Europe Independent Self-checkout System Market - Outlook 2025-2034

Europe Independent Self-checkout System Market is segmented by Type (Hardware (Barcode Scanners, Payment Terminals, Touchscreens), Software (Self-checkout Applications, AI Analytics, Cloud Solutions), Services (Installation, Integration, Maintenance & Support), Maintenance & Support, Integration Solutions), Application (Grocery Retail, Convenience Stores, Department Stores, Specialty Retail, Online Retail), Retail Format (Supermarkets, Hypermarkets, Discount Stores, Pharmacies, Shopping Malls), Deployment Model (Cloud-based, On-premise, Hybrid), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Independent Self-checkout System market is defined by the provision and adoption of standalone self-checkout technologies that empower consumers to autonomously complete their retail transactions. This market spans a wide array of retail sectors including grocery, convenience, department, and specialty stores, with applications increasingly extending to online retail fulfillment centers. The systems typically integrate advanced hardware components such as barcode scanners, touchscreens, and payment terminals with intelligent software solutions that leverage AI and IoT technologies to improve speed, accuracy, and security. The scope further extends to comprehensive services including installation, integration, and maintenance, ensuring seamless operation and adaptability to retailers’ evolving needs. The market addresses growing consumer demand for contactless, efficient, and personalized shopping experiences while enabling retailers to optimize labor costs and enhance operational efficiency. Technological innovations, regulatory compliance, and shifting consumer behaviors collectively define the dynamic scope and growth trajectory of this market, positioning it as a cornerstone of Europe’s retail automation transformation.

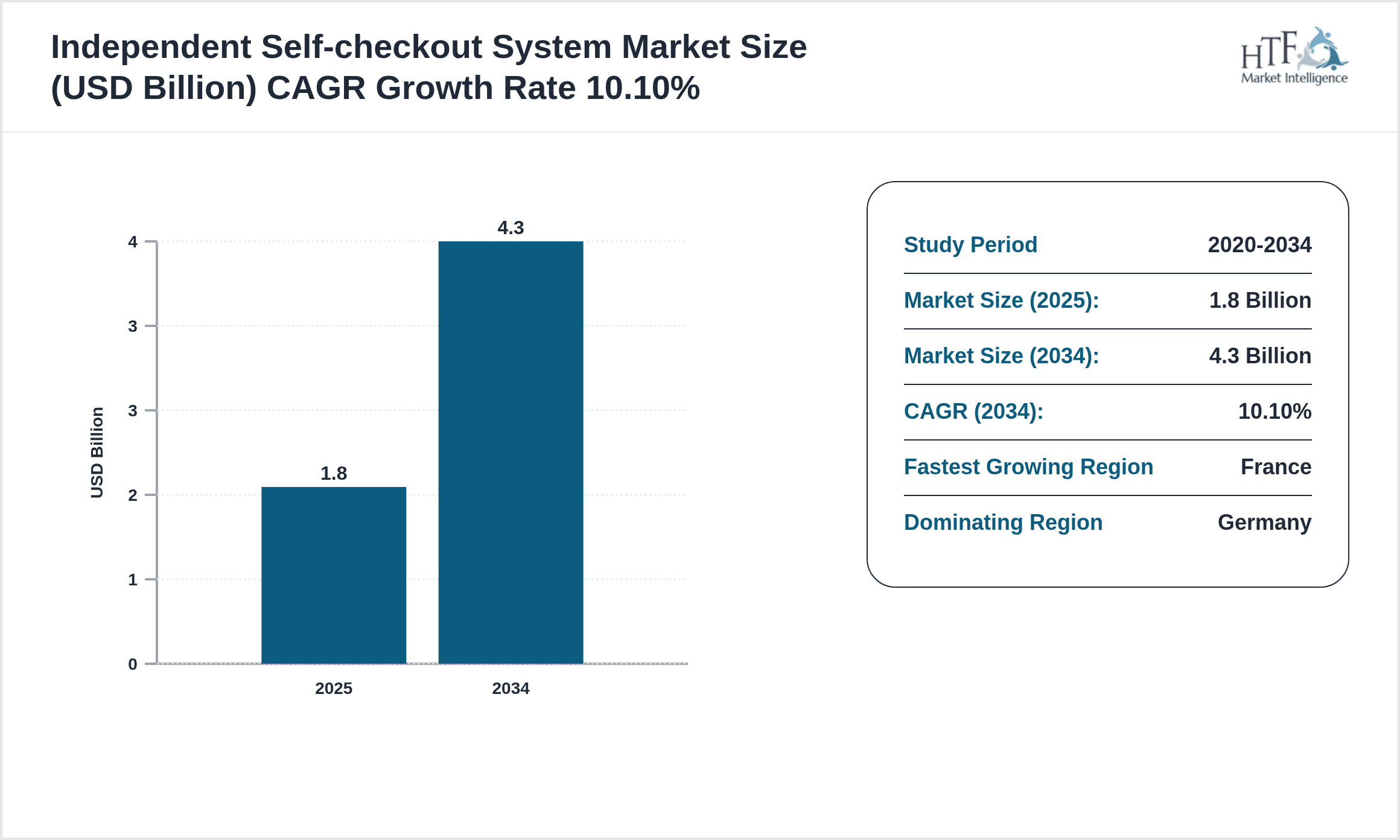

- •Key highlights indicate a robust market growth trajectory with a projected CAGR of 10.1% from 2025 to 2034, driven by rising demand for contactless payments and retail automation. The hardware segment dominates with 40% market share in 2025, while software segments are witnessing the fastest growth due to advancements in AI and cloud capabilities. Germany leads the market with a 27% share, reflecting mature adoption, whereas France is the fastest-growing country with a CAGR of 12.5%, buoyed by increasing investments and retail modernization initiatives. The market size is anticipated to more than double from USD 1.8 billion in 2025 to USD 4.3 billion by 2034, underscoring significant expansion opportunities across diverse retail formats and geographic clusters within Europe.

- •The market presents strategic value to retailers, technology providers, and service companies by facilitating operational efficiencies, reducing checkout times, and enhancing customer satisfaction. The convergence of hardware innovation, software intelligence, and service excellence creates a compelling value proposition that addresses labor shortages and evolving consumer expectations in Europe’s retail sector. Stakeholders benefit from scalable, customizable solutions that integrate easily with existing retail infrastructure while complying with stringent European regulatory standards. As retail landscapes evolve with digital transformation, the independent self-checkout market emerges as a pivotal enabler of sustainability, profitability, and competitive differentiation.

Competitive Landscape

Competition within the Europe Independent Self-checkout System market is characterized by a blend of innovation-driven product development, strategic collaborations, and focused regional expansion. Leading players compete rigorously on technological advancement, emphasizing AI integration, seamless payment processing, and user-friendly interfaces to differentiate their solutions. Market rivalry intensifies as companies invest in R&D to enhance system accuracy, reduce transaction times, and improve security features. Strategic partnerships with retailers and technology integrators play a critical role in market penetration and service delivery. Pricing strategies vary with customization levels and service agreements influencing buyer preferences. Barriers to entry include the need for robust after-sales support and compliance with Europe’s stringent data privacy and payment security regulations. Regional competition is shaped by local consumer behavior and regulatory nuances, prompting firms to tailor offerings accordingly. Looking ahead, innovation in cloud-based and mobile-enabled self-checkout solutions is expected to redefine competitive dynamics, fostering agile market responses and customer engagement.

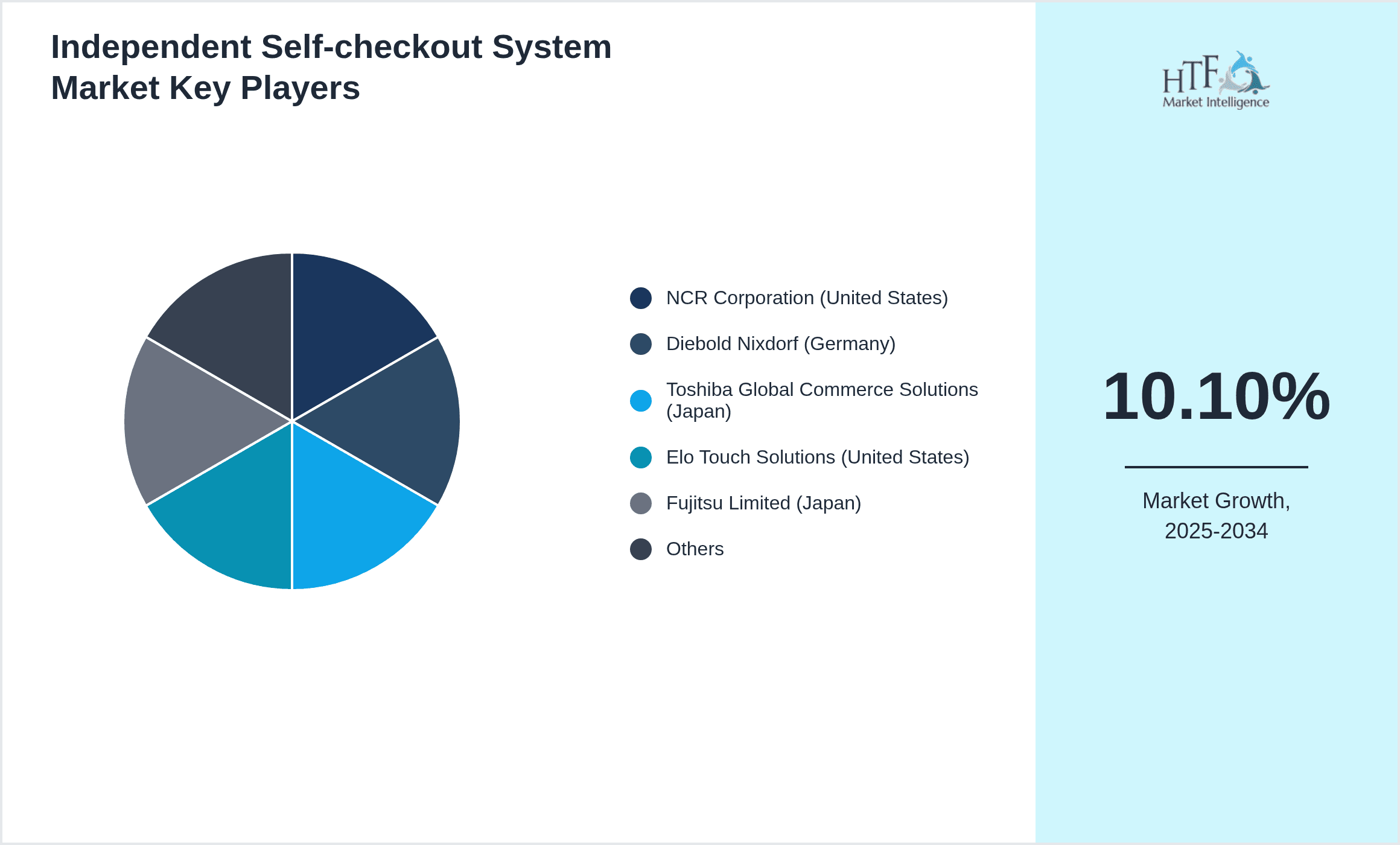

Prominent Players in Independent Self-checkout System Market

- •NCR Corporation (United States)

- •Diebold Nixdorf (Germany)

- •Toshiba Global Commerce Solutions (Japan)

- •Elo Touch Solutions (United States)

- •Fujitsu Limited (Japan)

- •Zebra Technologies (United States)

- •Panasonic Corporation (Japan)

- •Honeywell International Inc. (United States)

- •Nanonation (United Kingdom)

- •Wincor Nixdorf (Germany)

- •PAX Technology Limited (China)

- •AURES Technologies (France)

- •Posiflex Technology, Inc. (Taiwan)

- •Sharp Corporation (Japan)

- •Ingenico Group (France)

- •Diebold Nixdorf (Germany)

- •NCR Corporation (United States)

- •Elo Touch Solutions (United States)

- •Toshiba Global Commerce Solutions (Japan)

- •Wincor Nixdorf (Germany)

- •Fujitsu Limited (Japan)

- •Honeywell International Inc. (United States)

- •Panasonic Corporation (Japan)

- •Zebra Technologies (United States)

- •Nanonation (United Kingdom)

Market Breakdown

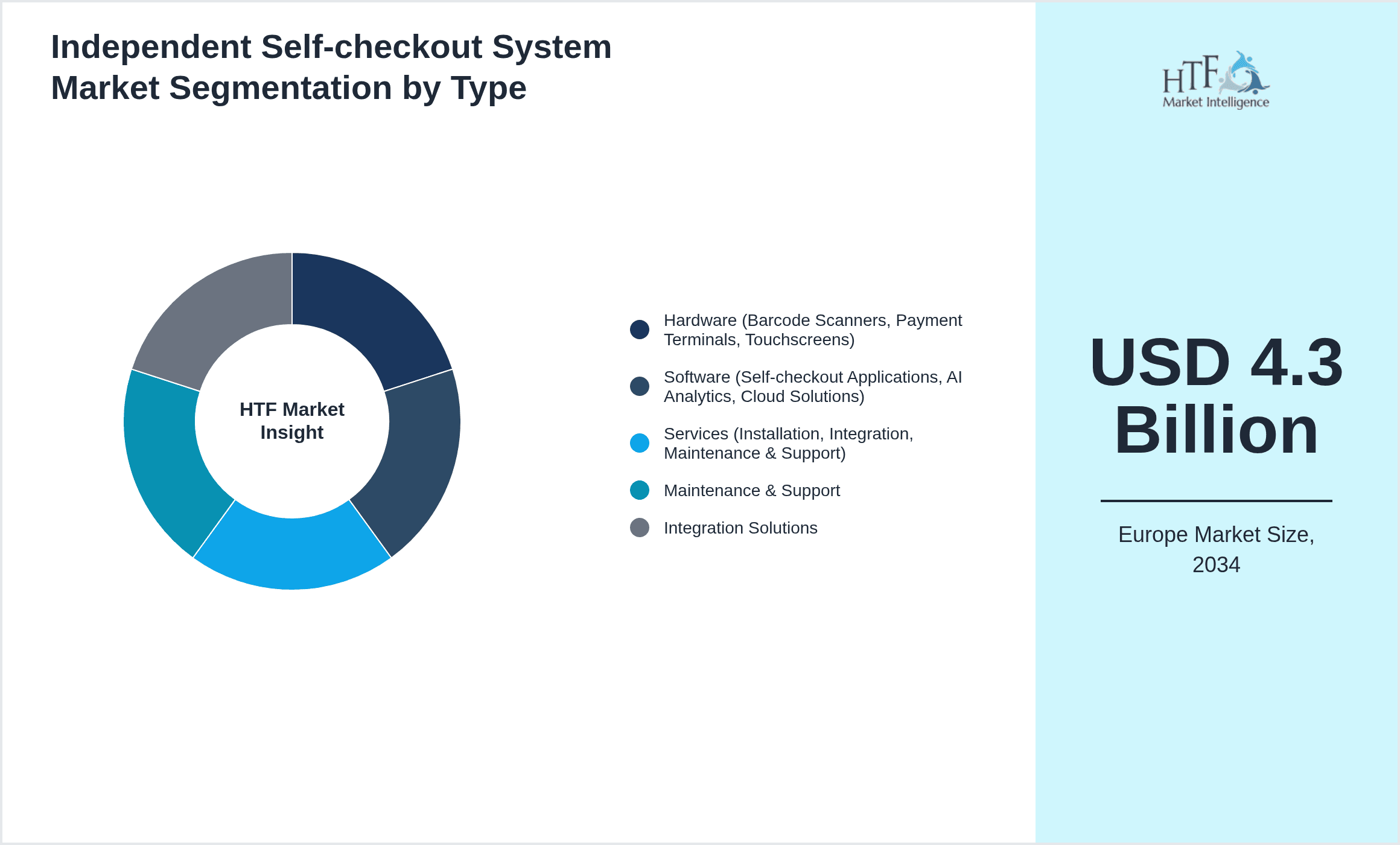

- •By Type

- ◦Hardware (Barcode Scanners, Payment Terminals, Touchscreens)

- ◦Software (Self-checkout Applications, AI Analytics, Cloud Solutions)

- ◦Services (Installation, Integration, Maintenance & Support)

- ◦Maintenance & Support

- ◦Integration Solutions

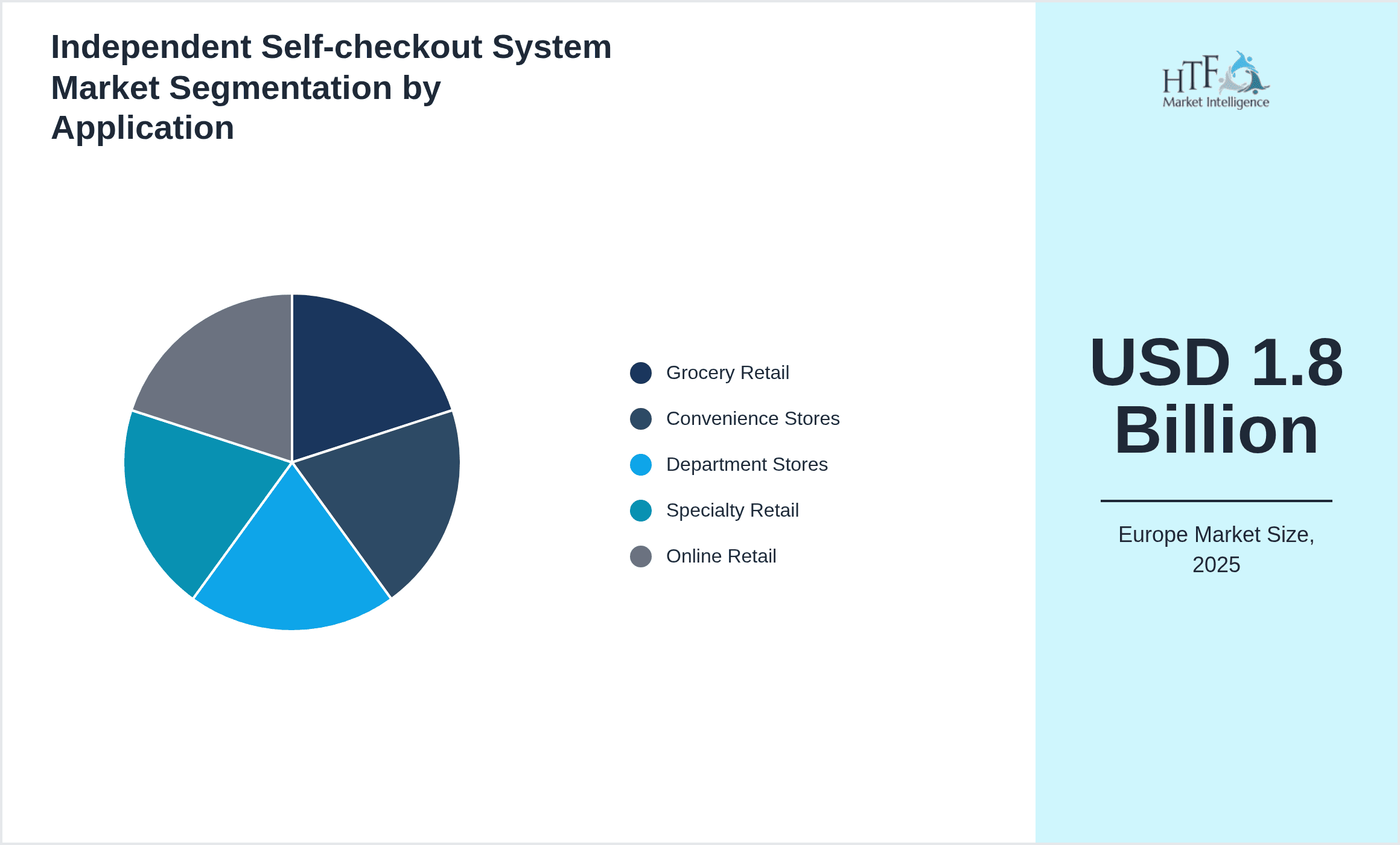

- •By Application

- ◦Grocery Retail

- ◦Convenience Stores

- ◦Department Stores

- ◦Specialty Retail

- ◦Online Retail

- •By Retail Format

- ◦Supermarkets

- ◦Hypermarkets

- ◦Discount Stores

- ◦Pharmacies

- ◦Shopping Malls

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

Growth Dynamics

- •Increasing consumer preference for contactless and autonomous shopping experiences is propelling the adoption of independent self-checkout systems across Europe. Retailers are investing heavily in automation technologies to reduce labor costs and enhance checkout speed, driving market expansion.

- •Advancements in AI and machine learning enable more accurate product recognition and fraud detection within self-checkout systems, enhancing reliability and consumer trust, which in turn fuels market growth.

- •Government initiatives promoting digital transformation and cashless payment infrastructures across European countries are facilitating widespread deployment of smart self-checkout solutions in retail environments.

- •The integration of cloud-based platforms allows seamless software updates and data analytics, providing retailers with actionable insights to optimize operations and customer engagement, thereby accelerating market adoption.

- •Rising urbanization and increasing retail outlet density in major European economies are creating demand for efficient checkout solutions that can handle high customer throughput with minimal staffing.

Market Trends

- •Integration of biometric authentication and facial recognition technologies is emerging as a key trend to enhance security and personalized shopping experiences within self-checkout systems.

- •Retailers are increasingly adopting hybrid deployment models combining on-premise hardware with cloud-based software to balance performance, scalability, and data security.

- •Sustainability initiatives are influencing the design of self-checkout hardware, with manufacturers prioritizing energy-efficient components and recyclable materials.

- •The COVID-19 pandemic accelerated the shift towards contactless retail technologies, solidifying the role of independent self-checkout systems as a standard offering in European stores.

- •Collaborations between technology providers and retail chains to co-develop customized solutions are becoming prevalent, fostering innovation and market penetration.

Market Opportunities

- •Expanding into underserved retail segments such as pharmacies and specialty stores offers significant growth potential for self-checkout system providers.

- •Emerging technologies like augmented reality (AR) can be integrated to enhance user interaction and support in self-checkout processes, opening new avenues for innovation.

- •Strategic partnerships with fintech companies to embed advanced payment solutions can differentiate offerings and increase adoption rates.

- •Expanding maintenance & support services tailored for SMEs can capture a broader customer base and ensure long-term revenue streams.

- •Geographic expansion into Eastern European markets presents opportunities due to rising retail modernization and increasing consumer spending power.

Market Challenges

- •High initial capital expenditure for hardware installation and integration poses a barrier for small and medium-sized retailers considering self-checkout adoption.

- •Consumer reluctance and unfamiliarity with self-checkout technology in certain regions limit market penetration and require focused education and awareness campaigns.

- •Complex regulatory compliance related to data privacy, payment security, and accessibility standards imposes operational challenges for providers and retailers.

- •Technical issues such as product mis-scanning and theft prevention remain concerns, necessitating continuous innovation and system refinement.

- •Competition from alternative retail automation technologies such as cashier-less stores and mobile self-checkout apps intensifies market rivalry.

Regulatory Framework

- •Between 2020 and 2025, the European Union enforced the Payment Services Directive 2 (PSD2), mandating strong customer authentication for electronic payments, significantly impacting self-checkout payment processing solutions by requiring enhanced security features.

- •GDPR regulations, fully effective since 2018 but reinforced through 2025, require self-checkout system providers to ensure stringent data privacy controls and transparent data handling for consumer information collected during transactions.

- •Accessibility legislation across the EU, including the European Accessibility Act adopted in 2019, requires self-checkout systems to be designed to accommodate users with disabilities, influencing hardware design and software interfaces.

- •The EU Cybersecurity Act introduced in 2019 establishes frameworks for certifying security in ICT products, including self-checkout systems, compelling vendors to meet standardized cybersecurity requirements by 2025.

- •Country-specific mandates such as Germany's Kassensicherungsverordnung (Cash Register Security Ordinance) implemented in 2020 require secure transaction logging and tamper-proof recording in point-of-sale systems, affecting self-checkout hardware compliance standards.

Market Intelligence

- •15th February 2024, Diebold Nixdorf launched a next-generation self-checkout solution integrating AI-powered video analytics and contactless payment options tailored for European grocery chains. The system enhances loss prevention capabilities while improving customer throughput with intuitive user interfaces and real-time data analytics. This launch underscores the company's commitment to innovation and its strategic focus on the European retail automation market. The platform supports cloud-based management and seamless integration with existing retail infrastructure, facilitating flexible deployments and scalable solutions for diverse store formats. The product rollout has been met with positive retailer feedback, signaling strong market acceptance and opening avenues for expanded adoption across Europe. Source: Diebold Nixdorf Official Press Release

- •10th November 2023, NCR Corporation announced the expansion of its European service network to support growing demand for self-checkout system installations and maintenance. The initiative includes opening new regional service centers in France, Spain, and Italy, ensuring faster response times and localized technical expertise. NCR also unveiled enhancements to its software platform, incorporating advanced fraud detection and adaptive machine learning algorithms to improve transaction accuracy and customer experience. This strategic move solidifies NCR’s market leadership in Europe and aligns with increasing retailer investments in automation and digital transformation. The expanded footprint facilitates tailored support for diverse European retail environments, fostering long-term partnerships and revenue growth. Source: NCR Corporation Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 4.3 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.1% |

| Scope of Report | Market is segmented by Type (Hardware (Barcode Scanners, Payment Terminals, Touchscreens), Software (Self-checkout Applications, AI Analytics, Cloud Solutions), Services (Installation, Integration, Maintenance & Support), Maintenance & Support, Integration Solutions), Application (Grocery Retail, Convenience Stores, Department Stores, Specialty Retail, Online Retail), Retail Format (Supermarkets, Hypermarkets, Discount Stores, Pharmacies, Shopping Malls), Deployment Model (Cloud-based, On-premise, Hybrid) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | NCR Corporation (United States), Diebold Nixdorf (Germany), Toshiba Global Commerce Solutions (Japan), Elo Touch Solutions (United States), Fujitsu Limited (Japan), Zebra Technologies (United States), Panasonic Corporation (Japan), Honeywell International Inc. (United States), Nanonation (United Kingdom), Wincor Nixdorf (Germany), PAX Technology Limited (China), AURES Technologies (France), Posiflex Technology, Inc. (Taiwan), Sharp Corporation (Japan), Ingenico Group (France), Diebold Nixdorf (Germany), NCR Corporation (United States), Elo Touch Solutions (United States), Toshiba Global Commerce Solutions (Japan), Wincor Nixdorf (Germany), Fujitsu Limited (Japan), Honeywell International Inc. (United States), Panasonic Corporation (Japan), Zebra Technologies (United States), Nanonation (United Kingdom) |

Europe Independent Self-checkout System Market - Outlook 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.