United States Ceramic Welding Ferrules Market Size, Growth & Revenue 2025-2034

United States Ceramic Welding Ferrules Market is segmented by Type (Standard Ferrules, Customized Ferrules, High-Temperature Ferrules, Precision Ferrules, Specialty Ferrules), Application (Automotive Manufacturing, Aerospace, Industrial Equipment, Energy Sector, Medical Devices), End-User Industry (Manufacturing Plants, Construction Firms, Repair and Maintenance Services, Research & Development Facilities), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

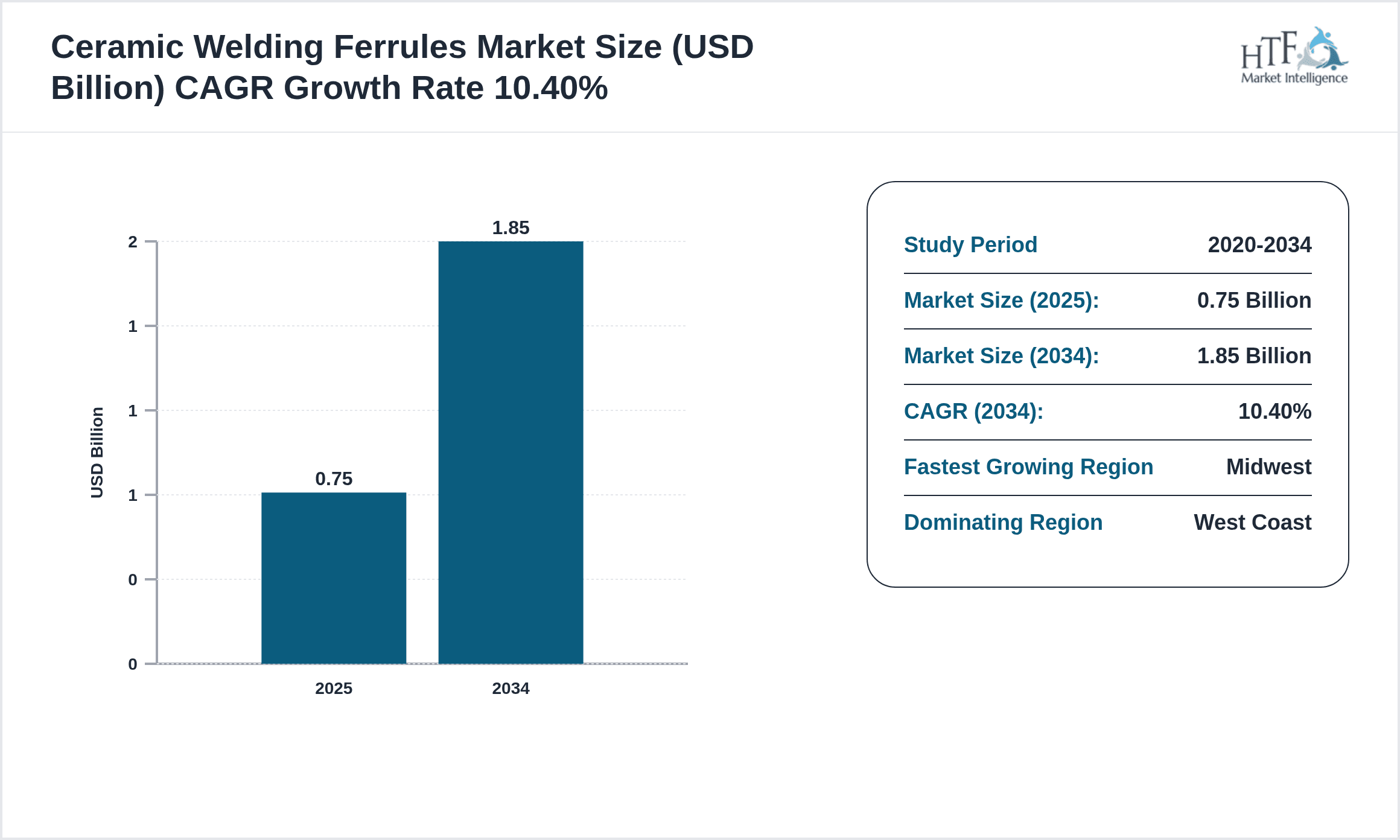

- •The United States Ceramic Welding Ferrules Market is a specialized sector focused on ceramic components that support welding quality and process efficiency. These ferrules are integral in containing molten metal during welding, preventing contamination, and stabilizing arcs across key industries like automotive, aerospace, energy, and medical devices. The market includes diverse product types such as standard, customized, high-temperature, precision, and specialty ferrules, each serving specific operational needs. This market is driven by increasing demand for high-integrity welds in advanced manufacturing and stringent quality standards. Technological innovations and regional manufacturing growth are propelling market expansion, with the West Coast currently dominating demand. The forecast period through 2034 anticipates a CAGR of over 10%, reflecting robust growth opportunities fueled by regulatory support and industrial modernization.

- •Key market highlights include a current valuation of USD 0.75 billion in 2025 with projections reaching USD 1.85 billion by 2034. The Midwest region is identified as the fastest growing submarket due to rising industrial activity and adoption of high-temperature ferrules. Leading product segments focus on standard ferrules, while high-temperature variants exhibit the highest growth rates. Market players are innovating to enhance material properties and customization capabilities, aligning with evolving welding technologies. Regulatory frameworks emphasizing welding quality and safety standards further reinforce market dynamics.

- •This market presents strategic importance to manufacturers, welding service providers, and end-users by enabling improved weld quality, operational efficiency, and cost savings. The integration of ceramic welding ferrules enhances process reliability in high-stakes industries, reducing downtime and defect rates. Stakeholders benefit from advancements in ceramic materials and fabrication methods, positioning the market as a critical component in the United States’ industrial technology landscape. The sector’s growth trajectory signals expanding opportunities for innovation, investment, and competitive differentiation.

Competitive Landscape

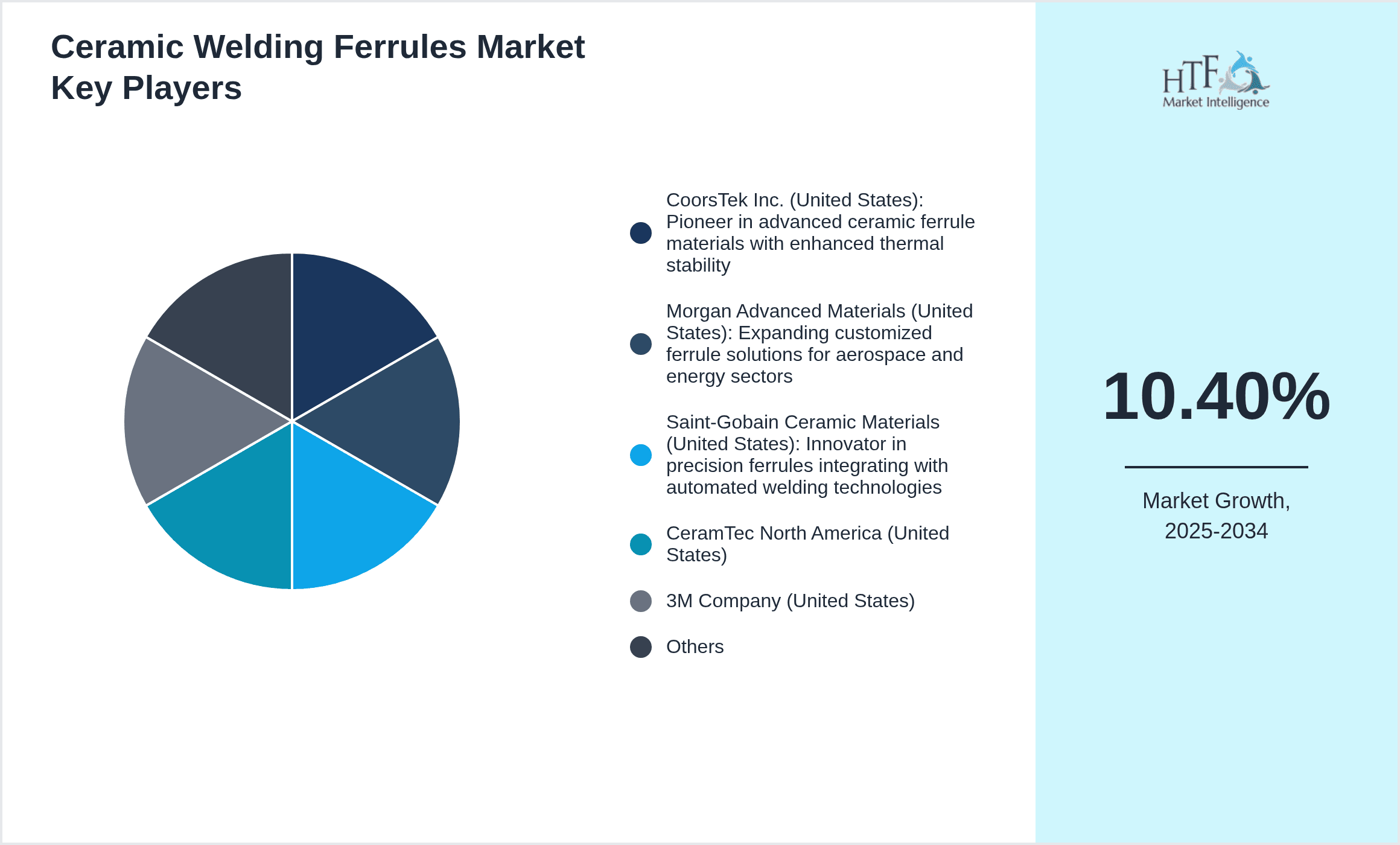

Competition within the United States Ceramic Welding Ferrules Market is marked by a blend of established manufacturers and emerging innovators, each striving to enhance product performance and customization. Companies compete on technological advancements, material quality, pricing strategies, and customer service excellence. Innovation centers on improving thermal resistance, dimensional precision, and compatibility with automated welding systems. Strategic partnerships and collaborations are common to expand product portfolios and geographic reach within the country. Market rivalry encourages continuous R&D investments, driving differentiation through unique ceramic formulations and tailored ferrule designs. Distribution efficiency and supply chain robustness also play crucial roles in sustaining competitive advantage. Overall, the market environment fosters a dynamic interplay of innovation and operational excellence aimed at meeting evolving industrial requirements.

Leading Companies in United States Ceramic Welding Ferrules Market

- •CoorsTek Inc. (United States): Pioneer in advanced ceramic ferrule materials with enhanced thermal stability

- •Morgan Advanced Materials (United States): Expanding customized ferrule solutions for aerospace and energy sectors

- •Saint-Gobain Ceramic Materials (United States): Innovator in precision ferrules integrating with automated welding technologies

- •CeramTec North America (United States)

- •3M Company (United States)

- •Praxair Surface Technologies (United States)

- •Harvey Performance Company (United States)

- •ITW Welding Products (United States)

- •Lincoln Electric Holdings (United States)

- •ESAB Corporation (United States)

- •K-TIG (United States)

- •Air Liquide Welding (United States)

- •Fronius USA LLC (United States)

- •Thermal Ceramics Inc. (United States)

- •Advanced Ceramic Components Inc. (United States)

- •CeramTec Inc. (United States)

- •CeramicX (United States)

- •Saint-Gobain (United States)

- •H.C. Starck Ceramics (United States)

- •Morgan Technical Ceramics (United States)

- •CoorsTek Ceramics (United States)

- •Tessenderlo Group (United States)

- •Plasmatech (United States)

- •CeramTec GmbH (United States)

- •Ceramic Capacitor Inc. (United States)

Market Breakdown

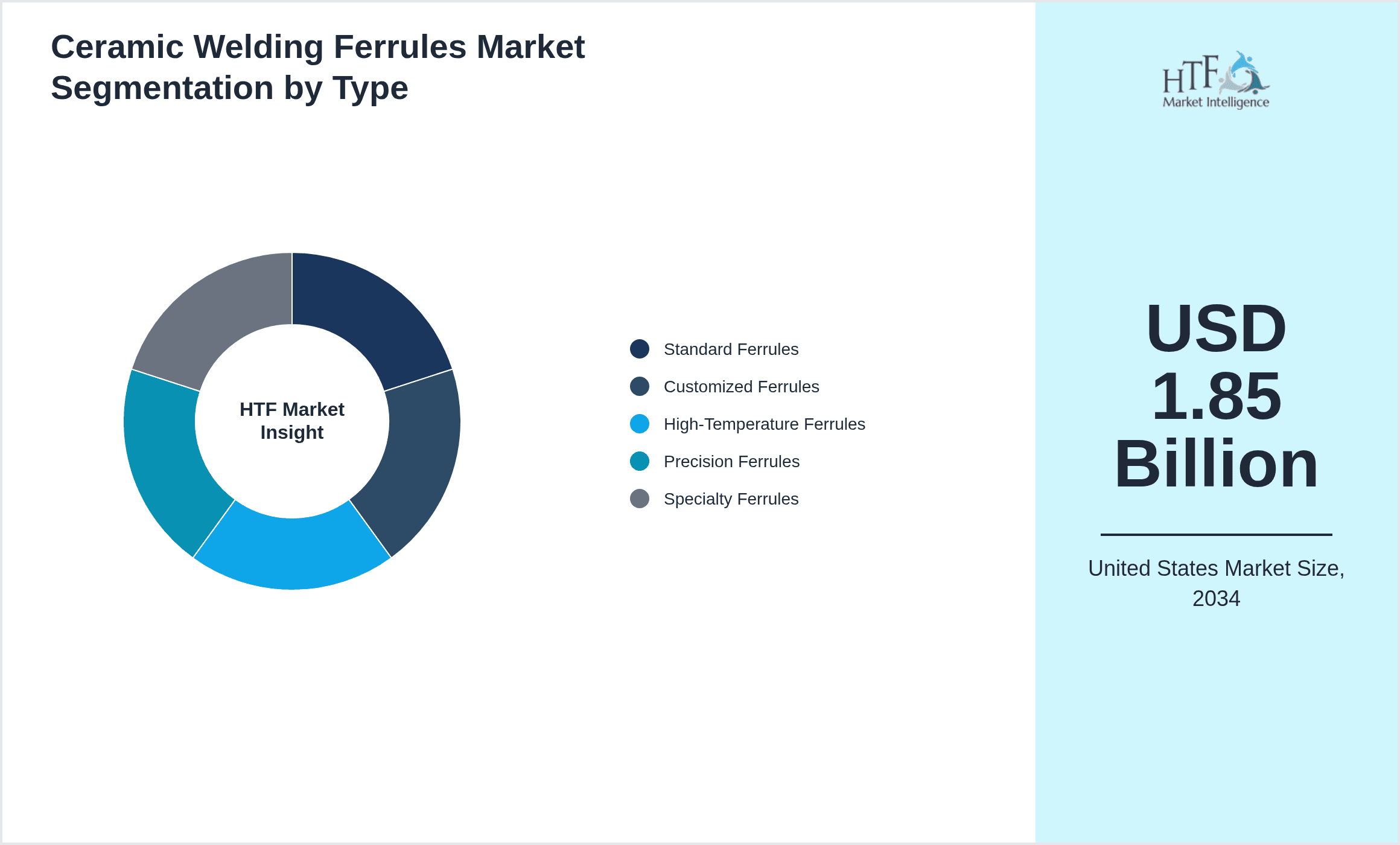

- •By Type

- ◦Standard Ferrules

- ◦Customized Ferrules

- ◦High-Temperature Ferrules

- ◦Precision Ferrules

- ◦Specialty Ferrules

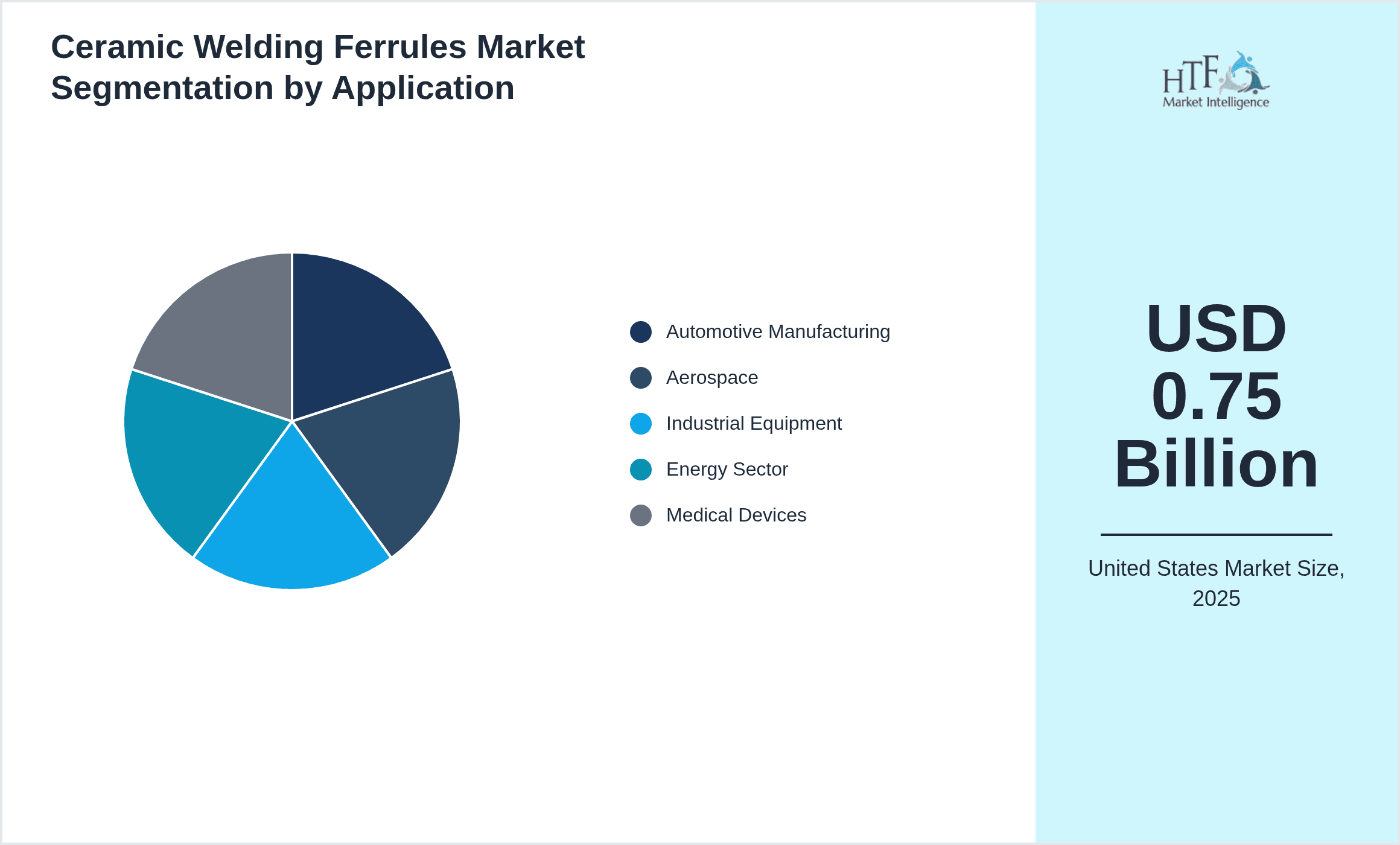

- •By Application

- ◦Automotive Manufacturing

- ◦Aerospace

- ◦Industrial Equipment

- ◦Energy Sector

- ◦Medical Devices

- •By End-User Industry

- ◦Manufacturing Plants

- ◦Construction Firms

- ◦Repair and Maintenance Services

- ◦Research & Development Facilities

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Government initiatives promoting advanced manufacturing and welding quality standards are accelerating adoption of ceramic welding ferrules, enhancing market growth prospects.

- •Strategic partnerships between ceramic material producers and welding equipment manufacturers are fostering integrated solutions that boost operational efficiency and customer value.

- •Technological innovations in ceramic composites and precision engineering are enabling ferrules to withstand higher temperatures and improve weld integrity across critical applications.

- •Growing demand for lightweight and durable welding accessories in aerospace and automotive sectors is driving expansion of customized and specialty ferrule segments.

- •Increasing automation in welding processes requires compatible ferrule designs, stimulating R&D and market penetration of advanced ceramic ferrules.

- •Cost efficiency achieved through reduced weld defects and faster production cycles is motivating end-users to transition towards ceramic welding ferrule solutions.

- •Environmental regulations encouraging sustainable manufacturing practices are influencing material selection and promoting ceramic ferrules due to their recyclability and durability.

Market Trends

- •The rise of Industry 4.0 is prompting adoption of smart ceramic welding ferrules compatible with automated and robotic welding systems, enhancing precision and repeatability.

- •Innovations integrating nano-ceramic coatings are emerging to improve ferrule wear resistance and longevity under extreme welding conditions.

- •Collaborations between material science firms and welding technology providers are accelerating product development cycles and market responsiveness.

- •Sustainability trends are driving interest in eco-friendly ceramic materials that reduce environmental impact during manufacturing and disposal.

- •Increasing customization demand is leading to modular ferrule designs tailored to specific welding processes and alloy types.

- •Expansion of aftermarket services offering ferrule refurbishment and recycling is gaining traction among industrial users.

- •The integration of digital tracking and quality assurance tools is becoming standard to monitor ferrule performance and lifecycle management.

Market Opportunities

- •Expanding applications in emerging sectors such as renewable energy and electric vehicle manufacturing represent significant growth opportunities for ceramic welding ferrules.

- •Untapped regional markets within the Midwest and Southeast offer potential for increased market penetration through localized manufacturing and distribution hubs.

- •Investment in R&D to develop ferrules compatible with next-generation welding technologies, such as laser and hybrid welding, can drive competitive advantage.

- •Collaborations with OEMs to co-develop customized ferrules for high-specification applications can open new revenue streams and deepen client relationships.

- •Growth in aftermarket services including ferrule repair, recycling, and lifecycle management provides avenues for service diversification and customer retention.

- •Leveraging digital platforms for direct sales and customer engagement can enhance market reach and operational efficiencies.

- •Adoption of sustainable ceramic materials aligned with evolving environmental regulations can position market players as industry leaders in eco-conscious manufacturing.

Market Challenges

- •High initial costs associated with advanced ceramic ferrule materials can deter price-sensitive customers, limiting broader adoption.

- •Infrastructure constraints in less industrialized regions slow distribution and timely delivery of specialized ceramic ferrules.

- •Lack of widespread awareness and technical expertise among end-users poses barriers to market penetration and technology adoption.

- •Competition from traditional ferrule materials and alternative welding accessories creates pricing and market share pressures.

- •Regulatory compliance complexity, especially concerning material certifications and environmental standards, increases operational costs.

- •Supply chain disruptions affecting raw ceramic materials can impact production schedules and market responsiveness.

- •Challenges in customizing ferrules for diverse welding processes require significant R&D investment and flexible manufacturing capabilities.

Regulatory Framework

- •The American Welding Society (AWS) established welding quality standards between 2020-2025, mandating precise material specifications for welding accessories including ceramic ferrules, driving compliance requirements.

- •Occupational Safety and Health Administration (OSHA) regulations implemented in 2021 require manufacturers to ensure ferrule materials do not emit hazardous particulates during welding operations, enhancing workplace safety.

- •Environmental Protection Agency (EPA) policies from 2022 emphasize sustainable manufacturing of ceramic components, promoting recyclable materials and reducing waste in production processes.

- •State-level mandates in California and New York between 2023-2025 introduced stricter emissions and material handling protocols for welding consumables, influencing regional market practices.

- •Federal incentives launched in 2024 support R&D investments in advanced ceramic materials to improve welding efficiency and environmental compliance, fostering innovation and market growth.

Market Intelligence

- •15th January 2025, CoorsTek Inc. unveiled a new line of high-temperature ceramic welding ferrules designed for aerospace applications, featuring enhanced thermal shock resistance and precision tolerances to improve weld quality and reduce defects. This launch aims to capture growing demand in the aerospace manufacturing sector and strengthen CoorsTek’s leadership position in advanced ceramic components. The company emphasized the ferrules' compatibility with automated welding systems and their contribution to operational efficiency. Source: CoorsTek Official Press Release

- •30th March 2025, Morgan Advanced Materials announced strategic expansion of its US manufacturing facility to increase production capacity of customized ceramic ferrules for energy and industrial equipment markets. This move supports rising demand and allows faster delivery timelines to key clients, enhancing market responsiveness. The expansion includes investment in new fabrication technologies enabling tighter dimensional control and material performance improvements. Morgan highlighted the role of this initiative in sustaining competitive advantage amid growing market competition. Source: Morgan Advanced Materials Corporate Announcement

- •10th May 2024, Saint-Gobain Ceramic Materials introduced precision ferrule products integrated with digital traceability features for welding quality assurance. This innovation enhances process monitoring and lifecycle management, providing end-users with real-time data to optimize weld consistency and reduce rework. The launch aligns with Industry 4.0 trends and increasing automation in the US welding industry. Saint-Gobain expects this technology to open new market segments and strengthen customer relationships. Source: Saint-Gobain Product Launch Brief

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Dominant Segments

- •Standard Ferrules lead the product segment with wide adoption due to their versatility across multiple welding applications and cost-effectiveness.

- •Automotive Manufacturing dominates application-wise, driven by high-quality welding requirements and volume production needs.

- •Direct Sales represent the prevailing business model, allowing close customer engagement and tailored solutions delivery.

Future Outlook: A Connected and Sustainable Ecosystem

- •The US market is expected to expand further into renewable energy and electric vehicle manufacturing, leveraging ceramic ferrules for enhanced weld performance in critical components.

- •The West Coast remains the dominant region, benefiting from its concentration of aerospace, automotive, and technology industries driving sustained demand.

- •Long-term transformation will be shaped by integration of smart manufacturing, sustainability mandates, and advanced material innovations, creating a resilient and efficient ecosystem.

Market Explosion: A Rapidly Growing Sector

- •The United States Ceramic Welding Ferrules Market is valued at USD 0.75 billion in 2025 with expectations to reach USD 1.85 billion by 2034, reflecting strong growth momentum.

- •The sector is projected to grow at a CAGR of 10.4%, supported by rising industrial demand and technological advancements in ceramic materials.

- •Additional growth is driven by increasing adoption of high-performance ferrules in aerospace and automotive industries, contributing to enhanced welding quality and operational efficiency.

Key Drivers of Growth

- •Federal and state government programs promoting manufacturing innovation and welding quality standards are propelling market adoption of ceramic ferrules.

- •Collaborative ventures between ceramic material producers and welding equipment manufacturers are creating integrated solutions that improve production workflows.

- •Innovations in ceramic composites and ferrule design are enhancing durability and adaptability, meeting stringent industrial requirements.

The Road Ahead: Embrace the Ceramic Welding Ferrules Revolution

- •The United States ceramic welding ferrules market is set to transform industrial welding landscapes by delivering superior weld quality, operational efficiency, and sustainability benefits.

- •Embracing advanced ceramic technologies will enable stakeholders to meet evolving manufacturing demands and secure long-term competitive advantages in a dynamic market.

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Midwest is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.75 Billion |

| Forecast Year Market Size | USD 1.85 Billion |

| CAGR | 10.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10% |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | CoorsTek Inc. (United States), Morgan Advanced Materials (United States), Saint-Gobain Ceramic Materials (United States), CeramTec North America (United States), 3M Company (United States), Praxair Surface Technologies (United States), Harvey Performance Company (United States), ITW Welding Products (United States), Lincoln Electric Holdings (United States), ESAB Corporation (United States), K-TIG (United States), Air Liquide Welding (United States), Fronius USA LLC (United States), Thermal Ceramics Inc. (United States), Advanced Ceramic Components Inc. (United States), CeramTec Inc. (United States), CeramicX (United States), Saint-Gobain (United States), H.C. Starck Ceramics (United States), Morgan Technical Ceramics (United States), CoorsTek Ceramics (United States), Tessenderlo Group (United States), Plasmatech (United States), CeramTec GmbH (United States), Ceramic Capacitor Inc. (United States) |

United States Ceramic Welding Ferrules Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.