United States High Strength Bolts for Steel Structures Market Roadmap to 2034

United States High Strength Bolts for Steel Structures Market is segmented by Bolt Type (Grade 8.8 High Strength Bolts, Grade 10.9 High Strength Bolts, Grade 12.9 High Strength Bolts, ASTM A325 Structural Bolts, ASTM A490 Structural Bolts), End-Use Application (Bridges, Commercial Buildings, Industrial Facilities, Residential Construction, Infrastructure Projects), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail, Specialized Construction Suppliers), Regional Zone within United States (Northeast, Southeast, Midwest, Southwest, West Coast), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

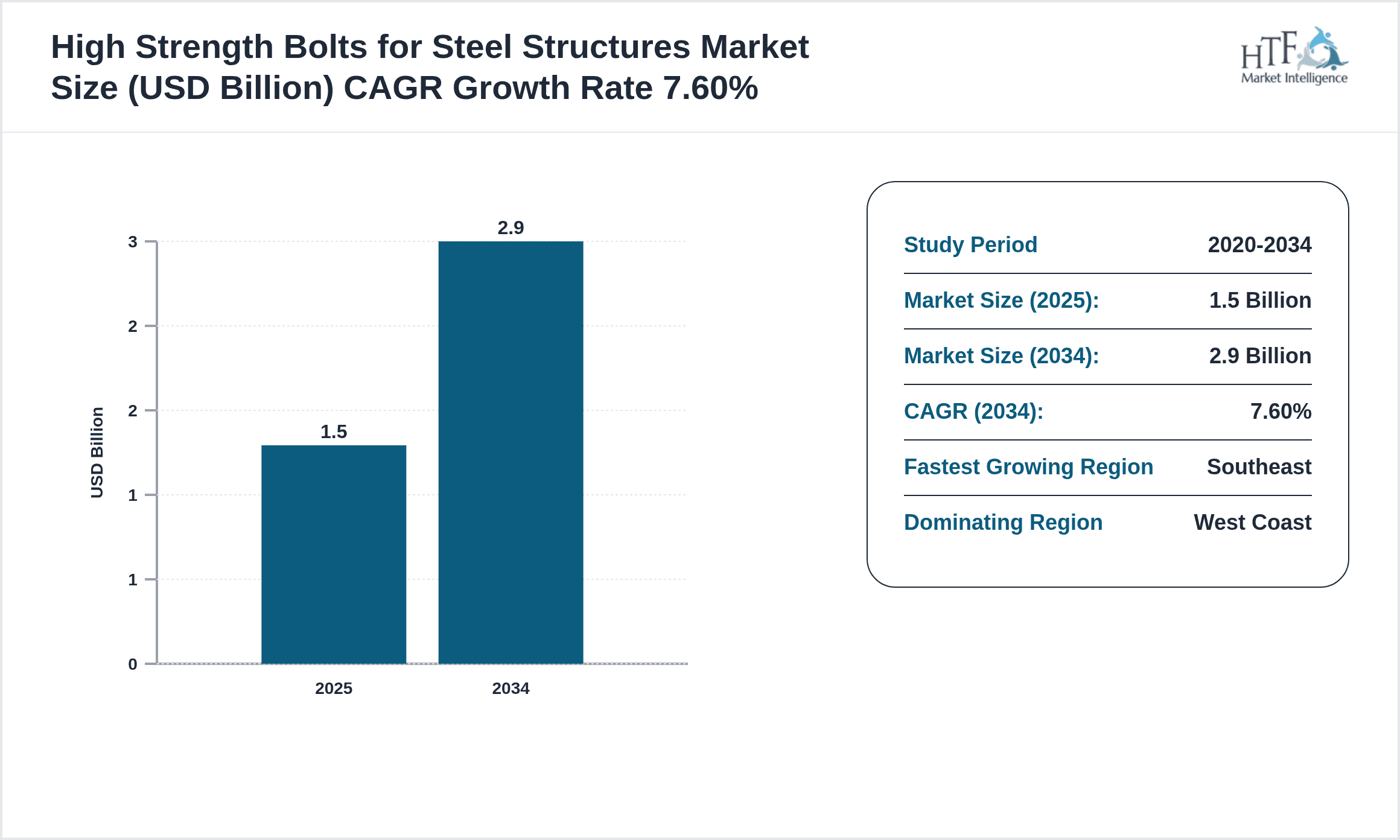

- •The United States High Strength Bolts for Steel Structures Market plays a pivotal role in ensuring the structural integrity and durability of steel frameworks across diverse construction sectors. This market involves the production and deployment of bolts engineered to meet stringent strength requirements, suited for applications ranging from bridges and commercial buildings to residential projects and large-scale industrial facilities. The industry scope includes multiple bolt grades and standards, such as Grade 8.8, Grade 10.9, Grade 12.9, ASTM A325, and ASTM A490, each offering specific mechanical properties to address varying load and environmental conditions. The market is influenced by evolving construction codes, increasing infrastructure spending, and technological advancements in material science that enhance bolt performance and longevity. Furthermore, regional demand within the United States varies, with the West Coast dominating due to extensive infrastructure development, while the Southeast region exhibits the fastest growth driven by rapid urbanization and industrial expansion. The market’s trajectory is shaped by factors such as regulatory compliance, competitive innovation, and the strategic focus of key industry players to address the growing demand for durable, high-performance fastening solutions.

- •Key highlights of the market include a base market size of USD 1.5 Billion in 2025, forecasted to nearly double to USD 2.9 Billion by 2034, reflecting a robust CAGR of 7.6%. The Grade 10.9 bolt type currently leads the market share, favored for its balanced strength and cost-efficiency, while ASTM A490 bolts are gaining increased adoption due to their superior tensile strength for critical applications. Applications in commercial buildings and bridges dominate demand segments, with infrastructure projects growing rapidly. Regionally, the West Coast commands the largest market share at 30%, supported by continuous investment in seismic-resistant infrastructure, whereas the Southeast region is the fastest growing with a CAGR of 9.3%, propelled by expanding industrial and residential construction activities.

- •This market offers significant value propositions for construction firms, engineering consultants, and bolt manufacturers by providing high-quality fastening solutions that enhance safety, reduce maintenance costs, and improve construction efficiency. The strategic importance of high strength bolts is underscored by their critical role in load-bearing steel assemblies, ensuring compliance with building codes and industry standards. Stakeholders benefit from continuous product innovation, supply chain optimization, and regulatory adherence that collectively drive market expansion. The market is also poised for growth through opportunities in retrofit projects, adoption of advanced coating technologies to combat corrosion, and integration of smart inspection systems that monitor bolt performance in real-time, thereby enhancing lifecycle management of steel structures.

Competitive Landscape

The competitive environment of the United States High Strength Bolts for Steel Structures Market is characterized by a mix of established multinational corporations and specialized regional manufacturers vying for market share through product innovation, quality assurance, and strategic partnerships. Companies focus on developing advanced bolt grades and coatings to meet evolving construction demands and regulatory standards, establishing differentiation through enhanced mechanical properties and corrosion resistance. Market rivalry is intense, with firms investing in research and development to pioneer high-performance fasteners that offer improved installation efficiency and longevity. Strategic collaborations between bolt manufacturers and construction contractors facilitate tailored solutions for complex structural projects, enhancing customer value propositions. Pricing strategies balance cost competitiveness with premium quality offerings to attract diverse end-users, including infrastructure developers and industrial construction firms. The adoption of digital technologies in supply chain management and quality testing further strengthens competitive positioning. Barriers to entry are significant due to stringent certification requirements and capital-intensive manufacturing processes, which consolidate market power among leading players. Regional competition also manifests in localized product customization and service responsiveness, shaping future competitive trends toward integrated solutions and sustainability.

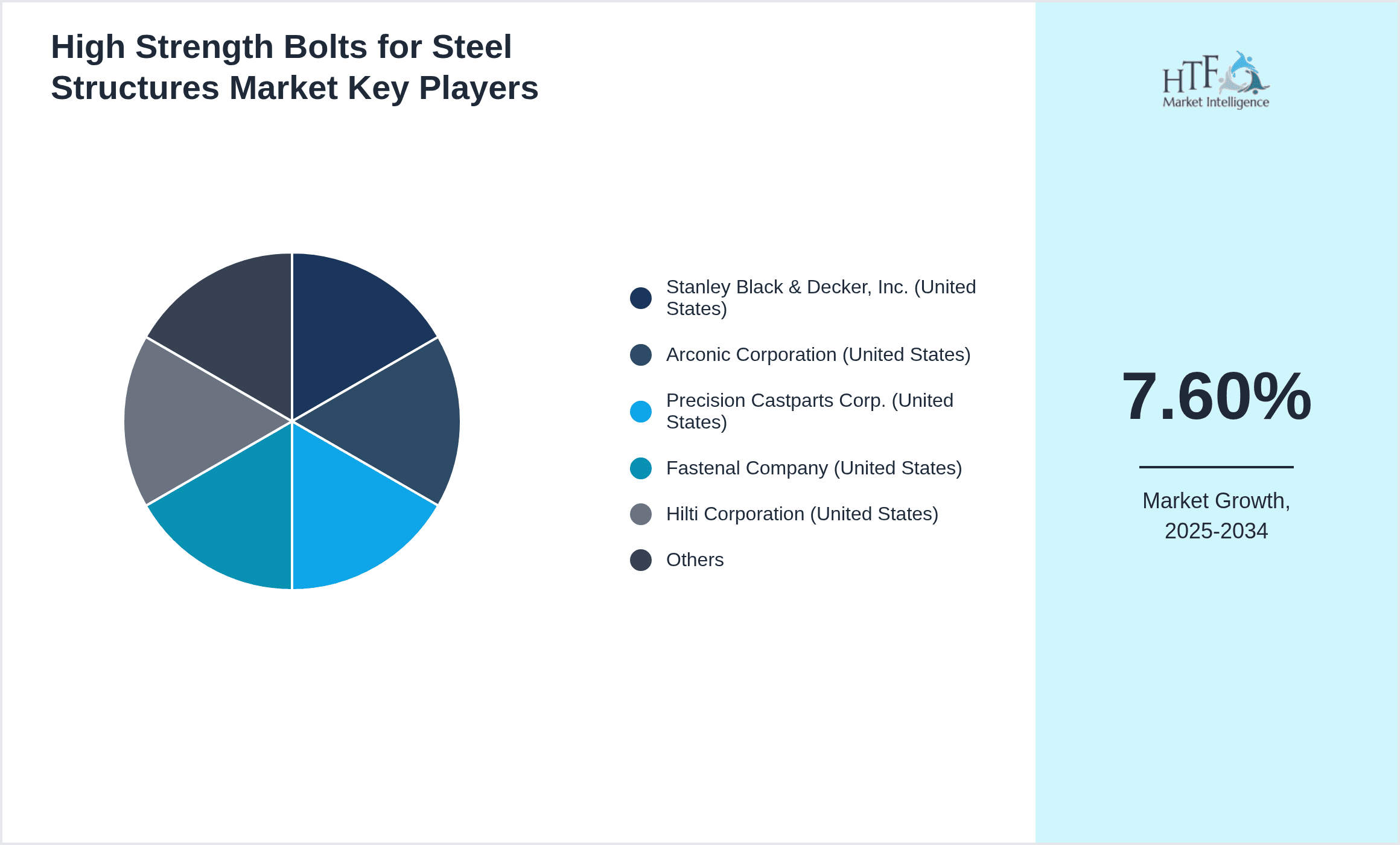

Leading Companies in High Strength Bolts for Steel Structures Market

- •Stanley Black & Decker, Inc. (United States)

- •Arconic Corporation (United States)

- •Precision Castparts Corp. (United States)

- •Fastenal Company (United States)

- •Hilti Corporation (United States)

- •Würth Group (Germany)

- •SFS Group AG (Switzerland)

- •LISI Group (France)

- •Nucor Corporation (United States)

- •ITW (Illinois Tool Works Inc.) (United States)

- •Bulten AB (Sweden)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Bossard Group (Switzerland)

- •Prysmian Group (Italy)

- •Anixter International Inc. (United States)

- •Hilti AG (Liechtenstein)

- •KVT-Fastening GmbH (Germany)

- •Rexnord Corporation (United States)

- •Pentair plc (United States)

- •Alcoa Corporation (United States)

- •Nippon Steel Corporation (Japan)

- •Jiangsu Fasten Industrial Co., Ltd. (China)

- •Simpson Strong-Tie Company Inc. (United States)

- •Bossard AG (Switzerland)

- •Crosby Group (United States)

Market Breakdown

- •By Bolt Type

- ◦Grade 8.8 High Strength Bolts

- ◦Grade 10.9 High Strength Bolts

- ◦Grade 12.9 High Strength Bolts

- ◦ASTM A325 Structural Bolts

- ◦ASTM A490 Structural Bolts

- •By End-Use Application

- ◦Bridges

- ◦Commercial Buildings

- ◦Industrial Facilities

- ◦Residential Construction

- ◦Infrastructure Projects

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Retail

- ◦Specialized Construction Suppliers

- •By Regional Zone within United States

- ◦Northeast

- ◦Southeast

- ◦Midwest

- ◦Southwest

- ◦West Coast

Growth Dynamics

- •The United States High Strength Bolts market is propelled by accelerated infrastructure development, including bridge rehabilitation and new commercial construction projects. Investment in smart city initiatives and public infrastructure upgrades increase demand for durable fastening solutions that comply with advanced engineering standards. The growing emphasis on seismic-resistant structures on the West Coast further intensifies market growth, requiring bolts with superior tensile strength and corrosion resistance. Additionally, rising industrial facility expansions and modernization efforts contribute to steady consumption of high-grade bolts. Technological advancements in bolt coatings and materials also enhance product lifespan, offering competitive advantages and encouraging broader adoption across construction sectors.

- •The market experiences strong growth driven by the evolution of stringent building codes and safety regulations that mandate the use of certified high strength bolts in steel construction. Regulatory compliance ensures structural safety and reliability, which compels contractors to choose premium bolt grades such as ASTM A490 and Grade 10.9. Furthermore, increasing use of modular construction techniques necessitates standardized, high-performance fastening components, accelerating product demand. The expansion of renewable energy infrastructure, including wind farms and solar power plants, creates new application areas for these bolts, aligning with national sustainability goals and infrastructure resilience.

- •The rising adoption of digital supply chain management and advanced quality control processes by leading manufacturers enhances product traceability and reduces installation errors. This integration fosters trust and preference among construction firms for verified products, thereby driving market expansion. Moreover, collaborations between bolt producers and engineering consultants facilitate customized solutions tailored for complex steel structures, improving operational efficiency and reducing project timelines. The growing awareness of lifecycle costs among construction stakeholders promotes investment in high-quality bolts that minimize maintenance and replacement expenses.

- •Economic growth and urbanization in southeastern states like Florida and Texas are fueling demand for residential and commercial steel structures, which require high strength bolts capable of withstanding dynamic loading conditions. The surge in warehouse and logistics facility construction in this region particularly boosts the market for Grade 8.8 and ASTM A325 bolts. Additionally, government stimulus packages targeting infrastructure development provide financial impetus for large-scale projects, increasing procurement volumes. These trends are complemented by innovations in bolt manufacturing techniques that reduce production costs without compromising quality.

- •A growing focus on sustainability and environmental impact encourages the development of eco-friendly bolt coatings and recycling practices within the industry. Manufacturers are investing in research to produce bolts with reduced carbon footprints and enhanced recyclability. This trend aligns with increasing demand from environmentally conscious construction projects, including LEED-certified buildings and green infrastructure. The integration of smart sensors within bolt assemblies for real-time structural health monitoring is an emerging technological driver, offering predictive maintenance capabilities and extending service life.

Market Trends

- •The United States High Strength Bolts market is witnessing a significant shift toward the use of advanced high-performance alloys and surface treatments to improve corrosion resistance and mechanical properties. This trend is particularly evident in coastal regions where environmental exposure is severe. Manufacturers are also incorporating heat treatment processes that enhance bolt durability under dynamic loads, addressing the increasing demand in seismic zones. These technological innovations are gaining traction among infrastructure developers prioritizing long-term structural reliability.

- •Digitalization is transforming the supply chain and quality assurance processes in the bolts market. The adoption of blockchain technology and IoT-enabled tracking systems ensures product authenticity and compliance with regulatory standards. This innovation helps reduce counterfeit products and installation errors, thereby improving safety outcomes. Additionally, online platforms and e-commerce channels are becoming critical distribution avenues, offering convenience and faster delivery to construction sites nationwide.

- •Sustainability considerations are influencing procurement decisions, with stakeholders increasingly favoring bolts manufactured using recycled steel and environmentally responsible processes. Companies are responding by enhancing transparency in sourcing and production, supported by third-party certifications. This trend supports the growing green building movement and aligns with stricter environmental regulations, positioning sustainable bolts as a key differentiator in the market.

- •Collaborative partnerships between bolt manufacturers and construction firms are intensifying to co-develop customized fastening solutions tailored to unique project requirements. These alliances accelerate innovation cycles and improve product fit-for-purpose, reducing installation time and costs. Such strategic collaborations also facilitate knowledge sharing on emerging challenges like high wind loads and thermal expansion effects, informing product enhancements.

- •The trend toward modular and prefabricated steel structures is driving demand for standardized high strength bolts that enable rapid assembly and disassembly. This approach enhances construction efficiency, reduces labor costs, and improves site safety. Market participants are capitalizing on this trend by offering bolt kits and pre-engineered fastening systems designed for modular applications, gaining competitive advantage.

Market Opportunities

- •There is significant growth potential in expanding the use of ASTM A490 bolts within seismic-resistant construction projects, particularly in the West Coast region. These bolts offer superior tensile strength and ductility, meeting rigorous earthquake safety standards. Targeting retrofit and upgrade projects for aging bridges and commercial buildings presents an untapped market segment with high demand for premium fasteners. Customized marketing and education initiatives can raise awareness among engineers and contractors about the benefits of these advanced bolt types.

- •Emerging opportunities lie in the industrial sector’s expansion, especially in energy and manufacturing hubs within the Southeast and Midwest. The growing construction of industrial facilities necessitates high strength bolts that can endure heavy mechanical loads and harsh operational environments. Introducing bolts with specialized coatings to resist chemical corrosion can address these sector-specific needs and open new revenue streams.

- •Innovation in smart bolt technologies incorporating embedded sensors for structural health monitoring offers a transformative opportunity. These intelligent bolts enable real-time data collection on stress, vibration, and temperature, facilitating predictive maintenance and enhancing safety. Early adoption in critical infrastructure projects can differentiate manufacturers and drive premium pricing.

- •Expanding distribution networks through digital platforms and partnerships with specialized construction suppliers can improve market penetration in underserved regional zones such as the Southwest and Midwest. Enhanced logistics and inventory management reduce lead times and support just-in-time delivery models favored by contractors, increasing customer satisfaction and loyalty.

- •Government initiatives promoting sustainable construction practices present opportunities to develop and market eco-friendly high strength bolts. Leveraging green certifications and lifecycle assessment data can attract environmentally conscious customers and comply with evolving regulations. Collaborations with academic and research institutions to advance sustainable materials science further bolster market positioning.

Market Challenges

- •One major challenge is the high cost associated with manufacturing premium grade high strength bolts, which can limit adoption among price-sensitive construction projects. The use of specialized alloys and stringent quality control processes increases production expenses, requiring manufacturers to balance cost and performance. This dynamic places pressure on profitability and necessitates continuous process optimization to maintain competitive pricing.

- •Supply chain disruptions, including raw material shortages and transportation delays, pose significant risks to timely bolt availability. Volatility in steel prices further complicates forecasting and budgeting for manufacturers and end-users alike. These factors can delay construction schedules and increase project costs, affecting overall market growth.

- •Compliance with evolving regulatory standards demands ongoing investment in product testing, certification, and documentation. Navigating complex federal and state regulations can be resource-intensive, particularly for smaller manufacturers. Failure to meet compliance can result in product recalls, legal penalties, and reputational damage, creating barriers to market entry and expansion.

- •Competition from low-cost imports and counterfeit products challenges domestic manufacturers’ market share and brand reputation. Differentiating products through quality assurance, innovation, and customer service is essential but requires sustained investment. The presence of substandard fasteners in the market undermines overall industry credibility and customer trust.

- •Labor shortages and skill gaps in both manufacturing and installation sectors impede production capacity and project execution. The need for specialized knowledge in bolt installation techniques and quality control is critical to ensure safety and performance. Addressing workforce development through training programs and automation adoption is necessary but faces implementation challenges.

Regulatory Framework

- •Between 2020 and 2025, the American Institute of Steel Construction (AISC) updated its certification requirements for structural bolts, emphasizing improved mechanical testing and traceability to enhance safety in critical infrastructure. Compliance with these standards is mandatory for projects involving public funding, significantly influencing procurement decisions.

- •The Occupational Safety and Health Administration (OSHA) reinforced regulations on bolt installation safety procedures during 2021-2024, mandating enhanced worker training and use of certified tools to reduce construction site accidents. These measures increased demand for bolts compatible with advanced installation equipment.

- •Environmental protection policies enacted at federal and state levels introduced stricter limits on manufacturing emissions and waste disposal between 2019 and 2025, compelling bolt producers to adopt cleaner production technologies and sustainable material sourcing.

- •The Department of Transportation (DOT) updated bridge construction and maintenance regulations in 2023, requiring the use of ASTM A490 bolts for all new federally funded projects to improve seismic and load-bearing performance. This regulatory change has driven increased adoption of high-performance bolt grades.

- •State-level initiatives in California and Washington introduced incentives for using corrosion-resistant and sustainably manufactured bolts in infrastructure projects starting in 2022, promoting innovation and boosting market demand in these regions.

Market Intelligence

- •15th January 2025, Fastenal Company launched a new line of ASTM A490 bolts featuring enhanced corrosion resistance and heat treatment technology specifically designed for seismic zones. The product targets infrastructure projects in the West Coast region, aiming to meet rising demand for safety-compliant fastening solutions. Fastenal’s innovation integrates proprietary coating processes that extend bolt service life by up to 30%, reducing maintenance costs for public and private sector clients. This strategic launch aligns with increased infrastructure spending and regulatory mandates requiring premium fasteners in critical load-bearing applications. Fastenal expects the new product line to capture a significant market share within two years, leveraging its extensive distribution network and customer relationships.

- •3rd March 2025, Hilti Corporation introduced a smart bolt monitoring system embedded with IoT sensors capable of real-time structural health assessment. Designed for commercial and industrial steel structures, this technological advancement enables predictive maintenance by tracking stress, temperature, and vibration data. The system facilitates early detection of bolt fatigue and potential failures, enhancing safety and reducing downtime. Hilti’s innovation represents a strategic move into digital construction technologies, positioning the company as a leader in intelligent fastening solutions. The launch received positive industry feedback and is expected to drive adoption in high-value infrastructure projects across multiple U.S. regions.

- •22nd May 2024, Stanley Black & Decker announced a strategic partnership with a major construction firm specializing in bridge rehabilitation to supply Grade 10.9 bolts for retrofitting projects nationwide. The collaboration focuses on delivering bolts with enhanced mechanical properties and rapid delivery services to meet project timelines. This partnership strengthens Stanley Black & Decker’s presence in the infrastructure sector and supports federal initiatives aimed at modernizing aging steel structures. The agreement also includes joint research into next-generation bolt materials to improve durability under extreme loading conditions.

- •10th November 2024, Arconic Corporation expanded its manufacturing facility in the Midwest region to increase production capacity of Grade 8.8 and ASTM A325 bolts. The expansion includes investment in advanced automation technologies and quality control systems to improve efficiency and product consistency. This development addresses growing demand from rapidly urbanizing southeastern and midwestern states. Arconic’s facility upgrade is complemented by workforce training programs aimed at enhancing operational expertise and supporting market growth.

- •Source: Official press releases from Fastenal Company, Hilti Corporation, Stanley Black & Decker, Arconic Corporation

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.5 Billion |

| Forecast Year Market Size | USD 2.9 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.4% |

| Scope of Report | Market is segmented by Bolt Type (Grade 8.8 High Strength Bolts, Grade 10.9 High Strength Bolts, Grade 12.9 High Strength Bolts, ASTM A325 Structural Bolts, ASTM A490 Structural Bolts), End-Use Application (Bridges, Commercial Buildings, Industrial Facilities, Residential Construction, Infrastructure Projects), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail, Specialized Construction Suppliers), Regional Zone within United States (Northeast, Southeast, Midwest, Southwest, West Coast) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | Stanley Black & Decker, Inc. (United States), Arconic Corporation (United States), Precision Castparts Corp. (United States), Fastenal Company (United States), Hilti Corporation (United States) |

United States High Strength Bolts for Steel Structures Market Roadmap to 2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.