EMEA LDPE Shrink Film Market Size, Growth & Revenue 2024-2034

EMEA LDPE Shrink Film Market is segmented by LDPE Shrink Film Type (Cast LDPE Shrink Film, Blown LDPE Shrink Film, Co-extruded LDPE Shrink Film, Laminated LDPE Shrink Film, Anti-fog LDPE Shrink Film), Application (Packaging, Food & Beverage, Consumer Goods, Pharmaceuticals, Industrial), End-Use Industry (Food Processing & Packaging, Pharmaceutical Manufacturing, Retail & Logistics, Electronics & Consumer Durables), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail, Specialty Packaging Suppliers), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA LDPE Shrink Film Market is a dynamic sector characterized by the production and utilization of specialized low-density polyethylene films designed for shrink packaging applications. These films are integral in various industries including packaging for food and beverages, pharmaceuticals, consumer goods, and industrial products, offering protection, tamper resistance, and enhanced product presentation. The market covers multiple LDPE shrink film types such as cast, blown, co-extruded, laminated, and anti-fog films, each tailored to meet diverse application needs and regulatory compliance within the EMEA region. This region comprises economically developed markets like Germany, France, and the UK, as well as emerging markets in Central and Eastern Europe and the Middle East & Africa, offering vast growth potential. Key drivers include increasing demand for sustainable packaging solutions, technological advancements in film production, and stringent food safety regulations. The market is shaped by competitive innovations, mergers and acquisitions, and evolving consumer preferences, positioning it as a vital segment within the broader plastic packaging industry in EMEA.

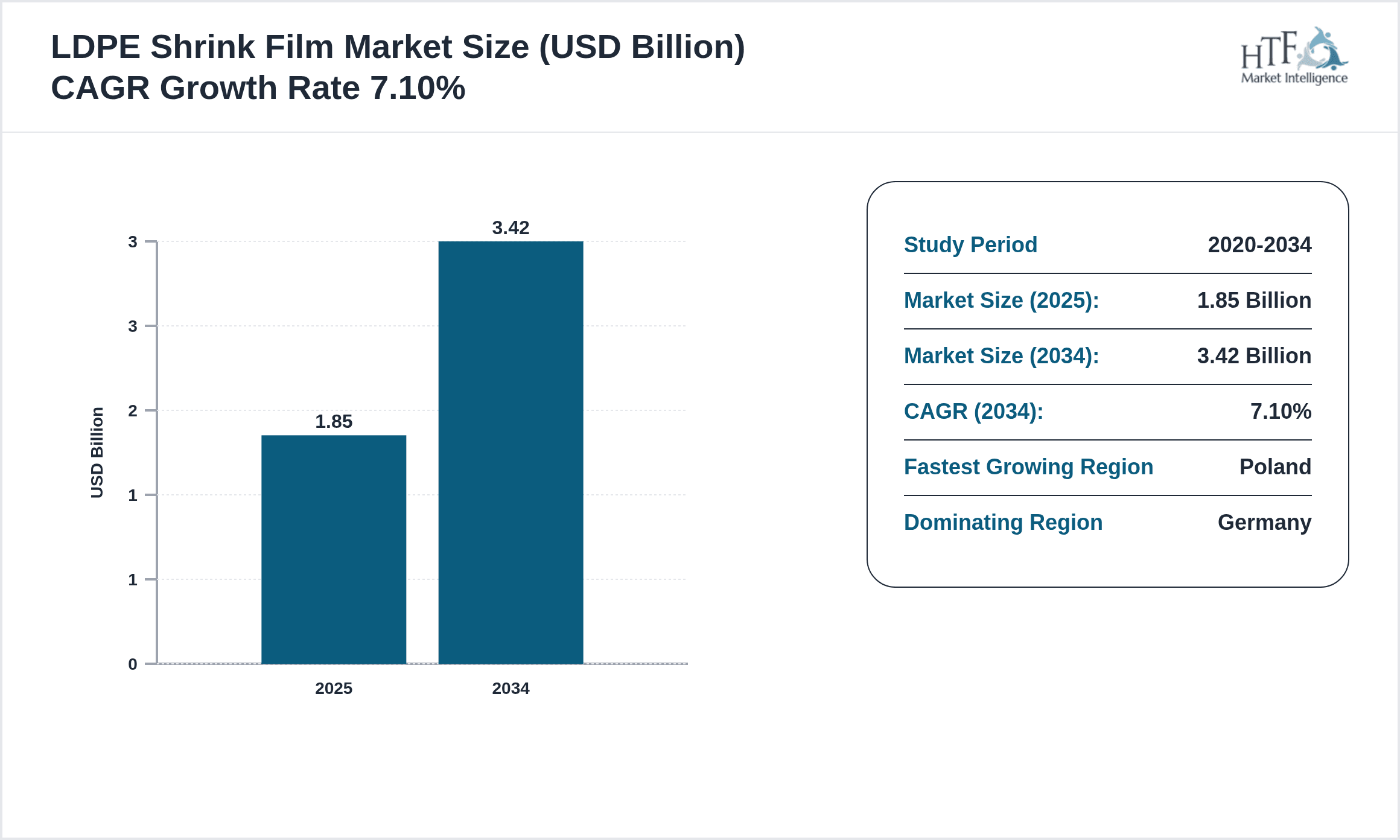

- •Significant market highlights include a projected compound annual growth rate (CAGR) of 7.1% between 2025 and 2034, with the market size expected to reach USD 3.42 billion by 2034 from USD 1.85 billion in 2025. Germany leads as the dominating country, accounting for 22% market share driven by its robust manufacturing and packaging sectors. Poland emerges as the fastest-growing market within EMEA with a CAGR of 9.3%, reflecting rising industrialization and packaging innovations. Cast LDPE shrink film remains the dominant product type due to its excellent clarity and strength, while anti-fog LDPE shrink films are the fastest-growing segment, propelled by increasing demand in the fresh food packaging sector. Packaging applications dominate consumption, benefiting from strong demand across food, beverage, and consumer goods industries. The market growth is further bolstered by adoption of eco-friendly materials and advanced production techniques.

- •The EMEA LDPE Shrink Film Market offers substantial value propositions to stakeholders including manufacturers, packaging companies, and end-users by facilitating innovative, cost-effective, and environmentally compliant packaging solutions. This market supports extended product shelf life, reduces waste, and enhances logistical efficiencies, making it strategically important for food safety and retail sectors. Companies operating in this market benefit from technological advances in film extrusion, coating, and recycling processes that address sustainability mandates. Furthermore, the rising consumer demand for aesthetically appealing and protective packaging fuels continuous product development. The market’s strategic importance is amplified by regulatory frameworks encouraging reduced plastic footprint and circular economy models across EMEA, fostering innovation and competitive differentiation. Consequently, the sector remains a key driver for packaging industry evolution in Europe, the Middle East, and Africa.

Competitive Landscape

The competitive landscape of the EMEA LDPE Shrink Film Market is marked by intense rivalry among global and regional manufacturers striving for technological leadership and market share expansion. Companies focus heavily on innovation in film compositions, such as multilayer co-extrusions and anti-fog coatings, to meet stringent environmental and functional requirements. Strategic partnerships and mergers have become essential to consolidate supply chains and enhance production capabilities. Market players differentiate themselves through customization, quality certifications, and value-added services including sustainable packaging solutions. Pricing strategies are influenced by raw material volatility and regulatory pressures to reduce carbon footprints, compelling firms to optimize operations. Distribution channels are diversified, with a strong presence in both direct sales to large industrial customers and through specialized distributors for SMEs. The market entry barriers include high capital requirements and compliance with evolving regional regulations. Overall, the competitive environment fosters continuous innovation, efficiency improvements, and sustainability initiatives, shaping the future trajectory of the EMEA LDPE shrink film sector.

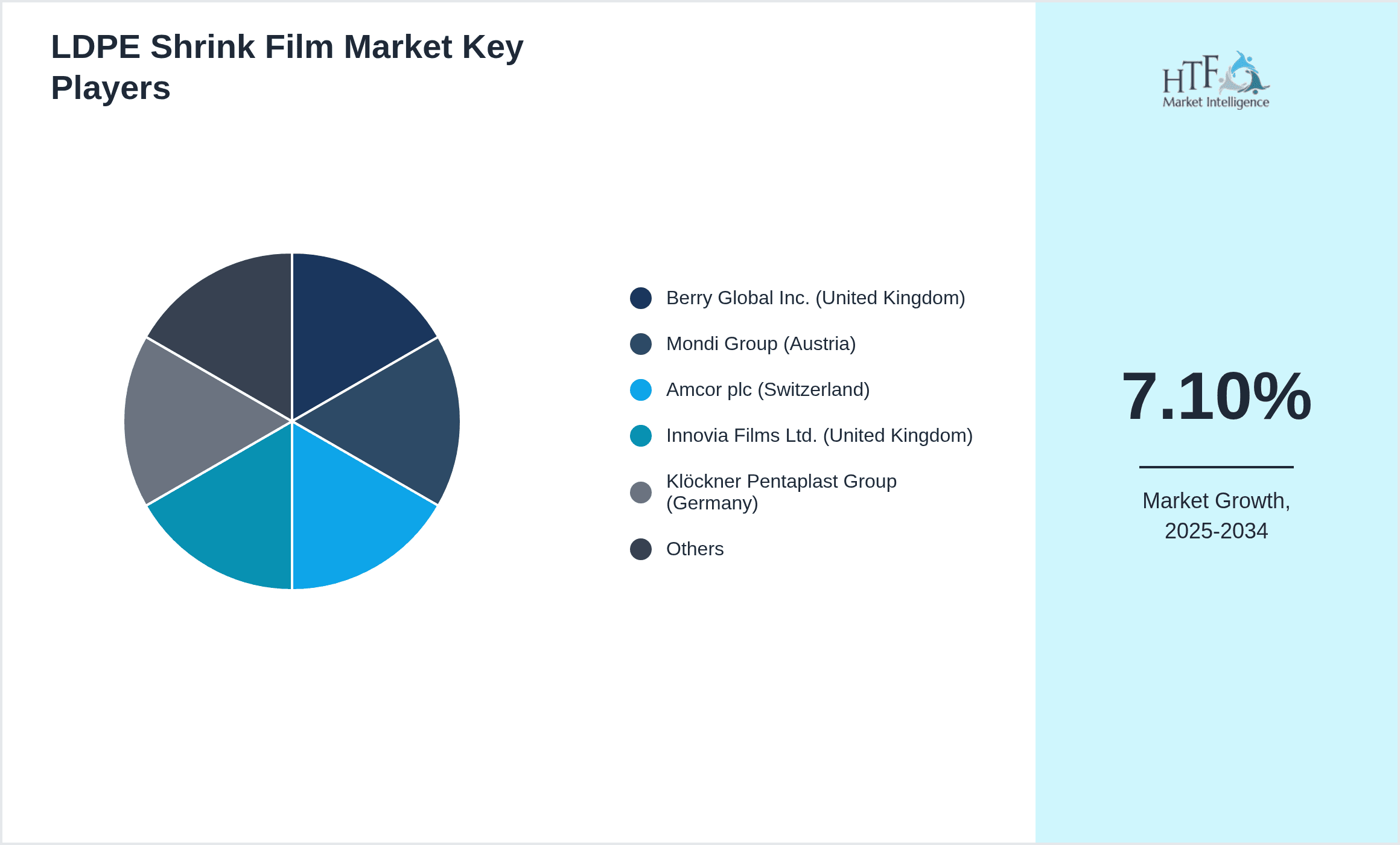

Leading Companies in EMEA LDPE Shrink Film Market

- •Berry Global Inc. (United Kingdom)

- •Mondi Group (Austria)

- •Amcor plc (Switzerland)

- •Innovia Films Ltd. (United Kingdom)

- •Klöckner Pentaplast Group (Germany)

- •Borealis AG (Austria)

- •Wipak Group (Finland)

- •FlexFilms Europe Ltd. (Netherlands)

- •Sealed Air Corporation (Ireland)

- •Plastika Kritis (Greece)

- •Coveris Holdings S.A. (Austria)

- •Constantia Flexibles (Austria)

- •Albis Plastic GmbH (Germany)

- •UPM Raflatac (Finland)

- •Jindal Poly Films Limited (UK Subsidiary)

- •Südpack Verpackungen GmbH (Germany)

- •Conitex Sonoco (France)

- •Polifilm Extrusion GmbH (Germany)

- •Grupo Gondi (Spain)

- •Flexopack S.A. (Greece)

- •Trioworld Group AB (Sweden)

- •Mitsui Chemicals Europe GmbH (Germany)

- •Nippon Gohsei Europe GmbH (Germany)

- •Klöckner Pentaplast Group (France)

- •Alpla Werke Alwin Lehner GmbH & Co KG (Austria)

Market Breakdown

- •By LDPE Shrink Film Type

- ◦Cast LDPE Shrink Film

- ◦Blown LDPE Shrink Film

- ◦Co-extruded LDPE Shrink Film

- ◦Laminated LDPE Shrink Film

- ◦Anti-fog LDPE Shrink Film

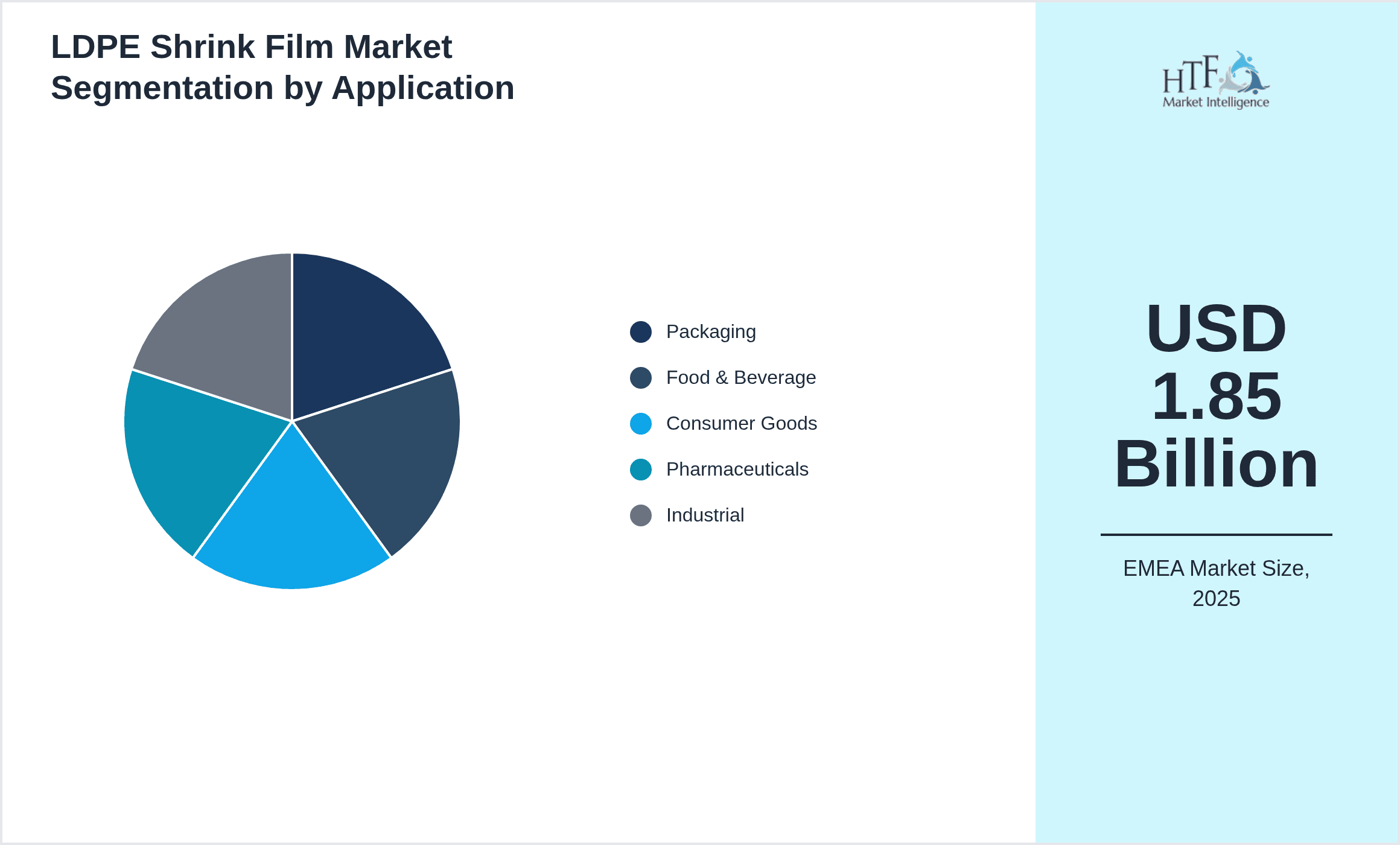

- •By Application

- ◦Packaging

- ◦Food & Beverage

- ◦Consumer Goods

- ◦Pharmaceuticals

- ◦Industrial

- •By End-Use Industry

- ◦Food Processing & Packaging

- ◦Pharmaceutical Manufacturing

- ◦Retail & Logistics

- ◦Electronics & Consumer Durables

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Retail

- ◦Specialty Packaging Suppliers

Growth Dynamics

- •The EMEA LDPE Shrink Film Market growth is primarily driven by the escalating demand for sustainable and efficient packaging solutions across food, pharmaceutical, and retail sectors. Increasing consumer awareness about product safety and packaging aesthetics is prompting manufacturers to adopt shrink films that extend shelf life and enhance presentation. Technological advancements in film extrusion and coating processes, such as multilayer and anti-fog technologies, are enhancing product performance and market appeal. Additionally, regulatory mandates aimed at reducing plastic waste encourage producers to innovate recyclable and biodegradable shrink films. The growth of e-commerce and logistics industries in the EMEA region further fuels demand due to the need for secure and tamper-evident packaging. These factors collectively provide a robust foundation for sustained market expansion over the forecast period.

- •Advancements in manufacturing techniques, including the transition from blown to cast film production, facilitate improved clarity and strength of LDPE shrink films, driving market preference towards cast films. The increasing use of co-extruded films enables multipurpose applications by combining barrier properties and mechanical strength, broadening the market scope. Growing investments in research and development by key players focus on enhancing film recyclability and reducing carbon footprint, aligning with the circular economy initiatives prevalent in EMEA. Furthermore, the expansion of organized retail and processed food sectors in emerging economies within the region stimulates demand for advanced shrink packaging solutions. These dynamics contribute to the evolving competitive landscape and increased adoption of LDPE shrink films.

- •The surge in demand for fresh and perishable food products in urban centers across EMEA necessitates packaging films with superior anti-fog and breathability features, boosting the anti-fog LDPE shrink film segment. Pharmaceutical companies increasingly rely on shrink films for secure packaging to prevent contamination and tampering, expanding application verticals. Additionally, the rise in consumer electronics and consumer durables requires protective shrink films to facilitate safe transportation. Strategic collaborations between film manufacturers and packaging converters enhance product customization capabilities, fostering growth. These developments underscore the market's responsiveness to evolving end-use requirements and technological innovations.

- •Emerging trends like the adoption of bio-based LDPE films and integration of nanotechnology for enhanced barrier properties represent significant growth opportunities. Government initiatives promoting sustainable packaging and banning single-use plastics encourage industry players to reformulate products. The growth of the circular economy and recycling infrastructure in Europe incentivizes manufacturers to produce shrink films compatible with existing recycling streams. Additionally, digitalization in supply chains enables better tracking and quality control of shrink film applications, improving efficiency. These factors collectively shape the market's future trajectory, emphasizing sustainability and innovation.

- •The increasing penetration of e-commerce across the EMEA region creates a substantial demand for protective and tamper-evident shrink packaging. Moreover, heightened consumer preference for environmentally friendly packaging stimulates the development and adoption of biodegradable and recyclable LDPE shrink films. The expansion of organized retail chains in Central and Eastern Europe provides new market avenues. Concurrently, the rise of private label brands necessitates customized shrink film solutions, fostering product differentiation. These market expansions highlight a shift towards customer-centric and sustainable packaging practices driving market growth.

Market Trends

- •The EMEA LDPE Shrink Film Market is witnessing a strong trend towards sustainability, with manufacturers increasingly offering recyclable and bio-based shrink films to comply with stringent environmental regulations. This shift is driven by consumer demand for eco-friendly packaging and government mandates across Europe aimed at reducing plastic waste, prompting innovation in film composition and processing.

- •Technological innovations such as multilayer co-extrusion and anti-fog coatings are enhancing functional properties of LDPE shrink films, improving clarity, strength, and breathability. These advances enable wider application in fresh food packaging and pharmaceuticals, influencing market dynamics and product development strategies.

- •Digitalization and automation in packaging lines are transforming shrink film application processes, improving operational efficiency and reducing material wastage. Industry players are investing in smart packaging technologies that integrate with shrink films to provide tamper evidence and supply chain traceability.

- •The rise of e-commerce has increased demand for secure, tamper-proof shrink packaging solutions, prompting manufacturers to develop films with enhanced mechanical properties and sealing capabilities to protect goods during transit and handling.

- •Collaborations between shrink film manufacturers and converters are fostering customized solutions tailored to specific end-user needs, enhancing product differentiation and customer satisfaction. This collaborative approach is becoming a key competitive advantage in the market.

- •Growing consumer preference for visually appealing and branded packaging is encouraging the integration of printing and labeling technologies with LDPE shrink films, expanding market opportunities in retail and consumer goods sectors.

- •Future market directions indicate increased focus on circular economy practices, with investments in recycling infrastructure and development of shrink films compatible with existing recycling streams, positioning sustainability at the core of industry evolution.

Market Opportunities

- •The expanding processed food and pharmaceutical sectors in emerging EMEA countries present significant growth opportunities for LDPE shrink film manufacturers. These sectors demand high-quality, compliant packaging films, creating new market segments. Additionally, the rising trend of sustainable packaging offers avenues for bio-based and recyclable film development, appealing to environmentally conscious consumers. Investment in R&D to innovate multi-functional shrink films with enhanced barrier and mechanical properties can open further application areas. Partnerships between film producers and brand owners can facilitate product customization, strengthening market presence. Geographic expansion into underpenetrated markets within Eastern Europe and the Middle East also offers promising potential. These opportunities encourage industry players to diversify their product portfolios and align offerings with evolving regulatory and consumer trends, driving long-term growth within the EMEA LDPE shrink film market.

- •The increasing adoption of e-commerce across EMEA escalates the demand for tamper-evident, high-performance protective packaging, representing a lucrative opportunity for shrink film manufacturers. Developing shrink films with advanced sealing and puncture resistance tailored for logistics applications can unlock new revenue streams. Furthermore, the integration of smart packaging technologies such as QR codes and RFID tags with shrink films offers prospects for enhanced product traceability and consumer engagement. The growing trend of private label brands also necessitates customized shrink packaging solutions, enabling differentiation and premiumization. These factors collectively foster innovation-driven growth and market expansion opportunities, encouraging strategic investments and collaborations within the sector.

- •Emerging environmental regulations mandating reduced plastic use and enhanced recyclability create a fertile landscape for innovation in biodegradable and compostable LDPE shrink films. Manufacturers investing in sustainable alternatives can capitalize on evolving consumer and regulatory demands. Expanding recycling infrastructure in Europe facilitates the adoption of circular economy models, further incentivizing green product development. Additionally, collaborations with waste management entities and policymakers can streamline compliance and market acceptance. These opportunities align with global sustainability goals, positioning companies for future growth and competitive advantage.

- •The diversification of shrink film applications beyond traditional packaging into sectors such as electronics, automotive, and industrial goods offers untapped market potential. Custom-engineered shrink films meeting sector-specific requirements, including enhanced durability and protective features, can drive incremental demand. Strategic partnerships with end-users to co-develop innovative solutions can accelerate market penetration. The convergence of technological advancements and market needs presents significant opportunities to broaden product offerings and revenue bases, fostering resilience and long-term sustainability.

- •Geographical expansion into Middle East and African markets, characterized by growing industrialization and urbanization, represents a significant opportunity for LDPE shrink film manufacturers. Rising consumer awareness and demand for packaged goods in these regions create a favorable environment for market entry and growth. Leveraging local partnerships and adapting products to regional preferences can facilitate successful penetration. These emerging markets offer high growth potential, balancing mature European markets and supporting overall EMEA market expansion.

Market Challenges

- •One of the primary challenges facing the EMEA LDPE Shrink Film Market is the stringent regulatory environment concerning plastic usage and waste management. Compliance with evolving European Union directives and national policies on single-use plastics and recyclability imposes significant operational constraints and cost pressures on manufacturers. These regulations necessitate continuous reformulation of products and investment in sustainable technologies, creating barriers for smaller players with limited resources.

- •Raw material price volatility, especially fluctuations in crude oil prices affecting LDPE resin costs, poses a substantial challenge to market stability and profitability. Such uncertainties complicate pricing strategies and supply chain management, potentially leading to margin erosion and supply disruptions. Manufacturers must adopt agile procurement and risk mitigation strategies to navigate these market conditions effectively.

- •The recycling and waste management infrastructure in parts of the EMEA region, particularly in Middle East and Africa, remains underdeveloped, hindering the adoption of circular economy models for LDPE shrink films. Limited recycling capabilities restrict the market penetration of recyclable and bio-based films, challenging sustainability efforts and regulatory compliance. This infrastructural gap requires coordinated industry and governmental actions to improve collection and processing systems.

- •Intense competition and market saturation in mature Western European countries limit growth prospects and pressure companies to differentiate through innovation and cost efficiency. The dominance of established players creates high entry barriers for new entrants, impacting market dynamics. Additionally, balancing cost competitiveness with quality and sustainability requirements poses ongoing challenges.

- •Technological limitations related to the scalability of bio-based and compostable LDPE shrink films restrict their widespread adoption. Challenges in achieving comparable performance to conventional films, alongside higher production costs, affect market acceptance. Continued research and development are needed to overcome these barriers and achieve commercial viability.

Regulatory Framework

- •Between 2020 and 2025, the European Union implemented the Single-Use Plastics Directive mandating reductions in specific plastic products, including shrink films, encouraging manufacturers to innovate recyclable and biodegradable alternatives. Compliance requirements include material labeling, waste collection targets, and restrictions on non-recyclable plastics, significantly impacting LDPE shrink film producers.

- •In 2023, REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) regulations were updated to include stricter controls on additives and plasticizers used in LDPE films, compelling manufacturers to reformulate products to meet safety and environmental standards. These changes affect raw material sourcing and production processes across EMEA.

- •Safety standards under the European Food Safety Authority (EFSA) require LDPE shrink films used in food packaging to meet rigorous migration limits and hygiene protocols, ensuring consumer protection. These regulations drive investment in quality assurance and certification processes, influencing market competitiveness.

- •Countries within the Middle East and Africa have increasingly adopted environmental regulations aligned with global sustainability goals, including extended producer responsibility (EPR) schemes and plastic waste reduction policies introduced between 2021 and 2024. These frameworks promote producer accountability and encourage sustainable packaging innovations.

- •Government initiatives such as the European Green Deal and Circular Economy Action Plan promote recycling infrastructure development and support for sustainable packaging materials, offering incentives and funding opportunities that benefit LDPE shrink film manufacturers investing in eco-friendly solutions.

Market Intelligence

- •15th March 2025, Mondi Group launched a new line of bio-based LDPE shrink films designed for food packaging applications in the EMEA region. This innovative product leverages renewable raw materials and offers enhanced recyclability without compromising film clarity or mechanical strength. The launch aligns with Mondi’s sustainability targets and European regulatory directives, positioning the company as a leader in eco-friendly packaging solutions. The new films are expected to capture significant market share from conventional LDPE films, addressing growing consumer demand for sustainable packaging. This development is anticipated to stimulate competitive responses and accelerate industry-wide adoption of green packaging technologies. Source: Mondi Official Press Release

- •10th January 2025, Berry Global Inc. expanded its production capacity for anti-fog LDPE shrink films at its European manufacturing facilities. This expansion responds to increased demand from the fresh produce and pharmaceutical sectors, where film clarity and moisture control are critical. The company invested in advanced extrusion and coating technologies to enhance product performance and reduce environmental impact. This strategic move strengthens Berry Global’s market position in EMEA and supports evolving customer requirements for high-performance sustainable packaging. The capacity increase is expected to improve supply chain responsiveness and reduce lead times. Source: Berry Global Corporate Announcement

- •22nd June 2025, Amcor plc announced a strategic partnership with a leading European recycling consortium to develop closed-loop recycling systems for LDPE shrink films. The initiative aims to enhance film collectability and recyclability, addressing regulatory pressures and consumer sustainability demands. Amcor will supply recyclable film products while collaborating on innovative sorting and processing technologies to improve recovery rates. This partnership is expected to set new industry standards for circular economy practices within EMEA and foster greater environmental responsibility across the packaging value chain. The collaboration leverages Amcor’s technical expertise and the consortium’s recycling infrastructure capabilities to drive systemic change. Source: Amcor Corporate News

- •5th April 2025, Klöckner Pentaplast Group introduced a next-generation co-extruded LDPE shrink film with integrated barrier properties for pharmaceutical packaging. The product offers superior protection against moisture and oxygen ingress, extending product shelf life and ensuring regulatory compliance. Developed through cutting-edge extrusion technology, this film meets stringent pharmaceutical industry standards and supports sustainable packaging initiatives by reducing material usage. The launch enhances Klöckner Pentaplast’s product portfolio and competitive differentiation in the EMEA market, addressing growing demand for high-performance, compliant shrink films. The new film is expected to gain rapid adoption across pharmaceutical manufacturers seeking reliable packaging solutions. Source: Klöckner Pentaplast Press Release

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Poland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 3.42 Billion |

| CAGR | 7.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by LDPE Shrink Film Type (Cast LDPE Shrink Film, Blown LDPE Shrink Film, Co-extruded LDPE Shrink Film, Laminated LDPE Shrink Film, Anti-fog LDPE Shrink Film), Application (Packaging, Food & Beverage, Consumer Goods, Pharmaceuticals, Industrial), End-Use Industry (Food Processing & Packaging, Pharmaceutical Manufacturing, Retail & Logistics, Electronics & Consumer Durables), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail, Specialty Packaging Suppliers) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Berry Global Inc. (United Kingdom), Mondi Group (Austria), Amcor plc (Switzerland), Innovia Films Ltd. (United Kingdom), Klöckner Pentaplast Group (Germany), Borealis AG (Austria), Wipak Group (Finland), FlexFilms Europe Ltd. (Netherlands), Sealed Air Corporation (Ireland), Plastika Kritis (Greece), Coveris Holdings S.A. (Austria), Constantia Flexibles (Austria), Albis Plastic GmbH (Germany), UPM Raflatac (Finland), Jindal Poly Films Limited (UK Subsidiary), Südpack Verpackungen GmbH (Germany), Conitex Sonoco (France), Polifilm Extrusion GmbH (Germany), Grupo Gondi (Spain), Flexopack S.A. (Greece), Trioworld Group AB (Sweden), Mitsui Chemicals Europe GmbH (Germany), Nippon Gohsei Europe GmbH (Germany), Klöckner Pentaplast Group (France), Alpla Werke Alwin Lehner GmbH & Co KG (Austria) |

EMEA LDPE Shrink Film Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.