EMEA Biosynthetic Squalene Market Scope & Changing Dynamics 2024-2034

EMEA Biosynthetic Squalene Market is segmented by Biosynthetic Squalene Type (Plant-Derived Biosynthetic Squalene, Microbial-Derived Biosynthetic Squalene, Synthetic Biosynthetic Squalene, Animal-Derived Biosynthetic Squalene, Others), Application Segment (Cosmetics, Pharmaceuticals, Food & Beverage, Nutraceuticals, Industrial Applications), End-User Industry (Personal Care and Beauty, Healthcare and Pharmaceuticals, Food Processing, Dietary Supplements), Distribution Channel (Direct Sales, Distributors and Wholesalers, Online Retail, Specialty Ingredient Suppliers), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Biosynthetic Squalene Market is a specialized segment focusing on the production and utilization of squalene derived through biosynthetic methods, including plant extraction, microbial fermentation, and synthetic chemistry. This market serves critical applications in cosmetics, pharmaceuticals, food and beverage, and nutraceutical sectors, leveraging biosynthetic squalene’s benefits such as sustainability, purity, and ethical sourcing. The market excludes animal-derived squalene, emphasizing alternative biotechnological approaches that align with environmental regulations and consumer demand for cruelty-free products. Covering countries across Europe, the Middle East, and Africa, the market reflects diverse regulatory frameworks and economic conditions, influencing product adoption and innovation. Key characteristics include high demand for natural and sustainable ingredients, increasing applications in vaccine adjuvants, and growth in personal care products. The market scope also includes supply chain dynamics, regional production hubs, and technological advances in fermentation and extraction methods. Primary use cases focus on enhancing product efficacy, shelf life, and consumer appeal across multiple industries, positioning biosynthetic squalene as a strategic ingredient in EMEA’s evolving bio-based chemical landscape.

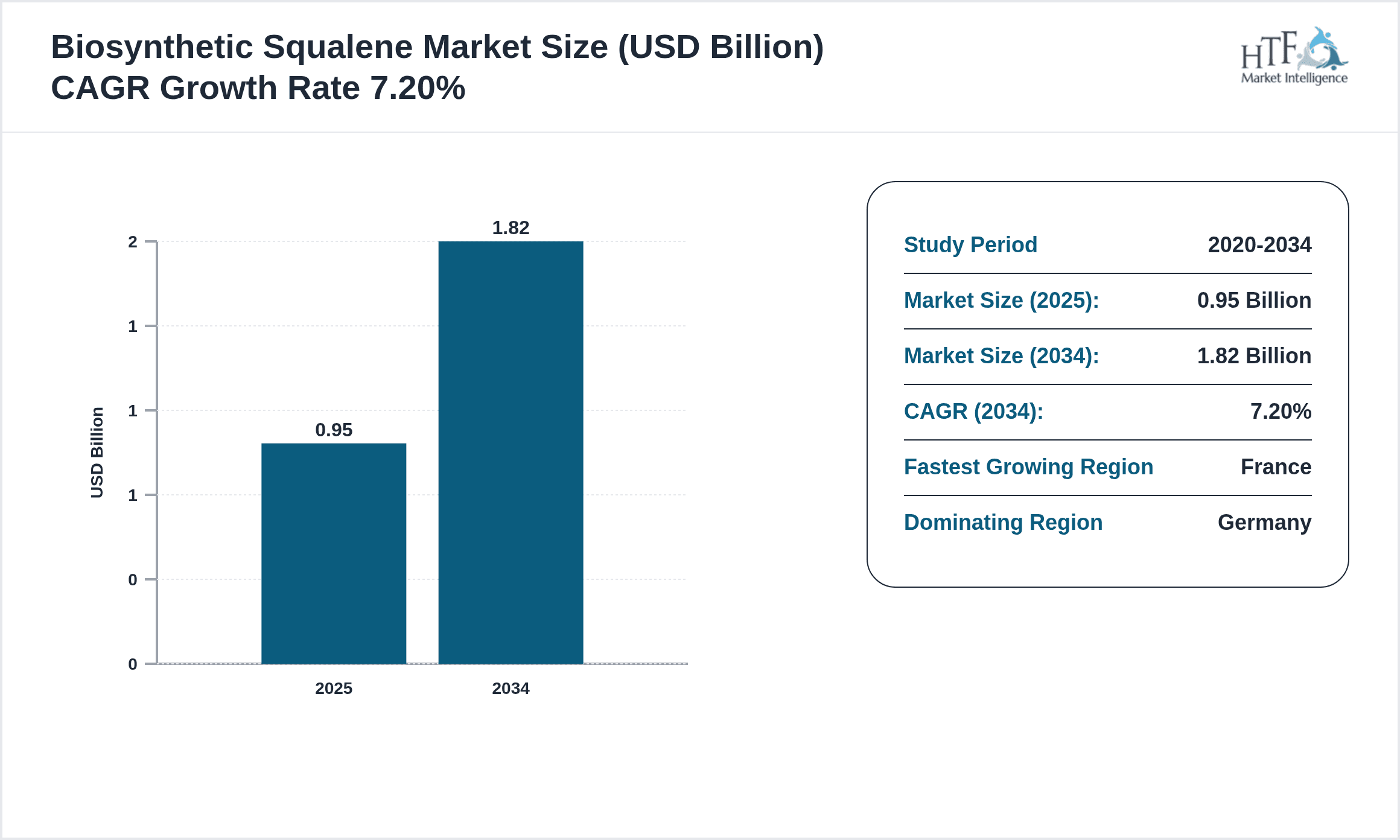

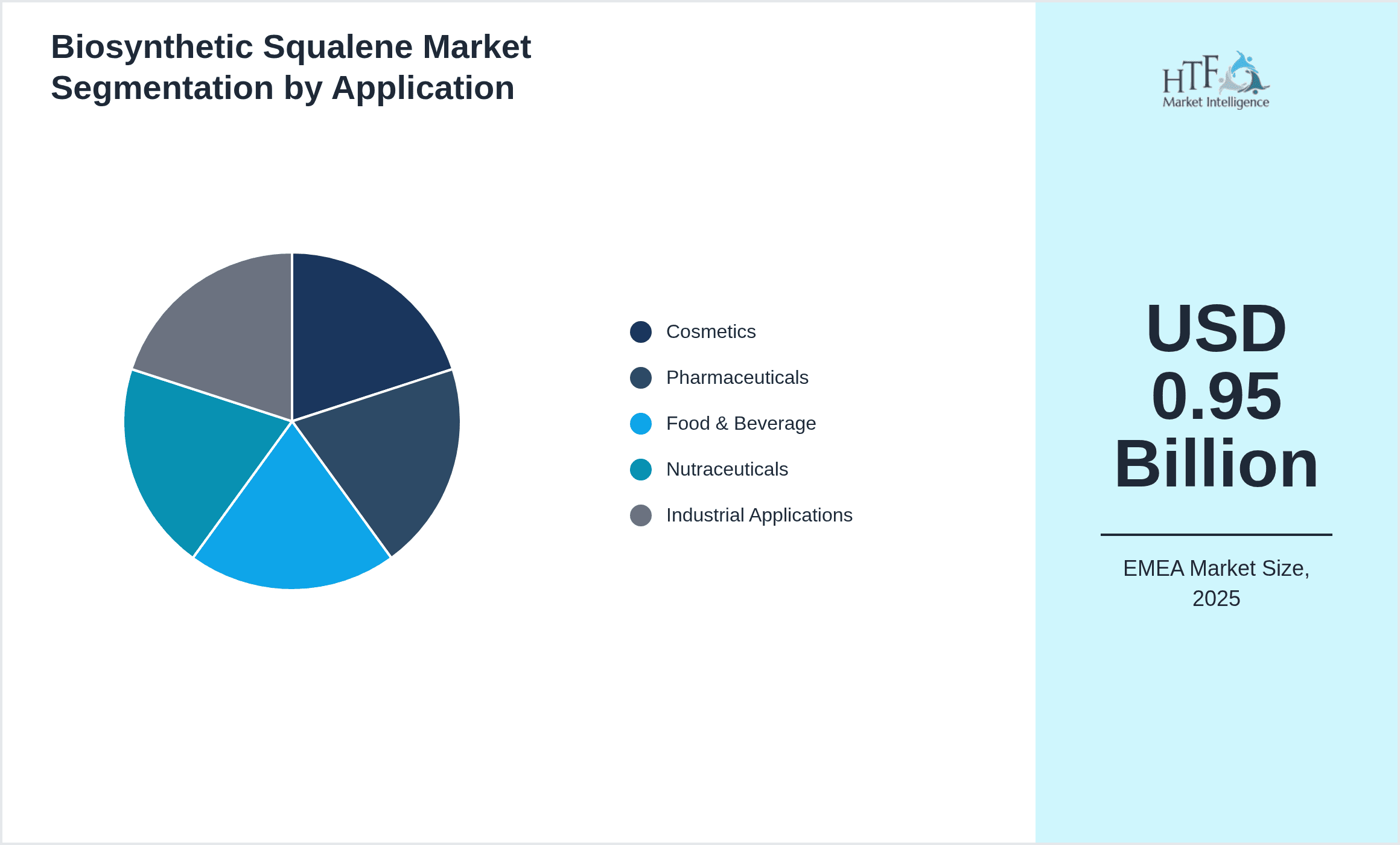

- •Key highlights of the EMEA Biosynthetic Squalene Market include a base market size of USD 0.95 Billion in 2025, projected to reach USD 1.82 Billion by 2034, demonstrating a robust CAGR of 7.2%. Germany leads the regional market with a 28% share, while France is the fastest-growing country, expected to expand at a CAGR of 9.1%. Among product types, plant-derived biosynthetic squalene dominates due to established supply chains and consumer preference for botanical ingredients. Microbial-derived biosynthetic squalene is the fastest growing, driven by advancements in fermentation technologies and increasing investment in sustainable manufacturing. Applications in cosmetics represent the largest revenue segment, followed by pharmaceuticals, leveraging squalene’s efficacy as an emollient and adjuvant. The market benefits from growing consumer awareness of ethical sourcing and stringent regulations pushing for alternatives to animal-derived squalene. The forecast period will witness increased innovation, strategic partnerships, and expansion of production capabilities across EMEA.

- •The EMEA Biosynthetic Squalene Market holds significant strategic importance for cosmetic manufacturers, pharmaceutical companies, and food ingredient suppliers aiming to meet sustainability and regulatory mandates while catering to evolving consumer preferences. Its role as a renewable and ethically sourced alternative to shark-derived squalene enhances corporate social responsibility profiles and aligns with green chemistry initiatives. The market’s growth supports regional economic development through biotechnology investments and innovation in bio-based chemicals. Stakeholders benefit from diverse applications, including vaccine development, skincare formulations, and functional food enrichment, creating multiple revenue streams. Additionally, the evolving regulatory landscape in Europe and neighboring regions fosters market transparency and product standardization, enabling companies to capitalize on emerging opportunities. Overall, the biosynthetic squalene market in EMEA is positioned as a critical growth area supporting environmental stewardship, technological advancement, and cross-industry collaboration.

Competitive Landscape

The competitive environment in the EMEA Biosynthetic Squalene Market is characterized by a mix of established chemical manufacturers, biotechnology firms, and specialty ingredient suppliers focusing on innovation, sustainability, and strategic collaborations. Players compete on product purity, cost efficiency, and regulatory compliance, emphasizing proprietary biosynthetic technologies such as advanced microbial fermentation and green extraction processes. Market rivalry intensifies with increased R&D investments aimed at scaling biosynthetic production to meet growing demand across cosmetics and pharmaceuticals. Companies leverage partnerships with research institutions and contract manufacturers to accelerate time-to-market and diversify application portfolios. Pricing strategies balance raw material costs and premium positioning for ethically sourced biosynthetic squalene. Distribution channel optimization and regional manufacturing hubs enhance market reach and responsiveness to regulatory changes. Future competitive trends indicate consolidation through mergers and acquisitions, expanded product differentiation through formulation innovation, and increased emphasis on certifications and sustainability credentials to gain market share in a demanding EMEA environment.

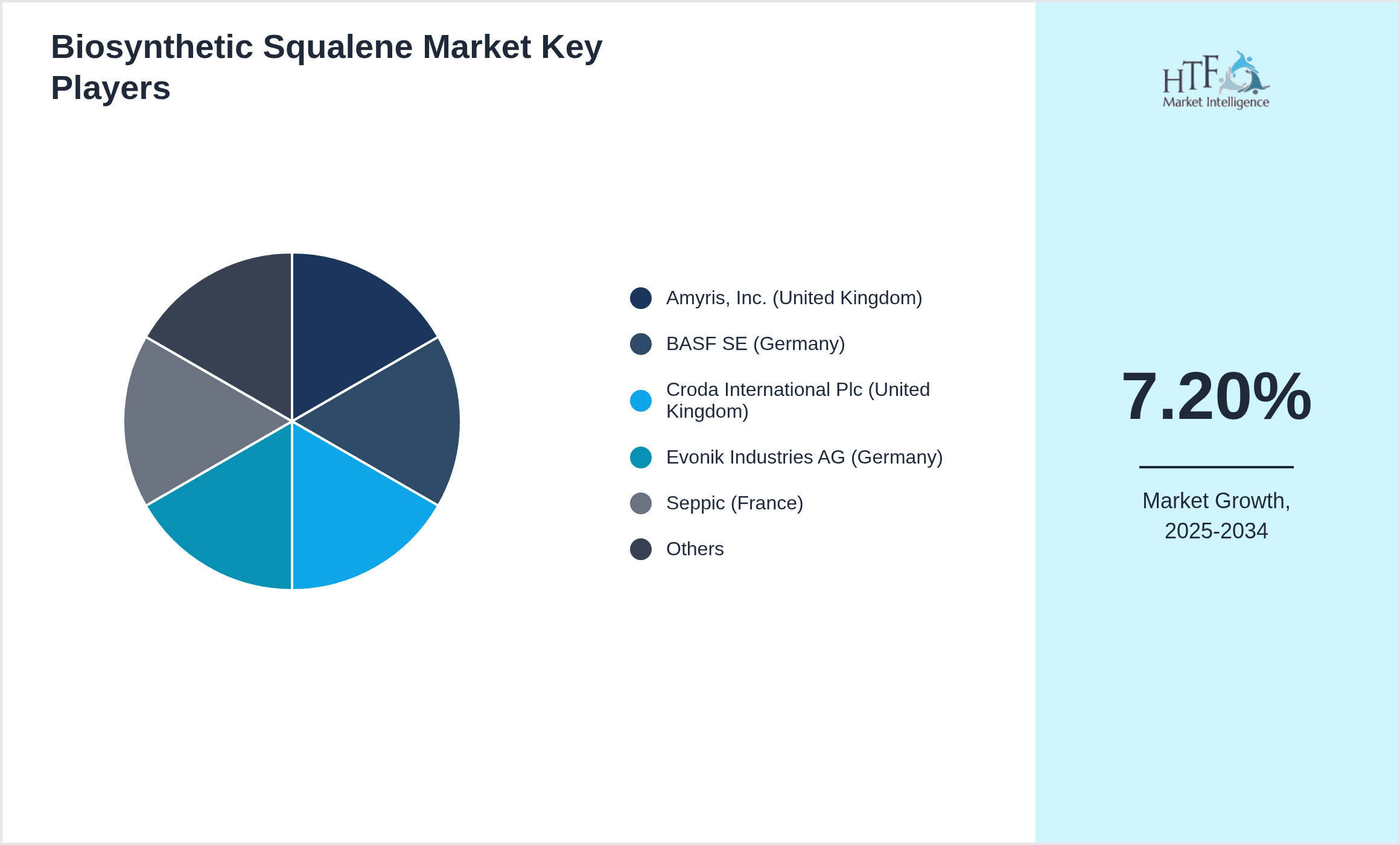

Leading Companies in EMEA Biosynthetic Squalene Market

- •Amyris, Inc. (United Kingdom)

- •BASF SE (Germany)

- •Croda International Plc (United Kingdom)

- •Evonik Industries AG (Germany)

- •Seppic (France)

- •Givaudan SA (Switzerland)

- •Clariant AG (Switzerland)

- •Symrise AG (Germany)

- •Lonza Group AG (Switzerland)

- •Lipoid GmbH (Germany)

- •Indena S.p.A. (Italy)

- •Sophim (France)

- •Evonik Nutrition & Care GmbH (Germany)

- •Sederma (France)

- •Sasol Limited (South Africa)

- •Brenntag AG (Germany)

- •Mibelle Group (Switzerland)

- •Croda France SAS (France)

- •Bio-Botanica, Inc. (Germany)

- •Symrise France SAS (France)

- •Evonik South Africa (South Africa)

- •BASF South Africa (South Africa)

- •L’Oréal Group (France)

- •Univar Solutions (Netherlands)

- •Clariant UK Ltd. (United Kingdom)

Market Breakdown

- •By Biosynthetic Squalene Type

- ◦Plant-Derived Biosynthetic Squalene

- ◦Microbial-Derived Biosynthetic Squalene

- ◦Synthetic Biosynthetic Squalene

- ◦Animal-Derived Biosynthetic Squalene

- ◦Others

- •By Application Segment

- ◦Cosmetics

- ◦Pharmaceuticals

- ◦Food & Beverage

- ◦Nutraceuticals

- ◦Industrial Applications

- •By End-User Industry

- ◦Personal Care and Beauty

- ◦Healthcare and Pharmaceuticals

- ◦Food Processing

- ◦Dietary Supplements

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Wholesalers

- ◦Online Retail

- ◦Specialty Ingredient Suppliers

Growth Dynamics

- •The EMEA Biosynthetic Squalene Market growth is propelled by increasing demand for sustainable and ethically sourced ingredients in cosmetics and pharmaceuticals. Consumers and manufacturers prioritize plant-based and microbial-derived squalene due to animal welfare concerns. Technological improvements in biosynthesis methods reduce production costs and enhance product purity, enabling wider adoption. Moreover, rising awareness of biosynthetic squalene’s benefits in vaccine adjuvants and skin-care formulations catalyzes market expansion. Regional regulations favoring natural and cruelty-free ingredients further stimulate demand. The growing health-conscious population in Europe and Middle East drives nutraceutical and dietary supplement applications, contributing additional market momentum. The integration of biosynthetic squalene in premium personal care products adds value and differentiation, attracting investment and innovation within the supply chain.

- •Emerging trends include the increased use of microbial fermentation technologies for squalene production, offering scalable, consistent, and eco-friendly alternatives. Companies invest in genetic engineering to optimize microorganisms for higher yields and lower environmental footprint. The cosmetics industry is witnessing a shift towards clean-label and vegan-certified products leveraging biosynthetic squalene. Additionally, pharmaceutical applications expand with squalene-based vaccine adjuvants, enhanced drug delivery systems, and anti-inflammatory formulations. Strategic collaborations between biotechnology firms and cosmetic manufacturers facilitate product development and faster commercialization. Digital marketing emphasizes sustainability credentials, influencing consumer purchase decisions across EMEA. The trend of circular economy principles encourages recycling and bio-based raw material sourcing, aligning with biosynthetic squalene’s market positioning.

- •Market restraints include high production costs associated with biosynthetic processes compared to traditional animal-derived squalene, limiting price competitiveness. Supply chain complexities and scalability challenges can delay market penetration, especially in emerging EMEA economies. Regulatory compliance across multiple jurisdictions imposes additional costs and time to market, particularly concerning purity standards and labeling. Consumer skepticism regarding synthetic origins versus natural sources may hinder adoption in certain segments. Furthermore, competition from chemically synthesized squalene and other emollients poses substitution risks. Limited awareness among end-users about biosynthetic squalene’s benefits restricts demand growth. These factors collectively temper market expansion and necessitate continued innovation and education.

- •Opportunities abound in expanding biosynthetic squalene applications beyond cosmetics into pharmaceuticals, particularly as vaccine adjuvants and drug delivery enhancers, driven by ongoing medical research. The growing nutraceutical segment presents demand for bioactive ingredient fortification with squalene’s antioxidant properties. Innovations in microbial engineering and fermentation can lower production costs, enhancing affordability and market accessibility. Geographic expansion into underserved Middle Eastern and African markets offers untapped potential as regulatory frameworks evolve. Strategic partnerships between biosynthesis technology developers and end-user industries can accelerate product development and acceptance. Additionally, increasing consumer inclination towards vegan and cruelty-free products creates marketing advantages. Technological advancements enabling scale-up and quality assurance further solidify growth prospects across EMEA.

- •Challenges include navigating complex and diverse regulatory environments across EMEA countries, requiring harmonization of standards for biosynthetic squalene. High capital investment for fermentation infrastructure and biotechnology R&D constrains smaller players. Fluctuations in raw material availability for plant-based squalene affect supply stability and pricing. Intense competition from established chemical suppliers and animal-derived squalene producers pressures market share. The need for extensive consumer education to overcome misconceptions about biosynthetic origins demands marketing resources. Supply chain disruptions and geopolitical uncertainties in parts of the Middle East and Africa add risk. Addressing scalability, cost-effectiveness, and regulatory compliance simultaneously remains a critical hurdle for sustained market advancement.

Market Trends

- •A significant trend is the rise of microbial-derived biosynthetic squalene, favored for its sustainability and reduced environmental impact. Advances in synthetic biology have enabled higher yields and cost efficiency, making it a preferred alternative to plant and animal sources. This trend aligns with increasing regulatory scrutiny on animal-derived ingredients and consumer demand for vegan products. Leading players are incorporating microbial squalene into premium cosmetic lines, emphasizing its purity and ethical sourcing. The shift toward green chemistry principles and clean-label formulations is reshaping product development strategies across EMEA.

- •The cosmetics sector is adopting biosynthetic squalene extensively for anti-aging and moisturizing formulations, driven by its skin compatibility and bioavailability. Companies are innovating with squalene-enriched serums and creams, positioning them as natural yet technologically advanced solutions. This trend is supported by growing consumer preferences for products combining efficacy with sustainability. Additionally, digital platforms and influencer marketing campaigns highlight biosynthetic squalene’s benefits, accelerating market penetration and brand loyalty.

- •Pharmaceutical applications of biosynthetic squalene, particularly as vaccine adjuvants and drug delivery agents, have gained traction post-pandemic. Research investments focus on enhancing immune response and optimizing formulation stability. Regulatory approvals for squalene-based adjuvants in EMEA countries have opened pathways for broader adoption. This trend underscores the intersection of biotechnology and healthcare innovation, with manufacturers exploring novel formulations incorporating biosynthetic squalene to improve therapeutic outcomes.

- •Sustainability and traceability are becoming central to supply chain strategies in the biosynthetic squalene market. Companies implement blockchain and certification systems to assure end-users of ethical sourcing and environmental compliance. This trend responds to increasing regulatory mandates and consumer demand for transparency. It drives investments in sustainable feedstock procurement and waste reduction throughout the biosynthesis process, reinforcing brand reputation and regulatory adherence.

- •Collaborative innovation ecosystems are emerging, involving partnerships between biotech firms, academic institutions, and cosmetic conglomerates. These alliances accelerate technology transfer, optimize production methods, and foster product diversification. The trend supports faster commercialization cycles and enhanced market responsiveness. Joint ventures and licensing agreements facilitate access to regional markets within EMEA, overcoming regulatory and logistical barriers while sharing risk and expertise.

Market Opportunities

- •Expanding pharmaceutical applications present significant opportunities, especially in vaccine formulations and targeted drug delivery systems that leverage biosynthetic squalene’s immunomodulatory properties. Increasing healthcare investments across Europe and the Middle East underpin demand growth, with potential for novel adjuvant development. Companies can capitalize on unmet needs for safer, more effective vaccine components, driving R&D and partnerships.

- •Emerging nutraceutical markets in EMEA offer growth potential through incorporation of biosynthetic squalene as a functional ingredient with antioxidant and anti-inflammatory benefits. Rising health awareness and aging populations in key countries create demand for dietary supplements fortified with natural bioactives. This segment allows product innovation and premium positioning.

- •Technological advancements in microbial fermentation and synthetic biology reduce production costs and enhance scalability. Adoption of these innovations enables new entrants to compete effectively and expands supply capacity. Market players investing in proprietary biosynthetic platforms can achieve competitive differentiation and faster market access.

- •Geographic expansion into Middle Eastern and African countries with growing cosmetics and pharmaceutical sectors represents untapped markets. Improving regulatory frameworks and increasing consumer sophistication support adoption of biosynthetic squalene-based products. Localized production and distribution partnerships can facilitate market entry and growth.

- •Strategic collaborations between biosynthesis technology firms and end-user industries enable co-development of tailored squalene formulations. These partnerships optimize product efficacy and market fit, accelerating commercialization. Joint ventures and licensing agreements help navigate regulatory complexities and extend regional footprints within EMEA.

Market Challenges

- •The market faces challenges from high capital and operational expenditures required for biosynthetic squalene production facilities, limiting participation mainly to well-funded companies. Smaller players struggle with access to advanced biotechnology and fermentation infrastructure, restricting innovation and scale.

- •Diverse and stringent regulatory requirements across EMEA nations create compliance complexities and increase time-to-market. Variations in purity standards, labeling mandates, and import-export regulations necessitate significant resources for certification and ongoing monitoring.

- •Raw material supply chain volatility, particularly for plant-based feedstocks, affects production schedules and pricing stability. Climatic and geopolitical factors disrupt consistent availability, impacting manufacturer reliability and profitability.

- •Consumer perception challenges persist where biosynthetic or synthetic origins are conflated with artificial ingredients, hindering acceptance among certain demographics preferring traditional natural sources. Extensive education and marketing investments are required to overcome skepticism.

- •Competition from established animal-derived squalene suppliers and alternative emollients limits market penetration, especially in price-sensitive segments. Differentiation through sustainability and efficacy claims remains essential but not always sufficient to capture market share.

Regulatory Framework

- •Between 2020 and 2025, the European Union implemented the REACH regulation updates, tightening chemical safety assessments and requiring comprehensive data on biosynthetic ingredient toxicity and environmental impact. This mandates manufacturers to ensure biosynthetic squalene complies with stringent safety and labeling standards, impacting production and marketing strategies.

- •In 2023, the EU Cosmetics Regulation (EC) No 1223/2009 was amended to emphasize cruelty-free and vegan certifications, compelling companies to certify biosynthetic squalene origins and prohibit animal-derived ingredients. This regulatory shift has accelerated biosynthetic squalene adoption in personal care products.

- •Pharmaceutical regulations under EMA guidelines updated in 2022 reinforced quality control and traceability for vaccine adjuvants, including squalene-based components. Companies marketing biosynthetic squalene in pharmaceutical applications must now meet enhanced GMP and documentation requirements.

- •Middle East countries, notably the UAE and Saudi Arabia, have introduced import and product registration regulations since 2021 that align closely with EU standards, facilitating smoother market access for biosynthetic squalene products while ensuring consumer safety.

- •Industry-wide initiatives support alignment with ISO sustainability certifications and green chemistry standards, encouraging adoption of biosynthetic processes and fostering transparency in supply chains. These voluntary frameworks complement mandatory regulations and enhance market credibility.

Market Intelligence

- •15th January 2025, Amyris, Inc. announced the launch of a new microbial-derived biosynthetic squalene production facility in the United Kingdom aimed at scaling sustainable supply to the European cosmetics and pharmaceutical industries. The plant employs proprietary fermentation technology to enhance yield and product purity while reducing carbon footprint. This initiative strategically positions Amyris as a key supplier in the growing biosynthetic squalene market within EMEA, enabling partnerships with leading personal care and vaccine manufacturers seeking ethical sourcing solutions. The facility’s operational start is expected to meet increasing demand driven by regulatory shifts and consumer preferences for cruelty-free ingredients. Source: Amyris Press Release

- •20th March 2025, BASF SE introduced an innovative synthetic biosynthetic squalene grade tailored for pharmaceutical applications, focusing on vaccine adjuvants and drug delivery systems. This product features enhanced stability and bioavailability, meeting stringent EMA quality standards. BASF’s launch reflects growing pharmaceutical interest in biosynthetic squalene as a safer and more sustainable alternative to animal-derived sources. The company highlighted strategic collaborations with biotech firms to further develop next-generation therapeutics incorporating the new squalene grade. This launch is expected to bolster BASF’s market share in the EMEA biosynthetic squalene segment and accelerate adoption in healthcare. Source: BASF Corporate News

- •5th May 2025, Croda International Plc expanded its biosynthetic squalene portfolio by acquiring a French biotechnology start-up specializing in microbial fermentation technologies. This acquisition aims to enhance Croda’s capacity to produce high-purity squalene sustainably and support innovation in clean-label cosmetics. The integration of advanced microbial fermentation platforms is expected to reduce production costs and environmental impact. Croda plans to leverage the acquired technology to strengthen its leadership in the EMEA biosynthetic squalene market, responding to increasing customer demand for ethical and traceable ingredients. Source: Croda Press Announcement

- •10th February 2025, Evonik Industries AG formed a strategic partnership with a leading Middle Eastern pharmaceutical manufacturer to develop biosynthetic squalene-based vaccine adjuvants tailored for regional markets. The collaboration focuses on optimizing formulations that meet local regulatory requirements and supply chain needs. Evonik’s expertise in biosynthetic ingredient production combined with regional manufacturing capabilities aims to expand vaccine accessibility and efficacy in the Middle East and Africa. This partnership demonstrates growing recognition of biosynthetic squalene’s role in advanced healthcare applications and supports the expansion of the biosynthetic squalene market across EMEA. Source: Evonik Corporate Communications

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.95 Billion |

| Forecast Year Market Size | USD 1.82 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Biosynthetic Squalene Type (Plant-Derived Biosynthetic Squalene, Microbial-Derived Biosynthetic Squalene, Synthetic Biosynthetic Squalene, Animal-Derived Biosynthetic Squalene, Others), Application Segment (Cosmetics, Pharmaceuticals, Food & Beverage, Nutraceuticals, Industrial Applications), End-User Industry (Personal Care and Beauty, Healthcare and Pharmaceuticals, Food Processing, Dietary Supplements), Distribution Channel (Direct Sales, Distributors and Wholesalers, Online Retail, Specialty Ingredient Suppliers) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Amyris, Inc. (United Kingdom), BASF SE (Germany), Croda International Plc (United Kingdom), Evonik Industries AG (Germany), Seppic (France), Givaudan SA (Switzerland), Clariant AG (Switzerland), Symrise AG (Germany), Lonza Group AG (Switzerland), Lipoid GmbH (Germany), Indena S.p.A. (Italy), Sophim (France), Evonik Nutrition & Care GmbH (Germany), Sederma (France), Sasol Limited (South Africa), Brenntag AG (Germany), Mibelle Group (Switzerland), Croda France SAS (France), Bio-Botanica, Inc. (Germany), Symrise France SAS (France), Evonik South Africa (South Africa), BASF South Africa (South Africa), L’Oréal Group (France), Univar Solutions (Netherlands), Clariant UK Ltd. (United Kingdom) |

EMEA Biosynthetic Squalene Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.