Europe Aluminum Alloy Precision Die Casting for Wiper Motor Market - Europe Size & Outlook 2024-2034

Europe Aluminum Alloy Precision Die Casting for Wiper Motor Market is segmented by Aluminum Alloy Type (Aluminum-Silicon Alloy, Aluminum-Copper Alloy, Aluminum-Magnesium Alloy, Aluminum-Zinc Alloy, Aluminum-Manganese Alloy), Application Segment (Automotive Wiper Motors, Industrial Equipment, Agricultural Machinery, Construction Vehicles, Marine Applications), End-Use Industry (Passenger Vehicles, Commercial Vehicles, Agriculture Sector, Construction Sector, Marine Industry), Manufacturing Technology (High-Pressure Die Casting, Low-Pressure Die Casting, Gravity Die Casting), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Aluminum Alloy Precision Die Casting for Wiper Motor market is a specialized segment focused on the production of high-precision aluminum alloy components used in wiper motors across various industries including automotive, agricultural, construction, and marine sectors. Precision die casting offers advanced manufacturing capabilities that ensure durability, lightweight structures, and corrosion resistance, essential for the efficient operation of wiper motors in demanding environments. The market covers multiple aluminum alloy types such as aluminum-silicon, aluminum-copper, aluminum-magnesium, aluminum-zinc, and aluminum-manganese alloys, each offering distinct mechanical and chemical properties tailored for specific applications. Demand is primarily driven by the automotive sector’s emphasis on safety and performance, alongside industrial machinery needs. Regionally, this market is concentrated in key European countries including Germany, France, the United Kingdom, Italy, and Spain, supported by strong manufacturing infrastructure and technological advancements. The market is expected to witness steady growth owing to innovations in die casting technology, stringent emission regulations leading to lightweight component requirements, and increased adoption of automated manufacturing processes.

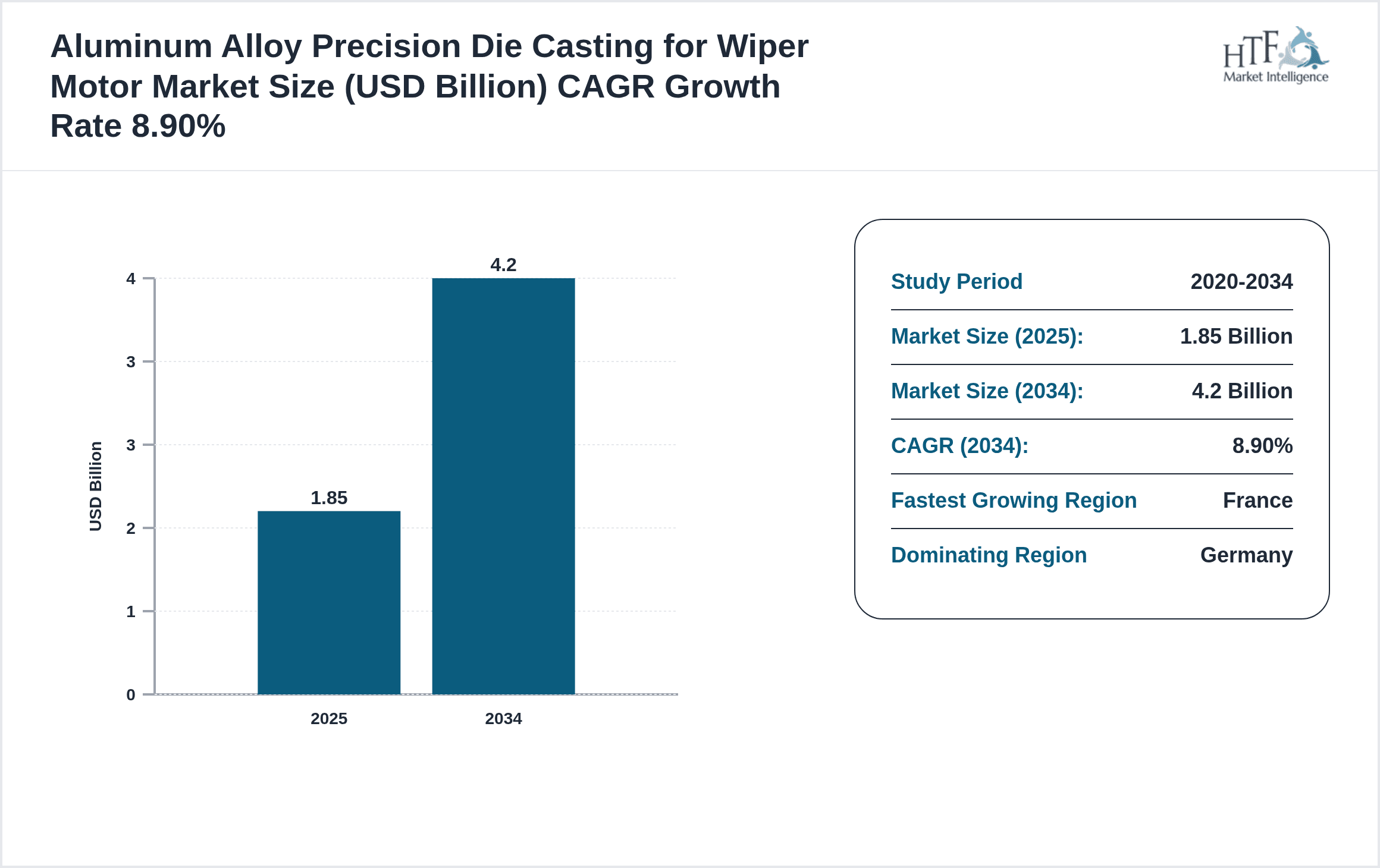

- •Key market highlights indicate a base market size of USD 1.85 Billion in 2024, projected to reach USD 4.20 Billion by 2034, representing a CAGR of approximately 8.9%. Germany dominates the market with a 32% share, followed by France at 18%, which is also the fastest growing country at a CAGR of 11.2%. Aluminum-silicon alloy remains the leading product type due to its excellent casting properties and corrosion resistance, while aluminum-magnesium alloy shows the fastest growth driven by demand for lightweight components. Automotive wiper motors are the predominant application segment, reflecting the automotive industry's central role in market expansion. Growth is further supported by technological advancements in precision die casting processes and increasing integration of wiper motors in diverse vehicle types, including electric and autonomous vehicles.

- •The market holds strategic importance for automotive OEMs, die casting manufacturers, and component suppliers as it directly impacts vehicle reliability, safety, and efficiency. Lightweight aluminum alloy components contribute significantly to reducing vehicle weight, thereby improving fuel efficiency and lowering emissions in compliance with European environmental regulations. Additionally, the market's evolution is critical for industrial equipment manufacturers seeking durable and precise motor components. Stakeholders benefit from continuous innovation in alloy compositions and casting technologies, enabling enhanced product performance and expanded application potential. The competitive landscape is characterized by technological expertise, capacity expansion, and strategic partnerships, which collectively drive market growth and value creation across the European industrial ecosystem.

Competitive Landscape

The Europe Aluminum Alloy Precision Die Casting for Wiper Motor market exhibits a competitive environment shaped by several key players leveraging technological innovation, strategic collaborations, and capacity expansions to maintain market share. Companies compete primarily on product quality, precision casting capabilities, alloy innovations, and adherence to stringent environmental standards. The rivalry is intensified by the increasing demand for lightweight and high-performance components driven by automotive and industrial applications. Innovation approaches focus on developing alloys with improved corrosion resistance and mechanical strength while optimizing casting processes for efficiency and sustainability. Strategic partnerships and joint ventures enable players to expand geographic reach and integrate advanced manufacturing technologies, fostering a dynamic landscape. Market entry barriers include the capital-intensive nature of precision die casting facilities and the necessity for specialized technical expertise. Future competition is expected to hinge on digitalization, automation, and sustainable manufacturing practices, with companies investing heavily in R&D to differentiate their offerings and capture emerging opportunities in electric and autonomous vehicle sectors.

Leading Companies in Aluminum Alloy Precision Die Casting for Wiper Motor Market

- •Nemak Europe GmbH (Germany)

- •GEDIA Automotive Group (Germany)

- •Alcoa Corporation (United States)

- •Rheinmetall Automotive AG (Germany)

- •Bühler AG (Switzerland)

- •THB Group (France)

- •Menzel GmbH (Germany)

- •Fonderie Rénovée (France)

- •Kostal Group (Germany)

- •Cast Metal Group (United Kingdom)

- •Leroy-Somer (France)

- •SLM Solutions (Germany)

- •GF Casting Solutions (Switzerland)

- •KSM Castings Group (United Kingdom)

- •Die Casting Company Europe (Germany)

- •BSC Die Casting (Netherlands)

- •Eckold GmbH (Germany)

- •Erbstück GmbH (Austria)

- •Metallum Grupa (Poland)

- •Aluminium Rheinfelden GmbH (Germany)

- •Alu-Die Casting Ltd (United Kingdom)

- •SAPA Group (Norway)

- •AluKönigStahl GmbH (Germany)

- •Magna International (Canada)

- •Constellium SE (Netherlands)

Market Breakdown

- •By Aluminum Alloy Type

- ◦Aluminum-Silicon Alloy

- ◦Aluminum-Copper Alloy

- ◦Aluminum-Magnesium Alloy

- ◦Aluminum-Zinc Alloy

- ◦Aluminum-Manganese Alloy

- •By Application Segment

- ◦Automotive Wiper Motors

- ◦Industrial Equipment

- ◦Agricultural Machinery

- ◦Construction Vehicles

- ◦Marine Applications

- •By End-Use Industry

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Agriculture Sector

- ◦Construction Sector

- ◦Marine Industry

- •By Manufacturing Technology

- ◦High-Pressure Die Casting

- ◦Low-Pressure Die Casting

- ◦Gravity Die Casting

Growth Dynamics

- •Increasing demand for lightweight and corrosion-resistant components in the automotive sector drives growth, as aluminum alloys reduce vehicle weight and improve fuel efficiency, directly impacting emission targets compliance.

- •Technological advancements in precision die casting, including automation and computer-controlled processes, enhance product quality and manufacturing efficiency, encouraging wider adoption across industries.

- •Expansion of electric and autonomous vehicle production in Europe fuels demand for precision die-cast wiper motor components, emphasizing high-performance and reliable materials.

- •Stricter environmental regulations in Europe push manufacturers to adopt sustainable materials and processes, benefiting the aluminum alloy precision die casting market due to its recyclability and energy efficiency.

- •Growing industrialization and mechanization in sectors like agriculture and construction increase demand for durable and precise wiper motor components, expanding application scope.

Market Trends

- •Adoption of advanced alloys such as aluminum-magnesium is rising due to their superior strength-to-weight ratio and corrosion resistance, aligning with automotive manufacturers’ lightweighting goals.

- •Integration of Industry 4.0 technologies in die casting operations is improving process monitoring, quality control, and production flexibility, enabling faster response to market demands.

- •Increasing use of recycled aluminum in die casting reduces environmental footprint and raw material costs, supporting circular economy initiatives in Europe.

- •Collaborations between component manufacturers and automotive OEMs are fostering innovation in alloy formulations and casting techniques tailored to electric and autonomous vehicle requirements.

- •Growing preference for modular wiper motor designs facilitates easier integration and maintenance, driving demand for precision die-cast components matching complex geometries.

Market Opportunities

- •Rising penetration of electric vehicles in Europe presents significant opportunities for aluminum alloy precision die casting suppliers to develop lightweight, high-performance motor components.

- •Expansion into emerging application areas such as marine and agricultural machinery can diversify market presence and revenue streams for die casting manufacturers.

- •Investment in R&D for novel aluminum alloys with enhanced thermal and mechanical properties can create competitive advantages and open new market segments.

- •Strategic partnerships with automotive OEMs and industrial equipment manufacturers enable co-development of customized casting solutions, fostering long-term contracts and market stability.

- •Increasing government incentives in Europe for sustainable manufacturing and lightweight material adoption support capital investments in advanced die casting technologies.

Market Challenges

- •High initial capital expenditure and maintenance costs for precision die casting equipment limit entry for smaller manufacturers, impacting market fragmentation.

- •Complex alloy formulations require specialized knowledge and quality control, posing challenges in maintaining consistent product performance and meeting stringent automotive standards.

- •Supply chain disruptions, especially for raw aluminum and alloying elements, can cause cost volatility and production delays affecting market reliability.

- •Increasing competition from alternative materials such as composites and plastics offering cost or weight advantages could constrain aluminum alloy die casting demand in certain applications.

- •Compliance with evolving environmental and safety regulations requires continuous adaptation in manufacturing processes, adding operational complexity and cost.

Regulatory Framework

- •Between 2019 and 2024, the European Union introduced stricter vehicle emission standards under Euro 6d regulations, indirectly promoting lightweight aluminum alloy components to improve fuel efficiency and reduce CO2 emissions.

- •The REACH regulation updates during this period mandated rigorous chemical safety assessments for alloys and coatings used in die casting, ensuring safer materials and compliance with environmental standards.

- •New European directives on waste management and recycling targets encourage manufacturers to adopt sustainable production practices and use recycled aluminum in die casting operations.

- •Country-specific mandates in Germany and France require automotive suppliers to implement energy-efficient manufacturing processes, influencing the adoption of modern die casting technologies.

- •Government incentive programs across Europe support investments in advanced manufacturing and lightweight materials, facilitating market growth through financial and technical assistance.

Market Intelligence

- •15th February 2025, Nemak Europe GmbH launched a new range of high-strength aluminum-silicon alloy components specifically designed for next-generation electric vehicle wiper motors. This product line features enhanced corrosion resistance and optimized weight reduction, aligning with stringent European emission regulations and OEM demands for sustainable mobility solutions. The launch underscores Nemak’s commitment to innovation and leadership in precision die casting technology in Europe, aiming to capture growing EV market share.

- •10th March 2025, Bühler AG announced the expansion of its precision die casting facility in Switzerland, incorporating advanced Industry 4.0 automation and AI-driven quality control systems. This strategic investment enhances production capacity and efficiency, enabling faster turnaround and customization capabilities for automotive and industrial clients across Europe. The upgrade supports Bühler’s vision to lead in sustainable manufacturing practices and high-performance aluminum alloy components.

- •22nd January 2025, GEDIA Automotive Group entered a strategic partnership with a major European electric vehicle manufacturer to co-develop lightweight aluminum-magnesium alloy die-cast wiper motor components. This collaboration focuses on delivering improved mechanical strength and thermal stability tailored to electric vehicle operating conditions, aiming to accelerate market penetration and meet evolving consumer expectations.

- •5th April 2025, Constellium SE unveiled an innovative recycling process that increases the yield and purity of recycled aluminum alloys used in precision die casting. This development supports the European circular economy goals and offers cost advantages to manufacturers by reducing reliance on primary aluminum. Constellium’s initiative is positioned to influence supply chain sustainability and material performance in the aluminum alloy precision die casting sector.

- •Source: Official company press releases, Industry publications

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 4.2 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.54% |

| Scope of Report | Market is segmented by Aluminum Alloy Type (Aluminum-Silicon Alloy, Aluminum-Copper Alloy, Aluminum-Magnesium Alloy, Aluminum-Zinc Alloy, Aluminum-Manganese Alloy), Application Segment (Automotive Wiper Motors, Industrial Equipment, Agricultural Machinery, Construction Vehicles, Marine Applications), End-Use Industry (Passenger Vehicles, Commercial Vehicles, Agriculture Sector, Construction Sector, Marine Industry), Manufacturing Technology (High-Pressure Die Casting, Low-Pressure Die Casting, Gravity Die Casting) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Nemak Europe GmbH (Germany), GEDIA Automotive Group (Germany), Alcoa Corporation (United States), Rheinmetall Automotive AG (Germany), Bühler AG (Switzerland), THB Group (France), Menzel GmbH (Germany), Fonderie Rénovée (France), Kostal Group (Germany), Cast Metal Group (United Kingdom), Leroy-Somer (France), SLM Solutions (Germany), GF Casting Solutions (Switzerland), KSM Castings Group (United Kingdom), Die Casting Company Europe (Germany), BSC Die Casting (Netherlands), Eckold GmbH (Germany), Erbstück GmbH (Austria), Metallum Grupa (Poland), Aluminium Rheinfelden GmbH (Germany), Alu-Die Casting Ltd (United Kingdom), SAPA Group (Norway), AluKönigStahl GmbH (Germany), Magna International (Canada), Constellium SE (Netherlands) |

Europe Aluminum Alloy Precision Die Casting for Wiper Motor Market - Europe Size & Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.