Latin America Inventory Management Software Market Size, Growth & Revenue 2024-2034

Latin America Inventory Management Software Market is segmented by Inventory Management Software Type (Cloud-based Inventory Management Software, On-premise Inventory Management Software, Hybrid Inventory Management Software, AI-enabled Inventory Management Software, Mobile Inventory Management Software), Application (Warehouse Management, Retail Inventory, Manufacturing Operations, Healthcare Inventory, E-commerce Fulfillment), End User Industry (Retail Chains, Manufacturing Companies, Healthcare Providers, Logistics and Distribution, E-commerce Businesses), Deployment Model (Cloud Deployment, On-premise Deployment, Hybrid Deployment), and Geography (Brazil, Argentina, Chile, Peru, Colombia, Rest of South America)

Pricing

Report Overview

Executive Summary

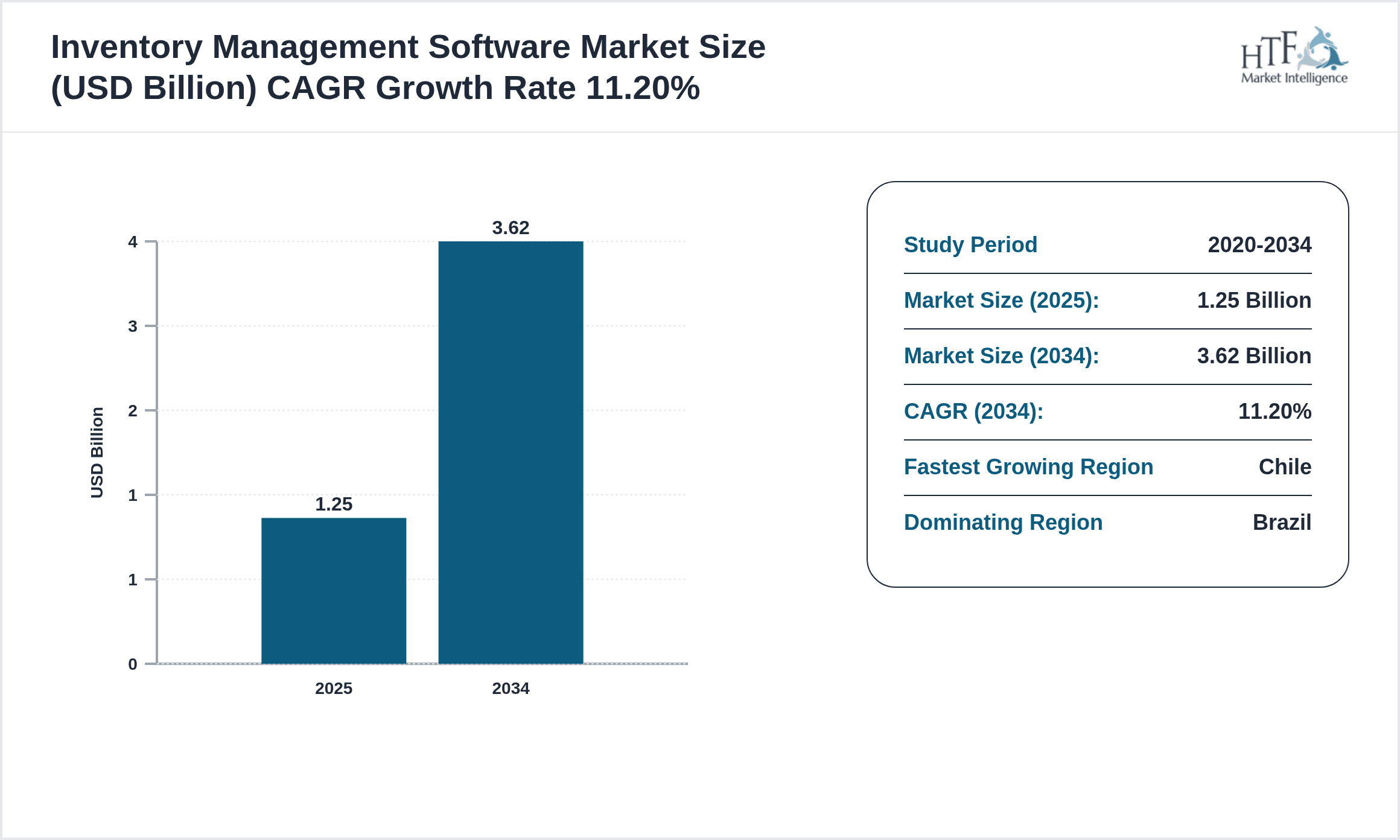

- •The Latin America Inventory Management Software market comprises comprehensive digital tools designed to streamline inventory processes across multiple sectors including retail, manufacturing, healthcare, and e-commerce. These software solutions offer real-time tracking, automated replenishment, analytics, and mobility to optimize supply chain operations. The market spans cloud-based, on-premise, hybrid, AI-enabled, and mobile inventory software types, catering to diverse user needs. Increasing digitization, demand for operational efficiency, and integration of emerging technologies like artificial intelligence drive market expansion. The software enables businesses to reduce costs, improve accuracy, and comply with regulatory standards, thereby enhancing overall competitiveness. Key geographic markets include Brazil, Argentina, Chile, Peru, and Colombia, with Brazil dominating due to its large industrial base. The forecast period from 2024 to 2034 is projected to witness robust growth, driven by rapid technology adoption, expanding e-commerce, and evolving customer expectations within the Latin American region.

- •The market is expected to grow from USD 1.25 billion in 2024 to approximately USD 3.62 billion by 2034, reflecting a CAGR of 11.2%. Cloud-based inventory management software leads with the largest market share, while AI-enabled solutions are the fastest growing segment owing to their predictive capabilities. Brazil holds the dominant position in the region, accounting for 38% market share, with Chile emerging as the fastest growing country at a CAGR of 14.5%. Significant investments in digital infrastructure and government initiatives to modernize supply chains are key growth enablers. The market landscape is shaped by competitive innovation, strategic partnerships, and increasing demand for scalable, integrated inventory solutions.

- •Inventory management software in Latin America presents strategic value to industries by enabling data-driven decisions, reducing inventory holding costs, and enhancing customer satisfaction. For stakeholders including software developers, logistics operators, and end-user businesses, the market offers opportunities to leverage cloud computing, AI, and mobile technologies. The growing complexity of supply chains and demand for omnichannel fulfillment accentuate the need for advanced inventory solutions. Consequently, market participants are focusing on innovation, customization, and regional expansion to capture emerging opportunities and address evolving operational challenges.

Competitive Landscape

The Latin America Inventory Management Software market features intense competition characterized by the presence of global leaders and strong regional players. Companies compete through continuous innovation in cloud capabilities, AI integration, and mobile platform enhancements to meet diverse customer demands. Strategic partnerships and localized solutions tailored to Latin American regulatory and business environments bolster competitive positioning. Pricing strategies vary from subscription-based cloud models to customized enterprise licenses, enabling accessibility across small to large enterprises. Market rivalry also drives investments in customer support, training, and integration services, which are critical for user adoption. Mergers and acquisitions have emerged as key tactics to consolidate market share and expand technological portfolios. Overall, the competitive landscape is dynamic, with companies prioritizing agility, innovation, and regional expertise to sustain and grow their footprint in the Latin American inventory management software sector.

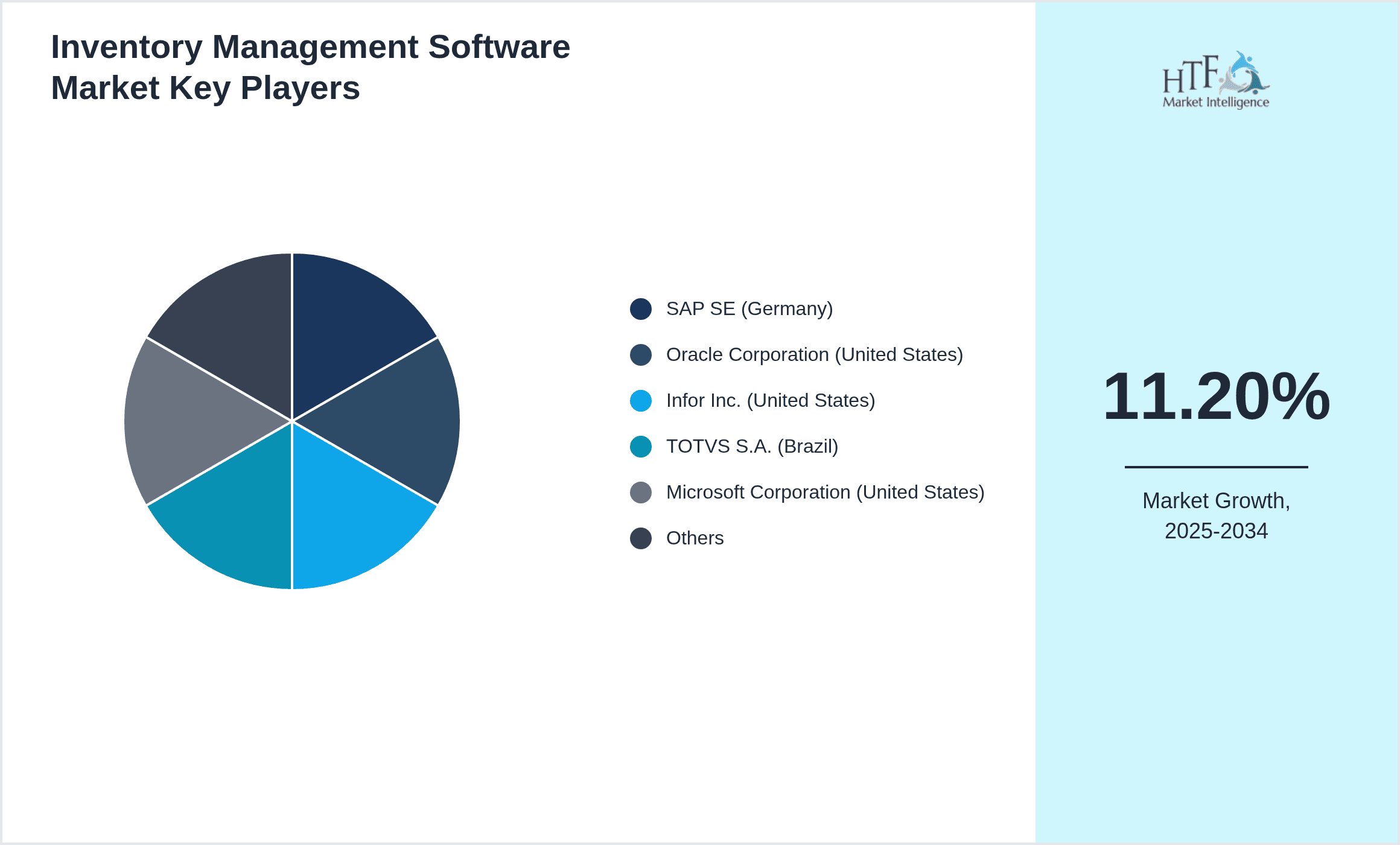

Leading Companies in Inventory Management Software Market

- •SAP SE (Germany)

- •Oracle Corporation (United States)

- •Infor Inc. (United States)

- •TOTVS S.A. (Brazil)

- •Microsoft Corporation (United States)

- •Epicor Software Corporation (United States)

- •Sage Group plc (United Kingdom)

- •NetSuite Inc. (United States)

- •IBM Corporation (United States)

- •HighJump (United States)

- •Logiwa Software (United States)

- •Netsuite (United States)

- •Fishbowl Inventory (United States)

- •Blue Yonder (United States)

- •JDA Software Group (United States)

- •Manhattan Associates (United States)

- •Linx S.A. (Brazil)

- •Senior Sistemas (Brazil)

- •TOTVS S.A. (Brazil)

- •Lintech Sistemas (Brazil)

- •Siesa (Colombia)

- •SAP Latam (Brazil)

- •Oracle Latin America (Brazil)

- •Komet Sales (Brazil)

- •Softland (Chile)

Market Breakdown

- •By Inventory Management Software Type

- ◦Cloud-based Inventory Management Software

- ◦On-premise Inventory Management Software

- ◦Hybrid Inventory Management Software

- ◦AI-enabled Inventory Management Software

- ◦Mobile Inventory Management Software

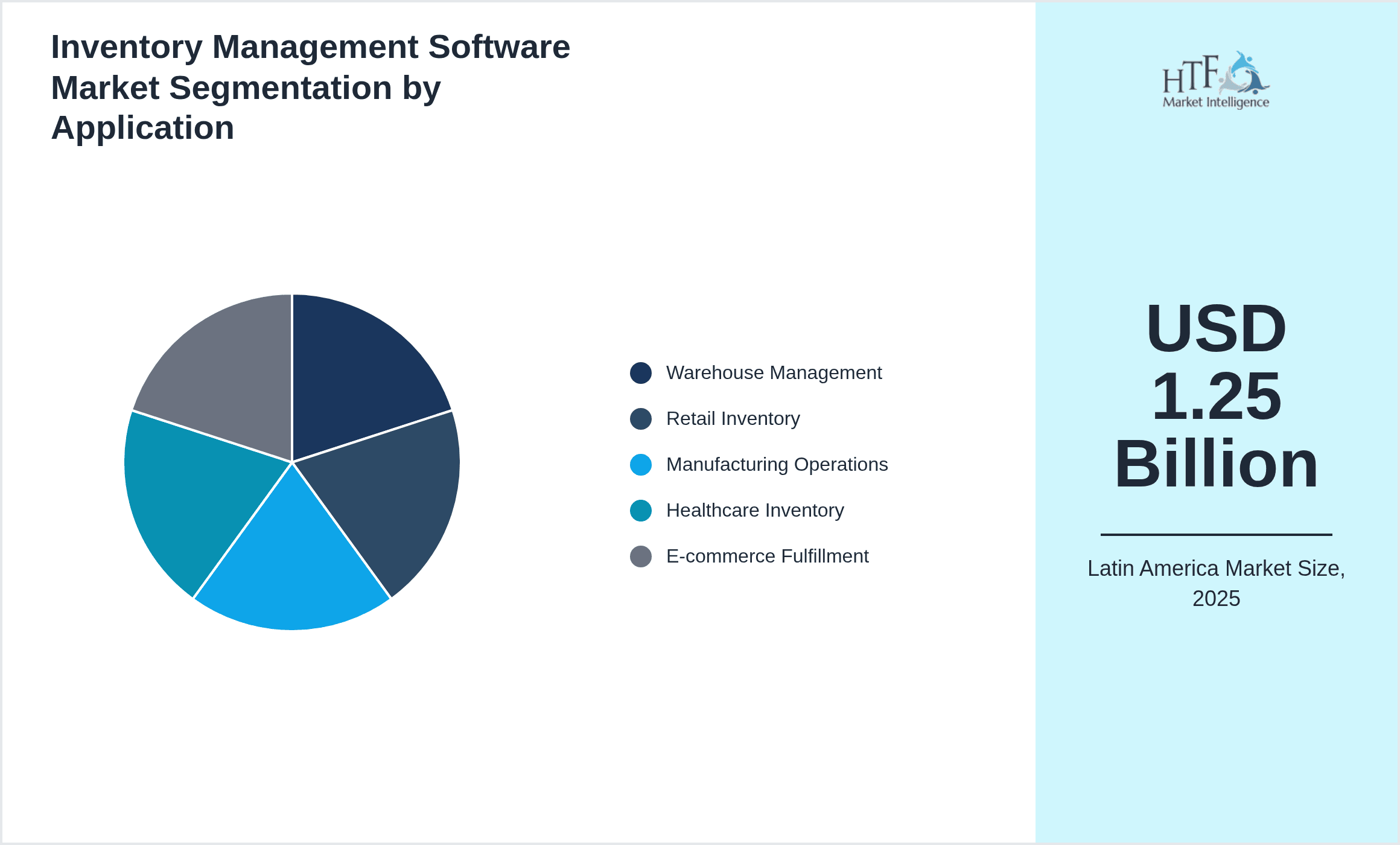

- •By Application

- ◦Warehouse Management

- ◦Retail Inventory

- ◦Manufacturing Operations

- ◦Healthcare Inventory

- ◦E-commerce Fulfillment

- •By End User Industry

- ◦Retail Chains

- ◦Manufacturing Companies

- ◦Healthcare Providers

- ◦Logistics and Distribution

- ◦E-commerce Businesses

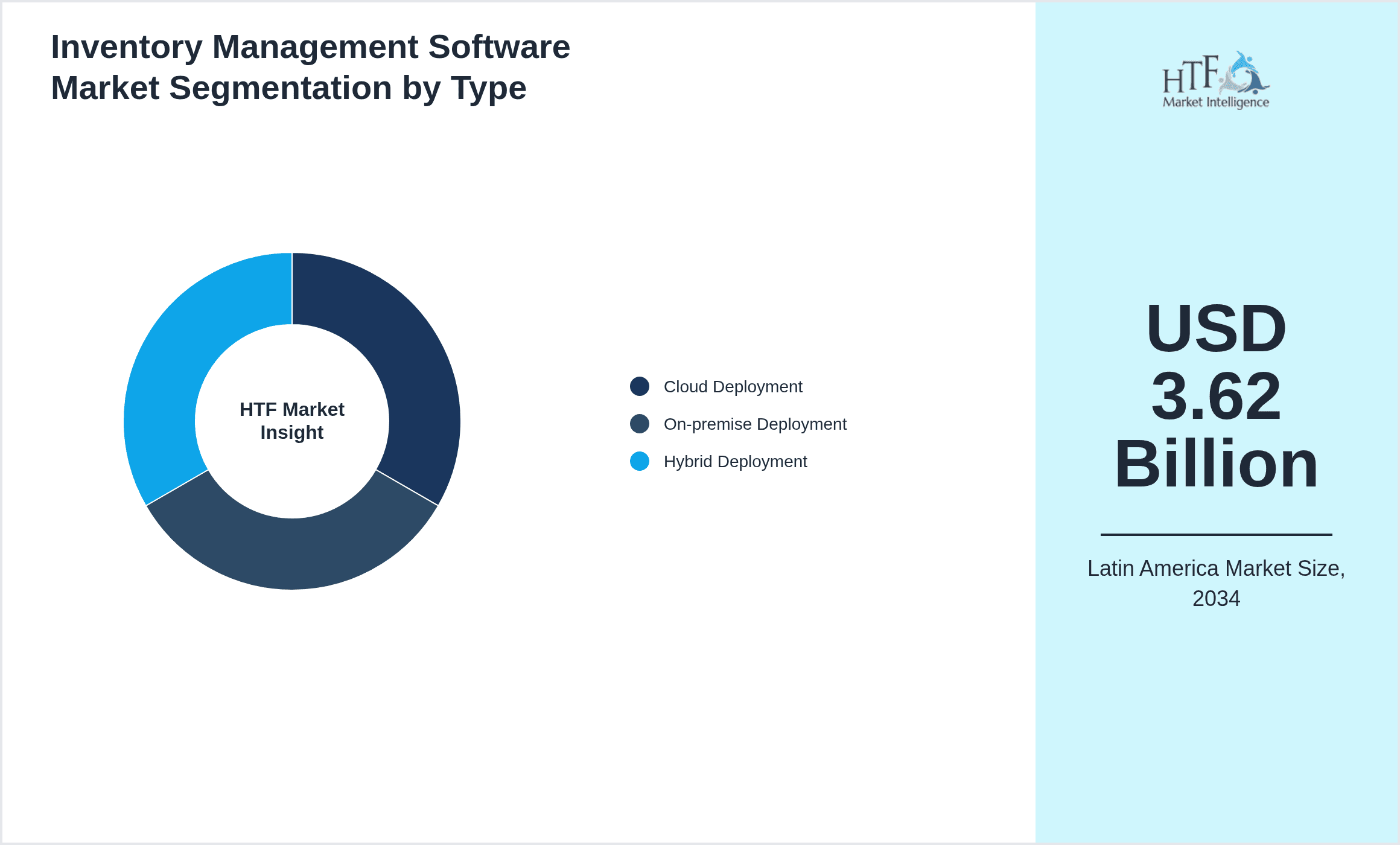

- •By Deployment Model

- ◦Cloud Deployment

- ◦On-premise Deployment

- ◦Hybrid Deployment

Growth Dynamics

- •The growing penetration of cloud technologies across Latin America is a major driver, enabling scalable and cost-efficient inventory management solutions that appeal to SMEs and large enterprises alike. Cloud adoption reduces upfront costs and enhances accessibility, accelerating market expansion.

- •E-commerce growth in countries like Brazil and Argentina fuels demand for real-time inventory tracking and fulfillment optimization, prompting businesses to invest in advanced software platforms that support omnichannel operations and improve customer experience.

- •Government initiatives promoting digital transformation and smart logistics infrastructure in key Latin American economies provide impetus for inventory software adoption, including incentives for technology modernization and data-driven supply chain management.

- •Increasing complexity of supply chains and heightened competition drive the need for AI-enabled inventory solutions capable of predictive analytics, demand forecasting, and automated replenishment, enhancing operational efficiency and reducing stockouts.

- •Rising mobile device usage among operational staff encourages deployment of mobile inventory management software, facilitating real-time updates and better on-ground coordination across warehouses, retail outlets, and delivery networks.

Market Trends

- •Integration of artificial intelligence and machine learning into inventory management software is becoming widespread, allowing for enhanced demand prediction, anomaly detection, and automated decision-making, which significantly improve supply chain responsiveness.

- •The shift towards cloud-native software architectures supports seamless scalability and continuous updates, enabling Latin American businesses to rapidly adapt to changing market conditions and increasing inventory complexity.

- •Sustainability initiatives are influencing inventory management practices, with companies adopting software that optimizes stock levels to reduce waste and carbon footprints, aligning with global environmental goals.

- •Collaboration between software vendors and logistics providers is intensifying, fostering integrated platforms that combine inventory data with transportation management for holistic supply chain visibility.

- •Mobile-first inventory applications are gaining traction, driven by the growing workforce mobility and the need for real-time data access across dispersed locations in the Latin American region.

Market Opportunities

- •Expanding internet penetration and digital literacy in Latin America present opportunities to onboard traditionally underserved small and medium enterprises into inventory management software adoption, fostering market growth.

- •Emerging markets in countries like Peru and Colombia show increasing demand for customized inventory solutions tailored to local regulatory and operational requirements, representing untapped potential.

- •Integration of AI with IoT devices for smart inventory tracking offers innovation avenues to improve accuracy and reduce manual interventions, appealing to industries with complex supply chains.

- •Strategic partnerships between Latin American software providers and global technology firms can facilitate knowledge transfer, enhance product portfolios, and accelerate market penetration.

- •Growth in e-commerce logistics and last-mile delivery services demands advanced inventory synchronization solutions, creating opportunities for specialized software development and deployment.

Market Challenges

- •Economic volatility and currency fluctuations in Latin American countries pose risks to IT investments, affecting customers’ willingness to adopt or upgrade inventory management systems.

- •Limited IT infrastructure and inconsistent internet connectivity in rural and remote areas hinder widespread deployment of cloud-based inventory solutions, restricting market reach.

- •Data privacy and cross-border data transfer regulations vary across Latin American countries, complicating compliance for multinational software providers and users.

- •Shortage of skilled IT professionals and digital transformation expertise delays implementation and reduces the effectiveness of inventory management software adoption.

- •Resistance to change among traditional industries and smaller businesses slows the transition from manual to automated inventory systems, limiting market penetration.

Regulatory Framework

- •Between 2019 and 2024, Latin American countries have enacted data protection laws aligned with global standards such as GDPR, including Brazil’s LGPD (Lei Geral de Proteção de Dados) in 2020, mandating stringent data privacy and security measures for inventory software providers.

- •Regulations promoting digital invoicing and tax reporting, such as Mexico’s CFDI system and Chile’s electronic invoicing mandates, require inventory management software to integrate compliant financial modules, impacting software design and deployment.

- •Environmental regulations emphasizing sustainable supply chain practices have led to government incentives encouraging adoption of inventory solutions that track and reduce waste, particularly in Brazil and Argentina.

- •Standards for cybersecurity and IT governance, including frameworks adapted from ISO/IEC standards, are increasingly enforced by regulatory bodies, necessitating robust security features in inventory management platforms.

- •Trade facilitation policies and customs modernization initiatives across Latin America promote interoperability between inventory software and government systems, facilitating smoother cross-border logistics and compliance.

Market Intelligence

- •15th February 2025, TOTVS S.A. launched an AI-powered inventory optimization module integrated within its cloud ERP platform, targeting mid-sized Latin American retailers. The new feature leverages machine learning to forecast demand and automate stock replenishment, aiming to reduce overstock and stockouts while improving customer satisfaction. This strategic enhancement aligns with the growing adoption of AI in the regional inventory management market and reinforces TOTVS’s position as a leading local software provider. The launch is expected to accelerate digital transformation among retail chains across Brazil, Argentina, and Chile, addressing key operational challenges with advanced analytics and automation.

- •10th July 2024, Oracle Corporation expanded its Latin America footprint by opening a new cloud data center in São Paulo, Brazil, enhancing service delivery for its Inventory Management Software suite. This move significantly reduces latency and compliance concerns for regional customers, facilitating faster adoption of cloud-based inventory solutions. Oracle’s investment underscores the strategic importance of Latin America as a growth market for enterprise software and aims to support industries such as manufacturing and logistics with scalable, secure cloud infrastructure. The new data center also enables integration with Oracle’s AI and IoT capabilities, providing customers with cutting-edge inventory optimization tools.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Brazil currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Chile is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Brazil

- Argentina

- Chile

- Peru

- Colombia

- Rest of South America

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 3.62 Billion |

| CAGR | 11.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.2% |

| Scope of Report | Market is segmented by Inventory Management Software Type (Cloud-based Inventory Management Software, On-premise Inventory Management Software, Hybrid Inventory Management Software, AI-enabled Inventory Management Software, Mobile Inventory Management Software), Application (Warehouse Management, Retail Inventory, Manufacturing Operations, Healthcare Inventory, E-commerce Fulfillment), End User Industry (Retail Chains, Manufacturing Companies, Healthcare Providers, Logistics and Distribution, E-commerce Businesses), Deployment Model (Cloud Deployment, On-premise Deployment, Hybrid Deployment) |

| Regions Covered | Brazil, Argentina, Chile, Peru, Colombia, Rest of South America |

| Key Companies | SAP SE (Germany), Oracle Corporation (United States), Infor Inc. (United States), TOTVS S.A. (Brazil), Microsoft Corporation (United States) |

Latin America Inventory Management Software Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.