Europe LED Secondary Optic Market - Europe Industry Size & Growth Analysis 2024-2034

Europe LED Secondary Optic Market is segmented by Application (Street Lighting, Automotive Lighting, Commercial Lighting, Residential Lighting, Architectural Lighting), Type (TIR Lenses, Reflectors, Diffusers, Collimators, Light Guides), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe LED Secondary Optic Market is a specialized sector focused on the development and supply of optical components that enhance the performance of LED lighting systems by shaping, directing, and diffusing emitted light. This market spans a broad range of products including TIR lenses, reflectors, diffusers, collimators, and light guides that are essential in applications such as street lighting, automotive lighting, commercial and residential illumination, and architectural lighting designs. By improving light efficiency and distribution, these secondary optics contribute significantly to energy savings and lighting quality, aligning with Europe’s stringent energy regulations. The industry involves multiple stakeholders including material suppliers, component manufacturers, and lighting system integrators, operating within an innovation-driven environment that emphasizes precision engineering and advanced materials. As LED adoption continues to grow across Europe, the demand for sophisticated secondary optics rises, driven by urbanization, smart city initiatives, and automotive electrification. The market is bounded by technological advancements, regulatory frameworks, and evolving end-user needs that shape product development and deployment strategies.

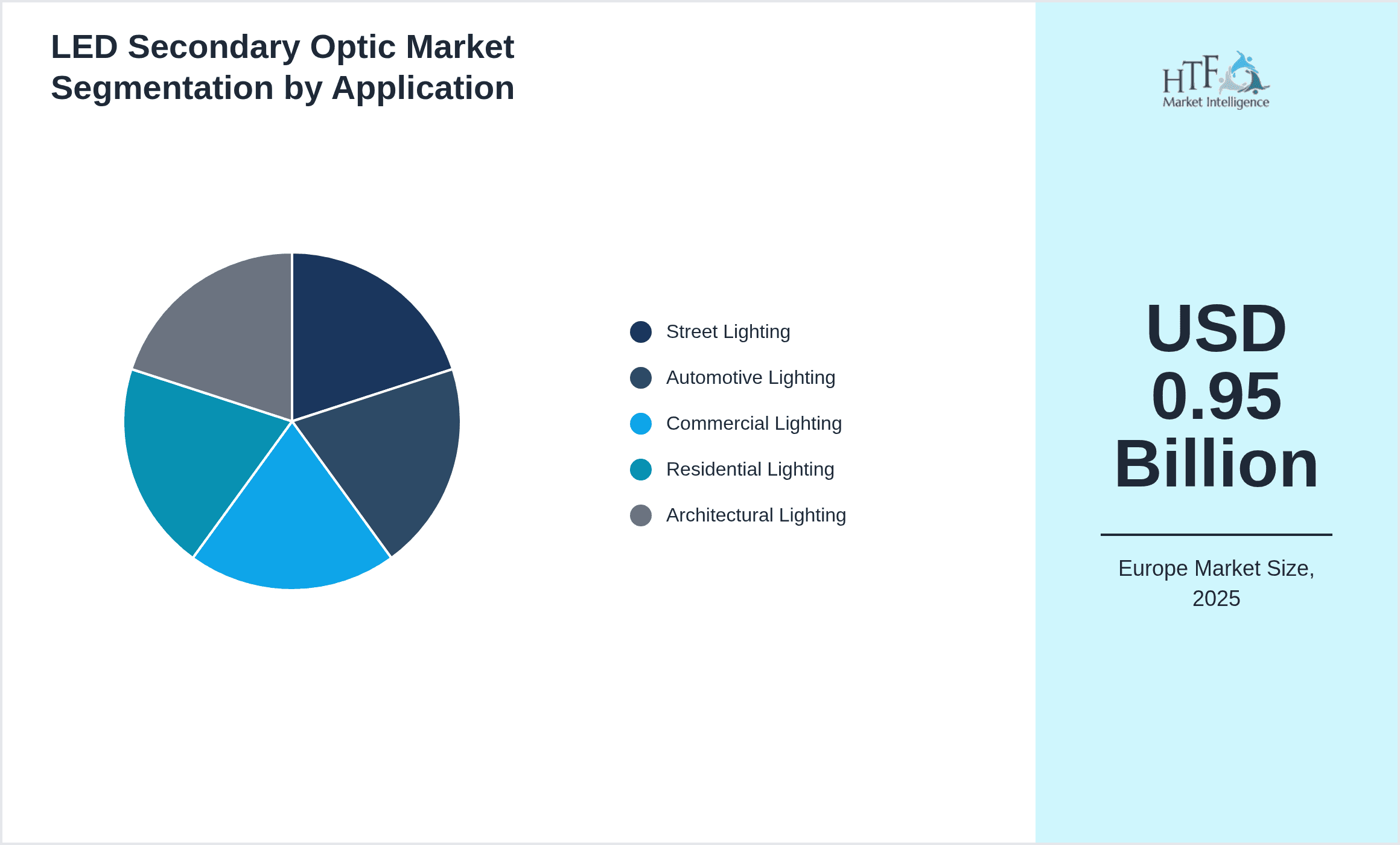

- •Key market highlights reveal steady growth with a current market size of USD 0.95 Billion in 2024, projected to reach USD 2.45 Billion by 2034, exhibiting a CAGR of 10.1%. Germany dominates the regional market accounting for 27% share, followed by France with the fastest growth rate at 12.5% CAGR. TIR lenses hold the leading product type position due to their efficiency and versatility, while reflectors are gaining traction as the fastest growing type. Street lighting and automotive lighting remain the most significant applications, collectively constituting over 50% of market demand. The market dynamics are influenced by increasing government investments in smart lighting infrastructure and stringent environmental policies encouraging energy-efficient lighting solutions.

- •The Europe LED Secondary Optic Market offers substantial value propositions to stakeholders by enabling enhanced lighting performance, energy efficiency, and compliance with environmental standards. Manufacturers benefit from expanding applications in automotive and public infrastructure lighting, while end-users gain from improved illumination quality and reduced operational costs. Strategic importance is underscored by ongoing technological innovations such as precision optical molding and integration with smart lighting controls, which propel market evolution. Additionally, the market’s role in supporting Europe’s sustainability goals and urban development initiatives underscores its criticality across multiple industries, including automotive, construction, and municipal services, fostering long-term growth potential.

Competitive Landscape

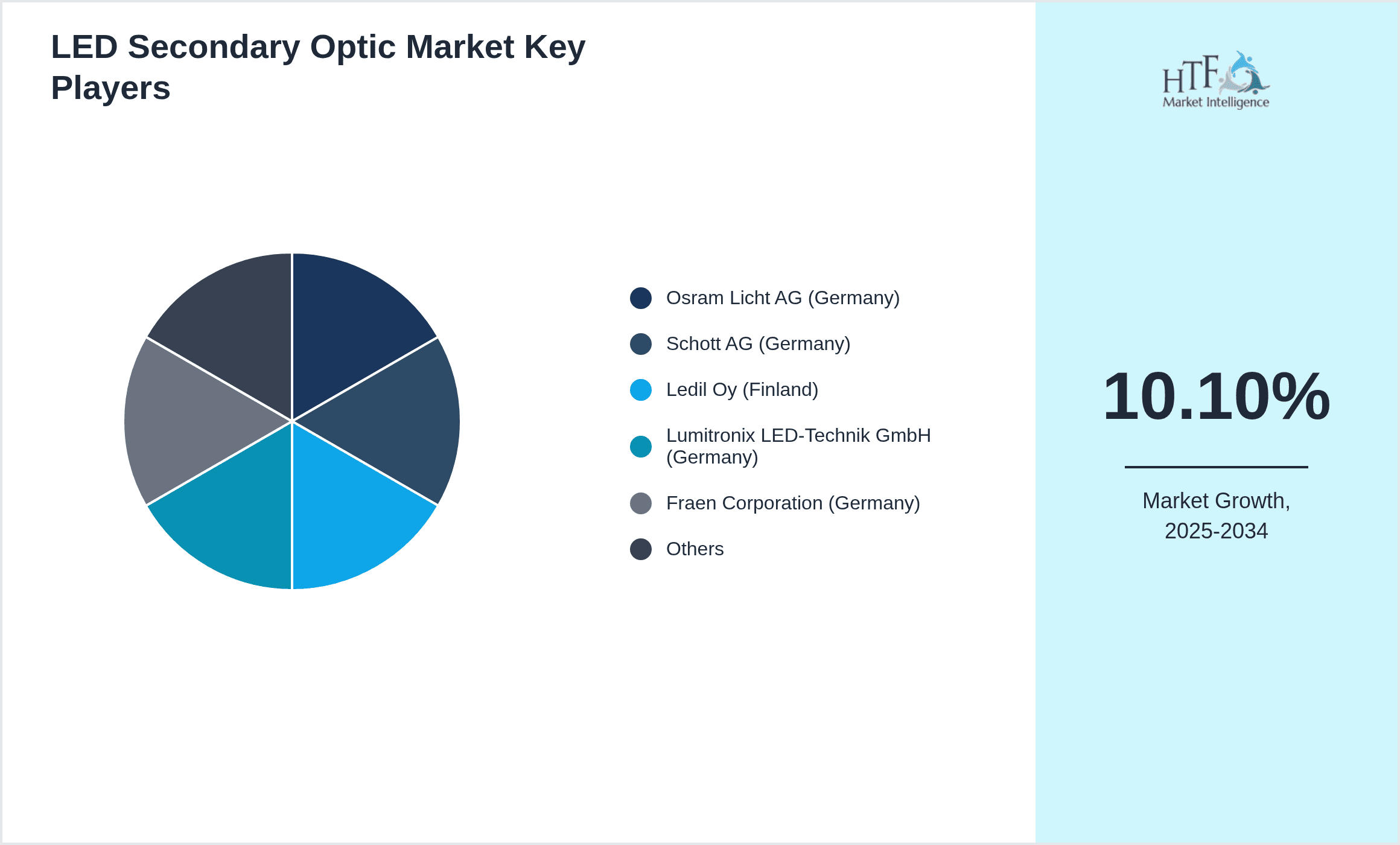

The Europe LED Secondary Optic Market is characterized by intense competition among established multinational corporations and agile regional players focusing on innovation, quality, and customization. Market participants employ strategies such as technological differentiation, strategic partnerships, and capacity expansion to strengthen their market positions. Innovation is central, with companies investing in advanced optical materials and precision manufacturing techniques to develop highly efficient and application-specific secondary optics. Rivalry is also evident in pricing strategies and after-sales support, where companies aim to provide integrated solutions including design and consultancy services. The competitive landscape is further shaped by regional specialization, with Germany and France emerging as hubs for R&D and manufacturing excellence. Mergers and acquisitions are common as firms seek to consolidate capabilities and expand geographic reach. The market is expected to witness increased collaboration between optics manufacturers and LED suppliers to drive integrated product offerings, enhancing competitive advantage and responding effectively to evolving customer requirements across Europe.

Leading Companies in LED Secondary Optic Market

- •Osram Licht AG (Germany)

- •Schott AG (Germany)

- •Ledil Oy (Finland)

- •Lumitronix LED-Technik GmbH (Germany)

- •Fraen Corporation (Germany)

- •Carclo plc (United Kingdom)

- •Rheinberg Lichttechnik GmbH (Germany)

- •ProPhotonix Limited (United Kingdom)

- •Light Shape GmbH (Germany)

- •Ledengin Ltd. (United Kingdom)

- •Opto Engineering Srl (Italy)

- •XAL GmbH (Austria)

- •Tridonic GmbH & Co KG (Austria)

- •LUXEON Technology (Netherlands)

- •Carclo Technical Plastics (United Kingdom)

- •Vossloh-Schwabe Deutschland GmbH (Germany)

- •LED Roadway Lighting (France)

- •Elix Lighting (France)

- •Ledvance GmbH (Germany)

- •Meyer Burger Technology AG (Switzerland)

- •Lumileds Holding B.V. (Netherlands)

- •Lumitronix LED-Technik GmbH (Germany)

- •Gaggione S.r.l. (Italy)

- •Voss Lighting GmbH (Germany)

- •Zumtobel Group AG (Austria)

Market Breakdown

- •By Type

- ◦TIR Lenses (Total Internal Reflection lenses)

- ◦Reflectors (Secondary Reflective Optics)

- ◦Diffusers (Light Diffusing Components)

- ◦Collimators (Beam Collimation Optics)

- ◦Light Guides (Optical Light Transmission Components)

- •By Application

- ◦Street Lighting

- ◦Automotive Lighting

- ◦Commercial Lighting

- ◦Residential Lighting

- ◦Architectural Lighting

- •By End User Sector

- ◦Municipal and Public Infrastructure

- ◦Automotive Manufacturers

- ◦Commercial Real Estate

- ◦Residential Construction

- ◦Architectural Design Firms

- •By Technology

- ◦Injection Molding Optics

- ◦Precision Glass Optics

- ◦Hybrid Optics

- ◦3D Printed Optical Components

Growth Dynamics

- •The Europe LED Secondary Optic Market is primarily driven by increasing adoption of LED lighting in automotive and public infrastructure sectors, where efficient light management is critical for safety and energy savings. Government regulations emphasizing energy efficiency and sustainability are accelerating replacement of traditional lighting with LED solutions, boosting demand for secondary optics. Technological advancements in optical materials and precision molding techniques enhance product performance and reduce costs, fostering wider application across commercial and residential projects. Additionally, urbanization and smart city initiatives in Europe promote intelligent lighting systems integrating advanced optics for optimized illumination control. Rising consumer preference for high-quality lighting with improved beam control further propels market expansion. Collaborative efforts between LED manufacturers and optics suppliers also drive innovation and product customization, meeting diverse application needs and underpinning robust market growth.

- •Market trends reveal a shift towards highly integrated optical systems combining lenses, reflectors, and diffusers to achieve tailored light distribution for specific applications such as automotive headlamps and street lighting. Increasing focus on miniaturization and weight reduction of optical components aligns with automotive electrification and LED fixture design requirements. The use of advanced materials like optical-grade silicone and glass enhances durability and light transmission efficiency. Digitalization and smart lighting controls incorporating secondary optics enable adaptive lighting solutions that adjust to environmental conditions and user preferences. Sustainability trends encourage development of recyclable and environmentally friendly optical components. Furthermore, regional manufacturing hubs in Germany, France, and the UK are increasingly investing in R&D to develop next-generation optics with improved thermal management and optical precision, reflecting a dynamic and innovation-led market landscape.

- •Despite robust growth, the market faces restraints including high initial costs associated with advanced optical components and manufacturing processes, which may limit adoption among price-sensitive end-users. Supply chain disruptions and raw material price volatility impact production cost stability, challenging manufacturers to maintain competitive pricing. Technical complexities in designing optics compatible with diverse LED types and applications require significant R&D investments, potentially hindering smaller players. Regulatory compliance across multiple European countries adds to operational challenges, especially concerning environmental and safety standards. Moreover, competition from alternative lighting technologies and evolving consumer preferences for simplified lighting solutions could restrain market growth. Addressing these restraints demands innovation in cost-effective manufacturing and strategic partnerships to optimize supply chains and expand market reach.

- •Market opportunities abound in expanding applications such as automotive LED headlamps, where advanced secondary optics enhance safety and aesthetic appeal, creating demand for innovative lens and reflector solutions. Growth in smart city projects across Europe provides avenues for integrated lighting systems requiring adaptable optics for energy-efficient street and architectural lighting. Emerging technology trends like 3D printing and hybrid optical materials enable customized and lightweight components, opening new product development potentials. Expansion into growing commercial and residential construction sectors seeking sustainable lighting solutions also offers substantial opportunities. Collaborations between optics manufacturers and LED producers facilitate co-development of tailored solutions, accelerating market penetration. Additionally, rising demand for retrofit kits leveraging secondary optics to upgrade existing lighting systems presents further growth avenues.

- •Key challenges in the Europe LED Secondary Optic Market include managing the complexity of multi-country regulatory compliance impacting product design and certification processes. Intense price competition from low-cost manufacturers outside Europe pressures profit margins for regional players. Rapid technological changes require continual investment in R&D to sustain innovation leadership, which may strain resources particularly for SMEs. Supply chain vulnerabilities exposed by geopolitical tensions and material shortages pose risks to timely product delivery. Additionally, educating end-users on the benefits of advanced optics remains critical to overcoming resistance to adoption, especially in traditional sectors. Addressing these challenges necessitates strategic investment in technology, quality assurance, and customer engagement to maintain competitive advantage and market growth.

Market Trends

- •The Europe LED Secondary Optic Market is witnessing a growing trend towards integration of secondary optics with smart lighting systems, enabling adaptive beam shaping and energy optimization in real-time. This integration is particularly prominent in automotive and street lighting applications, enhancing safety and reducing energy consumption. Manufacturers are increasingly adopting advanced manufacturing methods such as injection molding with optical-grade polymers to produce lightweight and high-precision components. The trend towards miniaturization and compact designs aligns with evolving LED fixture requirements, facilitating wider adoption in diverse applications. Sustainability-driven innovations focus on recyclable materials and lower environmental impact production processes. Regional hubs in Germany and France are pioneering research in novel optical materials and hybrid optics, reinforcing Europe’s leadership in this market segment.

- •Another significant trend is the rise of customizable optics tailored to specific client needs, supported by advancements in 3D printing technology. This allows rapid prototyping and flexible production, reducing time-to-market for new lighting solutions. The market is also seeing increased collaboration between LED manufacturers and optics suppliers to co-develop integrated solutions optimized for performance and cost efficiency. Digital simulation tools are becoming integral in the design process, enabling precise modeling of light distribution and enhancing product development cycles. Additionally, there is a growing emphasis on thermal management within secondary optics to maintain LED performance and longevity, leading to innovative material and design approaches. These trends collectively position the market for sustained innovation and expansion.

- •Sustainability and regulatory compliance remain key market drivers influencing product development trends, with manufacturers focusing on eco-friendly materials and energy-efficient designs. The shift towards electric vehicles in Europe creates new growth avenues for automotive LED secondary optics, driving demand for advanced lenses and reflectors that meet stringent quality and safety standards. Smart city initiatives promoting intelligent and adaptive street lighting systems are accelerating adoption of sophisticated optics enabling dynamic light control. The market also observes a trend towards consolidation with mergers and acquisitions enhancing technological capabilities and geographic reach. Consumer demand for high-quality, visually comfortable lighting fosters innovation in diffusers and collimators designed for uniform light distribution. Overall, these trends highlight a market evolving rapidly through technological, regulatory, and consumer-driven factors.

- •The evolving competitive landscape encourages companies to invest in digitalization, leveraging AI and IoT integration with optical components to enable predictive maintenance and enhanced lighting performance. This digital transformation trend is particularly significant in commercial and municipal lighting applications. Additionally, there is increasing focus on reducing production lead times and costs through automation and supply chain optimization. The market also witnesses growing demand for retrofit solutions that utilize secondary optics to upgrade existing lighting infrastructure, promoting sustainability and cost savings. Regional specialization in optics manufacturing drives innovation clusters, particularly in Germany and the UK, fostering ecosystem development and knowledge sharing. These strategic trends collectively enhance market competitiveness and responsiveness to changing industry demands.

- •Finally, the Europe LED Secondary Optic Market is exploring new application areas including horticultural lighting and medical illumination, where precise light control is critical. This diversification offers manufacturers opportunities to leverage their optical expertise beyond traditional sectors. The adoption of flexible and tunable optics enabling dynamic light spectrum control aligns with emerging application requirements. Partnerships between optics firms and technology providers are facilitating development of integrated systems combining optics, sensors, and controls. Consumer preferences for aesthetically pleasing lighting that also delivers functional benefits drive demand for innovative architectural lighting optics. These future-facing trends underscore the market’s adaptability and growth potential across multiple verticals.

Market Opportunities

- •The Europe LED Secondary Optic Market presents significant growth potential through expanding automotive lighting applications, where regulatory emphasis on vehicle safety and energy efficiency demands advanced optical components. Opportunities exist in developing lightweight, high-performance reflectors and lenses tailored for electric and autonomous vehicles. Additionally, public infrastructure modernization under smart city initiatives offers vast scope for integrated street lighting solutions requiring adaptive optics. The rising demand for retrofit kits in commercial and residential sectors enables market penetration by upgrading existing lighting systems with energy-efficient optics. Advanced manufacturing techniques such as 3D printing open avenues for customized and rapid production, appealing to niche markets. Collaborations between optics manufacturers and LED producers provide synergistic benefits, enhancing product portfolios and market reach. Furthermore, emerging applications in horticultural and medical lighting create new segments for specialized optical components, diversifying growth avenues and fostering innovation-led expansion.

- •Geographically, opportunities lie in expanding presence in fast-growing European markets such as France, Spain, and Italy, where urban development and regulatory support are accelerating LED adoption. Investment in R&D to develop eco-friendly and recyclable optical materials aligns with Europe’s sustainability agenda, meeting consumer and regulatory demands. Digital integration of optics with lighting control systems offers potential for value-added solutions commanding premium pricing. Strategic acquisitions and partnerships can enhance technological capabilities and access to new customer segments. Additionally, increasing awareness among end-users regarding energy savings and lighting quality supports market growth. The convergence of lighting and IoT technologies presents opportunities for innovative product offerings, enabling manufacturers to differentiate in a competitive market. Overall, these opportunities underscore the market’s dynamic nature and prospects for long-term value creation.

- •Investment in lightweight and compact optical designs tailored for portable and wearable lighting devices offers emerging opportunities in niche consumer electronics segments. The development of multi-functional optics combining illumination and sensing capabilities is gaining traction, enabling new product innovations. Expansion into adjacent sectors such as signage and display lighting further broadens application scope. Market players can leverage data analytics and customer insights to customize offerings and enhance user experience. Government incentives supporting energy-efficient lighting renovations in public and private sectors present financial motivation for adoption. Moreover, increasing demand for aesthetic lighting solutions in architectural and hospitality sectors drives product innovation in decorative optics. These diverse opportunities highlight the market’s potential to capitalize on evolving technological and consumer trends.

- •The growing emphasis on circular economy principles in Europe encourages development of sustainable optical products designed for easy recycling and material recovery. This aligns with regulatory pressures and consumer preferences, presenting market differentiation opportunities. Integration of secondary optics with advanced sensor technologies for adaptive lighting control can enhance functionality and energy efficiency. Expansion of e-commerce and digital sales channels facilitates broader market access and customer engagement. Partnerships with construction and urban planning firms enable early integration of advanced lighting solutions in new projects. Additionally, emerging trends in LED lighting for agricultural applications offer untapped potential for specialized secondary optics. These strategic opportunities support market diversification and resilience in a competitive environment.

- •Finally, leveraging artificial intelligence and machine learning in optical design processes improves precision and accelerates innovation cycles. This technological leverage can reduce time-to-market and optimize performance, providing competitive advantages. Participation in international standardization initiatives enhances product acceptance and marketability. Expanding training and education programs to increase awareness of secondary optics benefits among end-users can stimulate demand. Investment in after-sales services and technical support strengthens customer relationships and retention. Collectively, these opportunities foster sustainable growth and leadership in the Europe LED Secondary Optic Market.

Market Challenges

- •A significant challenge in the Europe LED Secondary Optic Market is the high capital investment required for advanced manufacturing facilities and precision tooling, which may limit entry and expansion for smaller players. The complexity of designing optics compatible across diverse LED platforms necessitates continuous R&D, increasing operational costs. Supply chain disruptions, including shortages of raw materials like optical-grade polymers and specialty glass, pose risks to manufacturing continuity and pricing stability. Furthermore, the fragmented regulatory landscape across European countries complicates compliance and certification processes, requiring extensive resources and expertise. Price sensitivity among end-users in certain sectors limits adoption of premium optical solutions despite their benefits. Overcoming these challenges demands strategic collaborations, efficient cost management, and focused innovation to maintain competitiveness and market growth.

- •Technological challenges include maintaining optical precision and consistency at scale, especially for complex multi-component systems. Balancing performance with thermal management and durability in harsh environmental conditions is critical but demanding. The rapid pace of LED technology evolution requires optics manufacturers to continuously adapt designs, risking obsolescence and inventory write-offs. Intellectual property protection remains a concern as product innovation intensifies competition. Market education to overcome end-user hesitation towards adopting advanced secondary optics is essential but resource-intensive. Additionally, competition from alternative lighting technologies and integrated LED designs with built-in optics could restrain standalone secondary optics demand. Addressing these multifaceted challenges is vital for sustaining market momentum and achieving long-term profitability.

- •Economic fluctuations and geopolitical uncertainties in Europe impact investment decisions and project timelines in infrastructure and automotive sectors, influencing optics market demand. Environmental regulations, while driving innovation, also impose compliance costs and procedural delays. The COVID-19 pandemic aftermath continues to affect supply chains and workforce availability, complicating production schedules. Variability in energy pricing influences end-user investment in LED upgrades and optics adoption. The competitive landscape with aggressive pricing from non-European manufacturers challenges regional companies to differentiate through quality and service. Furthermore, limited availability of skilled workforce in optics engineering and manufacturing hinders capacity expansion. Effective risk management, policy engagement, and workforce development are essential to mitigate these challenges and capitalize on market potential.

- •The transition towards circular economy principles requires redesigning products for recyclability, which can increase design complexity and costs. Ensuring compatibility of secondary optics with emerging LED light sources and smart control systems demands ongoing technical collaboration. Managing inventory risks associated with multiple product variants tailored to diverse applications adds operational complexity. Market penetration in emerging European economies faces infrastructure and awareness barriers. Additionally, balancing customization demands with standardization for cost efficiency is challenging. Overcoming these obstacles through strategic planning, technological investment, and stakeholder engagement is critical to sustaining competitive advantage and market relevance.

- •Finally, cybersecurity concerns arise as secondary optics increasingly integrate with IoT-enabled smart lighting systems, necessitating robust security protocols. Managing environmental and health safety standards related to optical materials requires stringent quality controls. The need to rapidly adapt to evolving customer preferences and regulatory changes imposes agility demands on manufacturers. Coordination among supply chain partners to ensure timely delivery and quality consistency remains a logistical challenge. Continuous market monitoring and strategic foresight are necessary to anticipate and navigate these complex challenges in the dynamic Europe LED Secondary Optic Market.

Regulatory Framework

- •Between 2019 and 2024, Europe implemented the Ecodesign Directive updates targeting energy efficiency in lighting products, requiring manufacturers to meet stringent performance and environmental standards. Compliance with REACH regulations governing chemical substances used in optical materials ensures safety and sustainability in production. The EU’s Restriction of Hazardous Substances (RoHS) directive enforces limits on hazardous materials in electronics, directly impacting LED secondary optic components. National regulations in Germany and France mandate certification and testing of lighting products for performance and safety before market entry. Additionally, the European Committee for Standardization (CEN) has developed harmonized standards for LED lighting and optics, facilitating unified compliance across member states. These regulatory frameworks collectively shape product design, manufacturing processes, and market access strategies, promoting environmentally responsible and high-performance LED optical solutions in Europe.

- •Enforcement mechanisms include mandatory product labeling, periodic audits, and penalties for non-compliance, which incentivize manufacturers to adhere strictly to regulations. Stakeholders actively engage with regulatory bodies to influence standards that balance innovation and safety. The European Green Deal further reinforces focus on sustainable products, encouraging circular economy practices in optics manufacturing. Compliance with the Waste Electrical and Electronic Equipment (WEEE) directive requires manufacturers to implement take-back and recycling schemes for lighting products. These evolving policies necessitate ongoing monitoring and adaptation by market participants to ensure continued access to European markets and alignment with environmental goals.

- •Safety standards such as EN 62471 address photobiological safety of lamps and luminaires, guiding design parameters of secondary optics to minimize health risks. Environmental norms restrict emissions and waste generation during production, promoting cleaner manufacturing technologies. Operational guidelines specify testing protocols for optical performance, durability, and thermal management, ensuring product reliability. Country-specific mandates, including France’s energy efficiency incentives and Germany’s lighting upgrade subsidies, support market growth and encourage adoption of compliant optical solutions. Government initiatives provide grants and tax benefits for R&D in energy-saving lighting technologies, fostering innovation and competitiveness within the Europe LED Secondary Optic Market.

- •The regulatory landscape is dynamic, with periodic reviews and updates reflecting technological advancements and environmental priorities. Industry associations and standardization bodies collaborate to streamline compliance processes and promote best practices. Manufacturers must proactively engage in certification and testing to maintain market credibility and consumer trust. Regulatory foresight and strategic planning are critical for navigating complex requirements and leveraging incentives, ensuring sustainable growth and market leadership in the evolving Europe LED Secondary Optic Market.

- •Overall, the regulatory framework fosters a balance between innovation, safety, and sustainability, driving the development of high-quality, energy-efficient secondary optics aligned with Europe’s environmental commitments. Compliance not only mitigates risks but also enhances market reputation and customer confidence, serving as a competitive differentiator in the LED optics sector.

Market Intelligence

- •15th January 2025, Osram Licht AG (Germany) launched a new series of TIR lenses designed specifically for automotive LED headlamps, featuring enhanced light distribution and thermal management capabilities. These lenses incorporate advanced optical-grade silicone materials, providing superior durability and efficiency. The product line targets premium electric vehicle manufacturers aiming to meet stringent European safety and energy regulations. Osram’s strategic objective is to capture significant market share in the growing automotive lighting segment by combining innovative material science with precision manufacturing. This launch reinforces Osram’s position as a technology leader and supports the broader shift towards sustainable and intelligent lighting systems in Europe. Source: Osram Official Press Release

- •3rd March 2025, Ledil Oy (Finland) introduced a hybrid secondary optic solution integrating collimators and diffusers for street lighting applications. This innovation enhances beam uniformity and reduces glare, improving visual comfort and energy efficiency. The product leverages injection molding techniques with recyclable polymers, aligning with European environmental standards. Ledil’s market positioning focuses on smart city infrastructure, collaborating with municipal authorities across Europe to deploy adaptive lighting systems. Expected to reduce operational costs and carbon footprint, this solution addresses increasing demand for sustainable public lighting. The launch signifies a strategic move to expand Ledil’s footprint in the commercial lighting optics sector. Source: Ledil Press Release

- •10th February 2024, Fraen Corporation (Germany) announced a strategic partnership with a leading European automotive OEM to co-develop custom reflector optics for next-generation electric vehicles. The collaboration focuses on optimizing light output and aesthetic design while ensuring compliance with evolving safety standards. Fraen’s precision molding technology combined with the OEM’s design expertise aims to accelerate product development cycles and market introduction. This initiative highlights the growing importance of tailored secondary optics in enhancing vehicle performance and brand differentiation. The partnership also includes joint research on sustainable materials and manufacturing processes. This alliance strengthens Fraen’s market presence and innovation capabilities within Europe’s automotive lighting market. Source: Fraen Corporate Announcement

- •20th April 2025, Carclo plc (United Kingdom) completed the acquisition of a European optics startup specializing in 3D printed light guides for architectural lighting. The acquisition expands Carclo’s product portfolio with customizable, lightweight optics designed to meet bespoke architectural requirements. The startup’s innovative additive manufacturing approach enables rapid prototyping and production flexibility, addressing growing demand for unique lighting solutions in commercial and residential projects. This strategic move enhances Carclo’s competitive positioning in the Europe LED Secondary Optic Market by integrating advanced manufacturing technologies and design services. The acquisition supports Carclo’s long-term growth strategy focused on innovation and customer-centric solutions. Source: Carclo plc Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.95 Billion |

| Forecast Year Market Size | USD 2.45 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Osram Licht AG (Germany), Schott AG (Germany), Ledil Oy (Finland), Lumitronix LED-Technik GmbH (Germany), Fraen Corporation (Germany), Carclo plc (United Kingdom), Rheinberg Lichttechnik GmbH (Germany), ProPhotonix Limited (United Kingdom), Light Shape GmbH (Germany), Ledengin Ltd. (United Kingdom), Opto Engineering Srl (Italy), XAL GmbH (Austria), Tridonic GmbH & Co KG (Austria), LUXEON Technology (Netherlands), Carclo Technical Plastics (United Kingdom), Vossloh-Schwabe Deutschland GmbH (Germany), LED Roadway Lighting (France), Elix Lighting (France), Ledvance GmbH (Germany), Meyer Burger Technology AG (Switzerland), Lumileds Holding B.V. (Netherlands), Lumitronix LED-Technik GmbH (Germany), Gaggione S.r.l. (Italy), Voss Lighting GmbH (Germany), Zumtobel Group AG (Austria) |

Europe LED Secondary Optic Market - Europe Industry Size & Growth Analysis 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.