Global Satellite M2M and IoT Network Market - Outlook 2020-2034

Global Satellite M2M and IoT Network Market is segmented by Application (Asset Tracking, Remote Monitoring, Fleet Management, Smart Metering, Emergency Response), Type (Low Earth Orbit Satellites, Medium Earth Orbit Satellites, Geostationary Satellites, Ground Stations, Network Services), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Satellite M2M and IoT Network market is a rapidly evolving sector that integrates advanced satellite communication technologies with Internet of Things applications to enable machine-to-machine data exchange in areas lacking terrestrial connectivity. The market comprises a diverse portfolio of satellite types including Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Earth Orbit (GEO) satellites, complemented by ground infrastructure and network services that facilitate seamless and reliable connectivity. This ecosystem supports critical applications such as asset tracking, fleet management, smart metering, remote environmental monitoring, and emergency response operations, delivering real-time data transmission and enabling enhanced operational efficiencies across multiple industries worldwide. Technological innovations like satellite miniaturization, higher bandwidth capabilities, and integration with terrestrial IoT platforms are propelling market growth. Increasing demand for connected devices in logistics, agriculture, energy, and public safety, alongside supportive regulatory frameworks and significant investments in satellite constellations, are key market drivers. The competitive landscape includes satellite manufacturers, network operators, IoT solution providers, and system integrators focusing on expanding service coverage and improving data analytics capabilities. The market outlook from 2025 to 2034 anticipates robust growth driven by global digital transformation efforts, expanding IoT adoption, and the rising need for ubiquitous connectivity in remote and underserved locations.

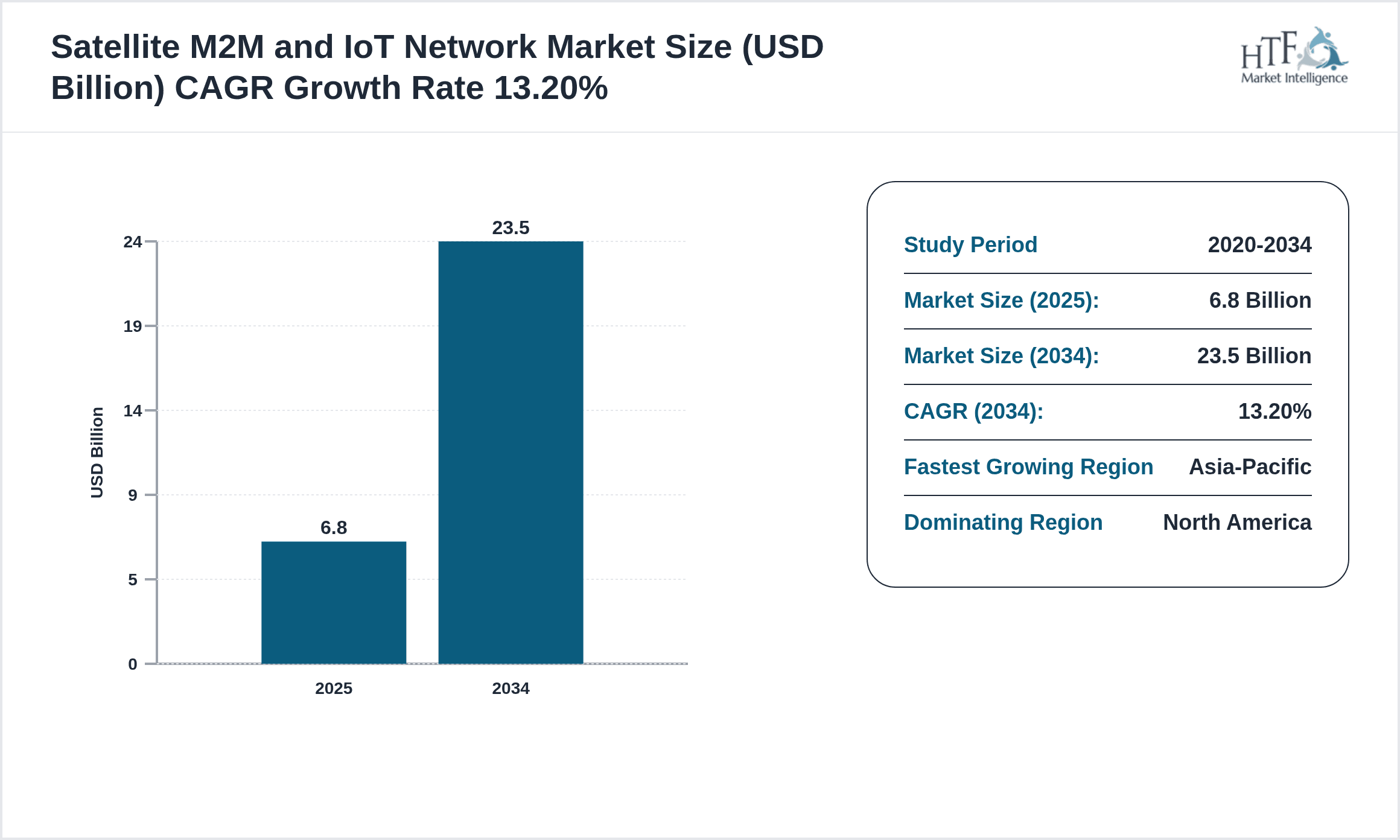

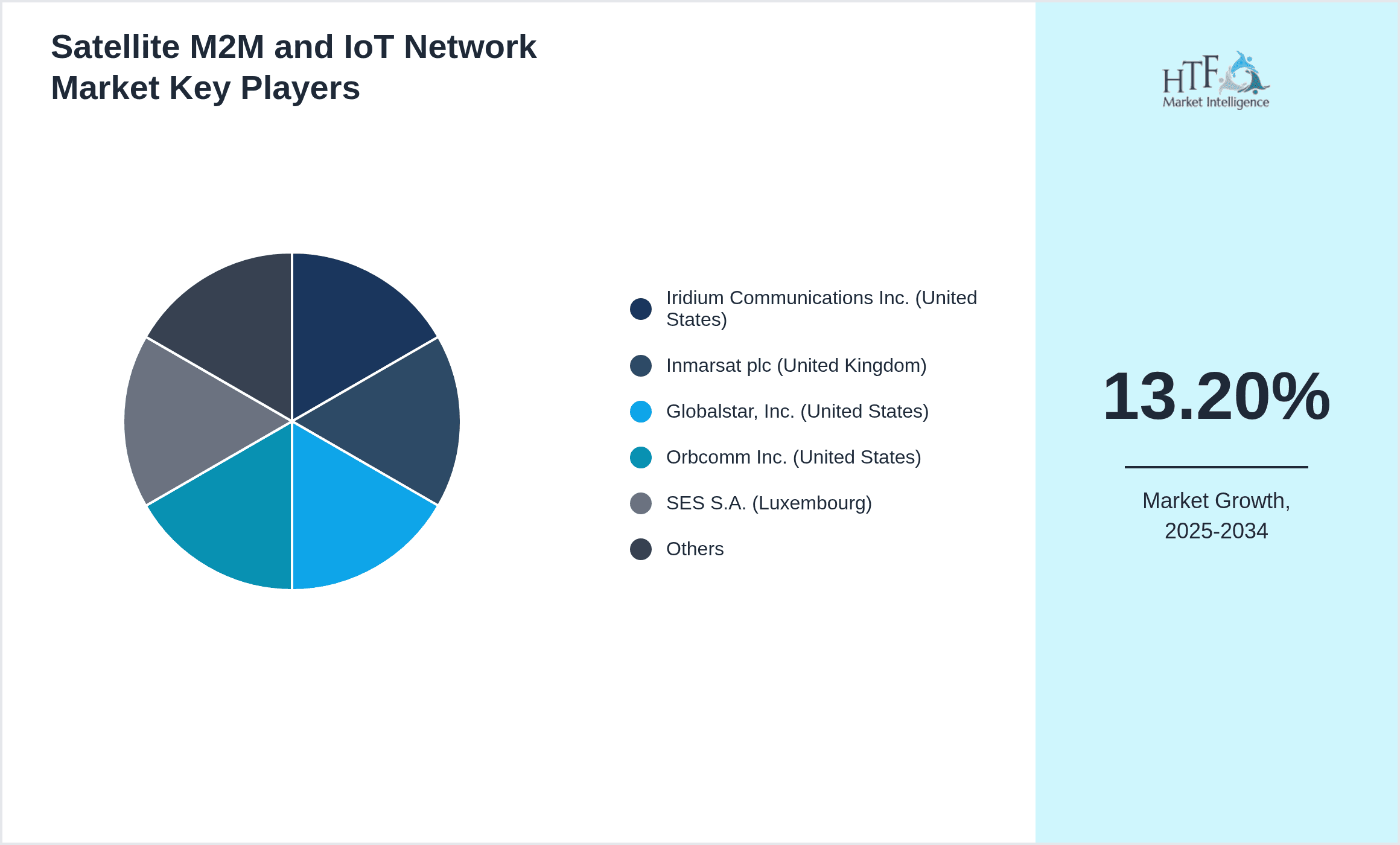

- •Key highlights of the market include a base market size of USD 6.8 Billion in 2025, forecasted to reach USD 23.5 Billion by 2034, reflecting a Compound Annual Growth Rate (CAGR) of 13.2%. The year-on-year growth rate is projected at 12.5%, driven by accelerating deployment of satellite constellations and increasing adoption of satellite IoT services across diverse verticals. North America currently dominates the market with a 35% share, attributed to advanced infrastructure, significant technological innovation, and strong vendor presence. Asia-Pacific is identified as the fastest growing region, expected to achieve a CAGR of 16.1%, fueled by expanding industrial IoT deployments, government initiatives, and growing investments in satellite technology. Low Earth Orbit satellites lead the product segment due to their lower latency and cost advantages, while Medium Earth Orbit satellites represent the fastest growing product category, benefiting from improved coverage and capacity. The market is also characterized by evolving regulatory frameworks, increasing emphasis on cybersecurity, and strategic partnerships among key players to enhance global network reach.

- •The strategic importance of the Global Satellite M2M and IoT Network market lies in its ability to bridge connectivity gaps worldwide, enabling critical industries such as transportation, agriculture, energy, and public safety to leverage IoT capabilities in remote and challenging environments. The market offers significant value propositions including enhanced operational efficiency, real-time data access, improved asset management, and resilience against terrestrial network failures. For stakeholders including satellite operators, IoT solution providers, system integrators, and end-users, the market presents substantial growth opportunities through innovation, service expansion, and integration with emerging technologies such as 5G, AI, and edge computing. The continuous evolution of satellite communication infrastructures combined with increasing demand for connected devices positions this market as a vital enabler of the global digital economy and smart infrastructure development.

Competitive Landscape

The competitive environment of the Global Satellite M2M and IoT Network market is characterized by intense rivalry among established satellite manufacturers, network operators, and emerging IoT solution providers aiming to capture market share through technological innovation and strategic alliances. Key competitive strategies include the development of advanced satellite constellations such as LEO and MEO networks that offer low latency and expanded coverage, integration of IoT platforms with satellite communication capabilities, and diversification of service portfolios to address vertical-specific requirements. Market participants are investing heavily in research and development to enhance satellite technology, improve data transmission speeds, and reduce costs to gain competitive advantage. Strategic partnerships and collaborations with telecom operators, cloud service providers, and IoT ecosystem players are prevalent, enabling comprehensive end-to-end connectivity solutions. Mergers and acquisitions are utilized to consolidate capabilities and expand geographic presence, while pricing strategies focus on balancing affordability with high service quality. The competitive landscape also reflects regional market dynamics, with North America and Europe hosting major players driving innovation, and Asia-Pacific emerging as a vital growth frontier fueled by government initiatives and expanding industrial IoT penetration. Future competition will likely revolve around enhancing network scalability, cybersecurity, and integration with next-generation technologies such as 5G and AI-powered analytics.

Prominent Players in Satellite M2M and IoT Network Market

- •Iridium Communications Inc. (United States)

- •Inmarsat plc (United Kingdom)

- •Globalstar, Inc. (United States)

- •Orbcomm Inc. (United States)

- •SES S.A. (Luxembourg)

- •Thales Group (France)

- •Hughes Network Systems, LLC (United States)

- •L3Harris Technologies, Inc. (United States)

- •Kymeta Corporation (United States)

- •Sky and Space Global Ltd. (Australia)

- •Comtech Telecommunications Corp. (United States)

- •Honeywell International Inc. (United States)

- •Ball Aerospace & Technologies Corp. (United States)

- •Astrocast SA (Switzerland)

- •Swarm Technologies, Inc. (United States)

- •LeoSat Enterprises (United States)

- •OneWeb Satellites (United Kingdom)

- •SES Government Solutions (United States)

- •Telesat Canada (Canada)

- •Rohde & Schwarz GmbH & Co KG (Germany)

- •ViaSat, Inc. (United States)

- •EchoStar Corporation (United States)

- •Redwire Corporation (United States)

- •SatixFy Communications Ltd. (Israel)

- •Kacific Broadband Satellites Group (Singapore)

Market Breakdown

- •By Satellite Type

- ◦Low Earth Orbit (LEO) Satellites

- ◦Medium Earth Orbit (MEO) Satellites

- ◦Geostationary Earth Orbit (GEO) Satellites

- ◦Ground Stations

- ◦Network Services

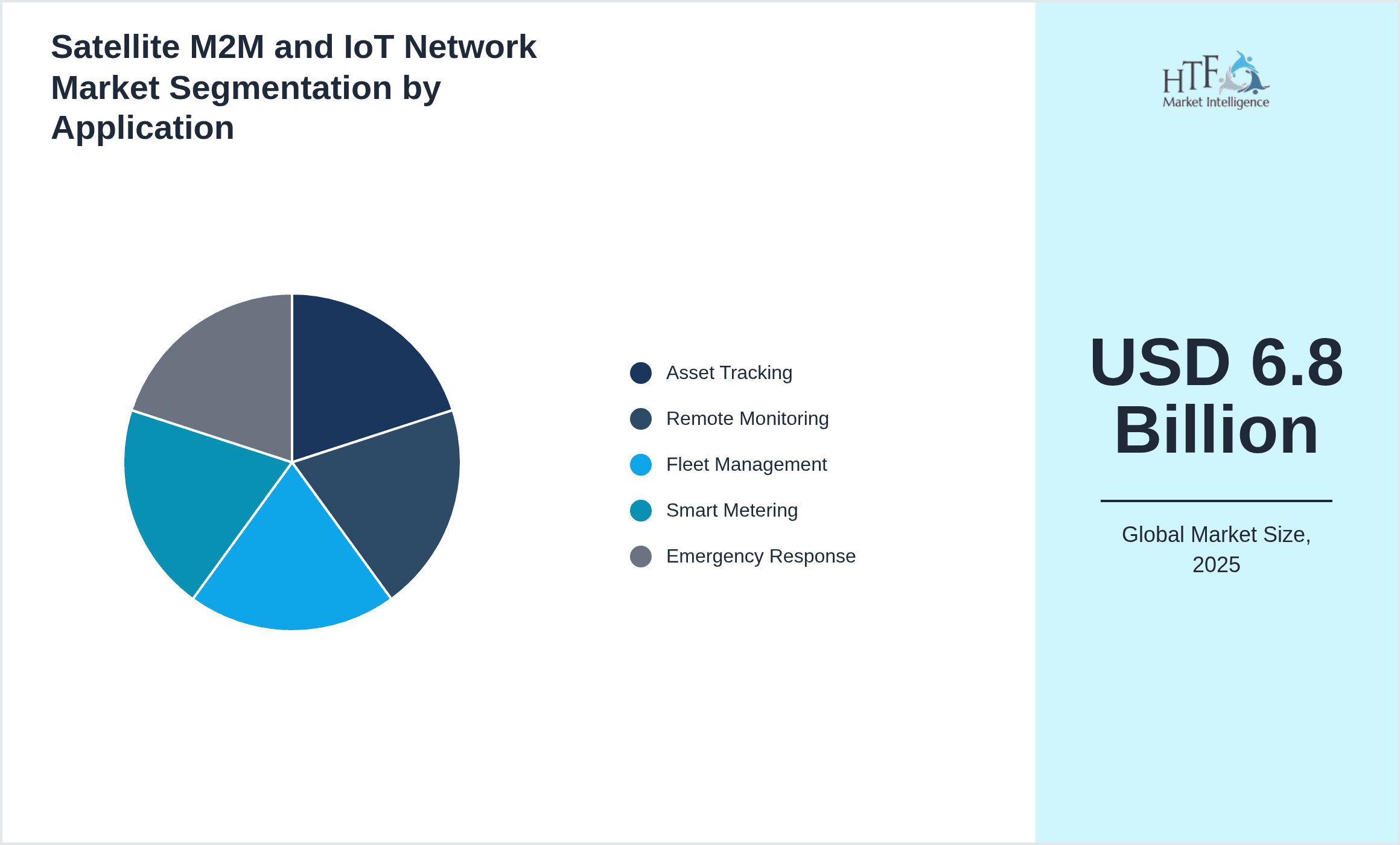

- •By Application

- ◦Asset Tracking

- ◦Remote Monitoring

- ◦Fleet Management

- ◦Smart Metering

- ◦Emergency Response

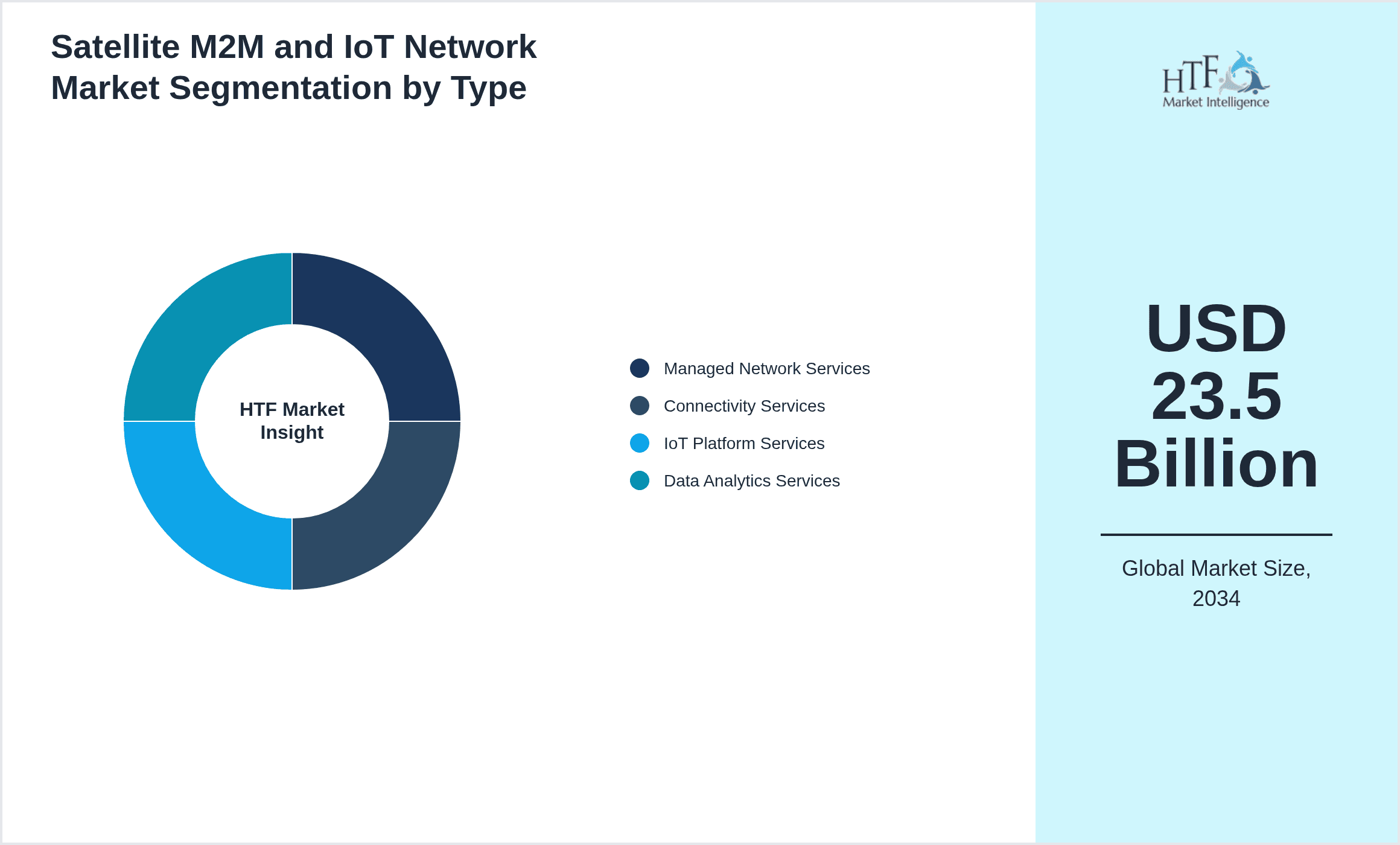

- •By Service Type

- ◦Managed Network Services

- ◦Connectivity Services

- ◦IoT Platform Services

- ◦Data Analytics Services

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

Growth Dynamics

The Global Satellite M2M and IoT Network market is propelled by increasing demand for reliable connectivity in remote and underserved regions, where terrestrial networks fall short. Advancements in satellite technology such as miniaturized Low Earth Orbit satellites enable cost-efficient, low-latency communication, facilitating expanded IoT device deployment across industries including logistics and agriculture. Moreover, the rising adoption of IoT in smart cities and energy management amplifies the necessity for ubiquitous satellite coverage. Strategic government initiatives and spectrum allocation policies further stimulate market growth by encouraging infrastructure investments. The convergence of satellite networks with 5G and cloud computing enhances data transmission capabilities, supporting advanced analytics and real-time decision-making. Increasing industrial automation and digitization drive the need for scalable and secure satellite IoT networks. The integration of AI and edge computing with satellite M2M communications is expected to unlock new use cases and operational efficiencies, while growing partnerships between satellite operators and IoT platform providers strengthen the ecosystem. Investment trends indicate sustained funding in satellite constellations and network expansion, underscoring the market’s robust growth trajectory.

Market Trends

The market is witnessing accelerated deployment of Low Earth Orbit satellite constellations, driven by their advantages in latency and cost, which significantly improve real-time IoT data transmission capabilities globally. Integration of satellite networks with terrestrial 5G infrastructure is emerging as a critical trend, enabling seamless hybrid communication models that optimize coverage and performance. There is an increased focus on developing secure satellite IoT platforms to address growing cybersecurity concerns amid expanding connected devices. Companies are adopting data analytics and AI-driven solutions to enhance network management and predictive maintenance. Additionally, sustainability trends have prompted innovations in satellite design for reduced space debris and energy-efficient operations. Collaborative ecosystem development between satellite operators, cloud service providers, and IoT application developers is fostering new service offerings tailored for industry-specific requirements. These trends collectively underpin the evolving competitive landscape and market expansion.

Market Opportunities

Significant growth opportunities exist in expanding satellite IoT connectivity to emerging markets in Asia-Pacific and Latin America, where terrestrial infrastructure is limited and demand for industrial IoT applications is rising. The development of Medium Earth Orbit satellite constellations presents an untapped potential to balance coverage and capacity, catering to diverse verticals such as maritime, agriculture, and energy management. Innovations in AI-powered IoT analytics integrated with satellite networks offer prospects for enhanced operational efficiency and new service models. Strategic partnerships between satellite operators and cloud providers enable scalable IoT solutions with improved data management and security. Additionally, government incentives and regulatory reforms aimed at promoting smart infrastructure development create fertile ground for market penetration. The growing need for disaster management and emergency response systems utilizing satellite M2M technology further opens avenues for specialized applications. Investment in next-generation satellite technologies and hybrid deployment models also presents lucrative opportunities for market participants.

Market Challenges

The Global Satellite M2M and IoT Network market faces challenges including high initial capital expenditure for satellite constellation deployment and ground infrastructure development, which can limit entry for smaller players. Technical complexities related to spectrum allocation, signal latency, and interference management pose operational hurdles. Regulatory compliance varies across regions, complicating global service standardization and increasing time-to-market. Cybersecurity risks inherent in satellite communication systems demand continuous investment in secure network architectures, increasing operational costs. Integration with terrestrial IoT networks requires interoperability solutions, which are still evolving. Market fragmentation and competition from alternative connectivity technologies such as terrestrial 5G and LPWANs challenge satellite IoT adoption in certain segments. Additionally, space debris and satellite lifespan limitations necessitate sustainable satellite design and end-of-life management strategies, adding to industry costs and regulatory scrutiny.

Regulatory Framework

Between 2020 and 2025, significant regulatory developments shaped the satellite M2M and IoT network market landscape, particularly in spectrum management and space traffic coordination. The International Telecommunication Union (ITU) updated regulations for frequency allocation to accommodate burgeoning satellite constellations, emphasizing interference mitigation and equitable spectrum access. National agencies introduced stricter guidelines for satellite licensing and operational compliance, impacting deployment timelines and costs. Data privacy and cybersecurity regulations intensified, compelling market players to adopt robust security frameworks to protect IoT data transmitted via satellite networks. Environmental regulations addressing space debris management gained prominence, with mandates requiring end-of-life satellite disposal plans to minimize orbital congestion. The European Union implemented regulations harmonizing satellite IoT standards across member states, promoting interoperability and market integration. In the United States, the Federal Communications Commission (FCC) accelerated approval processes for innovative satellite technologies while enforcing compliance with safety standards. Collectively, these regulations have fostered a more secure, sustainable, and competitive global satellite IoT ecosystem.

Market Intelligence

- •15th January 2025, Iridium Communications Inc. successfully launched its next-generation LEO satellite constellation upgrade, enhancing global IoT network capacity and reducing latency for critical M2M applications. The new satellites incorporate advanced phased-array antennas and AI-powered network management, enabling more efficient spectrum utilization and improved service reliability. This launch positions Iridium to meet the growing demand for satellite IoT connectivity in remote and industrial sectors, reinforcing its competitive edge. The technology upgrade supports expanded coverage for asset tracking, fleet management, and emergency response applications worldwide. Strategic partnerships with IoT platform providers are planned to leverage these enhancements for new service offerings. Source: Iridium Communications Official Press Release

- •22nd March 2025, SES S.A. announced a strategic collaboration with a leading cloud service provider to develop integrated satellite IoT solutions combining high-throughput satellite connectivity with scalable cloud-based data analytics. The partnership aims to deliver end-to-end managed IoT services for industries including agriculture, energy, and logistics, addressing the need for real-time insights and operational agility. SES will provide enhanced MEO satellite capacity while the cloud partner offers advanced AI-driven data processing capabilities. This initiative is expected to accelerate market adoption of satellite IoT networks by simplifying deployment and reducing total cost of ownership for end-users. Source: SES Official Corporate Statement

- •10th May 2024, OneWeb Satellites completed a successful contract to manufacture and deploy 30 additional LEO satellites, expanding its constellation to support growing IoT and broadband service demand across underserved regions in Asia-Pacific and Latin America. The satellites feature improved power efficiency and higher throughput capabilities, enabling more reliable and cost-effective IoT network coverage. This expansion supports OneWeb’s strategic objective to bridge the digital divide and capitalize on emerging market opportunities. The company also announced ongoing R&D efforts to integrate next-generation IoT protocols and enhance network security. Source: OneWeb Satellites Press Release

- •7th February 2025, Kymeta Corporation introduced its latest flat-panel electronically steered antenna technology designed for seamless satellite M2M and IoT connectivity on moving platforms such as vehicles and maritime vessels. The new antenna offers improved signal stability, reduced size, and higher data throughput, enabling continuous connectivity in challenging environments. This innovation addresses critical market needs in fleet management, logistics, and emergency services, where reliable satellite IoT links are essential. Kymeta’s solution integrates with multiple satellite constellations, providing flexible deployment options. Market analysts anticipate this development will drive increased adoption of satellite IoT services in transportation sectors globally. Source: Kymeta Corporation Product Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 6.8 Billion |

| Forecast Year Market Size | USD 23.5 Billion |

| CAGR | 13.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.5% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Iridium Communications Inc. (United States), Inmarsat plc (United Kingdom), Globalstar, Inc. (United States), Orbcomm Inc. (United States), SES S.A. (Luxembourg), Thales Group (France), Hughes Network Systems, LLC (United States), L3Harris Technologies, Inc. (United States), Kymeta Corporation (United States), Sky and Space Global Ltd. (Australia), Comtech Telecommunications Corp. (United States), Honeywell International Inc. (United States), Ball Aerospace & Technologies Corp. (United States), Astrocast SA (Switzerland), Swarm Technologies, Inc. (United States), LeoSat Enterprises (United States), OneWeb Satellites (United Kingdom), SES Government Solutions (United States), Telesat Canada (Canada), Rohde & Schwarz GmbH & Co KG (Germany), ViaSat, Inc. (United States), EchoStar Corporation (United States), Redwire Corporation (United States), SatixFy Communications Ltd. (Israel), Kacific Broadband Satellites Group (Singapore) |

Global Satellite M2M and IoT Network Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.