Europe Business Electronics & E-Waste Recycling Market - Outlook 2025-2034

Europe Business Electronics & E-Waste Recycling Market is segmented by Type (Mobile Devices, Computers & Laptops, Televisions & Displays, Batteries, Circuit Boards), Application (Consumer Electronics, Industrial Electronics, IT & Telecom Equipment, Medical Devices, Automotive Electronics), Service Type (Collection Services, Dismantling Services, Material Recovery, Refurbishing Services), Processing Technology (Mechanical Recycling, Chemical Recycling, Pyrometallurgical Processing), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Business Electronics & E-Waste Recycling market encompasses the systematic process of collecting, dismantling, and recovering valuable materials from electronic waste generated by business electronics such as consumer devices, industrial machinery, IT and telecom equipment, medical devices, and automotive electronics. This market addresses the environmental challenges posed by the rapid obsolescence of electronic products by enabling sustainable disposal and resource recovery. It includes advanced recycling techniques like automated sorting, chemical processing, and material recovery to extract precious metals and reduce hazardous waste. The market is driven by rigorous European regulations, increasing electronic consumption, and growing awareness about environmental sustainability. Key applications involve recycling of mobile devices, computers, televisions, batteries, and circuit boards, supporting circular economy initiatives. The sector is critical to reducing landfill use, minimizing toxic waste, and preserving raw materials, thereby fostering sustainable industrial practices and compliance with EU directives across member states.

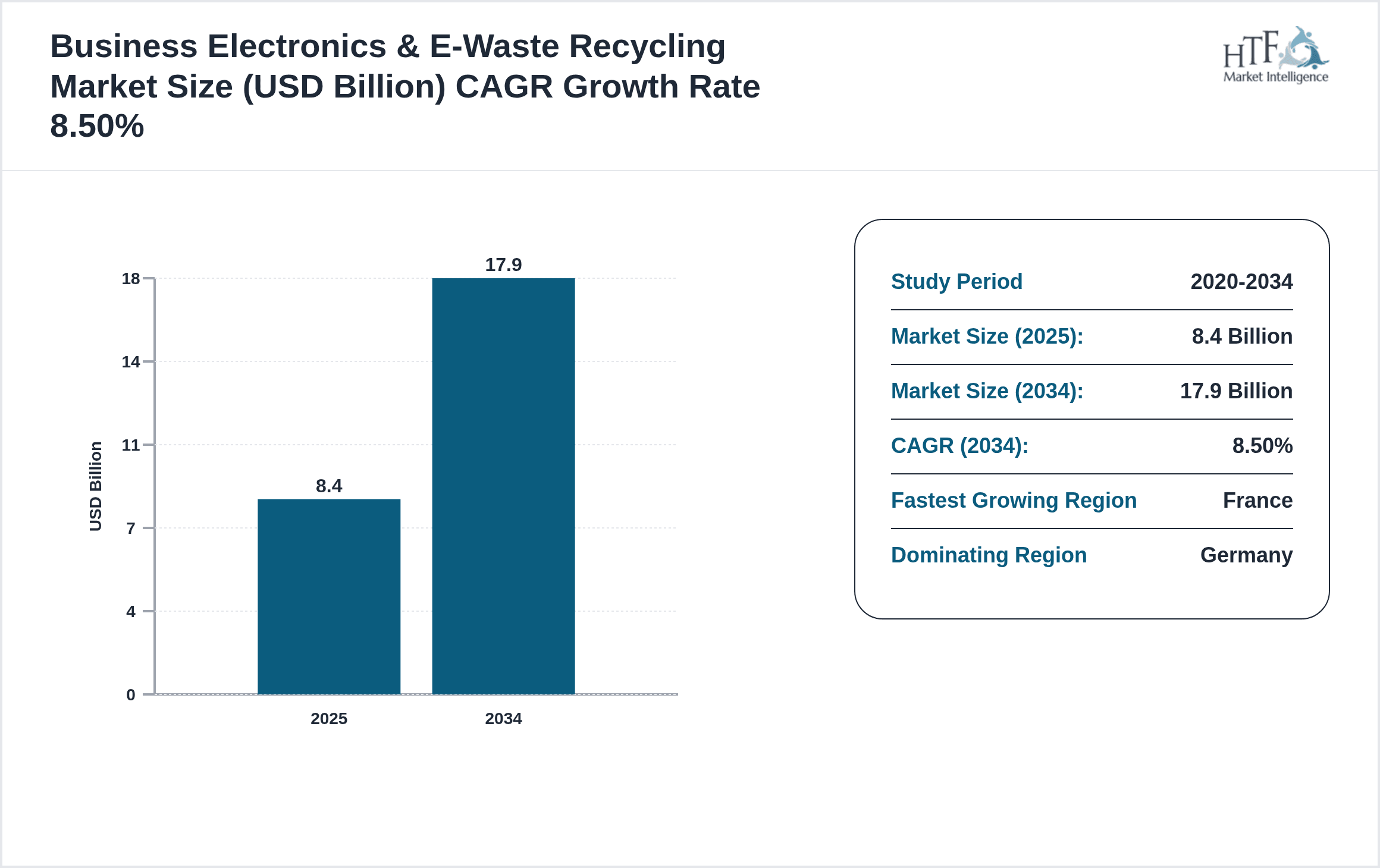

- •Europe's Business Electronics & E-Waste Recycling market is poised for substantial growth with a base market size of USD 8.4 Billion in 2025, projected to reach USD 17.9 Billion by 2034 at a CAGR of 8.5%. Germany leads the market with a 28% share, while France represents the fastest-growing country at an 11.3% CAGR. Mobile devices dominate the product segment, with batteries showing the fastest growth due to rising adoption of electric vehicles and portable electronics. Regulatory enforcement, technological advancements, and increasing corporate sustainability initiatives further fuel market expansion. Year-over-year growth is estimated at 8.2%, reflecting strong demand for efficient recycling solutions and material recovery technologies.

- •The Europe Business Electronics & E-Waste Recycling market offers strategic value by enabling companies, governments, and environmental agencies to mitigate electronic waste impact while capturing economic value from recovered materials. It supports the EU’s circular economy goals and compliance with directives such as WEEE and RoHS. The market facilitates innovation in recycling processes, promotes sustainable supply chains, and reduces dependency on raw material imports. Stakeholders benefit from enhanced environmental stewardship, reduced operational risks, and new revenue streams from secondary materials. This market forms a cornerstone of Europe’s environmental policy framework and contributes to global sustainability efforts by setting benchmarks in responsible e-waste management.

Competitive Landscape

Companies operating in the Europe Business Electronics & E-Waste Recycling industry employ diverse strategies to sustain and enhance their market presence. Key approaches include forming strategic partnerships with electronics manufacturers and waste management firms to secure steady e-waste supply and improve recycling efficiency. Global expansion efforts target emerging European markets with rising e-waste volumes. Innovation in automated sorting technologies, chemical recycling methods, and material recovery enhances product differentiation and operational efficiency. Firms invest in digital tracking and compliance solutions to meet stringent regulatory standards and provide transparency. Mergers and acquisitions consolidate market positions and broaden service portfolios. Pricing strategies emphasize value-added recycling services and sustainability certifications. Distribution channels expand to include reverse logistics networks and collection points. Technological adoption focuses on environmentally friendly processes and circular economy integration. Regional competition drives continuous improvements, while barriers such as high capital expenditure and regulatory complexities influence market entry. Future trends suggest intensified collaboration and digitalization to optimize resource recovery and regulatory compliance.

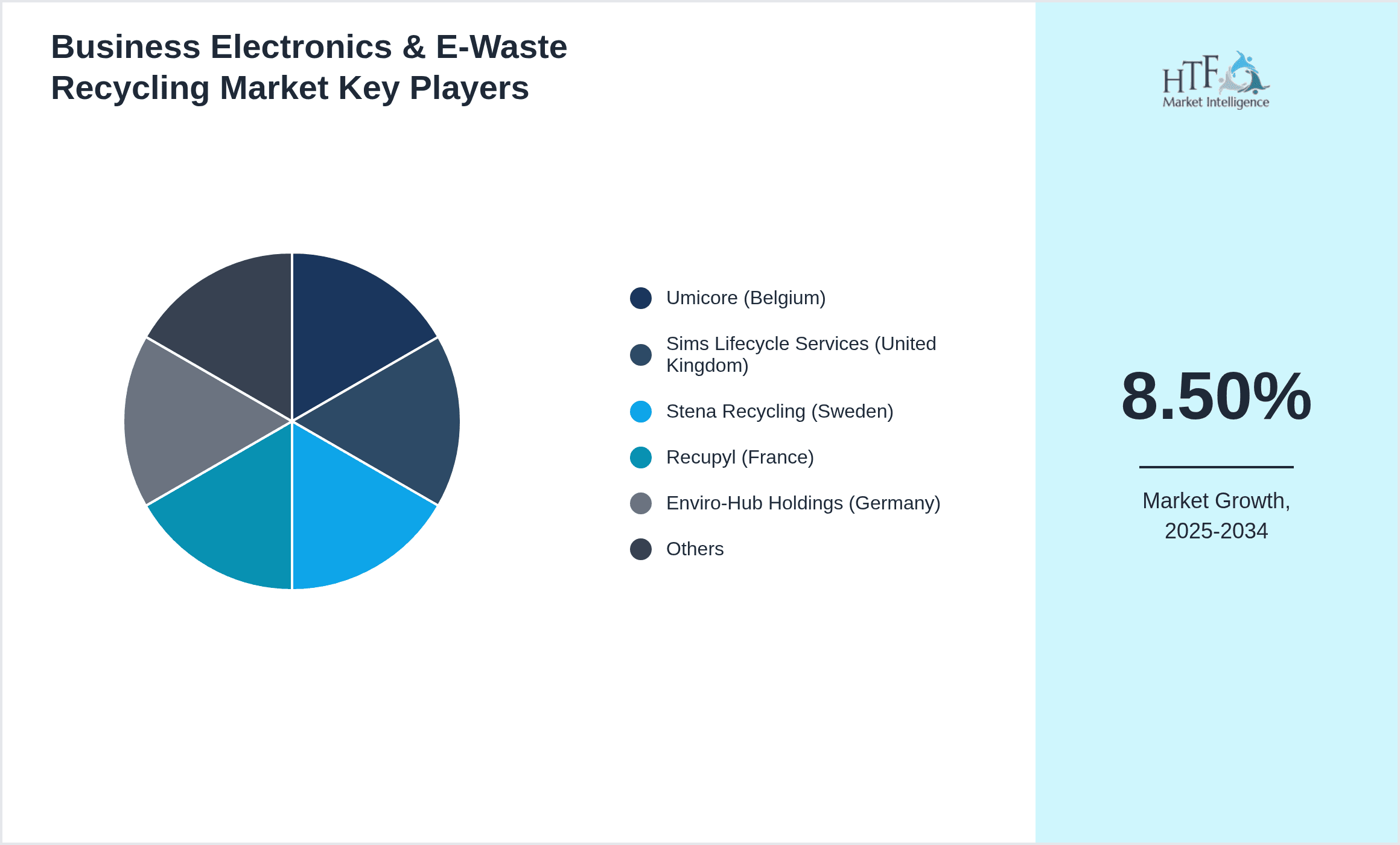

Leading Companies in Business Electronics & E-Waste Recycling Market

- •Umicore (Belgium)

- •Sims Lifecycle Services (United Kingdom)

- •Stena Recycling (Sweden)

- •Recupyl (France)

- •Enviro-Hub Holdings (Germany)

- •Veolia (France)

- •Boliden Group (Sweden)

- •TES (UK)

- •Attero Recycling (Netherlands)

- •Aurubis AG (Germany)

- •Renasci (Italy)

- •Ecoreco (Spain)

- •Recylex (France)

- •Suez (France)

- •Paprec Group (France)

- •Cycleurope (Sweden)

- •Recycling Technologies (UK)

- •Derichebourg (France)

- •Umweltschutz Recycling (Germany)

- •ECOBAT Technologies (Belgium)

Market Breakdown

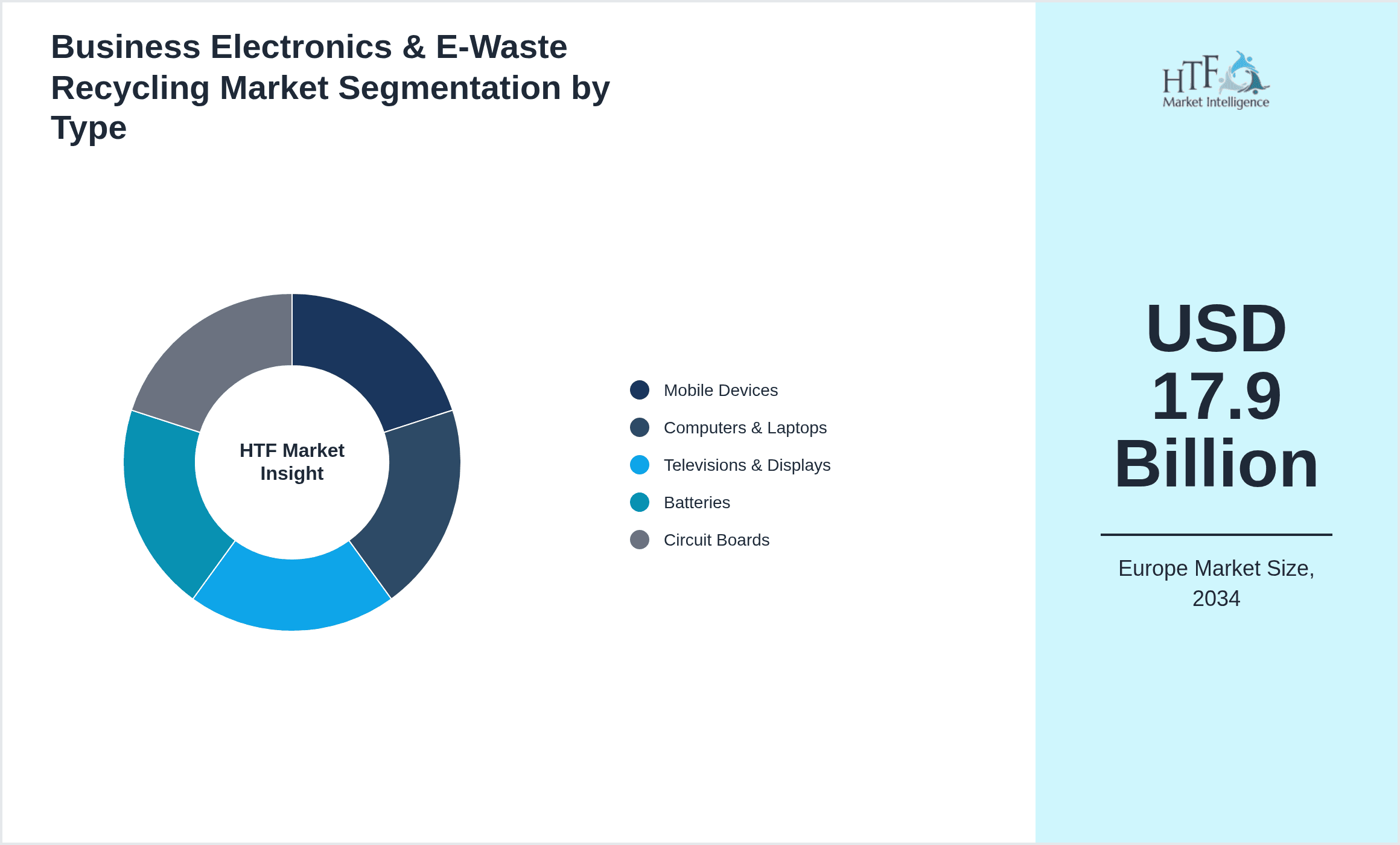

- •By Type

- ◦Mobile Devices

- ◦Computers & Laptops

- ◦Televisions & Displays

- ◦Batteries

- ◦Circuit Boards

- •By Application

- ◦Consumer Electronics

- ◦Industrial Electronics

- ◦IT & Telecom Equipment

- ◦Medical Devices

- ◦Automotive Electronics

- •By Service Type

- ◦Collection Services

- ◦Dismantling Services

- ◦Material Recovery

- ◦Refurbishing Services

- •By Processing Technology

- ◦Mechanical Recycling

- ◦Chemical Recycling

- ◦Pyrometallurgical Processing

Growth Dynamics

Europe's Business Electronics & E-Waste Recycling market experiences robust growth driven by increasing electronic consumption and rapid product obsolescence across consumer and industrial segments. The adoption of stringent EU directives such as WEEE and RoHS compels companies to invest in compliant recycling infrastructure, intensifying market expansion. Recent initiatives by leading players like Umicore's investment in battery recycling facilities in Germany exemplify strategic responses to rising lithium-ion battery waste from electric vehicles. Technological advancements in automated dismantling and material recovery optimize processing efficiency, reducing environmental impact and operational costs. Growing corporate sustainability mandates and circular economy goals promote expanded recycling programs across industries, supported by government incentives and funding. The surge in IT equipment upgrades and medical electronics disposal further fuel e-waste volumes. Additionally, increasing public awareness campaigns and collection schemes enhance material recovery rates, contributing to continuous market growth.

Market Trends

The Europe Business Electronics & E-Waste Recycling market is witnessing emerging trends focused on integrating digital technologies and circular economy principles. Advanced tracking systems employing blockchain ensure transparency and regulatory compliance throughout the e-waste lifecycle. Companies increasingly adopt chemical recycling methods to reclaim rare earth elements and precious metals with high efficiency, addressing supply chain vulnerabilities. The rise of electric vehicles accelerates demand for specialized battery recycling services, prompting innovations in lithium-ion extraction technologies. Collaborative platforms between manufacturers and recyclers promote product design for recyclability, enhancing resource recovery. Public-private partnerships expand collection infrastructure, especially in urban centers. Sustainability reporting and certifications become standard, reinforcing market credibility. Furthermore, the development of refurbished electronics markets complements recycling efforts, extending product lifecycles. These trends collectively position the market for sustainable growth aligned with Europe’s environmental targets and technological progress.

Market Opportunities

Significant opportunities exist in expanding battery recycling capacities driven by Europe’s aggressive electric vehicle adoption targets and renewable energy storage needs. Investments in chemical recycling technologies present avenues to recover high-value materials such as cobalt and lithium from complex waste streams. Emerging markets in Eastern Europe offer growth potential due to rising electronic consumption and evolving regulatory frameworks. The integration of AI and robotics in dismantling processes enhances operational efficiency and safety, attracting investments. Cross-border collaborations within the EU facilitate standardized recycling practices and economies of scale. Additionally, the growing demand for refurbished business electronics creates complementary revenue streams. Companies can capitalize on government subsidies and green finance instruments to expand infrastructure. Increasing consumer awareness and corporate ESG commitments support scalable collection and recycling programs. These dynamics create a favorable environment for innovation-driven growth and market diversification.

Market Challenges

Challenges in the Europe Business Electronics & E-Waste Recycling market include fluctuating raw material prices impacting profitability of recovered materials. Complex electronic products with miniaturized components complicate dismantling and material recovery, increasing operational costs. Regulatory compliance across multiple European countries requires continuous adaptation and investment in reporting and tracking systems. Illegal e-waste exports and informal recycling persist, undermining formal market growth and environmental goals. Limited consumer participation in collection programs hampers volume recovery. High capital expenditure for advanced recycling technologies creates entry barriers for smaller players. Recent reports highlight delays in implementing standardized EU-wide e-waste management policies, causing market fragmentation. Supply chain disruptions due to geopolitical tensions affect inbound and outbound logistics of recyclable materials. Additionally, hazardous substances in older electronics pose safety risks during processing, necessitating stringent health protocols. These factors collectively constrain market scalability and require coordinated industry and governmental efforts to address.

Regulatory Framework

The European Union’s Waste Electrical and Electronic Equipment Directive, updated in 2018, mandates member states to enhance collection, treatment, and recovery targets for e-waste, significantly influencing market operations. The Restriction of Hazardous Substances Directive restricts use of toxic materials in electronics, facilitating safer recycling processes. The EU Circular Economy Action Plan, launched in 2020, emphasizes sustainable product design and resource efficiency, driving innovation in recycling technologies. National regulations such as Germany’s Electrical and Electronic Equipment Act complement EU directives by establishing strict producer responsibility schemes and reporting requirements. These legislative frameworks collectively ensure environmental compliance, promote material recovery, and incentivize investments in advanced recycling infrastructure across Europe. Continuous updates to regulatory standards enforce transparency and traceability in e-waste management, aligning market growth with environmental and public health objectives.

Market Intelligence

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.4 Billion |

| Forecast Year Market Size | USD 17.9 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Type (Mobile Devices, Computers & Laptops, Televisions & Displays, Batteries, Circuit Boards), Application (Consumer Electronics, Industrial Electronics, IT & Telecom Equipment, Medical Devices, Automotive Electronics), Service Type (Collection Services, Dismantling Services, Material Recovery, Refurbishing Services), Processing Technology (Mechanical Recycling, Chemical Recycling, Pyrometallurgical Processing) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Umicore (Belgium), Sims Lifecycle Services (United Kingdom), Stena Recycling (Sweden), Recupyl (France), Enviro-Hub Holdings (Germany), Veolia (France), Boliden Group (Sweden), TES (UK), Attero Recycling (Netherlands), Aurubis AG (Germany), Renasci (Italy), Ecoreco (Spain), Recylex (France), Suez (France), Paprec Group (France), Cycleurope (Sweden), Recycling Technologies (UK), Derichebourg (France), Umweltschutz Recycling (Germany), ECOBAT Technologies (Belgium) |

Europe Business Electronics & E-Waste Recycling Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.