China Chromatography Media for Biopharmaceutical Market - China Size & Outlook 2025-2034

China Chromatography Media for Biopharmaceutical Market is segmented by Type (Ion Exchange Chromatography Media, Affinity Chromatography Media, Size Exclusion Chromatography Media, Hydrophobic Interaction Chromatography Media, Mixed-mode Chromatography Media), Application (Monoclonal Antibodies Purification, Vaccines Purification, Recombinant Proteins Processing, Gene Therapy Vectors Purification, Cell Therapy Products Purification), End-User Facility (Biopharmaceutical Manufacturing Plants, Contract Development and Manufacturing Organizations (CDMOs), Research and Development Laboratories, Academic and Government Research Institutes), Distribution Channel (Direct Sales, Distributors and Resellers, E-commerce Platforms), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Chromatography Media for Biopharmaceutical Market is a pivotal segment within the country's expanding biopharmaceutical industry, focusing on chromatographic materials essential for the purification of complex biologics such as monoclonal antibodies, vaccines, recombinant proteins, gene therapy vectors, and cell therapy products. This market includes various chromatography media types like ion exchange, affinity, size exclusion, hydrophobic interaction, and mixed-mode chromatography, which are critical in downstream processing to achieve the high purity and quality required by stringent regulatory standards. The market’s scope spans from raw resin production to application in contract manufacturing organizations and research institutions engaged in biopharmaceutical development and commercialization. China's rapid biopharma growth, driven by increased domestic R&D investment, rising demand for biologics, and government initiatives promoting biotechnology innovation, fuels market expansion. Key use cases include improving process efficiency, yield, and scalability of purification steps, enabling biopharmaceutical manufacturers to meet both domestic and international quality requirements. As a result, the chromatography media market is integral to China’s ambition to become a global leader in biopharmaceutical manufacturing by 2034.

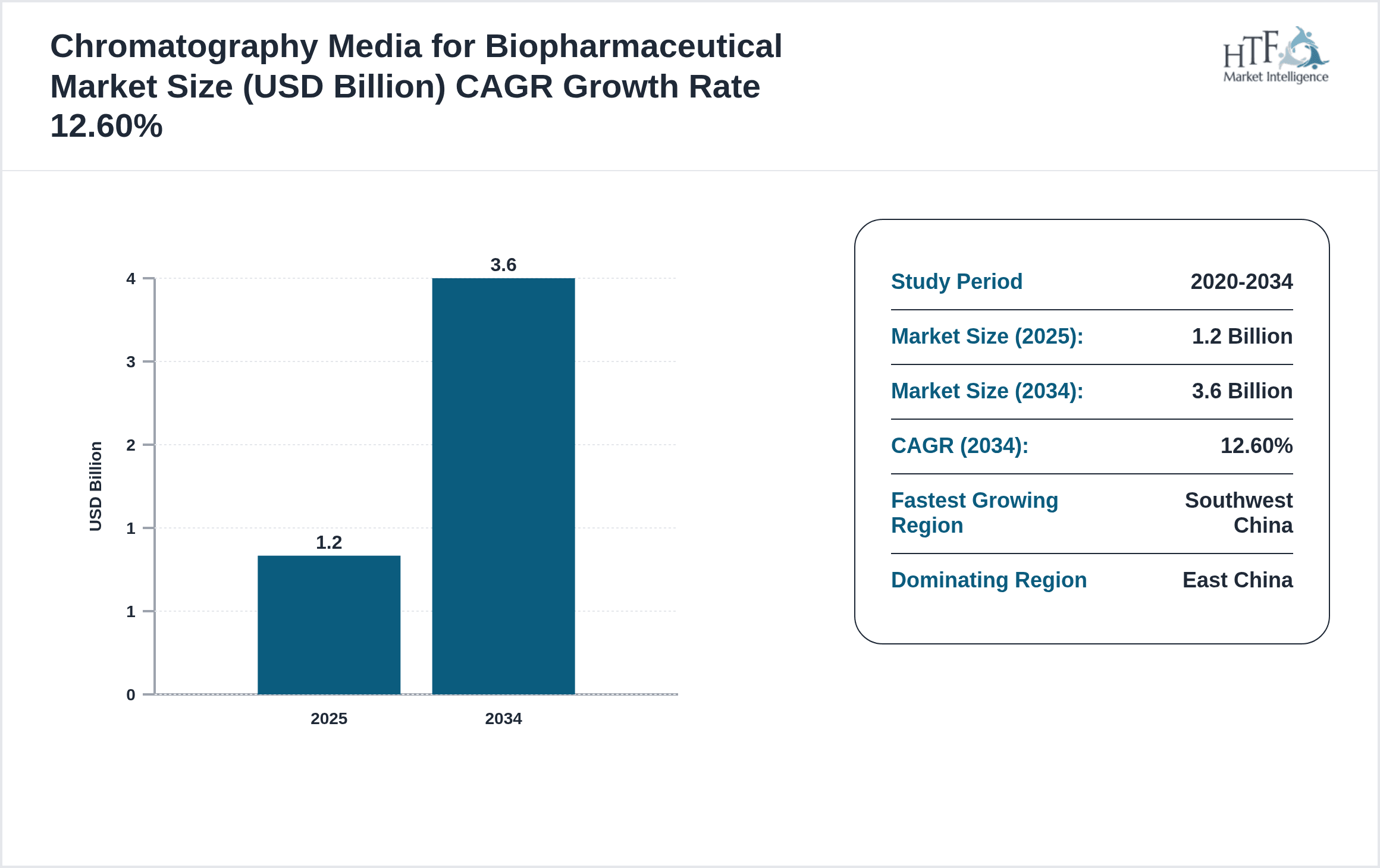

- •Market highlights reveal a robust CAGR of approximately 12.6% from 2025 to 2034, reflecting strong demand for advanced chromatography media that support high-purity biopharmaceutical production. The base market size in 2025 is estimated at USD 1.2 billion, forecasted to grow to USD 3.6 billion by 2034. East China dominates the market due to its concentration of biopharmaceutical manufacturing hubs and research centers, accounting for 35% market share. Meanwhile, Southwest China is projected as the fastest-growing sub-region with a CAGR of 15.2%, driven by increasing biotech investments and infrastructure development. Ion exchange chromatography remains the leading product type, favored for its versatility and efficiency, while mixed-mode chromatography is the fastest growing due to its ability to combine multiple separation mechanisms. Monoclonal antibodies represent the dominant application segment, with gene and cell therapies gaining traction as emerging applications. These dynamics underscore the evolving sophistication and scale of China's biopharmaceutical sector.

- •Strategically, the chromatography media market in China offers significant value to biopharmaceutical manufacturers, contract development and manufacturing organizations (CDMOs), and research institutions by enabling high-quality product purification at scale. The market’s growth is supported by government policies fostering innovation and quality assurance, investment in domestic production capabilities, and collaborations with global technology providers. This fosters technology transfer and localization of advanced chromatography media products, reducing reliance on imports and cost pressures. For stakeholders, the market presents opportunities for product differentiation, operational efficiency, and aligning with global regulatory expectations. As China’s biopharmaceutical industry matures, chromatography media providers that innovate in resin technology, offer tailored solutions for emerging modalities, and expand geographically within key regional zones will capture substantial market share and drive long-term growth.

Competitive Landscape

The competitive environment in the China Chromatography Media for Biopharmaceutical Market is characterized by intense rivalry among domestic and international companies striving for technological leadership and market penetration. Leading players focus on innovation in resin chemistry and media performance to meet the stringent purification requirements of complex biologics. Market positioning is influenced by a company's ability to offer high-quality, customizable chromatography media tailored to various biopharmaceutical applications, including monoclonal antibodies and gene therapies. Strategic collaborations and partnerships with biopharma manufacturers and CDMOs enable companies to enhance their value propositions and broaden their customer base. Additionally, pricing strategies and local manufacturing capabilities are crucial competitive factors, as China aims to reduce import dependency. Competitive dynamics also include ongoing investments in R&D to develop next-generation media with improved binding capacities, selectivity, and process scalability. Regional competition within China’s sub-markets further drives companies to expand geographically, while technological adoption and regulatory compliance remain key to sustaining competitive advantage. Overall, the market is evolving towards greater specialization and integration with bioprocess workflows, fostering a dynamic and competitive landscape.

Leading Companies in Chromatography Media for Biopharmaceutical Market

- •GE Healthcare Life Sciences (United States)

- •Cytiva (United States)

- •Sartorius AG (Germany)

- •Merck KGaA (Germany)

- •Tosoh Corporation (Japan)

- •Bio-Rad Laboratories (United States)

- •Repligen Corporation (United States)

- •ChromaNik Technologies Inc. (Japan)

- •Sepax Technologies, Inc. (Taiwan)

- •MabPlex International (China)

- •Hangzhou Wujing Biochemical Co., Ltd. (China)

- •Suzhou Nanomicro Technology Co., Ltd. (China)

- •Jiangsu Wuxi Biologics Co., Ltd. (China)

- •Shanghai Zheneng Chromatography Technology Co., Ltd. (China)

- •Beijing Biotech Chromatography Co., Ltd. (China)

- •BioVision Technologies (China)

- •Hangzhou Dayang Bio-Tech Co., Ltd. (China)

- •Jiangsu Tianmai Biotechnology Co., Ltd. (China)

- •Chengdu Biochemical Engineering Co., Ltd. (China)

- •Guangzhou Biotech Chromatography Co., Ltd. (China)

- •Ningbo Tianjiao Biotechnology Co., Ltd. (China)

- •Shanghai Lianshuo Biochemical Co., Ltd. (China)

- •Suzhou Yamei Biological Technology Co., Ltd. (China)

- •Shandong Huaxing Chromatography Technology Co., Ltd. (China)

- •Shanghai Yatai Biotechnology Co., Ltd. (China)

Market Breakdown

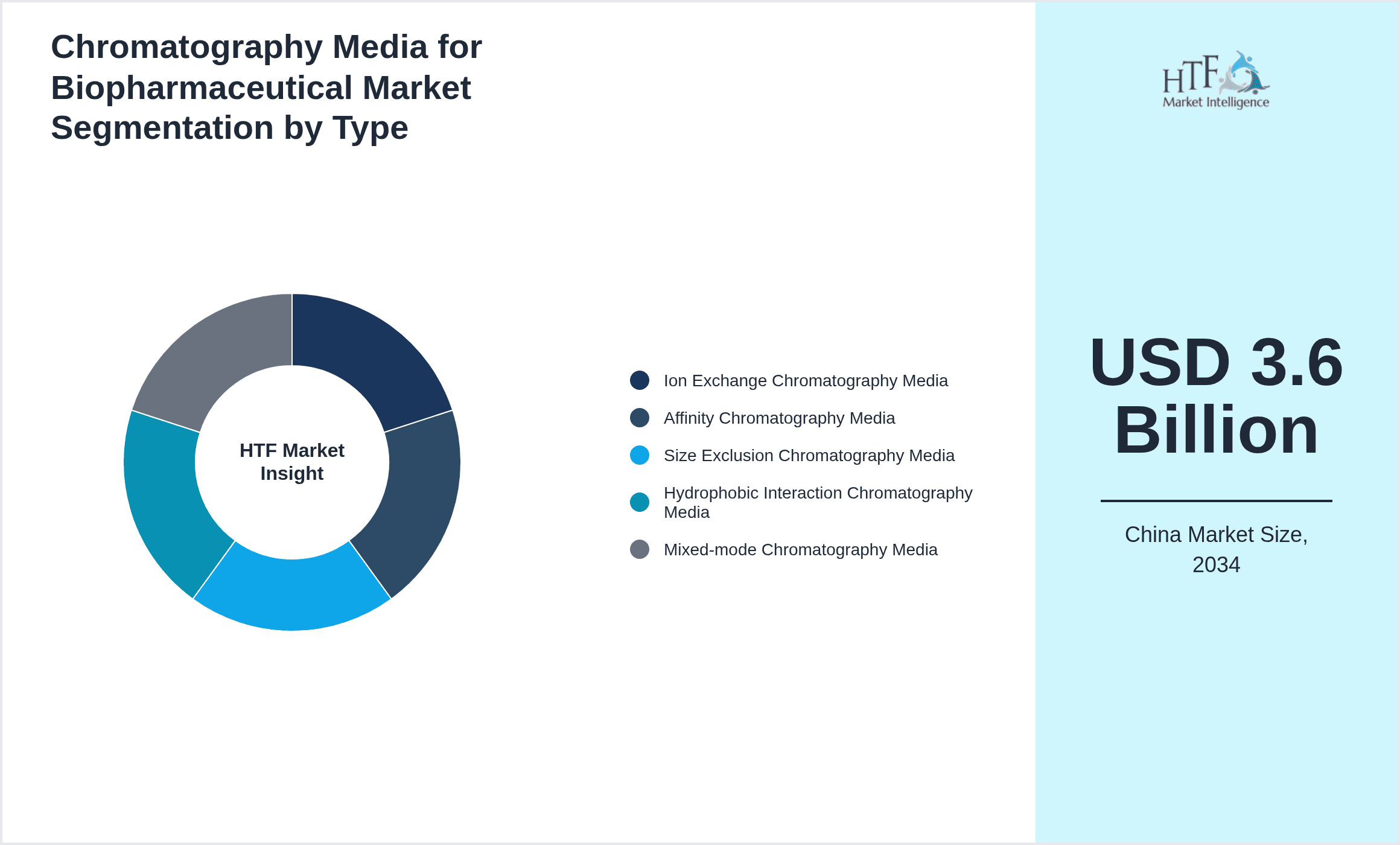

- •By Type

- ◦Ion Exchange Chromatography Media

- ◦Affinity Chromatography Media

- ◦Size Exclusion Chromatography Media

- ◦Hydrophobic Interaction Chromatography Media

- ◦Mixed-mode Chromatography Media

- •By Application

- ◦Monoclonal Antibodies Purification

- ◦Vaccines Purification

- ◦Recombinant Proteins Processing

- ◦Gene Therapy Vectors Purification

- ◦Cell Therapy Products Purification

- •By End-User Facility

- ◦Biopharmaceutical Manufacturing Plants

- ◦Contract Development and Manufacturing Organizations (CDMOs)

- ◦Research and Development Laboratories

- ◦Academic and Government Research Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Resellers

- ◦E-commerce Platforms

Growth Dynamics

China’s expanding biopharmaceutical sector, supported by government incentives and increased R&D investment, is the primary growth driver for chromatography media demand. The advancement of biologics such as monoclonal antibodies and gene therapies requires sophisticated purification media to meet quality and regulatory standards, fueling market expansion. Additionally, growing domestic manufacturing capabilities and efforts to reduce import dependence further boost demand for locally produced chromatography media. Increasing adoption of single-use technologies and continuous processing in downstream bioprocessing enhances the requirement for advanced chromatography solutions with improved efficiency and scalability. Furthermore, rising awareness of process optimization and cost reduction among manufacturers accelerates the uptake of innovative chromatography media tailored to specific biopharmaceutical applications.

Market Trends

The China market is witnessing a trend toward development and adoption of next-generation chromatography media that offer higher binding capacities, selectivity, and robustness, enabling manufacturers to improve product yields and process throughput. Integration of mixed-mode chromatography media, combining multiple separation mechanisms, is gaining traction due to its versatility in purifying complex biologics. There is also an increased focus on sustainability and cost-effectiveness, driving demand for reusable and high-performance media. Collaborations between domestic companies and global technology providers are facilitating technology transfer and localization of advanced chromatography products. Digitalization and automation in downstream processing are influencing chromatography media development to support real-time monitoring and process control, further enhancing purification efficiency and compliance with regulatory expectations.

Market Opportunities

The growing pipeline of innovative biologics, including gene and cell therapies, presents significant opportunities for chromatography media manufacturers to develop tailored purification solutions addressing unique molecular characteristics. Expansion of biopharmaceutical manufacturing in emerging zones like Southwest and Northwest China offers prospects for localized production and distribution networks. Increasing government focus on biotech innovation and quality standards encourages investment in R&D for advanced chromatography technologies. Opportunities also exist in developing sustainable, cost-effective media to reduce process costs and environmental impact, aligning with industry trends toward green bioprocessing. Furthermore, strategic partnerships and joint ventures with domestic biopharmaceutical firms can accelerate market penetration and technology adoption in China’s rapidly evolving biopharma landscape.

Market Challenges

Despite strong growth prospects, the China Chromatography Media market faces challenges such as high entry barriers due to the need for advanced technology, significant R&D investment, and stringent regulatory compliance. Dependence on imported raw materials and components for high-performance media creates supply chain vulnerabilities and cost pressures. Intellectual property protection concerns and competition from established global players complicate the market landscape for domestic manufacturers. Additionally, variability in regional infrastructure and expertise across China’s sub-regions poses challenges for uniform market development. Pricing pressures from biopharmaceutical manufacturers seeking cost reduction while maintaining quality further constrain profit margins for chromatography media producers. Navigating complex regulatory frameworks and adapting to rapid technological changes require continuous innovation and agile business strategies.

Regulatory Framework

Between 2020 and 2025, China implemented stringent regulations to enhance biopharmaceutical product safety and quality, directly impacting chromatography media requirements. Key regulatory updates include the revised Good Manufacturing Practice (GMP) guidelines mandating rigorous validation and performance standards for chromatography materials. The National Medical Products Administration (NMPA) introduced enhanced inspection protocols for purification media suppliers to ensure compliance with international standards. Environmental regulations on chemical usage in manufacturing have also tightened, prompting adoption of greener chromatography media technologies. Moreover, government incentives supporting domestic production have encouraged local manufacturers to align with regulatory expectations through quality certification programs. These frameworks collectively drive innovation, quality assurance, and localization in China’s chromatography media market, fostering increased trust and global competitiveness for biopharmaceutical products.

Market Intelligence

- •15th January 2025, Cytiva announced the launch of a new mixed-mode chromatography resin tailored for gene therapy vector purification, featuring enhanced selectivity and scalability to meet the growing demand in China’s advanced biopharma sector. This product aims to improve downstream process efficiency and reduce production costs while complying with NMPA regulatory requirements. Cytiva’s strategic focus on the China market is evident through increased local manufacturing and collaborations with leading biotech firms. The innovative resin supports complex biomolecule purification, addressing challenges in emerging therapy modalities and strengthening Cytiva’s competitive position in the region. Source: Official Cytiva press release.

- •10th March 2025, Sartorius AG expanded its chromatography media production facility in Shanghai to increase capacity and support the rising demand from biopharmaceutical manufacturers across China. The expansion includes integration of automated quality control systems and advanced resin synthesis technologies to enhance product consistency and reduce lead times. This investment underscores Sartorius’s commitment to the Chinese market and its role in localizing critical bioprocessing materials. The move aims to mitigate supply chain risks and strengthen partnerships with domestic CDMOs and pharma companies. Source: Sartorius corporate announcement.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 3.6 Billion |

| CAGR | 12.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12% |

| Scope of Report | Market is segmented by Type (Ion Exchange Chromatography Media, Affinity Chromatography Media, Size Exclusion Chromatography Media, Hydrophobic Interaction Chromatography Media, Mixed-mode Chromatography Media), Application (Monoclonal Antibodies Purification, Vaccines Purification, Recombinant Proteins Processing, Gene Therapy Vectors Purification, Cell Therapy Products Purification), End-User Facility (Biopharmaceutical Manufacturing Plants, Contract Development and Manufacturing Organizations (CDMOs), Research and Development Laboratories, Academic and Government Research Institutes), Distribution Channel (Direct Sales, Distributors and Resellers, E-commerce Platforms) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | GE Healthcare Life Sciences (United States), Cytiva (United States), Sartorius AG (Germany), Merck KGaA (Germany), Tosoh Corporation (Japan), Bio-Rad Laboratories (United States), Repligen Corporation (United States), ChromaNik Technologies Inc. (Japan), Sepax Technologies, Inc. (Taiwan), MabPlex International (China), Hangzhou Wujing Biochemical Co., Ltd. (China), Suzhou Nanomicro Technology Co., Ltd. (China), Jiangsu Wuxi Biologics Co., Ltd. (China), Shanghai Zheneng Chromatography Technology Co., Ltd. (China), Beijing Biotech Chromatography Co., Ltd. (China), BioVision Technologies (China), Hangzhou Dayang Bio-Tech Co., Ltd. (China), Jiangsu Tianmai Biotechnology Co., Ltd. (China), Chengdu Biochemical Engineering Co., Ltd. (China), Guangzhou Biotech Chromatography Co., Ltd. (China), Ningbo Tianjiao Biotechnology Co., Ltd. (China), Shanghai Lianshuo Biochemical Co., Ltd. (China), Suzhou Yamei Biological Technology Co., Ltd. (China), Shandong Huaxing Chromatography Technology Co., Ltd. (China), Shanghai Yatai Biotechnology Co., Ltd. (China) |

China Chromatography Media for Biopharmaceutical Market - China Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.