Global Biaxially Oriented Polypropylene (BOPP) Films Market Size, Growth & Revenue 2024-2034

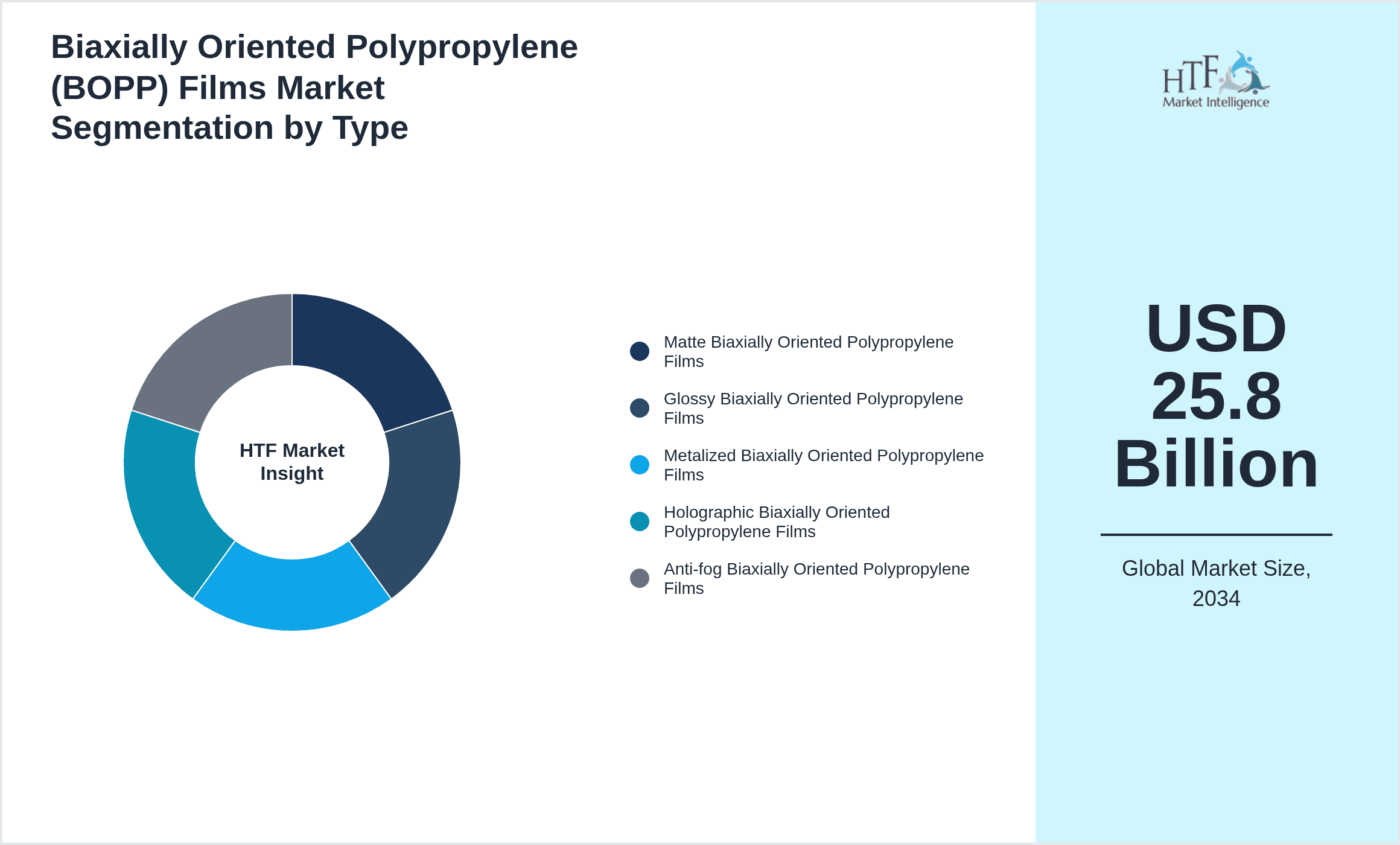

Global Biaxially Oriented Polypropylene (BOPP) Films Market is segmented by Type (Matte Biaxially Oriented Polypropylene Films, Glossy Biaxially Oriented Polypropylene Films, Metalized Biaxially Oriented Polypropylene Films, Holographic Biaxially Oriented Polypropylene Films, Anti-fog Biaxially Oriented Polypropylene Films), Application (Packaging, Labeling, Lamination, Industrial, Consumer Goods), End-Use Industry (Food & Beverage, Pharmaceuticals, Personal Care, Automotive, Electronics), Distribution Channel (Direct Sales, Distributors, Online Retail, Wholesale), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

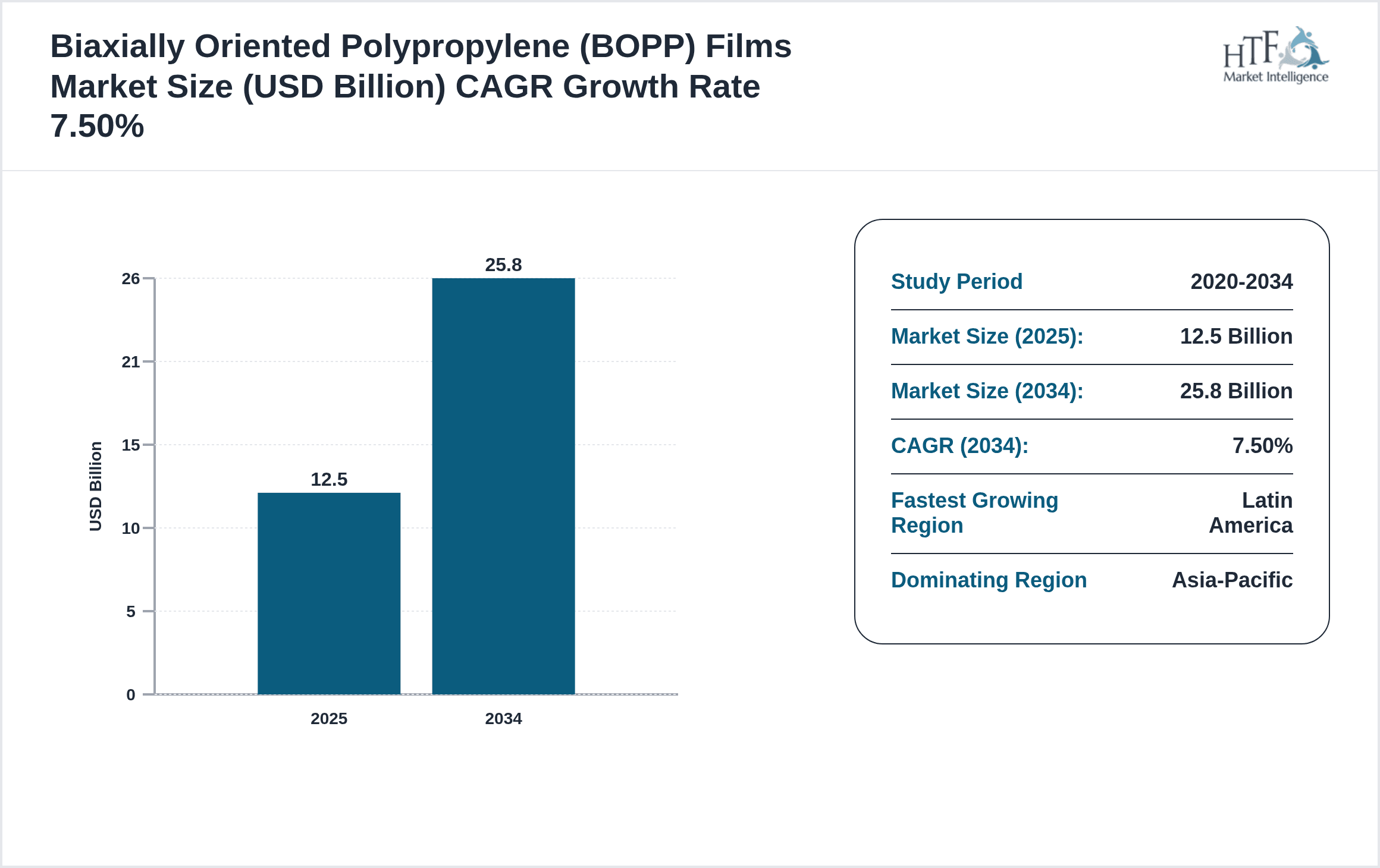

- •The Global Biaxially Oriented Polypropylene (BOPP) Films market represents a dynamic segment within the flexible packaging and industrial materials industry, defined by the production and application of polypropylene films oriented biaxially to enhance physical and optical properties. This market spans a wide range of film types including matte, glossy, metalized, holographic, and anti-fog variants, each serving distinct functions across packaging, labeling, lamination, industrial, and consumer goods sectors. The films' superior tensile strength, clarity, and barrier capabilities position them as preferred materials for food packaging, decorative labels, and protective wraps. Technological developments are driving innovations focused on sustainability, recyclability, and enhanced performance, responding to growing environmental concerns and regulatory demands. Geographically, the market is led by Asia-Pacific due to expanding manufacturing bases and rising demand from emerging economies, while Latin America is witnessing the fastest growth. The competitive landscape is marked by strategic partnerships, product innovation, and regional expansions. Forecasts indicate a strong CAGR of 7.5% through 2034, reflecting robust demand and evolving industry trends.

- •Key highlights include a base market valuation of USD 12.5 Billion in 2024 with an expected market size of USD 25.8 Billion by 2034, driven by increasing applications in packaging and labeling. Glossy BOPP dominates the product type segment, favored for its high clarity and printability, while anti-fog BOPP films are emerging rapidly due to their utility in fresh food packaging. Asia-Pacific commands a 38% market share, supported by strong manufacturing infrastructure and consumer markets. Latin America leads in growth rate at 9.3% CAGR, propelled by rising industrialization and demand for flexible packaging solutions. Market trends reveal a shift towards eco-friendly films and incorporation of nanotechnology to enhance barrier properties. Challenges include raw material price volatility and stringent environmental regulations. Opportunities lie in expanding applications in pharmaceuticals and e-commerce packaging, alongside advancements in biodegradable BOPP films.

- •The market's value proposition lies in offering versatile, cost-effective, and high-performance film solutions that enhance product protection, shelf life, and aesthetic appeal. This strategic importance spans industries such as food and beverage, personal care, and industrial sectors, where packaging integrity and visual differentiation are critical. Stakeholders benefit from continuous innovation in film technologies that address sustainability goals while maintaining functionality. The global reach and diverse application base create significant opportunities for manufacturers, converters, and suppliers to capitalize on evolving consumer preferences and regulatory landscapes. Investment in R&D and strategic alliances further underpin competitiveness, positioning the BOPP films market as a pivotal contributor to advancements in flexible packaging and material sciences worldwide.

Competitive Landscape

The competitive environment in the Global Biaxially Oriented Polypropylene (BOPP) Films market is characterized by intense rivalry among leading multinational corporations and regional players, focusing on innovation, product differentiation, and geographic expansion to secure market share. Companies invest heavily in R&D to develop advanced film variants such as anti-fog and biodegradable BOPP, aiming to meet stringent environmental standards and evolving customer demands. Strategic partnerships, mergers, and acquisitions are common tactics to enhance technological capabilities and broaden product portfolios. Pricing strategies are carefully balanced to maintain profitability amid raw material price fluctuations and competitive pressures. Distribution channel optimization and customer-centric service models further distinguish market leaders. Regional competition is vibrant, especially in Asia-Pacific where manufacturing hubs compete on scale and cost-efficiency. The future competitive landscape will likely witness increased consolidation, digitalization in supply chains, and sustainability-driven innovation as key factors shaping market trajectories.

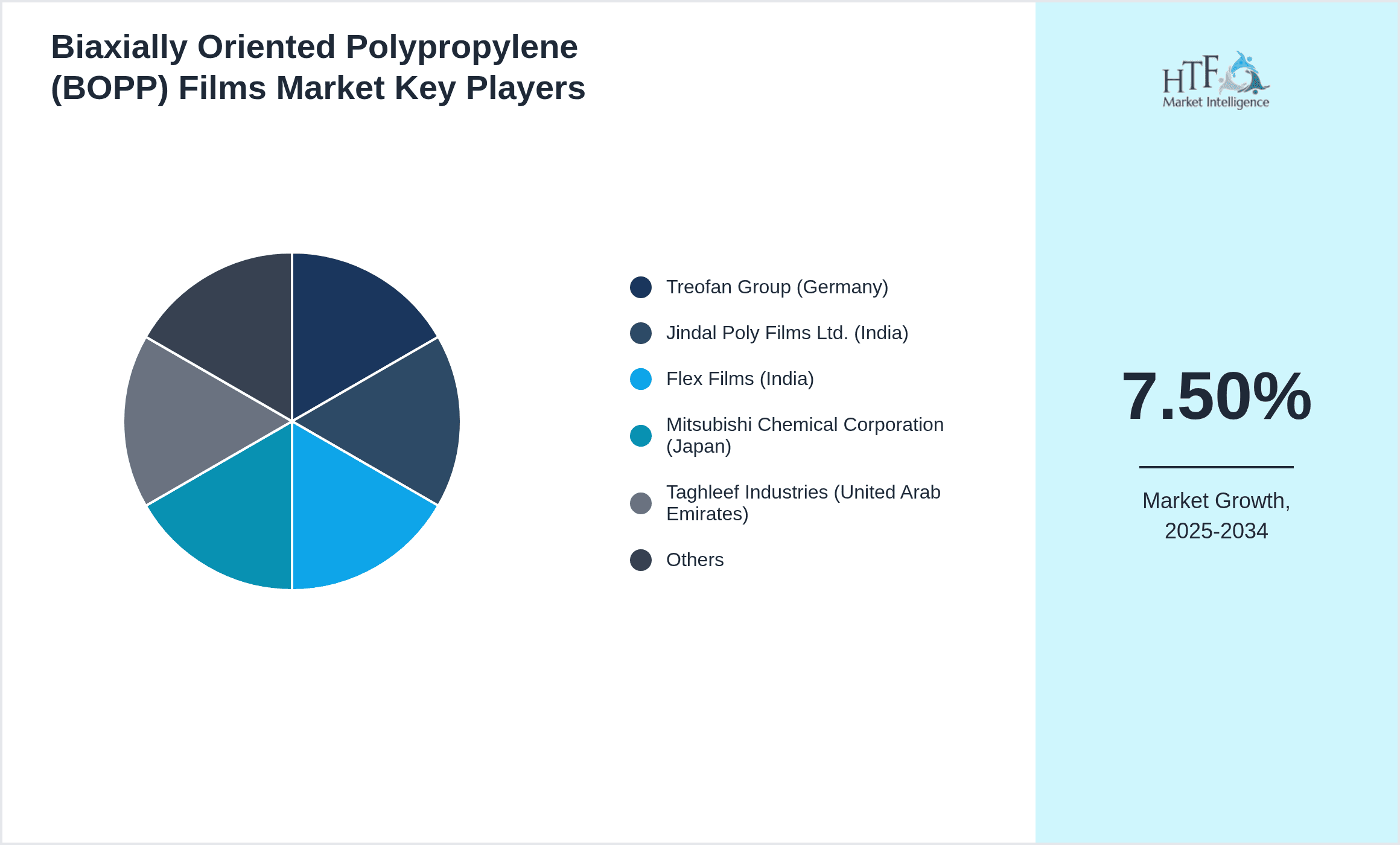

Leading Companies in Biaxially Oriented Polypropylene (BOPP) Films Market

- •Treofan Group (Germany)

- •Jindal Poly Films Ltd. (India)

- •Flex Films (India)

- •Mitsubishi Chemical Corporation (Japan)

- •Taghleef Industries (United Arab Emirates)

- •Cosmo Films Ltd. (India)

- •Innovia Films Ltd. (United Kingdom)

- •SRF Limited (India)

- •Jindal Films Inc. (United States)

- •Uflex Limited (India)

- •Wipak Group (Finland)

- •Bemis Company, Inc. (United States)

- •Mondi Group (United Kingdom)

- •Berry Global Group, Inc. (United States)

- •Amcor plc (Australia)

- •Winpak Ltd. (Canada)

- •Profol GmbH (Germany)

- •Nan Ya Plastics Corporation (Taiwan)

- •Toray Industries, Inc. (Japan)

- •Polyplex Corporation Limited (India)

- •Sealed Air Corporation (United States)

- •Constantia Flexibles (Austria)

- •Huhtamaki Oyj (Finland)

- •Intertape Polymer Group (Canada)

- •Bemis Company, Inc. (United States)

Market Breakdown

- •By Type

- ◦Matte Biaxially Oriented Polypropylene Films

- ◦Glossy Biaxially Oriented Polypropylene Films

- ◦Metalized Biaxially Oriented Polypropylene Films

- ◦Holographic Biaxially Oriented Polypropylene Films

- ◦Anti-fog Biaxially Oriented Polypropylene Films

- •By Application

- ◦Packaging

- ◦Labeling

- ◦Lamination

- ◦Industrial

- ◦Consumer Goods

- •By End-Use Industry

- ◦Food & Beverage

- ◦Pharmaceuticals

- ◦Personal Care

- ◦Automotive

- ◦Electronics

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Retail

- ◦Wholesale

Growth Dynamics

- •The global BOPP films market growth is primarily driven by rising demand for flexible packaging solutions due to increased consumer preference for convenience and product protection. The food and beverage industry extensively uses BOPP films for their excellent barrier and aesthetic qualities, accelerating adoption. Technological advancements enabling biodegradable and anti-fog films address environmental concerns, further propelling market expansion. Additionally, growth in e-commerce and pharmaceutical sectors fuels demand for labeling and lamination applications. Government initiatives promoting sustainable packaging and regulations against single-use plastics motivate manufacturers to innovate, enhancing market growth prospects. The expanding middle-class population in emerging economies and increasing disposable incomes also contribute to heightened consumption of packaged goods, positively influencing BOPP films demand.

- •Trends in the BOPP films market include a significant shift toward sustainable and recyclable film solutions, with companies investing in bio-based raw materials and advanced recycling technologies. There is a growing adoption of anti-fog and metalized films to enhance product shelf life and visual appeal. Digital printing and customization capabilities are becoming increasingly prevalent, enabling brand differentiation. The integration of nanotechnology to improve barrier properties and mechanical strength is gaining traction. Collaborations between film manufacturers and packaging converters facilitate faster innovation cycles. Furthermore, regional diversification strategies are prominent as companies target emerging markets in Asia-Pacific and Latin America to capitalize on growing demand. The COVID-19 pandemic has also accelerated demand for pharmaceutical and food-grade films, highlighting the market's resilience and adaptability.

- •Market restraints include volatility in raw material prices, particularly polypropylene resin, which affects production costs and profitability. Environmental concerns and stringent regulations on plastic usage impose compliance challenges, necessitating costly innovations and adjustments. The recycling infrastructure in many developing regions is inadequate, limiting the market penetration of sustainable BOPP films. Competition from alternative packaging materials such as polyethylene terephthalate (PET) and biodegradable polymers poses substitution risks. Additionally, the capital-intensive nature of film manufacturing and technological upgrades restricts entry for smaller players. Supply chain disruptions, especially in resin availability and logistics, can hamper consistent production. These factors collectively constrain market growth and require strategic mitigation by industry participants.

- •Opportunities abound in expanding applications of BOPP films beyond traditional packaging into pharmaceuticals, electronics, and automotive sectors, driven by their protective and lightweight properties. Innovations in biodegradable and compostable BOPP films open new market segments aligned with sustainability trends. The rising demand for premium labeling and decorative films in luxury consumer goods presents growth avenues. Geographic expansion into high-growth regions such as Latin America and Middle East & Africa offers untapped potential. Digital printing advances enable personalized packaging, enhancing consumer engagement. Strategic partnerships and mergers to combine technological expertise and market reach can accelerate penetration. Additionally, the emergence of circular economy models encourages investment in closed-loop recycling systems, creating new revenue streams.

- •Challenges include navigating complex regulatory environments with varying standards across regions, impacting product formulations and certifications. The reliance on fossil-fuel-based polypropylene subjects the market to environmental scrutiny and supply volatility. Achieving a balance between sustainability goals and maintaining film performance demands continuous R&D investment. Market fragmentation and intense competition drive pricing pressures, affecting margins. Educating end-users on the benefits and proper disposal of BOPP films remains a hurdle. Furthermore, fluctuating demand due to economic uncertainties can disrupt production planning. Addressing these challenges requires collaborative efforts among manufacturers, regulators, and supply chain partners to foster innovation and sustainability.

Market Trends

- •The BOPP films market is witnessing accelerated adoption of sustainable packaging solutions, with manufacturers incorporating recycled and bio-based materials to reduce environmental footprint. This trend aligns with global regulatory pressures and consumer demand for eco-friendly products, stimulating innovation and new product launches.

- •Digital and flexographic printing technologies are increasingly integrated into BOPP film production, enabling high-quality, customizable, and cost-effective packaging designs. This facilitates brand differentiation and responsiveness to diverse market needs, enhancing customer engagement.

- •Anti-fog and metalized BOPP films are gaining popularity due to their ability to extend shelf life and improve visual appeal, particularly in fresh food and beverage packaging. These functional enhancements are contributing to market growth and competitive positioning.

- •Collaborations between film manufacturers and packaging converters are becoming strategic to accelerate innovation cycles, optimize supply chains, and deliver integrated solutions that address complex customer requirements efficiently.

- •Emerging markets in Asia-Pacific and Latin America are experiencing rapid industrialization and urbanization, leading to increased demand for packaged goods and subsequently driving regional BOPP films consumption and production capacities.

- •The COVID-19 pandemic has highlighted the importance of hygienic and protective packaging, boosting demand for pharmaceutical-grade BOPP films and elevating standards for safety and traceability within the supply chain.

- •Technological advancements in nanocomposites and coating technologies are enhancing barrier properties and mechanical strength of BOPP films, enabling their use in more demanding industrial applications and expanding the market scope.

Market Opportunities

- •Expanding into pharmaceutical packaging offers significant growth potential for BOPP films due to stringent protection and regulatory requirements, combined with increasing global healthcare expenditure. Innovation in tamper-evident and child-resistant films can capture this niche.

- •Developing biodegradable and compostable BOPP films addresses growing environmental concerns and regulatory mandates, opening new markets among eco-conscious consumers and regions with strict plastic waste policies.

- •Leveraging digital printing capabilities to offer customized and premium packaging solutions can enhance brand value for consumer goods companies, driving demand for specialized BOPP films with unique visual and tactile properties.

- •Geographic expansion into Latin America and Middle East & Africa provides opportunities to serve emerging industrial and consumer markets with tailored BOPP film solutions, supported by favorable demographic and economic trends.

- •Forming strategic partnerships and joint ventures can accelerate access to new technologies, distribution networks, and customer segments, fostering innovation and competitive advantage in the global marketplace.

- •Investing in circular economy initiatives and closed-loop recycling systems can create sustainable business models, reduce environmental impact, and appeal to increasingly eco-aware stakeholders.

- •Exploring applications in electronics and automotive sectors expands the demand base for high-performance BOPP films, particularly where lightweight and protective materials are critical to product development.

Market Challenges

- •Navigating diverse regulatory requirements globally complicates product development and market entry for BOPP film manufacturers, necessitating extensive compliance efforts and localized strategies to meet environmental and safety standards.

- •Volatility in polypropylene resin prices, driven by crude oil market fluctuations, directly impacts manufacturing costs and pricing strategies, challenging profitability and supply chain stability.

- •Balancing sustainability with performance remains complex, as bio-based or recycled raw materials may compromise film quality or increase production costs, requiring ongoing innovation and process optimization.

- •Intense competition from alternative packaging materials such as PET and biodegradable polymers threatens market share and necessitates continuous differentiation through technology and service excellence.

- •Limited recycling infrastructure in developing markets restricts the adoption of sustainable BOPP films, affecting environmental impact and regulatory compliance, thus posing a barrier to market expansion.

- •Market fragmentation and price sensitivity, especially among small and medium-sized end users, pressure margins and complicate scale economies for producers.

- •Supply chain disruptions including logistics challenges and raw material shortages can delay production schedules and affect customer satisfaction, requiring robust risk management frameworks.

Regulatory Framework

- •Between 2019 and 2024, global regulations intensified on single-use plastics, compelling BOPP film manufacturers to innovate sustainable alternatives and comply with bans and reduction mandates, significantly influencing product development cycles.

- •The European Union’s Circular Economy Action Plan introduced strict guidelines on recyclability and waste reduction for packaging films, leading to mandatory compliance for BOPP films used in the region, affecting global supply chains.

- •New regulations on food contact materials were enacted in North America, requiring enhanced testing and certification for BOPP films to ensure consumer safety and traceability, impacting production and distribution protocols.

- •Environmental Protection Agencies in Asia-Pacific countries implemented extended producer responsibility (EPR) schemes, obligating manufacturers to manage post-consumer waste, driving investments in recyclable and biodegradable BOPP film solutions.

- •Government incentive programs encouraging sustainable packaging innovations have emerged globally, providing subsidies and tax benefits to companies developing eco-friendly BOPP films, fostering industry-wide shifts towards greener technologies.

Market Intelligence

- •15th March 2024, Treofan Group launched a new line of biodegradable BOPP films designed specifically for food packaging applications, featuring enhanced barrier properties and compostability certified under international standards. This launch supports the company's commitment to sustainability and meets rising consumer demand for eco-friendly packaging. The new product is expected to capture significant market share in Europe and North America, providing a competitive edge and aligning with regulatory trends favoring biodegradable materials. Treofan's strategic focus on R&D and sustainability positions it as an industry leader in innovation.

- •22nd July 2023, Taghleef Industries announced a strategic partnership with a leading packaging converter in Asia-Pacific to expand the distribution of its advanced anti-fog BOPP films. This collaboration aims to accelerate market penetration in the fresh food sector, enhancing shelf life and consumer appeal. The partnership leverages Taghleef’s technological expertise and the converter’s regional market knowledge, enabling customized solutions tailored to local consumer preferences. This initiative reflects the growing trend of localized partnerships to address diverse market demands effectively.

- •5th November 2024, Jindal Poly Films Ltd. completed the acquisition of a European BOPP film manufacturer, enhancing its global footprint and product portfolio. This acquisition bolsters Jindal’s position in premium film segments such as metalized and holographic films, expanding its reach across Europe and North America. The consolidation facilitates technology exchange, economies of scale, and increased R&D capabilities, strengthening competitive positioning amid intensifying market rivalry.

- •30th January 2025, Cosmo Films Ltd. introduced a digitally printable BOPP film variant with improved surface smoothness and print adhesion, catering to the growing demand for high-quality, customized packaging. This innovation supports brand owners seeking premium aesthetics and enhanced consumer engagement. The product launch aligns with market trends emphasizing digitalization and personalization across various end-use industries, including food, cosmetics, and pharmaceuticals.

- •Source: Official press releases, company websites, industry publications

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 25.8 Billion |

| CAGR | 7.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.25% |

| Scope of Report | Market is segmented by Type (Matte Biaxially Oriented Polypropylene Films, Glossy Biaxially Oriented Polypropylene Films, Metalized Biaxially Oriented Polypropylene Films, Holographic Biaxially Oriented Polypropylene Films, Anti-fog Biaxially Oriented Polypropylene Films), Application (Packaging, Labeling, Lamination, Industrial, Consumer Goods), End-Use Industry (Food & Beverage, Pharmaceuticals, Personal Care, Automotive, Electronics), Distribution Channel (Direct Sales, Distributors, Online Retail, Wholesale) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Treofan Group (Germany), Jindal Poly Films Ltd. (India), Flex Films (India), Mitsubishi Chemical Corporation (Japan), Taghleef Industries (United Arab Emirates), Cosmo Films Ltd. (India), Innovia Films Ltd. (United Kingdom), SRF Limited (India), Jindal Films Inc. (United States), Uflex Limited (India), Wipak Group (Finland), Bemis Company, Inc. (United States), Mondi Group (United Kingdom), Berry Global Group, Inc. (United States), Amcor plc (Australia), Winpak Ltd. (Canada), Profol GmbH (Germany), Nan Ya Plastics Corporation (Taiwan), Toray Industries, Inc. (Japan), Polyplex Corporation Limited (India), Sealed Air Corporation (United States), Constantia Flexibles (Austria), Huhtamaki Oyj (Finland), Intertape Polymer Group (Canada), Bemis Company, Inc. (United States) |

Global Biaxially Oriented Polypropylene (BOPP) Films Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.