China Sic Diesel Particulate Filter Market - Size & Outlook 2025-2034

China Sic Diesel Particulate Filter Market is segmented by Application (Commercial Vehicles, Passenger Cars, Industrial Machinery, Marine Engines, Construction Equipment), Type (Wall-Flow Filters, Flow-Through Filters, Partial Filters, Catalyzed Filters, Non-Catalyzed Filters), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Sic Diesel Particulate Filter Market is a specialized segment focusing on silicon carbide (SiC) based filters that mitigate diesel engine emissions by capturing particulate matter and soot. These filters are integral to complying with China’s increasingly stringent environmental and emission regulations, especially within the automotive and industrial sectors. The market comprises diverse types including wall-flow, flow-through, catalyzed, and non-catalyzed filters, each optimized for specific performance and application needs. Application sectors encompass commercial vehicles, passenger cars, marine engines, construction equipment, and industrial machinery, reflecting the broad utility of these filters in reducing pollution from diesel-powered equipment. China’s regulatory framework, rapid automotive growth, and technological advancements in filter materials and designs drive market expansion. Geographically, East China dominates due to its dense industrial base and vehicle population, while Southwest China shows the fastest growth owing to infrastructural development and rising environmental awareness. The market outlook through 2034 forecasts robust growth driven by innovation, policy enforcement, and increasing diesel vehicle adoption, positioning SiC filters as critical components in China's sustainable transportation and industrial strategies.

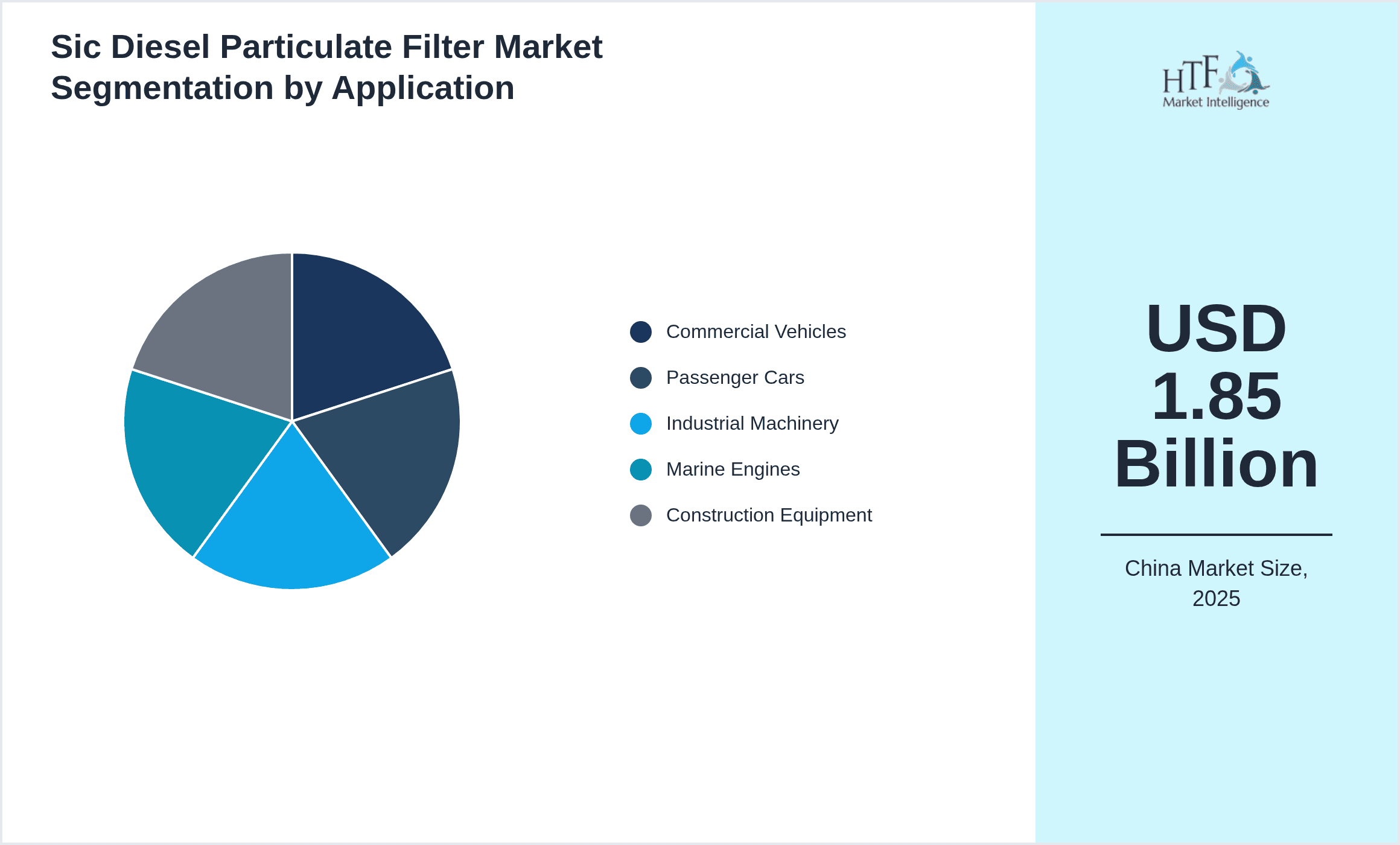

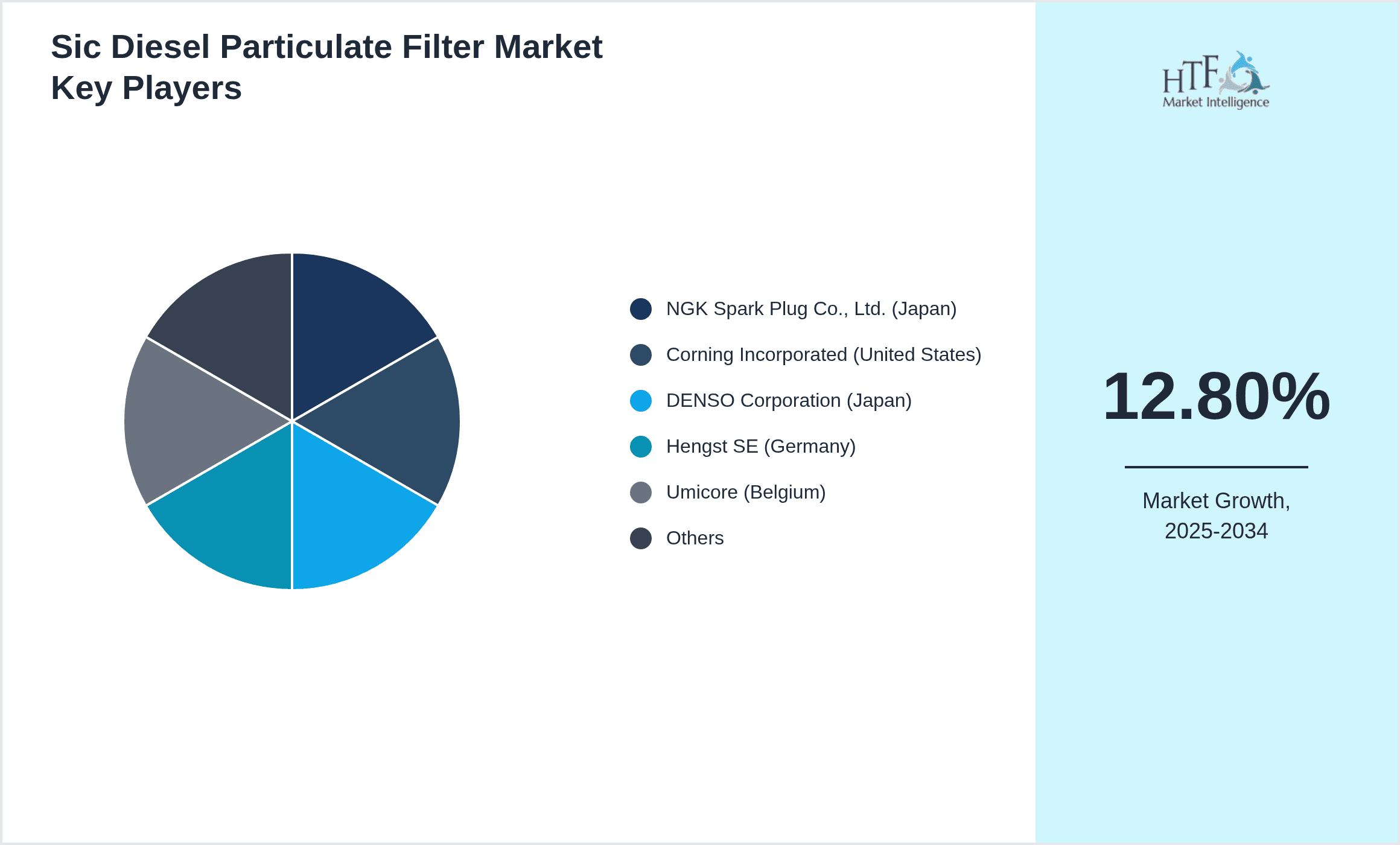

- •The China Sic Diesel Particulate Filter Market is projected to grow from USD 1.85 Billion in 2025 to USD 5.12 Billion by 2034, exhibiting a CAGR of 12.8%. Key highlights include the dominance of wall-flow filters with a substantial market share, and catalyzed filters leading in growth rate due to their enhanced emission control capabilities. East China currently holds the largest regional market share at 35%, benefiting from advanced manufacturing infrastructure and stringent emission norms. Southwest China is emerging as the fastest growing sub-region with a CAGR of 15.3%, supported by government initiatives promoting cleaner diesel technologies. The commercial vehicle segment remains the largest application area, driven by regulatory mandates on heavy-duty diesel engines. The market’s strategic importance lies in its alignment with China’s environmental goals and industrial modernization, offering substantial opportunities for filter manufacturers, automotive OEMs, and aftermarket service providers to capitalize on evolving emission standards and consumer demand for cleaner diesel vehicles.

- •The value proposition of the China Sic Diesel Particulate Filter Market is underscored by its critical role in enabling compliance with China’s rigorous emission standards, thus contributing to improved air quality and public health. For automotive manufacturers and industrial operators, adopting advanced SiC filters ensures reduced particulate emissions and enhanced engine performance. The market holds strategic importance for environmental regulators, technology developers, and investors focusing on sustainable transportation solutions. Continuous innovations in filter materials and coating technologies provide competitive advantages and operational efficiencies. Additionally, the growing demand for diesel-powered commercial vehicles and machinery in key economic zones expands the market potential. Stakeholders benefit from insights into regional demand patterns, regulatory impacts, and technological trends that shape product development and supply chain strategies, making this market pivotal in China’s transition towards greener diesel technologies and sustainable industrial growth.

Competitive Landscape

The competitive landscape of the China Sic Diesel Particulate Filter Market is characterized by intense rivalry among domestic and international manufacturers focusing on technological innovation, product quality, and strategic partnerships. Market leaders invest heavily in R&D to enhance filter efficiency, durability, and thermal stability, leveraging silicon carbide’s superior material properties. Companies differentiate through proprietary coating technologies and integration with emission control systems. Pricing strategies and after-sales service quality also influence market positioning, as clients demand cost-effective and reliable solutions. Market entry barriers include high capital requirements, technical expertise, and compliance with stringent emission standards. Regional competition is pronounced with East China hosting major manufacturing hubs, while emerging zones like Southwest China attract new entrants driven by supportive policies. Strategic alliances, joint ventures, and acquisitions are common to expand product portfolios and geographical reach. Future trends indicate increased consolidation and innovation aimed at meeting evolving regulatory requirements and customer expectations for cleaner diesel technologies.

Leading Companies in China Sic Diesel Particulate Filter Market

- •NGK Spark Plug Co., Ltd. (Japan)

- •Corning Incorporated (United States)

- •DENSO Corporation (Japan)

- •Hengst SE (Germany)

- •Umicore (Belgium)

- •Clarios (United States)

- •Yantai Wanhua Silicone Co., Ltd. (China)

- •Zhejiang Zheneng New Energy Co., Ltd. (China)

- •Shandong Sinocera Functional Material Co., Ltd. (China)

- •Ningbo Jinhong Technology Co., Ltd. (China)

- •BASF SE (Germany)

- •Johnson Matthey Plc (United Kingdom)

- •Tenneco Inc. (United States)

- •Mann+Hummel GmbH (Germany)

- •Faurecia S.A. (France)

- •Eberspaecher Group (Germany)

- •Hitachi Automotive Systems (Japan)

- •Cummins Inc. (United States)

- •BorgWarner Inc. (United States)

- •Wanhua Chemical Group Co., Ltd. (China)

- •Saint-Gobain S.A. (France)

- •Cataler Corporation (Japan)

- •Engelhard Corporation (United States)

- •Ceres Power Holdings plc (United Kingdom)

- •Hitachi Metals, Ltd (Japan)

China Sic Diesel Particulate Filter Market Segmentation

- •By Filter Type

- ◦Wall-Flow Filters

- ◦Flow-Through Filters

- ◦Partial Filters

- ◦Catalyzed Filters

- ◦Non-Catalyzed Filters

- •By Application

- ◦Commercial Vehicles

- ◦Passenger Cars

- ◦Industrial Machinery

- ◦Marine Engines

- ◦Construction Equipment

- •By End-Use Industry

- ◦Automotive OEMs

- ◦Aftermarket Services

- ◦Industrial Equipment Manufacturers

- ◦Marine Equipment Providers

- •By Technology

- ◦Ceramic Silicon Carbide Filters

- ◦Metallic Silicon Carbide Filters

- ◦Coated vs. Uncoated Filters

Growth Dynamics

The China Sic Diesel Particulate Filter Market growth is propelled by stringent government regulations targeting diesel emission reductions to combat air pollution. China’s National VI emission standards have accelerated adoption of SiC filters, which offer superior thermal resistance and filtration efficiency. The expanding commercial vehicle fleet and industrial machinery usage further boost demand. Technological advancements in filter materials and coatings improve longevity and performance, attracting OEMs and aftermarket players. Additionally, increased environmental awareness among consumers and businesses drives market expansion, supported by government subsidies and incentives for cleaner diesel technologies.

Market Trends

Emerging trends in the China Sic Diesel Particulate Filter Market include the integration of catalyzed filters combining filtration with catalytic conversion to simultaneously reduce particulates and NOx emissions. Adoption of advanced manufacturing techniques like 3D printing and nano-coatings enhances filter efficiency and durability. Strategic collaborations between filter manufacturers and automotive OEMs streamline product development and compliance. Furthermore, rising investments in aftermarket services reflect growing demand for replacement filters as diesel vehicle stock expands. The market also witnesses a shift towards lightweight and compact filter designs to improve fuel efficiency and reduce vehicle weight.

Market Opportunities

Significant opportunities exist in expanding filter applications beyond traditional commercial vehicles to marine engines and construction equipment, sectors increasingly adopting emission control technologies. Growth potential is also notable in developing coated SiC filters with multifunctional capabilities, enhancing emission reduction performance. Regional expansion into rapidly industrializing sub-regions such as Southwest China offers fresh market avenues. Additionally, aftermarket replacement demand is poised for strong growth as diesel vehicles age, presenting lucrative opportunities for filter manufacturers and distributors. Investment in R&D for next-generation filter materials and digital monitoring solutions can further enhance market position.

Market Challenges

Challenges in the China Sic Diesel Particulate Filter Market include high initial costs of SiC filters compared to traditional alternatives, which may limit adoption among cost-sensitive OEMs and end-users. Manufacturing complexity and raw material supply constraints pose risks to scaling production. Additionally, fluctuating diesel vehicle sales due to electrification trends and alternative fuel adoption could impact market demand. Compliance with evolving and regionalized emission standards requires continuous innovation and investment. Furthermore, competition from emerging filtration technologies and substitute materials intensifies pressure on established players to maintain differentiation and cost efficiency.

Regulatory Framework

Between 2020 and 2025, China implemented the National VI emission standards requiring substantial reductions in diesel particulate emissions, catalyzing the adoption of advanced SiC diesel particulate filters. These regulations mandate stricter limits on particulate matter and nitrogen oxides for heavy-duty and light-duty diesel vehicles, driving OEM compliance and aftermarket upgrades. Enforcement includes rigorous vehicle inspection and maintenance protocols, impacting filter replacement cycles. Regional policies in key industrial provinces further incentivize cleaner diesel technologies through subsidies and penalties for non-compliance. Additionally, eco-labeling and green procurement policies promote the use of certified SiC filters across automotive and industrial sectors, shaping market demand and innovation focus.

Market Intelligence

- •15th January 2025, NGK Spark Plug Co., Ltd. launched a new generation of silicon carbide diesel particulate filters designed specifically for China’s National VI compliant commercial vehicles. These filters feature enhanced thermal shock resistance and catalytic coating technology that improves particulate and NOx reduction efficiency by over 20%. The product aims to support OEMs in meeting stringent emission targets while optimizing fuel economy. NGK plans to expand manufacturing capacity in China to meet growing domestic demand, reinforcing its leadership position in the market. Source: NGK Spark Plug Official Announcement.

- •5th April 2025, Corning Incorporated introduced an innovative ceramic matrix composite SiC filter targeting heavy-duty diesel vehicles in China. This technology enhances filter durability and regeneration cycles under high thermal loads typical in China’s diverse climatic regions. Corning’s strategic collaboration with leading Chinese automotive manufacturers focuses on integrating this filter technology into next-generation diesel engines, aiming for improved emission performance and lifecycle cost reduction. This launch underscores Corning’s commitment to sustainable mobility solutions in China’s evolving emission landscape. Source: Corning Press Release.

- •20th June 2025, Shandong Sinocera Functional Material Co., Ltd. announced a strategic partnership with Zhejiang Zheneng New Energy Co., Ltd. to develop high-efficiency catalyzed SiC filters tailored for marine diesel engines operating in China’s coastal regions. The collaboration combines Sinocera’s advanced ceramic expertise with Zheneng’s marine engine market knowledge to address rising environmental regulations on maritime emissions. The partnership aims to commercialize products by late 2026, targeting a growing segment driven by China’s Blue Economy initiatives. Source: Company Websites.

- •1st September 2025, DENSO Corporation expanded its research facility in Shanghai to accelerate development of lightweight SiC filters for passenger cars in China. This expansion supports DENSO’s strategic focus on emission compliance and fuel efficiency improvements amid increasingly strict urban emission controls. The facility will facilitate joint projects with Chinese automotive OEMs, incorporating advanced materials and sensor integration for real-time filter condition monitoring. This initiative is expected to enhance product offerings and reinforce DENSO’s competitive edge in the China diesel particulate filter market. Source: DENSO Corporate News.

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 5.12 Billion |

| CAGR | 12.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.1% |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | NGK Spark Plug Co., Ltd. (Japan), Corning Incorporated (United States), DENSO Corporation (Japan), Hengst SE (Germany), Umicore (Belgium), Clarios (United States), Yantai Wanhua Silicone Co., Ltd. (China), Zhejiang Zheneng New Energy Co., Ltd. (China), Shandong Sinocera Functional Material Co., Ltd. (China), Ningbo Jinhong Technology Co., Ltd. (China), BASF SE (Germany), Johnson Matthey Plc (United Kingdom), Tenneco Inc. (United States), Mann+Hummel GmbH (Germany), Faurecia S.A. (France), Eberspaecher Group (Germany), Hitachi Automotive Systems (Japan), Cummins Inc. (United States), BorgWarner Inc. (United States), Wanhua Chemical Group Co., Ltd. (China), Saint-Gobain S.A. (France), Cataler Corporation (Japan), Engelhard Corporation (United States), Ceres Power Holdings plc (United Kingdom), Hitachi Metals, Ltd (Japan) |

China Sic Diesel Particulate Filter Market - Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.