EMEA Automatic Doors Market - Outlook 2024-2034

EMEA Automatic Doors Market is segmented by Type (Sliding Doors, Swing Doors, Revolving Doors, Folding Doors, Hermetic Doors), Application (Commercial Buildings, Healthcare Facilities, Transportation Hubs, Residential Complexes, Industrial Facilities), End User Segment (Public Sector, Private Enterprises, Retail Chains, Hospitality Industry, Manufacturing Units), Technology (Sensor-Based Automation, IoT-Enabled Doors, Manual-Assist Automatic Doors, Energy Efficient Doors), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Automatic Doors market comprises advanced automated access solutions designed for diverse applications such as commercial buildings, healthcare centers, transportation hubs, residential complexes, and industrial facilities. It includes various door types like sliding, swing, revolving, folding, and hermetic doors, integrating sensor and automation technologies to improve accessibility, security, and energy efficiency. This market plays a critical role in modern infrastructure development across Europe, the Middle East, and Africa, adapting to regional standards and climatic conditions. It serves a broad customer base including facility managers, architects, and end-users seeking seamless entrance solutions. The market is driven by rapid urbanization, smart building adoption, and rising demand for contactless access systems, positioning automatic doors as essential components in sustainable and intelligent building ecosystems across the EMEA region.

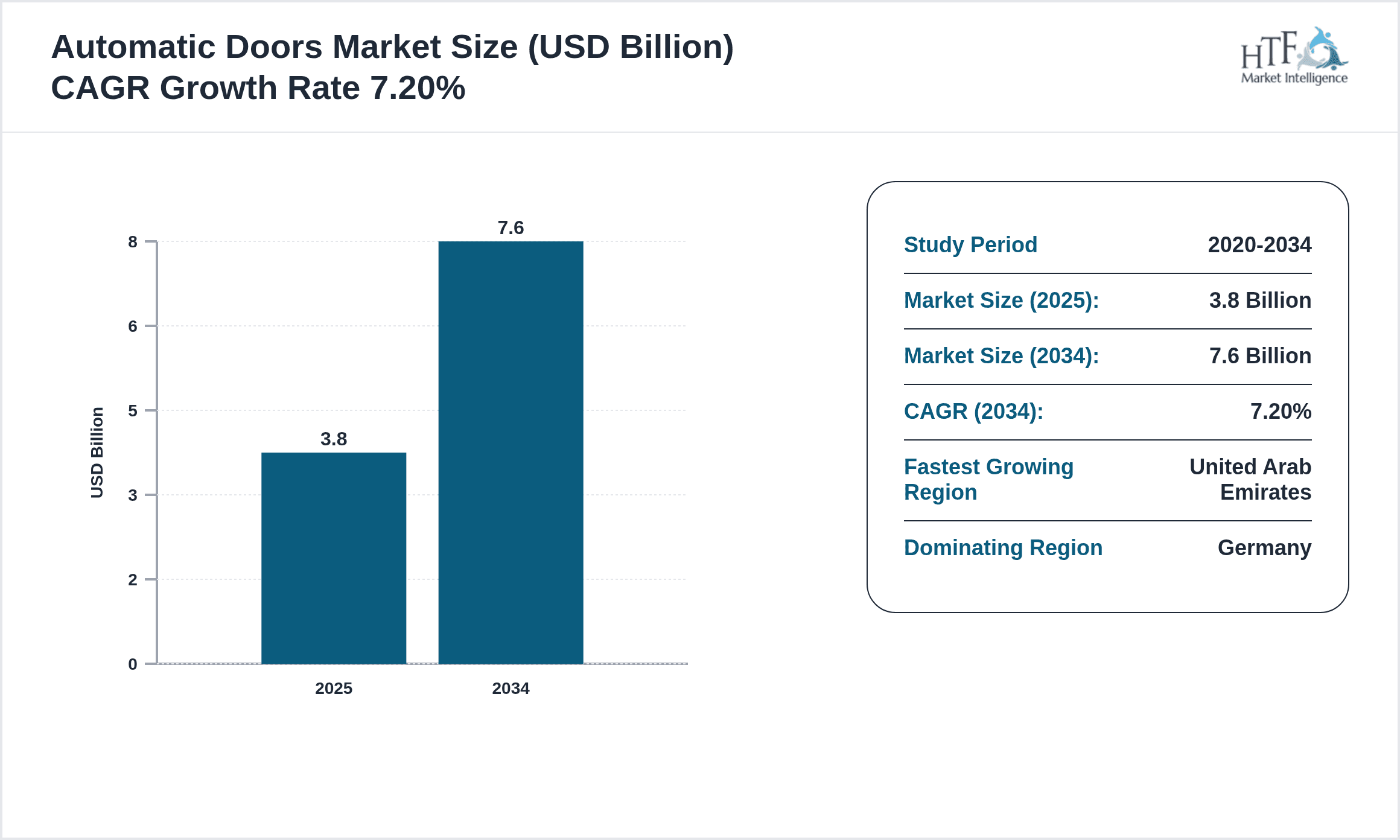

- •Key highlights of the EMEA Automatic Doors market include a base market size of USD 3.8 Billion in 2024, forecasted to reach USD 7.6 Billion by 2034, representing a CAGR of 7.2%. Sliding doors dominate the product segment with significant market share, while folding doors exhibit the fastest growth trajectory. Germany leads the market by share, followed by France and the UK, with the United Arab Emirates emerging as the fastest growing country within the region. Increasing infrastructure projects, technological integration, and regulatory frameworks supporting energy-efficient building components propel market expansion. The market also witnesses evolving customer preferences toward smart, secure, and hygienic access solutions, reinforcing long-term growth potential.

- •The EMEA Automatic Doors market holds strategic importance for stakeholders across construction, real estate, healthcare, and transportation sectors by enhancing building functionality and safety. It offers value through seamless user experience, energy conservation, and compliance with stringent regional standards. Manufacturers and service providers benefit from continuous innovation in sensor technology and connectivity, enabling differentiation and competitive advantage. Investors find promising opportunities in the rising adoption of automated access systems driven by urbanization and smart city initiatives. The market’s dynamic nature requires emphasis on regulatory compliance, technological advancement, and regional customization, ensuring sustained value creation and industry relevance within the evolving built environment landscape of EMEA.

Competitive Landscape

The competitive environment in the EMEA Automatic Doors market is characterized by intense rivalry among global and regional players striving to innovate and expand their market presence. Companies focus on developing advanced automation technologies, including sensor integration, IoT-enabled access control, and energy-efficient door systems to differentiate offerings. Strategic partnerships and investments in R&D drive product enhancements and customization capabilities addressing diverse regional regulations and customer needs. Market leaders leverage extensive distribution networks and comprehensive service portfolios to secure dominant positions across key countries such as Germany, France, and the UAE. Pricing strategies balance cost competitiveness with quality and technological sophistication. Barriers to entry include high capital investment, regulatory compliance, and the need for strong technical expertise. Future trends indicate increased collaboration between technology providers and construction firms, accelerating adoption of smart access solutions and reinforcing competitive dynamics.

Leading Companies in EMEA Automatic Doors Market

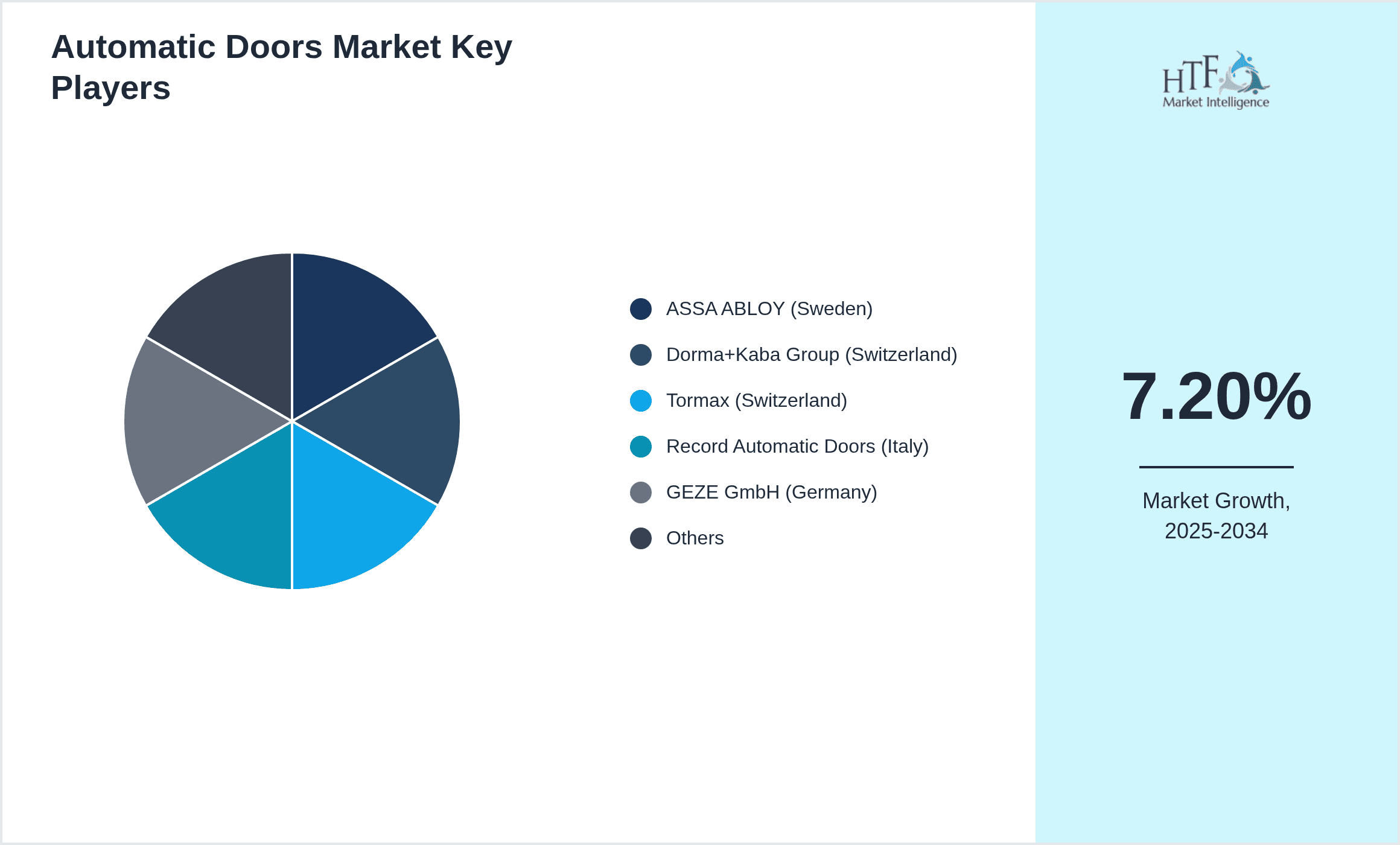

- •ASSA ABLOY (Sweden)

- •Dorma+Kaba Group (Switzerland)

- •Tormax (Switzerland)

- •Record Automatic Doors (Italy)

- •GEZE GmbH (Germany)

- •Boon Edam (Netherlands)

- •Crawford (Sweden)

- •Porta Systems (Turkey)

- •Hormann Group (Germany)

- •TSA UK Ltd (United Kingdom)

- •Albany Doors (United Kingdom)

- •Besam Entrance Solutions (Sweden)

- •Record Doors (Italy)

- •Porteo (France)

- •Rite-Hite Europe (Belgium)

- •Kaba Group (Switzerland)

- •Norton Door Controls (United Kingdom)

- •EFAFLEX Tor- und Sicherheitssysteme GmbH (Germany)

- •Interflex Group (Germany)

- •Centurion Systems (United Kingdom)

- •Stanley Access Technologies (United Kingdom)

- •Hörmann UK (United Kingdom)

- •Besam Entrance Solutions (UK/Sweden)

- •G-U Door Controls (Germany)

- •Record Italia (Italy)

Market Breakdown

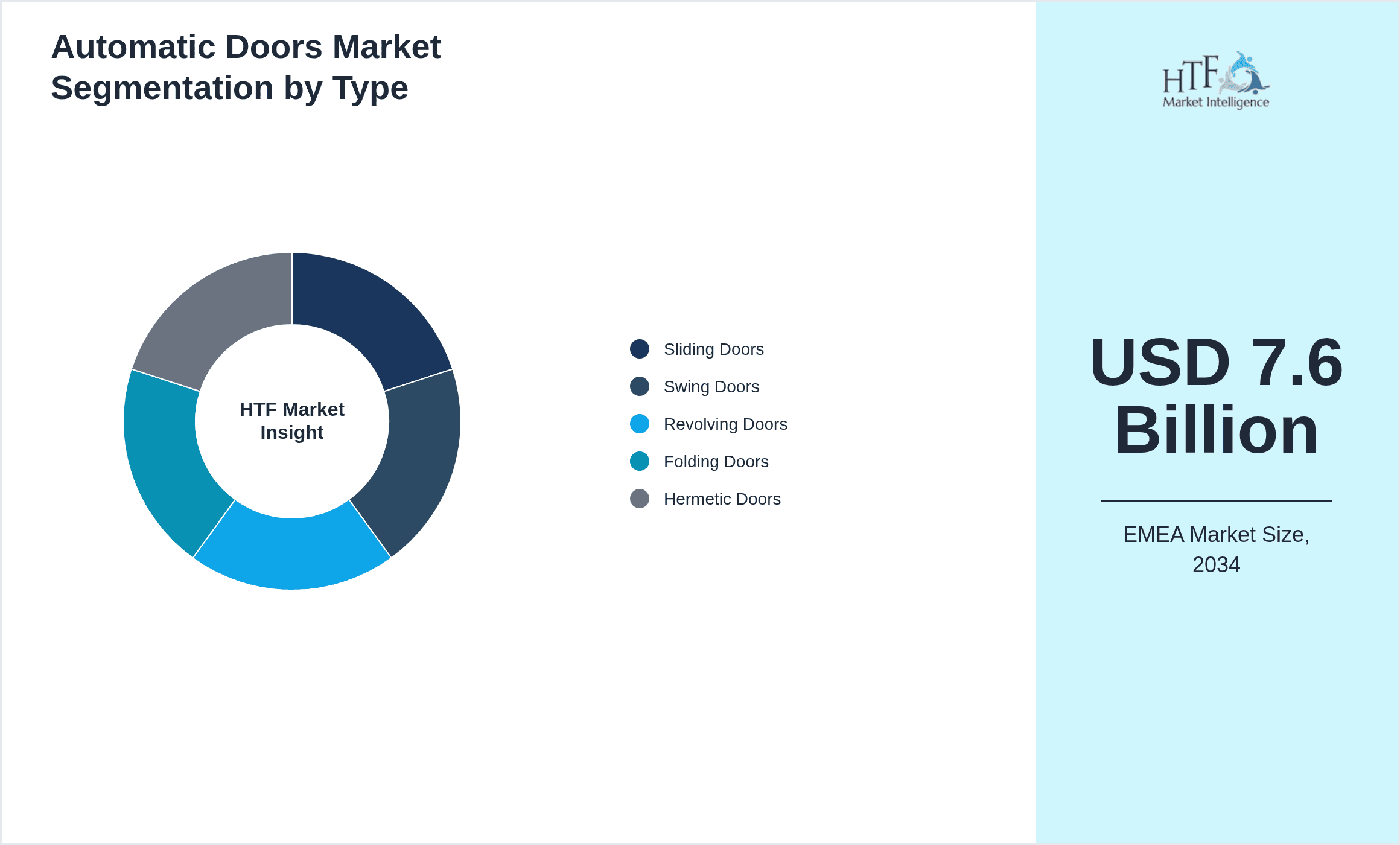

- •By Type

- ◦Sliding Doors

- ◦Swing Doors

- ◦Revolving Doors

- ◦Folding Doors

- ◦Hermetic Doors

- •By Application

- ◦Commercial Buildings

- ◦Healthcare Facilities

- ◦Transportation Hubs

- ◦Residential Complexes

- ◦Industrial Facilities

- •By End User Segment

- ◦Public Sector

- ◦Private Enterprises

- ◦Retail Chains

- ◦Hospitality Industry

- ◦Manufacturing Units

- •By Technology

- ◦Sensor-Based Automation

- ◦IoT-Enabled Doors

- ◦Manual-Assist Automatic Doors

- ◦Energy Efficient Doors

Growth Dynamics

- •The EMEA Automatic Doors market growth is propelled by increasing urbanization and infrastructural development across Europe, the Middle East, and Africa. Expanding commercial real estate projects and modernization of existing buildings fuel demand for automated access solutions. Technological advancements such as sensor integration and IoT connectivity enhance door functionalities, driving adoption. Additionally, growing awareness of energy efficiency and building sustainability, supported by regional regulations, incentivizes investments in automatic doors with advanced insulation and control features. The rising need for contactless access systems, accelerated by health and hygiene concerns post-pandemic, further boosts market expansion. Collectively, these factors create a robust environment for market growth through 2034.

- •Trends in the EMEA Automatic Doors market include the adoption of smart building technologies that integrate automatic doors with building management systems for enhanced security and energy management. There is a marked shift towards eco-friendly materials and energy-efficient designs, complying with stringent European Union directives. The Middle East is witnessing increased infrastructure investments supporting state-of-the-art transit hubs equipped with advanced revolving and sliding doors. Additionally, modular and customizable door systems are gaining traction, allowing for tailored solutions across various sectors. The integration of AI and predictive maintenance features is emerging, enhancing operational reliability and reducing downtime, shaping future market directions.

- •Market restraints include high initial installation costs and complex integration requirements with existing building systems that may deter smaller enterprises. Regulatory compliance across diverse EMEA countries involves navigating varying safety and accessibility standards, adding complexity and cost. Limited awareness about long-term benefits of automatic doors in some regions restricts market penetration. Moreover, supply chain disruptions and rising raw material prices impact manufacturing and delivery timelines. Resistance to change in traditional construction practices slows adoption rates in certain segments. These factors collectively pose challenges to faster market growth despite strong demand drivers.

- •Opportunities in the EMEA Automatic Doors market arise from expanding smart city initiatives and government infrastructure projects that prioritize accessible and energy-efficient building components. The healthcare sector’s growing demand for hygienic, touchless entry systems presents significant potential. Emerging markets within Africa and the Middle East offer untapped growth avenues due to increasing urban development and modernization efforts. Innovations in door automation technology, such as AI-based predictive maintenance and integration with security systems, open paths for new product offerings. Collaborations between technology providers and construction firms can accelerate adoption, while retrofitting older structures with automatic doors provides additional market scope.

- •Challenges facing the EMEA Automatic Doors market include managing the complexity of adhering to diverse regional regulations spanning safety, accessibility, and environmental standards. The high cost of advanced technology integration can limit adoption in price-sensitive segments. Skilled labor shortages and technical expertise gaps affect installation and maintenance quality. Intense competition drives pricing pressures, potentially impacting profitability. Additionally, fluctuating raw material costs and geopolitical uncertainties in parts of the Middle East and Africa create supply chain vulnerabilities. Companies must also address cybersecurity risks associated with IoT-enabled door systems to ensure user safety and privacy, necessitating robust security frameworks.

Market Trends

- •The EMEA Automatic Doors market is witnessing a growing trend towards integration of IoT and smart sensors, enabling remote monitoring and predictive maintenance which reduce operational costs and downtime. Energy-efficient door systems designed to improve building insulation and reduce HVAC loads are increasingly favored amid stricter environmental regulations. The adoption of contactless access solutions has surged due to heightened hygiene awareness post-pandemic, influencing product designs and customer preferences. Additionally, modular and customizable door solutions allow for flexible installation in diverse architectural settings, gaining traction across commercial and residential sectors. Regional infrastructure investments, especially in transportation hubs and healthcare, drive demand for high-performance automatic door systems equipped with advanced security features.

- •Sustainability is a key market trend, with manufacturers focusing on eco-friendly materials and energy-saving technologies in automatic doors to comply with European Union directives and national regulations. Collaboration between door manufacturers and smart building system providers is increasing to deliver integrated solutions enhancing safety and energy management. The rise of AI-powered automation for adaptive door control and fault detection is setting new benchmarks in operational efficiency. The Middle East’s infrastructural modernization fuels demand for aesthetically advanced and durable door systems. Additionally, digitalization in supply chain and service processes enhances customer experience and after-sales support, further shaping market innovation and growth.

- •The trend towards urbanization and smart city development across the EMEA region is influencing the proliferation of automated door systems in commercial and public infrastructure projects. Emphasis on universal accessibility standards is driving demand for compliant door solutions in healthcare and public facilities. Technological advancements such as integration of biometric access control and AI-driven analytics are gaining momentum. The refurbishment of aging infrastructure with modern automatic doors presents another growth vector. Furthermore, increased focus on user convenience and experience is pushing manufacturers to innovate in design and functionality, supporting broader market expansion.

- •Digital transformation initiatives within the building automation sector are fostering the adoption of connected automatic doors, offering enhanced control and data analytics capabilities. The convergence of safety, security, and energy efficiency requirements is prompting the development of multi-functional door systems. Manufacturers are investing in R&D to improve door durability and weather resistance, catering to diverse climatic conditions across EMEA. Partnerships between technology firms and construction companies optimize project execution and solution integration, reinforcing market competitiveness. The growing importance of building certifications related to green and smart buildings further accelerates the deployment of advanced automatic door technologies.

- •Consumer preferences are evolving towards seamless, hygienic, and energy-efficient entrance solutions, driving demand for automatic doors with advanced sensor technologies and minimal physical contact. The expansion of retail, hospitality, and healthcare sectors in EMEA fosters increased installation of automatic door systems tailored to specific environmental and traffic requirements. Market segmentation based on end-user needs encourages specialized product developments. Moreover, the integration of automatic doors with security and fire safety systems reflects a holistic approach to building safety. These trends underscore a shift towards comprehensive, intelligent entry management solutions that enhance occupant experience and operational sustainability.

- •Emerging technologies such as AI-enabled adaptive control and machine learning for predictive maintenance are shaping the future of the EMEA Automatic Doors market. Increasing adoption of cloud-based management platforms allows for centralized monitoring and enhanced operational efficiency. The trend towards modular, scalable door systems facilitates easier customization and upgrades, meeting dynamic market demands. Sustainability considerations are driving innovation in materials and energy consumption reduction. Furthermore, collaborations between startups and established manufacturers are accelerating technology diffusion. These developments position the market for continued expansion and technological leadership in automated access solutions across EMEA.

- •Forward-looking market dynamics emphasize the integration of automatic doors with broader smart infrastructure ecosystems, enabling interoperability with lighting, HVAC, and security systems. The rise of predictive analytics and fault diagnosis tools enhances preventive maintenance, reducing lifecycle costs. Industry focus on user-centric design and accessibility compliance fosters inclusive solutions across diverse demographics. Expansion into emerging EMEA markets with rapid urban growth creates new revenue streams. Additionally, regulatory support for energy-efficient construction materials propels the adoption of advanced door technologies. These strategic trends set the stage for sustained innovation and competitive differentiation in the EMEA Automatic Doors market.

Market Opportunities

- •Infrastructure modernization projects across EMEA present significant opportunities for automatic door manufacturers, particularly in commercial and transportation segments where demand for efficient access solutions is rising. Retrofitting older buildings with energy-efficient and contactless doors offers an expanding market niche. The healthcare sector’s increasing emphasis on infection control drives uptake of hygienic automatic doors, boosting sales. Emerging economies within Africa and the Middle East provide untapped potential due to accelerating urbanization and construction activities. Moreover, growing interest in integrated building management systems creates avenues for technological partnerships and product innovation, enabling companies to capture higher market shares.

- •Expanding smart city initiatives across Europe and the Middle East create avenues for automatic doors integrated with IoT and AI technologies, offering enhanced security and operational efficiency. Development of customizable door solutions tailored to diverse architectural and climatic requirements addresses specific customer demands. The rise of green building certifications incentivizes adoption of energy-saving door technologies. Additionally, strategic alliances between manufacturers and construction firms facilitate faster market penetration and innovation. Export opportunities to emerging EMEA markets with infrastructure deficits further augment growth prospects for established players.

- •Investment in research and development focused on AI-driven automation and predictive maintenance represents a lucrative opportunity to differentiate products and improve customer retention. The increasing use of eco-friendly materials and sustainable manufacturing practices aligns with regulatory trends, enhancing brand reputation and access to new customer segments. Expanding digital distribution channels and after-sales service platforms improve market reach and customer satisfaction. Furthermore, partnerships with technology startups foster innovation and accelerate time-to-market for advanced automatic door solutions, strengthening competitive positioning.

- •Diversification into niche applications such as hermetic doors for cleanrooms and controlled environments in pharmaceutical and semiconductor industries offers specialized growth segments. The commercial real estate sector's focus on occupant comfort and security drives demand for versatile door systems with integrated access control and energy management features. Developing retrofit kits for existing door infrastructure facilitates market expansion among cost-conscious customers. Additionally, leveraging data analytics from connected door systems provides opportunities for service innovation and new business models based on predictive maintenance and performance optimization.

- •Geographical expansion into underpenetrated African and Middle Eastern markets is a strategic opportunity given increasing investments in urban infrastructure and smart building projects. Tailoring product portfolios to local regulatory and environmental conditions enhances acceptance and market share. Collaborations with regional distributors and service providers improve market access and customer service. Growing demand for barrier-free access solutions in public and private sectors supports diversified product offerings. These factors collectively create a favorable environment for sustained growth and competitive advantage in the EMEA Automatic Doors market.

- •Emerging technologies such as voice-activated and gesture-controlled automatic doors open innovative product development paths, enhancing user experience and accessibility. Integration with building security ecosystems using biometric and AI-based authentication provides differentiation and value addition. The increasing role of government incentives for energy-efficient building components promotes adoption. Furthermore, expanding urban population and rising construction activities in secondary cities offer new market segments. These trends encourage manufacturers to invest in innovation and market expansion strategies to capitalize on evolving customer demands.

- •Strategic acquisitions and mergers allow companies to broaden product portfolios, enhance technological capabilities, and expand geographic footprints across EMEA. Investment in digital marketing and e-commerce platforms increases brand visibility and customer engagement. Collaborations with architectural firms and contractors enable early integration of automatic doors in building designs, fostering long-term partnerships. Emphasis on training and certification programs improves installation and maintenance quality, enhancing customer satisfaction. These initiatives contribute to stronger market positioning and accelerated growth within the EMEA Automatic Doors market.

Market Challenges

- •Compliance with diverse and stringent regulatory requirements across multiple countries in EMEA poses a significant challenge, necessitating customization and testing that increase cost and complexity. Navigating heterogeneous safety, accessibility, and environmental standards demands thorough expertise and resource allocation. Varying electrical and building codes complicate product standardization and delay market entry. Moreover, the high upfront capital investment required for advanced automatic door systems limits adoption in price-sensitive segments and emerging economies. These factors create barriers for manufacturers, particularly new entrants aiming for regional scalability.

- •Supply chain disruptions and volatility in raw material prices, exacerbated by geopolitical tensions and the COVID-19 pandemic aftermath, impact manufacturing timelines and profitability. Dependence on specialized components and global suppliers exposes manufacturers to risks of delays and increased costs. Fluctuating currency exchange rates further add financial uncertainty, affecting pricing strategies and contract negotiations. These operational challenges necessitate robust contingency planning and diversified sourcing strategies to maintain market competitiveness.

- •Shortage of skilled labor and technical expertise in installation and maintenance of sophisticated automatic door systems affects service quality and customer satisfaction. Training requirements and retention of qualified personnel represent ongoing operational challenges, especially in emerging markets. Inadequate after-sales support can lead to reduced product lifespan and customer trust. Addressing these workforce issues requires investment in comprehensive training programs and partnerships with technical institutions.

- •Intense competition from both established global players and agile regional manufacturers drives pricing pressure, potentially eroding margins. Differentiating products solely on technology becomes challenging as innovations diffuse rapidly. Additionally, counterfeit and low-quality imports may undermine brand reputation and market trust. Companies must continuously invest in innovation, branding, and quality assurance to sustain competitive advantage and customer loyalty.

- •Cybersecurity concerns related to IoT-enabled automatic doors pose new risks of unauthorized access and data breaches. Ensuring robust security protocols and compliance with data protection regulations is critical to maintaining user trust. The evolving threat landscape requires continuous monitoring, software updates, and collaboration with cybersecurity experts, adding complexity to product development and maintenance cycles.

- •The fragmented nature of the EMEA market with diverse cultural, economic, and regulatory environments complicates marketing and sales strategies. Tailoring products and services to meet local preferences and standards demands significant localization efforts. Managing multiple distribution channels and after-sales networks increases operational overheads. These challenges require companies to adopt flexible and region-specific approaches to effectively capture market share.

- •Economic uncertainties, including fluctuating construction activities and investment cycles in certain EMEA countries, affect demand predictability. Political instability in parts of the Middle East and Africa introduces additional risks impacting long-term planning and resource allocation. Companies must adopt agile business models and risk management frameworks to navigate these volatile conditions and sustain growth momentum.

Regulatory Framework

- •Between 2020 and 2024, the European Union strengthened regulations on energy efficiency and accessibility for building components, including automatic doors, through directives such as the Energy Performance of Buildings Directive (EPBD) and the Construction Products Regulation (CPR). These regulations mandate compliance with minimum insulation standards, fire safety, and accessibility requirements, influencing product design and certification processes.

- •The General Data Protection Regulation (GDPR) enforcement has impacted IoT-enabled automatic doors by requiring stringent data privacy and user consent management, compelling manufacturers to integrate robust cybersecurity measures and transparent data handling protocols.

- •National regulations in key EMEA countries like Germany, France, and the United Kingdom have introduced specific safety standards for automatic door operation, including sensor sensitivity, emergency override systems, and maintenance schedules, enhancing overall user safety and compliance.

- •In the Middle East, countries such as the United Arab Emirates and Saudi Arabia have implemented building codes emphasizing sustainable construction and smart infrastructure integration, boosting demand for energy-efficient and intelligent automatic door systems compliant with these mandates.

- •Government incentive programs promoting green building certifications and smart city projects across EMEA encourage adoption of advanced automatic doors, providing financial support and tax benefits to compliant manufacturers and end-users, thereby accelerating market growth.

Market Intelligence

- •15th March 2024, ASSA ABLOY announced the launch of its latest sliding automatic door system featuring AI-powered sensors and energy-efficient drive units, targeting commercial and healthcare sectors across EMEA. The new product promises enhanced safety, reduced energy consumption, and improved user experience through adaptive speed control and remote diagnostics capabilities. This innovation aligns with increasing demand for smart, sustainable building solutions and compliance with evolving regional regulations. ASSA ABLOY aims to strengthen its market leadership by addressing the diverse operational requirements of EMEA customers with this advanced system. Source: ASSA ABLOY Official Press Release

- •10th November 2023, Dorma+Kaba Group introduced an IoT-enabled revolving door platform designed for high-traffic transportation hubs and commercial complexes in Europe and the Middle East. The platform integrates cloud-based monitoring, predictive maintenance alerts, and customizable access controls to optimize operational efficiency and security. This strategic product launch reflects the company’s commitment to innovation and digital transformation in the automatic doors market. The solution supports smart city infrastructure initiatives and enhances user convenience with minimal energy consumption. Dorma+Kaba targets expansion in key EMEA markets through this offering, reinforcing its competitive position. Source: Dorma+Kaba Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 7.6 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Type (Sliding Doors, Swing Doors, Revolving Doors, Folding Doors, Hermetic Doors), Application (Commercial Buildings, Healthcare Facilities, Transportation Hubs, Residential Complexes, Industrial Facilities), End User Segment (Public Sector, Private Enterprises, Retail Chains, Hospitality Industry, Manufacturing Units), Technology (Sensor-Based Automation, IoT-Enabled Doors, Manual-Assist Automatic Doors, Energy Efficient Doors) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | ASSA ABLOY (Sweden), Dorma+Kaba Group (Switzerland), Tormax (Switzerland), Record Automatic Doors (Italy), GEZE GmbH (Germany), Boon Edam (Netherlands), Crawford (Sweden), Porta Systems (Turkey), Hormann Group (Germany), TSA UK Ltd (United Kingdom), Albany Doors (United Kingdom), Besam Entrance Solutions (Sweden), Record Doors (Italy), Porteo (France), Rite-Hite Europe (Belgium), Kaba Group (Switzerland), Norton Door Controls (United Kingdom), EFAFLEX Tor- und Sicherheitssysteme GmbH (Germany), Interflex Group (Germany), Centurion Systems (United Kingdom), Stanley Access Technologies (United Kingdom), Hörmann UK (United Kingdom), Besam Entrance Solutions (UK/Sweden), G-U Door Controls (Germany), Record Italia (Italy) |

EMEA Automatic Doors Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.