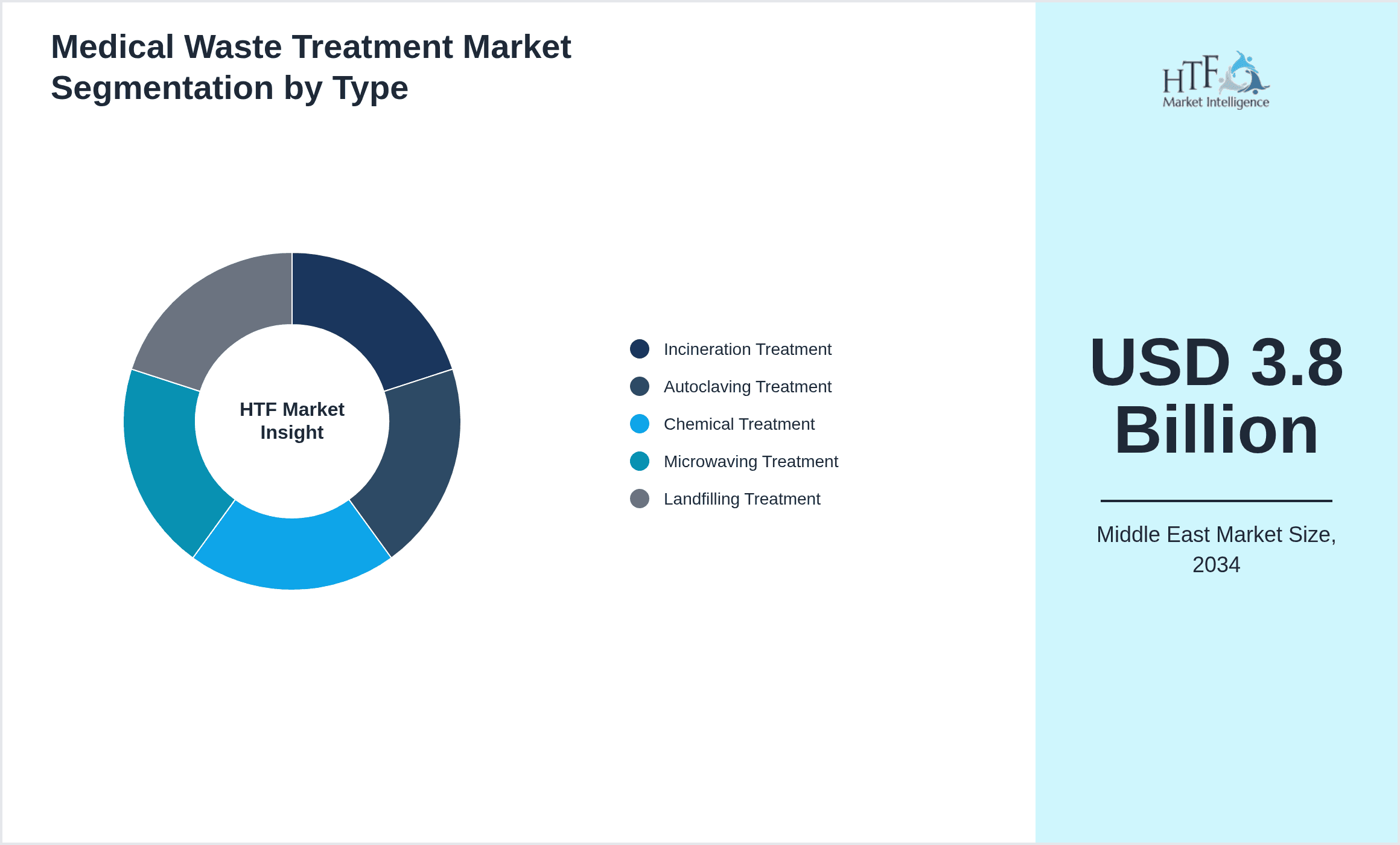

- •By Type

- ◦Incineration Treatment

- ◦Autoclaving Treatment

- ◦Chemical Treatment

- ◦Microwaving Treatment

- ◦Landfilling Treatment

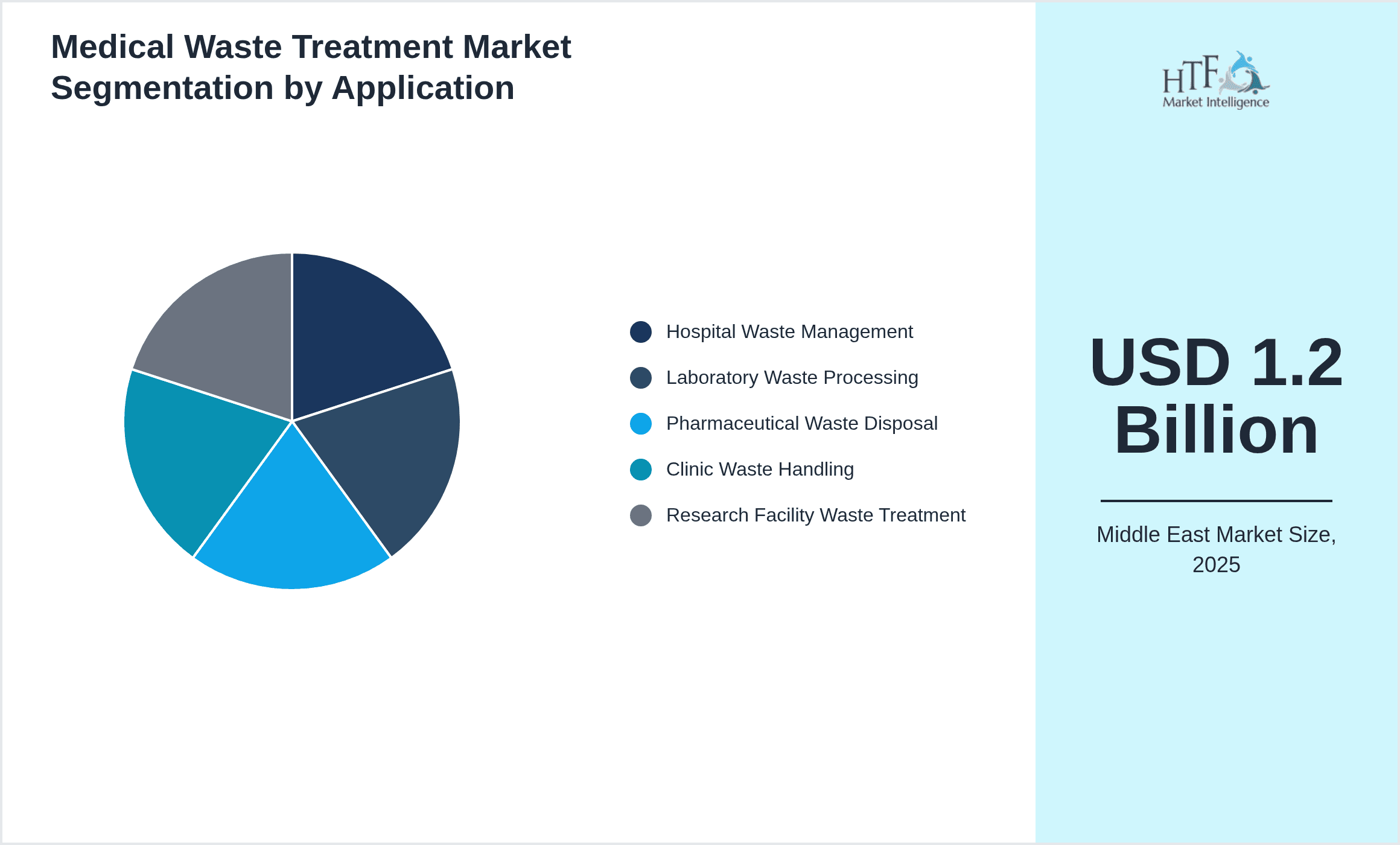

- •By Application

- ◦Hospital Waste Management

- ◦Laboratory Waste Processing

- ◦Pharmaceutical Waste Disposal

- ◦Clinic Waste Handling

- ◦Research Facility Waste Treatment

- •By End User

- ◦Public Hospitals

- ◦Private Hospitals

- ◦Diagnostic Laboratories

- ◦Pharmaceutical Companies

- ◦Research Institutions

- •By Technology

- ◦Thermal Treatment Technologies

- ◦Chemical Disinfection Technologies

- ◦Mechanical Treatment Technologies

Growth Dynamics

The Middle East Medical Waste Treatment market is primarily driven by rapid expansion in healthcare infrastructure and the corresponding increase in medical waste generation. Growing public and private investments in healthcare facilities across Saudi Arabia, UAE, and other Gulf countries amplify the demand for efficient waste treatment solutions. Additionally, stringent government regulations and environmental policies mandating safe disposal of hazardous medical waste stimulate market growth. The rising prevalence of infectious diseases and advancements in medical technologies further necessitate improved waste management. Technological innovations in autoclaving and chemical treatments offer environmentally friendly alternatives, attracting adoption. The heightened awareness about health hazards associated with improper waste disposal among healthcare providers and the public also propels market demand. Overall, these drivers collectively establish a robust growth environment and sustained market momentum through 2034.

Market Trends

A significant trend in the Middle East Medical Waste Treatment market is the increased adoption of sustainable and eco-friendly waste treatment technologies such as autoclaving and chemical disinfection, reducing reliance on traditional incineration due to environmental concerns. Public-private partnerships are emerging as crucial mechanisms for infrastructure development and service delivery. Digitalization and automation in waste tracking and management enhance operational efficiency and regulatory compliance. Furthermore, the integration of advanced monitoring systems ensures real-time waste management and reporting. Market players are also focusing on expanding their service portfolios to include comprehensive waste management solutions covering collection, transportation, treatment, and disposal. These trends reflect a shift towards holistic, environmentally conscious, and technologically advanced medical waste treatment practices in the Middle East.

Market Opportunities

The Middle East Medical Waste Treatment market presents vast opportunities for technological innovation, particularly in developing low-emission and energy-efficient treatment systems tailored for the region’s climatic and regulatory conditions. Expansion into underpenetrated countries such as Oman and Kuwait offers growth potential, supported by increasing healthcare investments. There is scope for service providers to offer integrated waste management solutions combining treatment and compliance consulting. The rising awareness campaigns about biomedical waste hazards open avenues for educational partnerships and market expansion. Additionally, collaborations with international technology providers can facilitate technology transfer and adoption of best practices. Capitalizing on government incentives and sustainability mandates can further accelerate market penetration and revenue growth.

Market Challenges

Despite promising growth, the Middle East Medical Waste Treatment market faces challenges including inconsistent regulatory frameworks across different countries, which complicate compliance and operational standardization. High capital investment requirements for advanced treatment technologies limit entry for smaller players and slow infrastructure upgrades. The shortage of skilled personnel trained in medical waste management hinders optimal service delivery and innovation. Disposal site scarcity, especially for hazardous waste landfilling, poses environmental and logistical challenges. Moreover, resistance to adopting new technologies due to cost concerns and lack of awareness among smaller healthcare providers restricts market expansion. Addressing these challenges requires coordinated regulatory harmonization, capacity building, and incentivization to foster sustainable market development.

Regulatory Framework

Between 2019 and 2024, Middle Eastern countries have implemented stricter medical waste management regulations to align with global environmental standards. Saudi Arabia introduced the Medical Waste Management Regulation in 2020, mandating waste segregation, treatment, and tracking with substantial penalties for non-compliance. The UAE updated its Federal Law on Waste Management in 2021, emphasizing eco-friendly treatment technologies and requiring licensed disposal facilities. Qatar and Kuwait enacted guidelines focusing on safe storage and transportation of infectious waste in 2019-2022. These regulations enhance market demand for compliant treatment solutions and foster investments in modern waste management infrastructure. The regulatory landscape continues to evolve with increased government oversight, incentivizing adoption of advanced technologies and improving overall medical waste treatment standards across the Middle East.

Market Intelligence

- •15th January 2024, Transmed Waste Management (United Arab Emirates) launched an innovative autoclaving system designed to optimize energy consumption and reduce emissions by 30%. This new system targets large hospitals and research facilities seeking environmentally sustainable waste treatment solutions compliant with recent UAE regulations. The launch aims to position Transmed as a leader in green medical waste technologies, addressing growing environmental concerns and regulatory pressures in the Middle East healthcare sector. The product features automated waste segregation and real-time monitoring capabilities, enhancing operational efficiency and compliance reporting.

- •22nd November 2023, Veolia Environnement S.A. (France) announced a strategic partnership with Bio Medical Waste Management LLC (Saudi Arabia) to expand hazardous waste treatment services across the Gulf region. This collaboration includes technology transfer agreements and capacity-building programs to improve treatment standards and infrastructure in Saudi Arabia and neighboring countries. The partnership aims to enhance service reach, deliver cutting-edge waste treatment technologies, and support compliance with evolving regulatory frameworks, thereby strengthening Veolia's market presence in the Middle East.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •In March 2023, Stericycle, Inc. (United States) completed the acquisition of MedWaste Management LLC (United Arab Emirates), a leading regional medical waste treatment company. This strategic move expanded Stericycle’s footprint in the Middle East, enabling it to leverage MedWaste’s established client base and local regulatory expertise. The acquisition enhances Stericycle’s service offerings by integrating advanced waste treatment technologies and strengthens its position in the growing Middle Eastern healthcare waste market, aligning with its global growth strategy focused on emerging markets.

- •In September 2022, SUEZ (France) finalized a merger with Arabian Environmental Solutions (Saudi Arabia), combining their medical waste treatment operations to create a dominant regional player. The merger facilitates resource sharing, technology integration, and expanded service coverage across Saudi Arabia and neighboring countries. This consolidation aims to improve operational efficiencies, foster innovation in waste treatment technologies, and reinforce compliance with the evolving regulatory landscape in the Middle East healthcare waste sector.

Recent Industry News

- •10th May 2024, Clean Harbors, Inc. (United States) announced the opening of a state-of-the-art medical waste treatment facility in Dubai, UAE. This facility features advanced incineration and autoclaving technologies designed to serve growing healthcare demands in the Gulf region. The expansion supports Clean Harbors’ strategic goal to enhance environmental sustainability and regulatory compliance across the Middle East medical waste management sector. Source: Company Press Release

- •18th December 2023, Bio Medical Waste Management LLC (Saudi Arabia) launched a mobile medical waste treatment unit capable of onsite autoclaving for remote healthcare facilities. This innovation addresses logistical challenges in waste management across vast and underserved areas, improving compliance and reducing transportation risks. The initiative received strong support from local health authorities aiming to promote sustainable waste practices. Source: Industry Publication

- •5th August 2022, Veolia Environnement S.A. (France) initiated a partnership with Qatar’s Ministry of Public Health to implement an integrated waste tracking and treatment system using IoT technology. This project aims to enhance transparency, efficiency, and compliance in medical waste management across public hospitals. The initiative is expected to serve as a model for other Middle Eastern countries to adopt digital solutions in waste treatment. Source: Company Website

- •30th November 2021, Transmed Waste Management (United Arab Emirates) expanded its service portfolio by introducing chemical disinfection treatment capabilities compliant with the latest UAE federal regulations. This expansion aims to cater to pharmaceutical companies and research institutions requiring specialized hazardous waste handling solutions. The move strengthens Transmed’s market position amid rising demand for diversified treatment technologies. Source: Official Press Release

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 3.8 Billion |

| CAGR | 12.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.7% |

| Scope of Report | Market is segmented by Type (Incineration Treatment, Autoclaving Treatment, Chemical Treatment, Microwaving Treatment, Landfilling Treatment), Application (Hospital Waste Management, Laboratory Waste Processing, Pharmaceutical Waste Disposal, Clinic Waste Handling, Research Facility Waste Treatment), End User (Public Hospitals, Private Hospitals, Diagnostic Laboratories, Pharmaceutical Companies, Research Institutions), Technology (Thermal Treatment Technologies, Chemical Disinfection Technologies, Mechanical Treatment Technologies) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | Veolia Environnement S.A. (France), Stericycle, Inc. (United States), SUEZ (France), Clean Harbors, Inc. (United States), Danone Group (France), Transmed Waste Management (United Arab Emirates), Buzwair Scientific & Technical Services (Saudi Arabia), MedWaste Management LLC (United Arab Emirates), Bio Medical Waste Management LLC (Saudi Arabia), Environmental Waste Services LLC (Kuwait), Gulf Medical Waste Solutions (Qatar), Envirocare Waste Management (Oman), Al Reyami Medical Waste Management (United Arab Emirates), Apex Medical Waste Solutions (Saudi Arabia), Al Jazeera Medical Waste Management (Qatar), Arabian Environmental Solutions (Saudi Arabia), Emirates Medical Waste Services (United Arab Emirates), Zahra Medical Waste Management (Oman), Meditech Medical Waste Services (Kuwait), Al Nahda Medical Waste Management (Saudi Arabia), Al Saqr Medical Waste Management (United Arab Emirates), Al Fouzan Medical Waste Services (Kuwait), BioSecure Medical Waste Solutions (United Arab Emirates), MedPro Waste Management (Saudi Arabia), Gulf Environmental Services (Qatar) |

Middle East Medical Waste Treatment Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.