Global Ultra Thin Flexible Glass UTG For Foldable Phone Market Size, Growth & Revenue 2024-2034

Global Ultra Thin Flexible Glass UTG For Foldable Phone Market is segmented by Application (Smartphones, Tablets, Wearable Devices, Laptops, Other Consumer Electronics), Type (Single Layer UTG, Multi-Layer UTG, Chemically Strengthened UTG, Coated UTG, Others), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Ultra Thin Flexible Glass (UTG) for Foldable Phone Market is focused on ultra-thin glass substrates that enable the flexibility and durability required for foldable display technology. These glasses are engineered to withstand repeated bending and folding while maintaining optical clarity and touch sensitivity, essential for next-generation foldable smartphones and other flexible electronic devices. The market is segmented by type including single layer, multi-layer, chemically strengthened, and coated UTG, each offering distinct benefits such as enhanced toughness or scratch resistance. Key applications span smartphones, tablets, wearables, laptops, and emerging consumer electronics. With rising consumer demand for innovative, compact, and multifunctional devices, the market is expanding rapidly globally, especially across Asia-Pacific and North America. The scope of this market covers raw material sourcing, advanced glass manufacturing processes, chemical strengthening techniques, coating technologies, and integration into electronic devices. This ecosystem involves collaboration between glass producers, smartphone manufacturers, and technology innovators aiming to address challenges of material flexibility and durability for foldable devices.

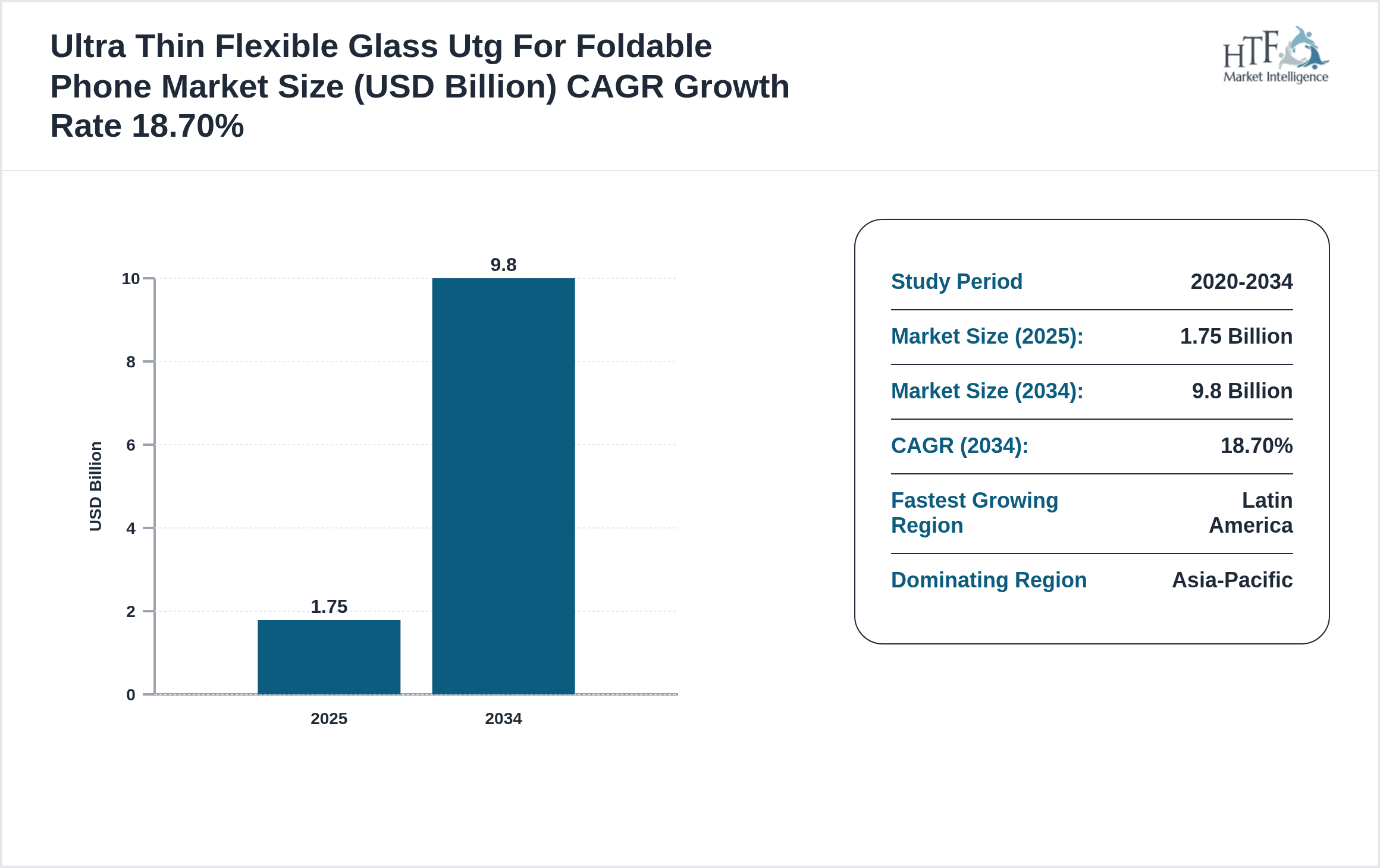

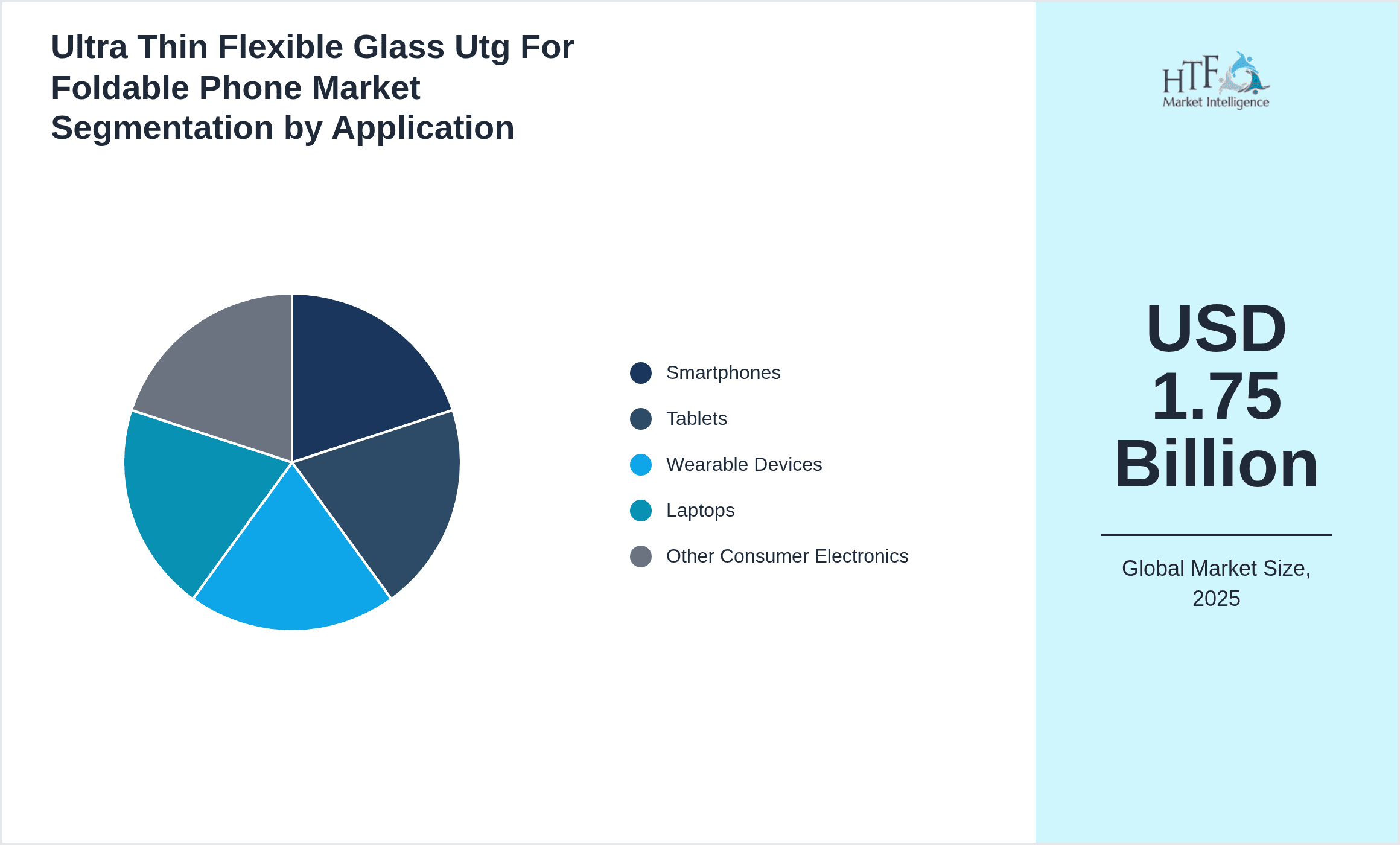

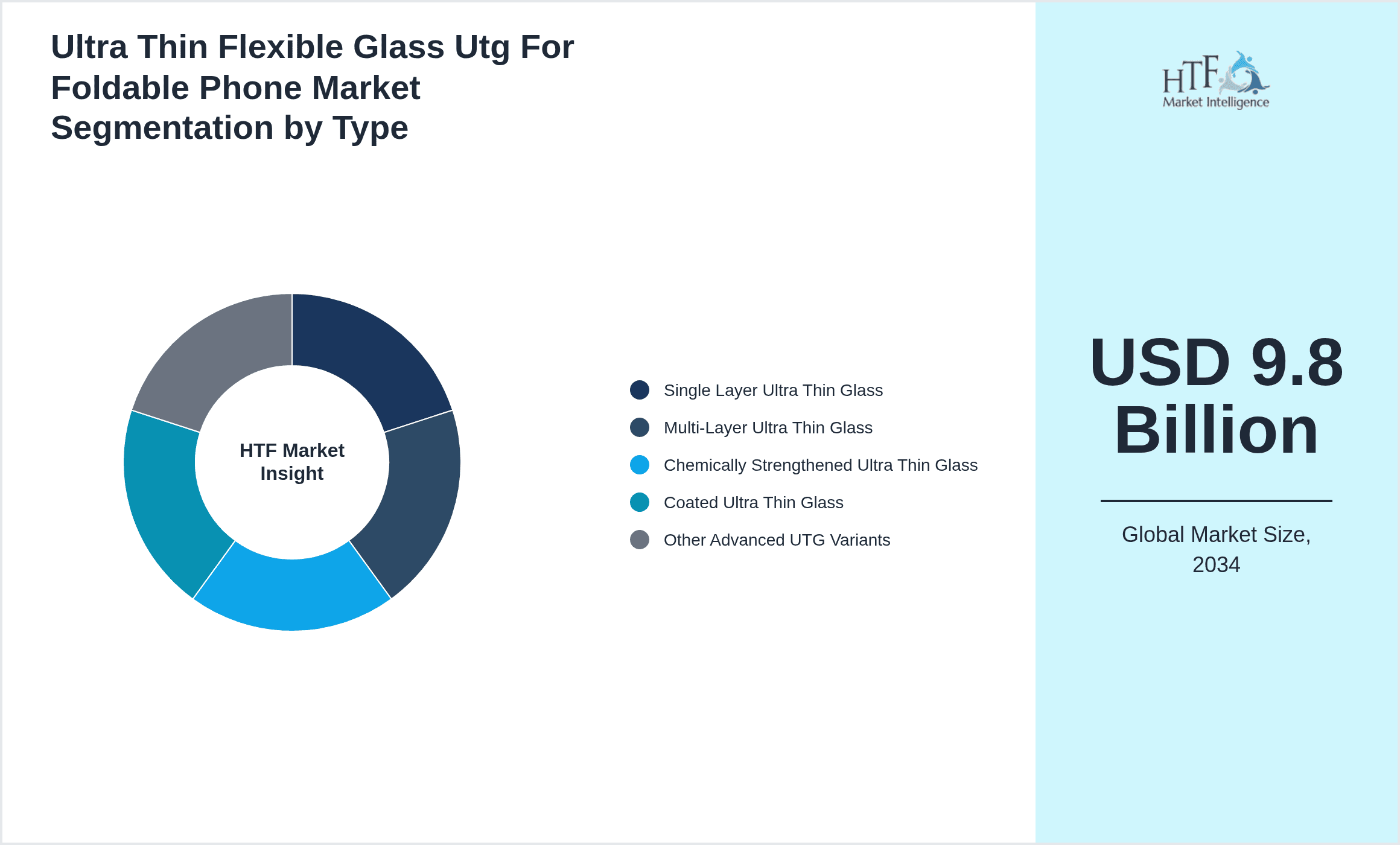

- •Key market highlights include a base market size of USD 1.75 Billion in 2024, projected to reach USD 9.8 Billion by 2034, reflecting a robust compound annual growth rate (CAGR) of 18.7%. Asia-Pacific dominates with a 47.8% market share owing to leading smartphone manufacturers and advanced production facilities. Latin America emerges as the fastest growing region with a CAGR of 23.4%, driven by increasing smartphone penetration and adoption of foldable technology. Chemically Strengthened UTG leads product types due to superior durability, while Coated UTG exhibits fastest growth driven by enhanced scratch and fingerprint resistance. Smartphones remain the dominant application segment, closely followed by tablets and wearable devices, reflecting broadening use cases. Year-over-year growth stands at approximately 18.5%, underscoring a dynamic market environment fueled by technological innovation and consumer demand.

- •The value proposition of this market is centered on enabling the foldable phone revolution, providing manufacturers with materials that combine flexibility with robustness, critical for consumer satisfaction and device longevity. Strategic importance is underscored by the material’s role in miniaturization, device portability, and new form factors, contributing to competitive differentiation in the consumer electronics sector. Stakeholders including glass suppliers, device OEMs, and component integrators benefit from expanding applications, innovation opportunities, and emerging markets. Regulatory compliance and environmental considerations further shape the industry landscape, fostering sustainable manufacturing practices. This market drives technological advancements and economic growth globally, positioning ultra-thin flexible glass as an indispensable enabler for next-generation foldable and flexible devices.

Competitive Landscape

The global ultra thin flexible glass UTG for foldable phone market is characterized by intense competition among several key players focusing on innovation, strategic collaborations, and capacity expansions to secure leadership. Competitors invest heavily in R&D to improve glass flexibility, strength, and scratch resistance while reducing thickness and weight. Market leaders leverage proprietary chemical strengthening and coating technologies to differentiate their offerings and meet stringent device specifications. The competitive environment features frequent technology licensing, joint ventures, and partnerships with smartphone manufacturers to accelerate product adoption. Pricing strategies vary from premium pricing for cutting-edge UTG products to cost-competitive options targeting emerging markets. Distribution channels span direct OEM supply agreements and collaborations with glass component distributors. Regional competition is pronounced, with Asia-Pacific players dominating production and innovation, while North American and European companies focus on advanced materials and specialty glass solutions. Future trends indicate consolidation through mergers and acquisitions, increased focus on eco-friendly production, and expansion into adjacent flexible electronics markets to maintain competitive advantages.

Key Players in Ultra Thin Flexible Glass UTG For Foldable Phone Market

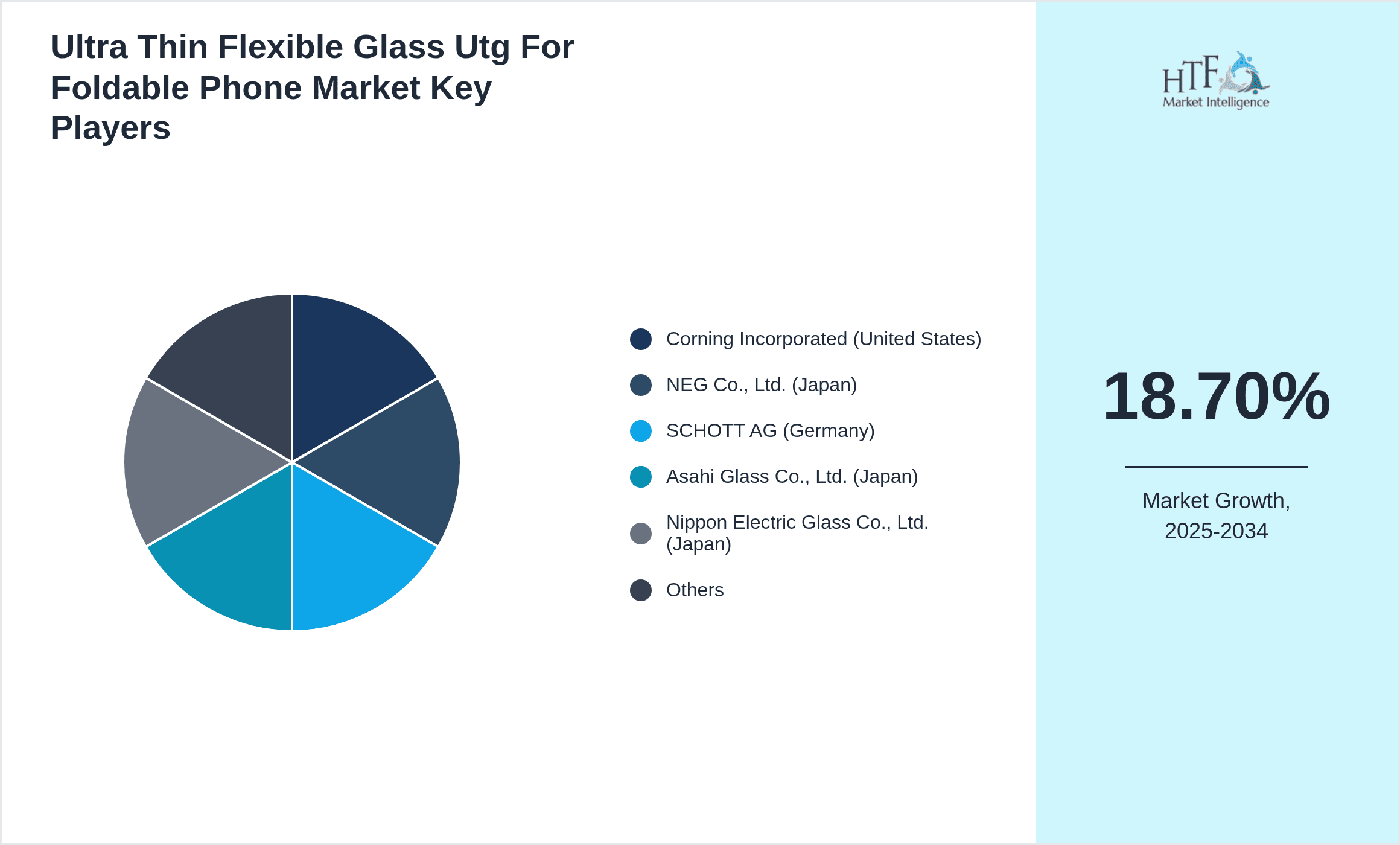

- •Corning Incorporated (United States)

- •NEG Co., Ltd. (Japan)

- •SCHOTT AG (Germany)

- •Asahi Glass Co., Ltd. (Japan)

- •Nippon Electric Glass Co., Ltd. (Japan)

- •NSG Group (Japan)

- •AGC Inc. (Japan)

- •Samsung Corning Precision Materials Co., Ltd. (South Korea)

- •Dow Inc. (United States)

- •Fuyao Glass Industry Group Co., Ltd. (China)

- •Saint-Gobain S.A. (France)

- •Heraeus Holding GmbH (Germany)

- •Guardian Industries (United States)

- •Xinyi Glass Holdings Limited (China)

- •Schott AG (Germany)

- •Laminex Group (Australia)

- •Corning Precision Materials Korea (South Korea)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Tianma Microelectronics Co., Ltd. (China)

- •LG Display Co., Ltd. (South Korea)

- •BOE Technology Group Co., Ltd. (China)

- •Universal Display Corporation (United States)

- •Applied Materials, Inc. (United States)

- •Hoya Corporation (Japan)

- •Kuraray Co., Ltd. (Japan)

Market Breakdown

- •By Type

- ◦Single Layer Ultra Thin Glass

- ◦Multi-Layer Ultra Thin Glass

- ◦Chemically Strengthened Ultra Thin Glass

- ◦Coated Ultra Thin Glass

- ◦Other Advanced UTG Variants

- •By Application

- ◦Smartphones

- ◦Tablets

- ◦Wearable Devices

- ◦Laptops

- ◦Other Consumer Electronics

- •By Manufacturing Technology

- ◦Chemical Strengthening Process

- ◦Ion Exchange Technology

- ◦Coating Technologies

- ◦Laser Cutting & Polishing

- •By Distribution Channel

- ◦Direct OEM Supply

- ◦Component Distributors

- ◦Online B2B Platforms

Growth Dynamics

- •The growing consumer demand for foldable smartphones and flexible electronic devices is a primary growth driver, pushing manufacturers to adopt ultra thin flexible glass to enable innovative product designs and enhanced durability. This demand is accelerating investments in R&D and manufacturing capacity expansions globally.

- •Advancements in chemical strengthening and coating technologies have improved the mechanical properties of UTG, offering better scratch resistance and fold endurance, which supports broader adoption across premium and mid-tier device segments.

- •Strategic collaborations between glass manufacturers and leading smartphone OEMs have streamlined supply chains and enabled faster integration of UTG in foldable devices, enhancing market penetration and reducing time-to-market.

- •Rising awareness about sustainability and eco-friendly manufacturing has driven the development of recyclable and low-energy production processes for UTG, aligning market growth with global environmental regulations and consumer preferences.

- •The increasing use of UTG in applications beyond smartphones, such as tablets, wearables, and ultrathin laptops, presents diversified growth opportunities, expanding the market scope and potential revenue streams for manufacturers.

Market Trends

- •The integration of advanced coatings on UTG to enhance fingerprint resistance and reduce glare is gaining traction, improving user experience and device aesthetics, particularly in premium foldable smartphones.

- •Emerging trend towards hybrid glass-polymer composites is observed, combining the flexibility of polymers with the hardness of glass to achieve superior foldability and impact resistance in foldable displays.

- •Manufacturers are increasingly adopting laser cutting and polishing techniques to produce ultra-thin glass layers with precise dimensions and minimal defects, supporting high yield rates and scalability.

- •The market is witnessing increased investment in Asia-Pacific, driven by robust smartphone manufacturing hubs, creating a competitive advantage in cost and innovation compared to other regions.

- •Sustainability initiatives are influencing material selection and production methods, with companies exploring bio-based coatings and energy-efficient strengthening processes to reduce environmental impact.

Market Opportunities

- •The expansion of foldable technology into mid-range and budget smartphone segments represents a significant opportunity for UTG manufacturers to increase volume and diversify customer base.

- •Development of UTG variants with enhanced flexibility and durability tailored for emerging wearable devices and foldable tablets opens new application avenues and market segments.

- •Strategic partnerships with emerging smartphone brands in Latin America and Middle East & Africa offer access to fast-growing markets with increasing adoption of foldable devices.

- •Innovation in coating technologies that provide anti-reflective, anti-smudge, and antimicrobial properties to UTG can create differentiated product offerings and competitive advantage.

- •Investment in sustainable manufacturing processes and recyclable glass materials could meet rising regulatory demands and consumer expectations, enhancing brand reputation and compliance.

Market Challenges

- •High production costs associated with chemically strengthened and coated ultra thin flexible glass limit accessibility for lower-priced device segments, constraining market penetration.

- •Technical challenges in achieving consistent fold endurance and scratch resistance while maintaining optical clarity require continuous R&D investment and process optimization.

- •Supply chain disruptions and raw material scarcity, exacerbated by geopolitical tensions and global logistics issues, pose risks to stable production and delivery timelines.

- •Competition from alternative flexible display technologies such as plastic substrates and OLED films may limit UTG adoption in certain applications due to cost and design preferences.

- •Stringent regulatory standards and certification requirements across regions increase compliance costs and complexity for manufacturers aiming for global market access.

Regulatory Framework

- •Between 2020 and 2024, key regulations on environmental impact and chemical usage in glass manufacturing were enacted globally, requiring manufacturers to reduce emissions and adopt eco-friendly processes, impacting UTG production methods.

- •Safety standards specific to electronic device components, including durability and chemical resistance testing, have been increasingly mandated by regulatory bodies in North America, Europe, and Asia-Pacific to ensure consumer protection.

- •The European Union’s RoHS and REACH directives have imposed restrictions on hazardous substances used in glass coatings and chemical strengthening agents, compelling manufacturers to reformulate products accordingly.

- •Several countries have introduced incentives and subsidies for manufacturers implementing sustainable and energy-efficient production technologies, fostering innovation in UTG manufacturing.

- •Intellectual property regulations have evolved to protect proprietary glass strengthening and coating technologies, encouraging investments in R&D and collaborative ventures while safeguarding competitive advantages.

Market Intelligence

- •15th January 2025, Corning Incorporated launched its latest ultra-thin flexible glass product designed specifically for foldable smartphones, featuring enhanced scratch resistance and improved fold endurance. The new product utilizes advanced chemical strengthening and coating processes aimed to extend device lifespan and improve consumer experience. This launch aligns with increasing demand for durable foldable displays and strengthens Corning's market position in flexible glass solutions. The product is expected to be adopted by major smartphone OEMs across Asia-Pacific and North America in 2025, facilitating broad market penetration and technological leadership. Source: Corning official press release

- •10th March 2025, NEG Co., Ltd. announced a strategic partnership with a leading foldable smartphone manufacturer to supply chemically strengthened UTG with proprietary anti-fingerprint coatings. This collaboration aims to accelerate the integration of flexible glass in next-generation foldable devices by ensuring superior durability and user experience. NEG’s commitment to innovation includes expanding production capacity and enhancing coating technologies, positioning the company as a key supplier in the growing foldable phone market segment. The partnership underscores the increasing importance of UTG technology in device differentiation and consumer adoption. Source: NEG Co., Ltd. industry news

- •22nd February 2025, AGC Inc. introduced a novel multi-layer UTG designed to offer enhanced flexibility without compromising structural integrity. The innovation targets wearable electronics and foldable tablets, broadening application scope beyond smartphones. AGC’s multi-layer glass leverages cutting-edge ion exchange and lamination techniques, aiming to meet evolving consumer demands for ultra-portable and durable devices. The product launch is supported by pilot production lines in Asia and Europe, signaling the company's drive for global market expansion in flexible glass technologies. Source: AGC corporate announcement

- •5th April 2025, SCHOTT AG expanded its manufacturing facility in Germany to increase output of coated ultra thin flexible glass optimized for foldable devices. The expansion includes investment in environmentally friendly production technologies to meet stringent European regulations and sustainability goals. This move strengthens SCHOTT’s supply capabilities amid growing global demand, particularly in Europe and North America. The company also announced plans to collaborate with smartphone manufacturers for co-development projects aimed at next-generation foldable glass solutions. Source: SCHOTT AG press release

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.75 Billion |

| Forecast Year Market Size | USD 9.8 Billion |

| CAGR | 18.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 18.5% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Corning Incorporated (United States), NEG Co., Ltd. (Japan), SCHOTT AG (Germany), Asahi Glass Co., Ltd. (Japan), Nippon Electric Glass Co., Ltd. (Japan), NSG Group (Japan), AGC Inc. (Japan), Samsung Corning Precision Materials Co., Ltd. (South Korea), Dow Inc. (United States), Fuyao Glass Industry Group Co., Ltd. (China), Saint-Gobain S.A. (France), Heraeus Holding GmbH (Germany), Guardian Industries (United States), Xinyi Glass Holdings Limited (China), Schott AG (Germany), Laminex Group (Australia), Corning Precision Materials Korea (South Korea), Samsung Electronics Co., Ltd. (South Korea), Tianma Microelectronics Co., Ltd. (China), LG Display Co., Ltd. (South Korea), BOE Technology Group Co., Ltd. (China), Universal Display Corporation (United States), Applied Materials, Inc. (United States), Hoya Corporation (Japan), Kuraray Co., Ltd. (Japan) |

Global Ultra Thin Flexible Glass UTG For Foldable Phone Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.