North America Targeted Cat Food Market Size, Growth & Revenue 2025-2034

North America Targeted Cat Food Market is segmented by Product Type (Dry Food, Wet Food, Semi-Moist Food, Organic/Natural Food, Veterinary Prescription Diets), Application (Indoor Cats, Outdoor Cats, Kitten Nutrition, Senior Cats, Special Health Needs), Distribution Channel (Pet Specialty Stores, Supermarkets/Hypermarkets, Veterinary Clinics, Online Retailers), Packaging Format (Pouches, Cans, Bags, Trays), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Targeted Cat Food market is defined by its focus on specialized nutrition solutions tailored to distinct feline needs, including age-specific, lifestyle-based, and health-related formulations. It covers a diverse product portfolio comprising dry, wet, semi-moist, organic/natural, and veterinary prescription diets designed for indoor cats, outdoor cats, kittens, senior cats, and cats requiring special health attention. The end users primarily include pet owners, veterinary professionals, and pet specialty retailers. The value chain spans from ingredient sourcing and manufacturing to distribution through retail and e-commerce channels, emphasizing quality, safety, and nutritional efficacy. Market dynamics are influenced by trends such as pet humanization, increasing disposable incomes, and rising awareness of pet health, driving premiumization and innovation across product lines. The North American market is characterized by mature consumer bases in the United States and Canada, with Mexico exhibiting emerging growth potential due to urbanization and rising pet adoption rates.

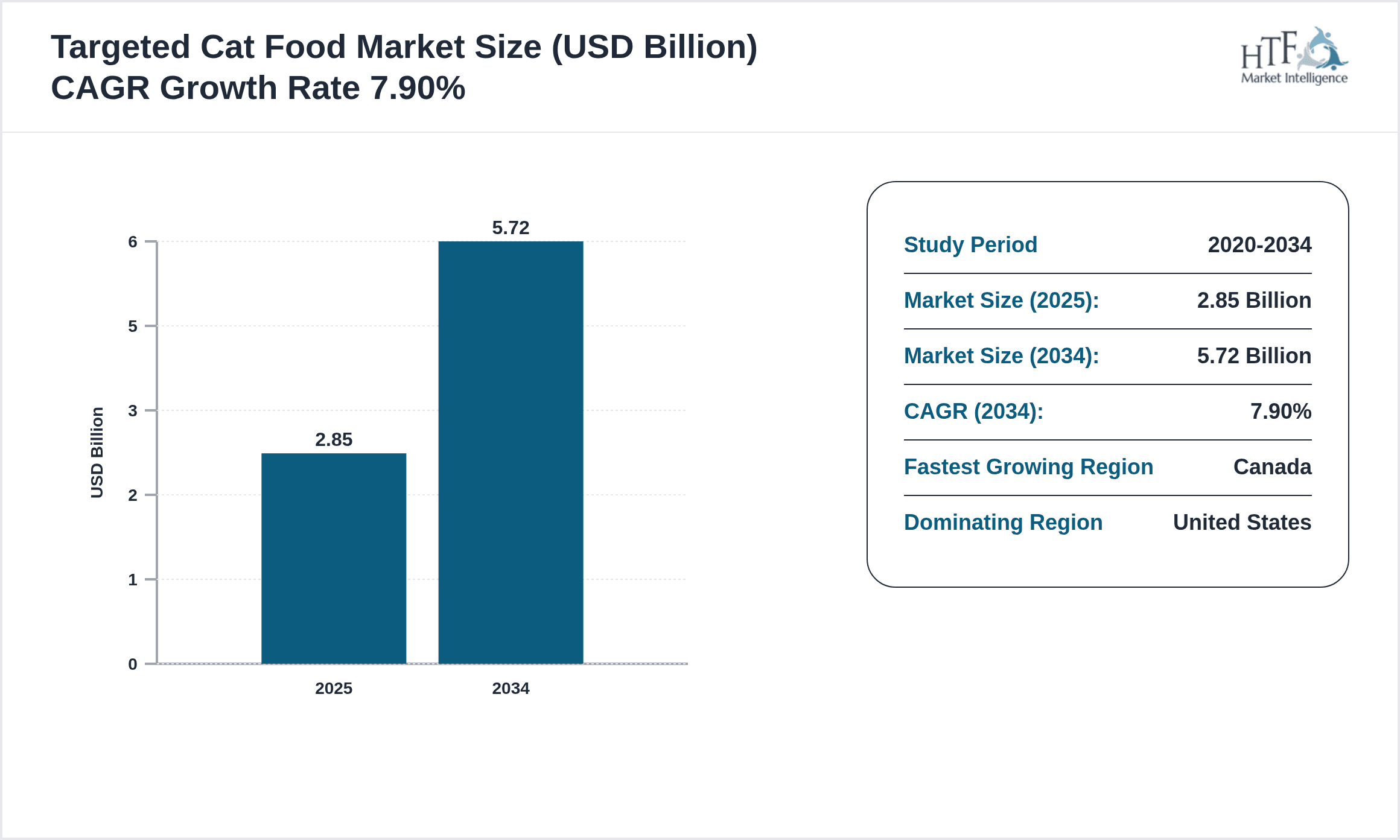

- •The market’s base size in 2025 is valued at USD 2.85 Billion, expanding robustly to an estimated USD 5.72 Billion by 2034, reflecting a CAGR of 7.9%. This growth trajectory is driven by factors including increased preference for organic and natural ingredients, a surge in demand for veterinary diets addressing chronic feline conditions, and expanding e-commerce penetration facilitating direct-to-consumer sales. Year-on-year growth rates remain steady around 7.6%, underpinned by consistent consumer spending and product innovation. The United States dominates the market with a 58% share, while Canada is the fastest growing with a CAGR of 9.1%, capitalizing on health-conscious consumer trends and premiumization.

- •North America’s targeted cat nutrition market presents substantial value propositions to pet food manufacturers, retailers, veterinarians, and consumers. It strategically aligns with growing health and wellness trends, sustainability focus, and advanced nutritional science. Stakeholders benefit from leveraging innovation in product formulations, enhanced ingredient transparency, and multi-channel distribution models to capture evolving consumer demands. The market’s growth potential is further amplified by demographic shifts, increasing pet ownership, and regulatory frameworks supporting pet food safety and quality. As such, the market is pivotal for companies aiming to consolidate leadership in the premium pet food segment within North America.

Competitive Landscape

The North America Targeted Cat Food market is highly competitive, characterized by the presence of multinational corporations, specialized regional players, and emerging niche brands. Market dynamics are shaped by product innovation with emphasis on health-specific formulations, ingredient transparency, and sustainability credentials. Leading companies employ diverse strategies including mergers and acquisitions, strategic partnerships, and expanding direct-to-consumer channels to strengthen market positioning. Innovation in organic and veterinary prescription diets is a key differentiator, fostering brand loyalty and premium pricing. Pricing strategies range from value-based offerings to ultra-premium segments, with distribution spanning mass retailers, specialty pet stores, veterinary clinics, and growing online platforms. Regulatory compliance and quality assurance serve as critical competitive barriers, while rapid consumer preference shifts challenge companies to maintain agility. Regional competition varies with the United States commanding the largest share, supported by mature retail infrastructure and consumer awareness, whereas Canada and Mexico exhibit dynamic growth driven by emerging consumer segments and adoption of novel products. Future competitive trends indicate increased digital engagement, personalized nutrition, and sustainability-focused product development as key factors defining market leadership.

Leading Companies in Targeted Cat Food Market

- •Nestlé Purina PetCare (United States)

- •Hill's Pet Nutrition (United States)

- •Blue Buffalo (United States)

- •Spectrum Brands Holdings (United States)

- •The J.M. Smucker Company (United States)

- •WellPet LLC (United States)

- •Champion Petfoods LP (Canada)

- •Big Heart Pet Brands (United States)

- •Natural Balance Pet Foods (United States)

- •Blue Ridge Beef (United States)

- •Diamond Pet Foods (United States)

- •Petcurean Pet Nutrition (Canada)

- •Tuffy's Pet Foods (United States)

- •Midwestern Pet Foods (United States)

- •Ainsworth Pet Nutrition (United States)

- •Central Garden & Pet Company (United States)

- •Nature's Variety (United States)

- •Canidae Corporation (United States)

- •Merrick Pet Care (United States)

- •Wellness Pet Food (United States)

- •Orijen (Canada)

- •Acana (Canada)

- •Solid Gold Pet (United States)

- •Farmina Pet Foods (United States)

- •Natural Planet Pet Foods (United States)

Market Breakdown

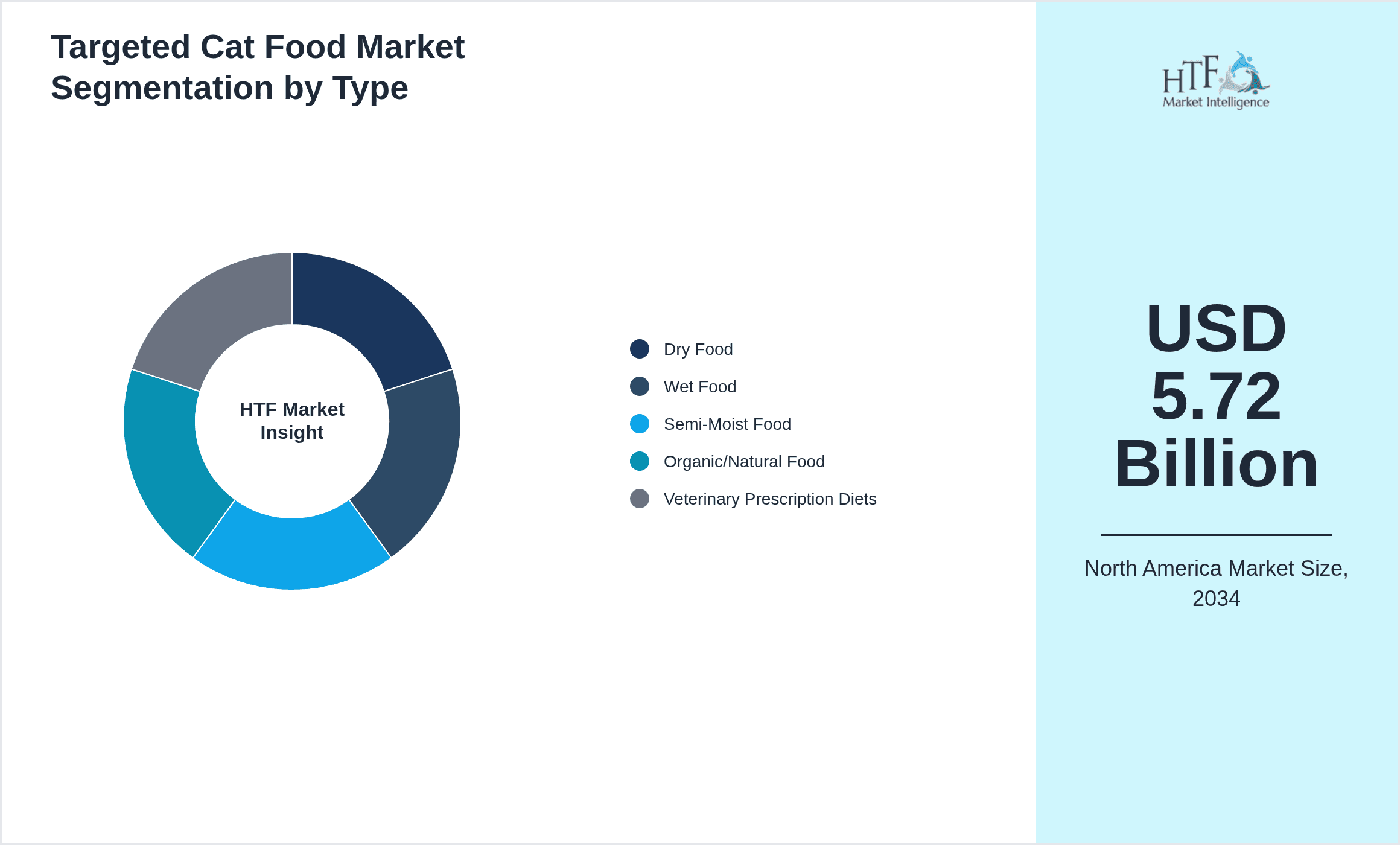

- •By Product Type

- ◦Dry Food

- ◦Wet Food

- ◦Semi-Moist Food

- ◦Organic/Natural Food

- ◦Veterinary Prescription Diets

- •By Application

- ◦Indoor Cats

- ◦Outdoor Cats

- ◦Kitten Nutrition

- ◦Senior Cats

- ◦Special Health Needs

- •By Distribution Channel

- ◦Pet Specialty Stores

- ◦Supermarkets/Hypermarkets

- ◦Veterinary Clinics

- ◦Online Retailers

- •By Packaging Format

- ◦Pouches

- ◦Cans

- ◦Bags

- ◦Trays

Growth Dynamics

- •The North America targeted cat food market growth is driven by increasing pet humanization, where cat owners seek premium nutrition options that mirror human health trends. This shift has led to rising demand for organic and natural ingredient-based cat foods that promise higher quality and safety standards.

- •Veterinary prescription diets are gaining traction due to rising awareness of feline chronic health conditions such as kidney disease and obesity. This specialized segment is supported by veterinary endorsements and targeted formulations, boosting market growth significantly.

- •E-commerce expansion has revolutionized product accessibility, with online retail channels offering convenience, wider product ranges, and subscription services, thereby driving increased consumer adoption and repeat purchases in the targeted cat food segment.

- •Rising disposable incomes coupled with increasing pet ownership rates in North America, particularly among millennials and urban households, contribute to sustained demand growth for premium and specialized cat food products.

- •Innovation in ingredient sourcing, including the incorporation of superfoods, probiotics, and functional additives, is creating differentiation opportunities and attracting health-conscious consumers seeking enhanced benefits for their cats.

- •Environmental and sustainability concerns are influencing product development, with companies focusing on eco-friendly packaging and sustainable ingredient sourcing, appealing to environmentally aware consumers and supporting market expansion.

- •Strategic initiatives such as partnerships between pet food manufacturers and veterinary institutions facilitate the development of clinically validated products, reinforcing consumer trust and driving higher market penetration.

Market Trends

- •Organic and natural targeted cat food products have witnessed a surge in popularity, propelled by consumer preference for clean-label and non-GMO ingredients, impacting product portfolios across leading brands.

- •Subscription-based e-commerce models are transforming the pet food distribution landscape, offering convenience and personalized nutrition plans, thereby enhancing customer retention and recurring revenue streams.

- •Increasing integration of pet nutrition with health monitoring technologies, such as smart feeders and health tracking apps, is emerging as a trend that aligns diet with individual cat health profiles.

- •Sustainability initiatives including recyclable packaging and ethical ingredient sourcing are becoming integral to brand value propositions, responding to growing consumer environmental consciousness.

- •Premiumization continues as a central theme, with consumers willing to pay a premium for products offering functional benefits like digestive health, weight management, and joint support tailored to cat life stages.

- •Collaborations between pet food companies and veterinary professionals are increasing, facilitating the co-development of therapeutic diets and enhancing market credibility.

- •The rise of plant-based and alternative protein sources in cat food formulations reflects innovation aimed at sustainability and allergen reduction, gaining traction among niche consumer segments.

Market Opportunities

- •Expanding the organic and natural product lines offers significant growth potential, capitalizing on the increasing consumer demand for clean-label and health-focused cat food options in North America.

- •Growth in veterinary prescription diets presents opportunities for companies to collaborate with veterinary professionals to develop tailored formulations addressing specific feline health issues.

- •E-commerce platform expansion and digital marketing enable manufacturers to reach niche consumer segments efficiently, enhancing brand visibility and facilitating direct consumer engagement.

- •Innovation in sustainable packaging and ingredient sourcing can differentiate products and attract environmentally conscious consumers, aligning with broader sustainability trends in the pet food industry.

- •Geographic expansion into underpenetrated markets within North America, such as Mexico, driven by rising urbanization and pet adoption rates, offers untapped revenue streams.

- •Personalized nutrition based on breed, age, and health condition represents a future growth avenue, leveraging data analytics and consumer insights to deliver customized cat food solutions.

- •Strategic acquisitions and partnerships with ingredient innovators and technology providers can accelerate product development and market penetration in the targeted cat food segment.

Market Challenges

- •High costs associated with premium ingredient sourcing and formulation development create pricing pressures that may limit accessibility for price-sensitive consumer segments.

- •Stringent regulatory compliance and quality assurance requirements increase operational complexity and costs for manufacturers, particularly in veterinary prescription diets.

- •Intense competition from both established multinational brands and emerging local players challenges market share retention and necessitates continuous innovation.

- •Supply chain disruptions, including raw material shortages and logistical constraints, can impact product availability and increase costs.

- •Consumer skepticism regarding health claims and ingredient authenticity requires transparent communication and rigorous product testing to maintain trust.

- •Limited consumer awareness in emerging markets such as Mexico poses obstacles to market penetration and necessitates focused educational campaigns.

- •Balancing sustainability goals with cost-effectiveness in packaging and sourcing remains a complex challenge for manufacturers aiming to meet consumer expectations.

Regulatory Framework

- •The FDA's Food Safety Modernization Act (FSMA), enforced between 2011 and 2025, mandates rigorous preventive controls and sanitation standards for pet food manufacturers, enhancing product safety and traceability within North America.

- •The Association of American Feed Control Officials (AAFCO) sets nutrient profile guidelines and ingredient definitions that govern pet food labeling and formulation, ensuring consumer protection and industry standardization across the United States and Canada.

- •Canada’s Safe Food for Canadians Regulations (SFCR), implemented by the Canadian Food Inspection Agency between 2018 and 2025, imposes licensing, traceability, and preventive control requirements on pet food businesses, harmonizing safety protocols with international standards.

- •Mexico’s NOM-051-SCFI/SSA1-2010 regulation on labeling requirements for pet food products enforces clear ingredient disclosure and nutritional information, supporting consumer transparency and market integrity.

- •Emerging regulations focused on sustainability and environmental impact are prompting manufacturers to adopt eco-friendly packaging and sustainable ingredient sourcing practices, aligning with North American policy trends and consumer expectations.

Market Intelligence

- •15th February 2025, Nestlé Purina PetCare announced the launch of a new organic line of targeted cat food products designed to address digestive health and immunity. The line features non-GMO, grain-free ingredients and incorporates superfoods such as pumpkin and turmeric, targeting health-conscious consumers across the United States and Canada. This initiative reflects growing demand for natural pet nutrition and aligns with Nestlé Purina’s sustainability commitments. The new range is available through e-commerce platforms and specialty pet stores, aiming to enhance market share in the premium segment. Source: Nestlé Purina official press release.

- •10th May 2025, Blue Buffalo introduced a veterinary prescription diet specifically formulated for cats with chronic kidney disease. Employing advanced nutritional science, the product offers controlled phosphorus levels and enhanced omega fatty acids. The launch was supported by partnerships with veterinary clinics across North America to facilitate clinical trials and professional endorsements. This product expansion strengthens Blue Buffalo’s position in the therapeutic pet food category, addressing a critical health need within the feline population. Source: Blue Buffalo corporate news.

- •23rd August 2025, Champion Petfoods LP announced a strategic partnership with a leading biotechnology firm to integrate probiotic and prebiotic blends into their organic cat food lines. This collaboration aims to improve gut health and nutrient absorption in cats, leveraging cutting-edge microbiome research. The initiative is expected to enhance product efficacy and consumer trust, reinforcing Champion Petfoods’ commitment to innovation and natural nutrition. Market analysts anticipate increased competitive pressure in the organic segment due to this development. Source: Champion Petfoods investor relations.

- •5th November 2024, WellPet LLC completed the acquisition of a regional natural pet food manufacturer in Mexico, expanding its footprint in the underpenetrated Mexican market. This acquisition is part of WellPet’s growth strategy to capitalize on rising urbanization and pet ownership trends in Latin America. The deal includes integration of sustainable packaging technologies and enhanced distribution networks, positioning WellPet for accelerated market entry and revenue growth. Industry observers view this as a significant consolidation move within North America’s targeted cat food landscape. Source: WellPet official announcement.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.85 Billion |

| Forecast Year Market Size | USD 5.72 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Product Type (Dry Food, Wet Food, Semi-Moist Food, Organic/Natural Food, Veterinary Prescription Diets), Application (Indoor Cats, Outdoor Cats, Kitten Nutrition, Senior Cats, Special Health Needs), Distribution Channel (Pet Specialty Stores, Supermarkets/Hypermarkets, Veterinary Clinics, Online Retailers), Packaging Format (Pouches, Cans, Bags, Trays) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Nestlé Purina PetCare (United States), Hill's Pet Nutrition (United States), Blue Buffalo (United States), Spectrum Brands Holdings (United States), The J.M. Smucker Company (United States), WellPet LLC (United States), Champion Petfoods LP (Canada), Big Heart Pet Brands (United States), Natural Balance Pet Foods (United States), Blue Ridge Beef (United States), Diamond Pet Foods (United States), Petcurean Pet Nutrition (Canada), Tuffy's Pet Foods (United States), Midwestern Pet Foods (United States), Ainsworth Pet Nutrition (United States), Central Garden & Pet Company (United States), Nature's Variety (United States), Canidae Corporation (United States), Merrick Pet Care (United States), Wellness Pet Food (United States), Orijen (Canada), Acana (Canada), Solid Gold Pet (United States), Farmina Pet Foods (United States), Natural Planet Pet Foods (United States) |

North America Targeted Cat Food Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Market market is expected to see significant growth and value in 2025.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.