United Kingdom Mugwort Pollen and Allergies Therapeutics Drug Market Size, Growth & Revenue 2025-2034

United Kingdom Mugwort Pollen and Allergies Therapeutics Drug Market is segmented by Therapeutic Drug Type (Antihistamines, Corticosteroids, Leukotriene Receptor Antagonists, Mast Cell Stabilizers, Immunomodulators), Treatment Application (Symptomatic Relief, Immunotherapy, Preventive Treatment, Emergency Treatment, Diagnostics), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics), Formulation Type (Oral Tablets, Nasal Sprays, Injectables, Topical Applications), and Geography (England, Scotland, Wales, Northern Ireland)

Pricing

Report Overview

Executive Summary

- •The United Kingdom Mugwort Pollen and Allergies Therapeutics Drug Market comprises a broad spectrum of pharmaceutical products aimed at mitigating allergic reactions caused by mugwort pollen. These include antihistamines, corticosteroids, leukotriene receptor antagonists, mast cell stabilizers, and immunomodulators, which serve to relieve symptoms, provide immunotherapy, and offer preventive and emergency treatment options. The market caters to various applications such as symptomatic relief, immunotherapy, preventive care, emergency interventions, and diagnostic support for allergic rhinitis and asthma induced by mugwort pollen exposure. End users primarily include hospitals, allergy clinics, specialty care centers, and outpatient facilities, supported by a comprehensive value chain from R&D through to distribution and retail. The market growth is fueled by increasing prevalence of mugwort pollen allergies in the UK, rising awareness of allergy management, and innovations in biologic therapies and immunomodulatory treatments. The regulatory landscape, healthcare infrastructure, and patient access within the UK uniquely shape market dynamics, alongside evolving epidemiological patterns. Strategic importance lies in addressing the unmet needs for effective, targeted allergy therapeutics to improve patient quality of life and reduce healthcare burden.

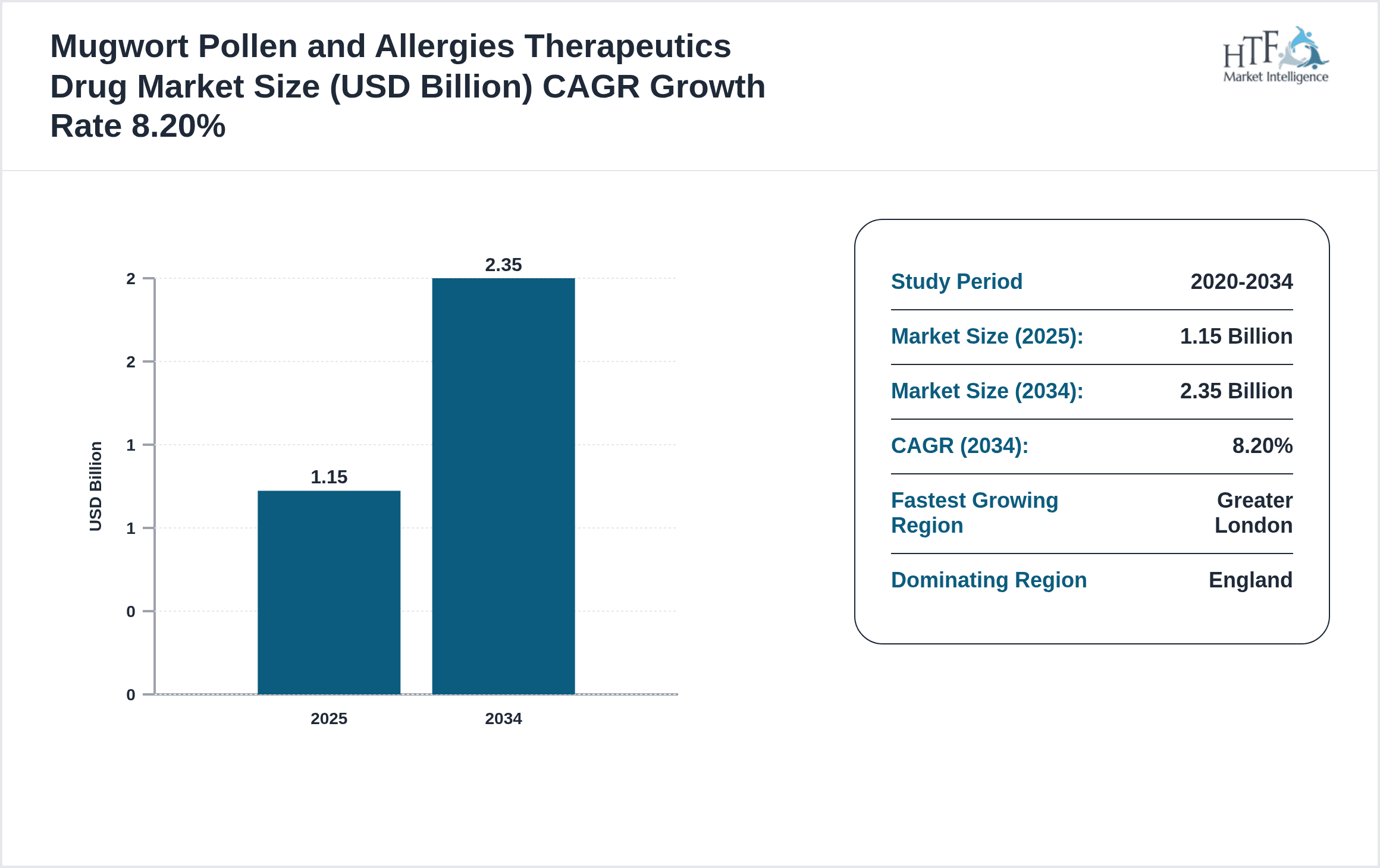

- •Key market highlights include a base market size of USD 1.15 Billion in 2025 with a forecast to reach USD 2.35 Billion by 2034, reflecting a robust CAGR of 8.2%. The dominant product segment is antihistamines, while immunomodulators represent the fastest growing drug type. Regionally, England leads market share, whereas Greater London exhibits the highest growth trajectory driven by urbanization and healthcare access. Year-on-year growth approximates 8.0%, underscoring steady demand expansion supported by increasing allergy incidence and therapeutic innovations.

- •The market’s value proposition is anchored in providing effective and accessible therapeutics for mugwort pollen allergies, addressing a growing patient population in the UK. It holds strategic importance for pharmaceutical companies, healthcare providers, and policymakers aiming to enhance allergy management and reduce associated healthcare costs. Innovations in drug formulations and immunotherapy techniques present opportunities for differentiation and improved patient outcomes, while regulatory compliance and reimbursement frameworks shape market access and growth potential.

Competitive Landscape

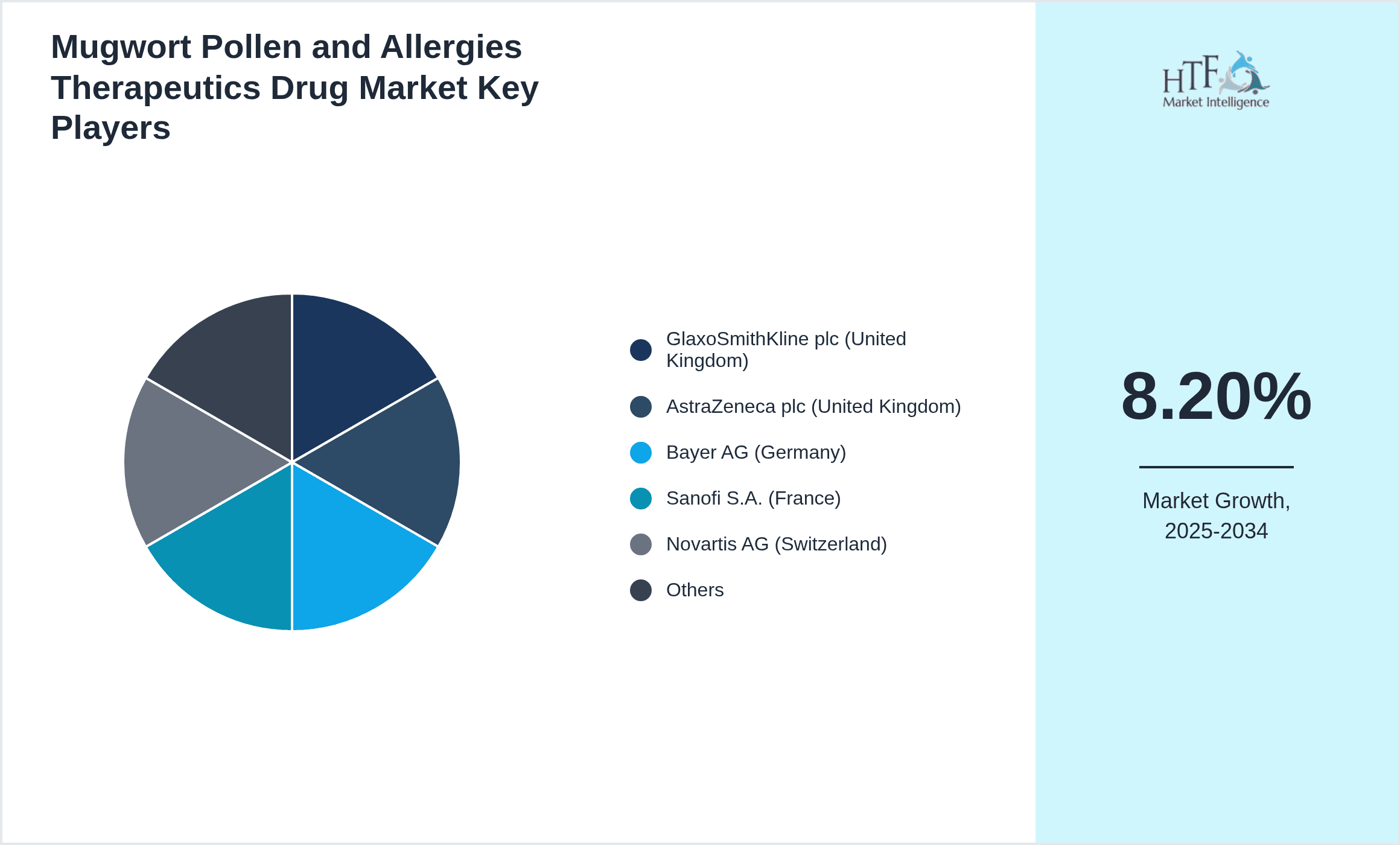

The competitive environment in the United Kingdom Mugwort Pollen and Allergies Therapeutics Drug Market is characterized by a diverse mix of multinational pharmaceutical corporations and specialized biotech firms focusing on allergy therapeutics. Competitive strategies predominantly revolve around innovation in drug formulation, development of novel immunotherapies, strategic partnerships, and acquisition of smaller players to enhance market presence. Companies emphasize differentiation through efficacy, safety profiles, and delivery mechanisms to capture patient and physician preference. Pricing strategies balance affordability with premium biologics offerings, while distribution channels leverage established hospital networks and retail pharmacies to maximize reach. Regulatory compliance and rapid adoption of cutting-edge technologies remain critical factors influencing market positioning. Furthermore, M&A activity serves as a key driver for consolidation, enabling expansion of product pipelines and geographic footprint. The market faces moderate entry barriers due to strict regulatory standards and high R&D costs, yet opportunities exist for niche players with innovative therapeutics. Regional competition is intensified by localized healthcare policies and population density variances. Anticipated future trends include increased focus on personalized medicine, digital health integrations for allergy management, and expansion of immunomodulatory treatments, shaping a dynamic competitive landscape.

Leading Companies in Mugwort Pollen and Allergies Therapeutics Drug Market

- •GlaxoSmithKline plc (United Kingdom)

- •AstraZeneca plc (United Kingdom)

- •Bayer AG (Germany)

- •Sanofi S.A. (France)

- •Novartis AG (Switzerland)

- •Pfizer Inc. (United States)

- •Johnson & Johnson (United States)

- •Teva Pharmaceutical Industries Ltd. (Israel)

- •Meda AB (Sweden)

- •Chiesi Farmaceutici S.p.A. (Italy)

- •ALK-Abelló A/S (Denmark)

- •Stallergenes Greer (France)

- •Mylan N.V. (United States)

- •Fresenius Kabi AG (Germany)

- •Regeneron Pharmaceuticals, Inc. (United States)

- •Boehringer Ingelheim GmbH (Germany)

- •Vifor Pharma Group (Switzerland)

- •Horizon Therapeutics plc (United States)

- •Mallinckrodt Pharmaceuticals (United States)

- •UCB S.A. (Belgium)

- •Lofarma S.p.A. (Italy)

- •Circassia Pharmaceuticals plc (United Kingdom)

- •Meda Pharma GmbH & Co. KG (Germany)

- •Cipla Limited (India)

- •Bausch Health Companies Inc. (Canada)

Market Breakdown

- •By Therapeutic Drug Type

- ◦Antihistamines

- ◦Corticosteroids

- ◦Leukotriene Receptor Antagonists

- ◦Mast Cell Stabilizers

- ◦Immunomodulators

- •By Treatment Application

- ◦Symptomatic Relief

- ◦Immunotherapy

- ◦Preventive Treatment

- ◦Emergency Treatment

- ◦Diagnostics

- •By Distribution Channel

- ◦Hospital Pharmacies

- ◦Retail Pharmacies

- ◦Online Pharmacies

- ◦Specialty Clinics

- •By Formulation Type

- ◦Oral Tablets

- ◦Nasal Sprays

- ◦Injectables

- ◦Topical Applications

Growth Dynamics

- •Increasing prevalence of mugwort pollen allergies in the UK due to climatic changes and urban pollution is significantly driving demand for effective therapeutics, expanding the patient base year-over-year.

- •Advancements in immunotherapy and biologic treatments provide enhanced efficacy and safety profiles, encouraging greater adoption among healthcare providers and patients seeking long-term allergy management.

- •Government initiatives and healthcare policies supporting allergy diagnosis and treatment accessibility stimulate market growth by improving patient outreach and reimbursement frameworks.

- •Rising public awareness and education campaigns around allergy symptoms and management are boosting early diagnosis rates and therapeutic intervention uptake across the UK.

- •Investment in pharmaceutical R&D focused on novel immunomodulators and combination therapies opens new avenues for market expansion and competitive differentiation.

- •Expansion of retail and online pharmacy channels enhances drug accessibility and convenience, supporting sustained market growth through improved patient adherence.

- •Collaborative partnerships between pharma companies and healthcare providers enable integrated allergy care solutions, fostering innovation and market penetration.

Market Trends

- •The growing shift towards personalized medicine in allergy therapeutics is driving development of tailored treatment regimens based on patient-specific allergen sensitivities and genetic profiles.

- •Increasing integration of digital health tools and mobile applications for allergy symptom tracking and management is enhancing patient engagement and treatment adherence.

- •The rising adoption of sublingual immunotherapy (SLIT) as a non-invasive alternative to traditional allergy shots is gaining traction due to improved patient compliance and safety.

- •Sustainability considerations in pharmaceutical manufacturing and packaging are influencing product development, with eco-friendly initiatives becoming a competitive differentiator.

- •Collaborations between biotech startups and established pharma players are accelerating innovation pipelines, particularly in novel biologics targeting allergic inflammation pathways.

- •Market segmentation based on severity of allergy symptoms is enabling more precise targeting of therapeutics across mild, moderate, and severe patient cohorts.

- •Enhanced regulatory support for accelerated approval pathways is facilitating faster market entry for breakthrough allergy therapeutics in the UK.

Market Opportunities

- •Development of next-generation immunomodulators with improved efficacy and reduced side effects presents substantial opportunities to capture unmet needs in severe mugwort pollen allergy cases.

- •Expansion into underserved regional zones within the UK, such as Wales and Northern Ireland, offers growth potential by improving therapeutic access and awareness.

- •Innovations in drug delivery systems, including needle-free injectables and extended-release formulations, can enhance patient convenience and adherence rates.

- •Strategic collaborations with allergy diagnostic companies to bundle therapies with advanced testing solutions may strengthen market differentiation and customer loyalty.

- •Leveraging telemedicine platforms for remote allergy management and consultation can tap into growing digital health adoption trends across the UK.

- •Government incentives focused on chronic disease management provide funding opportunities for research and market expansion initiatives.

- •Rising consumer preference for natural and biopharmaceutical allergy remedies opens avenues for product portfolio diversification.

Market Challenges

- •High costs associated with biologic and immunomodulatory therapies limit patient accessibility and reimbursement coverage, constraining market penetration.

- •Stringent regulatory requirements and lengthy approval processes pose barriers to rapid introduction of innovative allergy therapeutics in the UK market.

- •Fragmented healthcare delivery and regional disparities in allergy diagnosis and treatment access create uneven market growth across UK zones.

- •Limited patient adherence due to treatment complexity and prolonged therapy durations hampers optimal therapeutic outcomes and market expansion.

- •Competition from over-the-counter allergy remedies and alternative medicine options challenges prescription drug uptake.

- •Supply chain disruptions and raw material shortages impact manufacturing continuity and product availability.

- •Lack of widespread public awareness about mugwort pollen allergens compared to more common allergens restricts early diagnosis and treatment demand.

Regulatory Framework

- •The UK Medicines and Healthcare products Regulatory Agency (MHRA) implemented the Human Medicines Regulations 2012 (amended 2020-2025), mandating stringent safety and efficacy evaluations for allergy therapeutics, ensuring patient safety and product quality.

- •Post-Brexit regulatory realignment since 2021 has introduced UK-specific approval pathways, requiring companies to obtain separate MHRA authorization for allergy drugs alongside EMA procedures, impacting market entry timelines.

- •The National Institute for Health and Care Excellence (NICE) guidelines updated between 2020-2025 emphasize cost-effectiveness and clinical efficacy criteria for reimbursement of allergy therapeutics within the NHS framework.

- •The UK government’s 2023 Allergy Strategy includes mandates for improved allergy care access and funding for immunotherapy research, fostering a supportive environment for therapeutic innovation and adoption.

- •Data protection and pharmacovigilance requirements under the UK GDPR and PV regulations ensure ongoing monitoring of allergy drug safety post-market authorization, reinforcing patient trust and compliance.

Market Intelligence

- •15th January 2025, GlaxoSmithKline plc announced the launch of a novel immunomodulator targeting mugwort pollen-induced allergic rhinitis, featuring enhanced efficacy and a favorable safety profile. The biologic aims to reduce symptom recurrence and improve quality of life for moderate-to-severe allergy sufferers. The product launch is supported by a comprehensive clinical trial program conducted across UK allergy centers, with strategic plans to expand into wider European markets. This innovation is expected to strengthen GSK's leadership in the allergy therapeutics space and meet rising patient demand. Source: GlaxoSmithKline Official Press Release

- •3rd March 2025, AstraZeneca plc introduced an advanced corticosteroid nasal spray formulated with proprietary delivery technology designed for rapid onset of action and prolonged symptom relief in mugwort pollen allergy patients. The product received MHRA approval after demonstrating superior performance in Phase III UK-based clinical studies. AstraZeneca plans extensive educational campaigns targeting allergy specialists and primary care physicians to accelerate adoption. This launch enhances AstraZeneca's portfolio and addresses a critical unmet need in allergy management. Source: AstraZeneca Corporate Communications

- •7th July 2025, Novartis AG announced a strategic partnership with a UK-based biotech firm specializing in allergen diagnostics to co-develop integrated therapy and testing solutions for mugwort pollen allergies. The collaboration aims to combine precision diagnostics with targeted immunotherapy to optimize patient outcomes. The partnership includes joint R&D funding and plans for pilot programs within UK allergy clinics. This initiative reflects growing industry focus on personalized medicine approaches in allergy therapeutics. Source: Novartis News Release

- •22nd September 2024, Circassia Pharmaceuticals plc completed acquisition of a local immunotherapy startup focused on innovative sublingual tablets for mugwort pollen allergy treatment. The acquisition enhances Circassia’s product pipeline and accelerates commercialization capabilities in the UK market. Circassia aims to leverage its established distribution network to maximize market penetration. This deal exemplifies consolidation trends within the allergy therapeutics sector, driving competitive advantage through innovation. Source: Circassia Pharmaceuticals Investor Relations

Regional Outlook

The England currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Greater London is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- England

- Scotland

- Wales

- Northern Ireland

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.15 Billion |

| Forecast Year Market Size | USD 2.35 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Therapeutic Drug Type (Antihistamines, Corticosteroids, Leukotriene Receptor Antagonists, Mast Cell Stabilizers, Immunomodulators), Treatment Application (Symptomatic Relief, Immunotherapy, Preventive Treatment, Emergency Treatment, Diagnostics), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics), Formulation Type (Oral Tablets, Nasal Sprays, Injectables, Topical Applications) |

| Regions Covered | England, Scotland, Wales, Northern Ireland |

| Key Companies | GlaxoSmithKline plc (United Kingdom), AstraZeneca plc (United Kingdom), Bayer AG (Germany), Sanofi S.A. (France), Novartis AG (Switzerland), Pfizer Inc. (United States), Johnson & Johnson (United States), Teva Pharmaceutical Industries Ltd. (Israel), Meda AB (Sweden), Chiesi Farmaceutici S.p.A. (Italy), ALK-Abelló A/S (Denmark), Stallergenes Greer (France), Mylan N.V. (United States), Fresenius Kabi AG (Germany), Regeneron Pharmaceuticals, Inc. (United States), Boehringer Ingelheim GmbH (Germany), Vifor Pharma Group (Switzerland), Horizon Therapeutics plc (United States), Mallinckrodt Pharmaceuticals (United States), UCB S.A. (Belgium), Lofarma S.p.A. (Italy), Circassia Pharmaceuticals plc (United Kingdom), Meda Pharma GmbH & Co. KG (Germany), Cipla Limited (India), Bausch Health Companies Inc. (Canada) |

United Kingdom Mugwort Pollen and Allergies Therapeutics Drug Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Market market is projected to grow at a steady CAGR from 2025 to 2030, driven by increasing demand and expansion in various applications.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.