Europe Amoled Microdisplay Market Size, Growth & Revenue 2024-2034

Europe Amoled Microdisplay Market is segmented by Amoled Microdisplay Type (Active Matrix Amoled Microdisplays, Passive Matrix Amoled Microdisplays, Flexible Amoled Microdisplays, Transparent Amoled Microdisplays, Monochrome Amoled Microdisplays), Application Segment (Augmented Reality (AR) Displays, Virtual Reality (VR) Displays, Wearable Devices, Military & Defense Displays, Consumer Electronics), Display Technology (Rigid AMOLED Technology, Flexible AMOLED Technology, Transparent AMOLED Technology), End-User Industry (Healthcare & Medical Devices, Automotive Industry, Gaming & Entertainment, Industrial & Commercial Applications), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Amoled Microdisplay Market is a dynamic sector focused on the manufacturing and application of AMOLED microdisplays used extensively in AR/VR devices, wearable technologies, military equipment, and consumer electronics. Characterized by high pixel density, low power consumption, and compact form factors, these displays are critical in enabling advanced user experiences and functionality. The market covers a range of types including Active Matrix, Passive Matrix, Flexible, Transparent, and Monochrome AMOLED microdisplays, each catering to specific performance and design requirements. Geographically, the market spans key European countries such as Germany, France, the UK, Italy, and Nordic regions, influenced by strong technological infrastructure, R&D investments, and regulatory standards. Industry advancements are fueled by escalating demand for immersive technologies in gaming, defense, and healthcare, alongside growing consumer electronics adoption. The competitive landscape is marked by innovation, strategic collaborations, and regional manufacturing expansion, positioning Europe as a significant player in the global AMOLED microdisplay ecosystem.

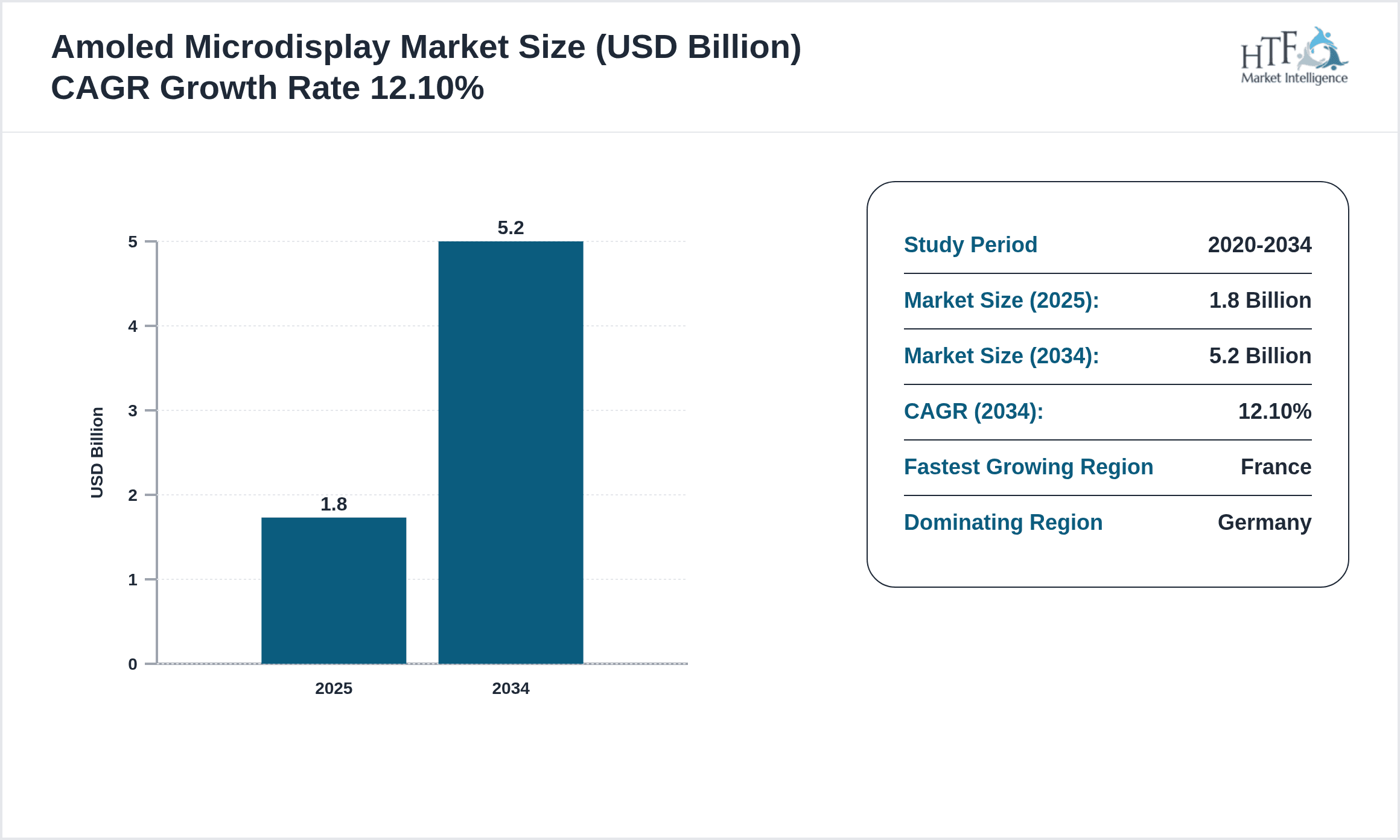

- •The market is projected to grow from USD 1.8 billion in 2025 to USD 5.2 billion by 2034, exhibiting a CAGR of 12.1%. Germany leads with 29% market share, driven by its robust manufacturing base and innovation capacity, while France is the fastest growing with a CAGR of 15.5%, supported by government initiatives and startup activity. Active Matrix AMOLED dominates product type owing to superior display quality and widespread adoption in AR/VR devices. Flexible AMOLED microdisplays are rapidly gaining traction due to their adaptability in wearable and foldable devices, underpinning growth opportunities. The European market is shaped by evolving consumer preferences for high-performance displays and stringent energy efficiency regulations, fostering technology upgrades and product differentiation. Key players are investing in R&D to optimize microdisplay performance and cost, ensuring competitive advantage in a rapidly evolving landscape.

- •Europe's Amoled Microdisplay Market offers strategic value to industries such as defense, consumer electronics, and healthcare, where immersive display technologies drive innovation. The market’s growth supports the development of next-generation devices that enhance user interaction and experience, providing a competitive edge for manufacturers and technology providers. Investments in flexible and transparent AMOLED technologies open new avenues for product design and application expansion. Regulatory frameworks emphasizing sustainability and energy efficiency further incentivize innovation and adoption. Stakeholders including component manufacturers, device makers, and system integrators benefit from a collaborative ecosystem fostering technology transfer and market penetration. Overall, the market’s trajectory presents lucrative opportunities for investors and businesses committed to advanced display solutions in Europe's technologically progressive environment.

Competitive Landscape

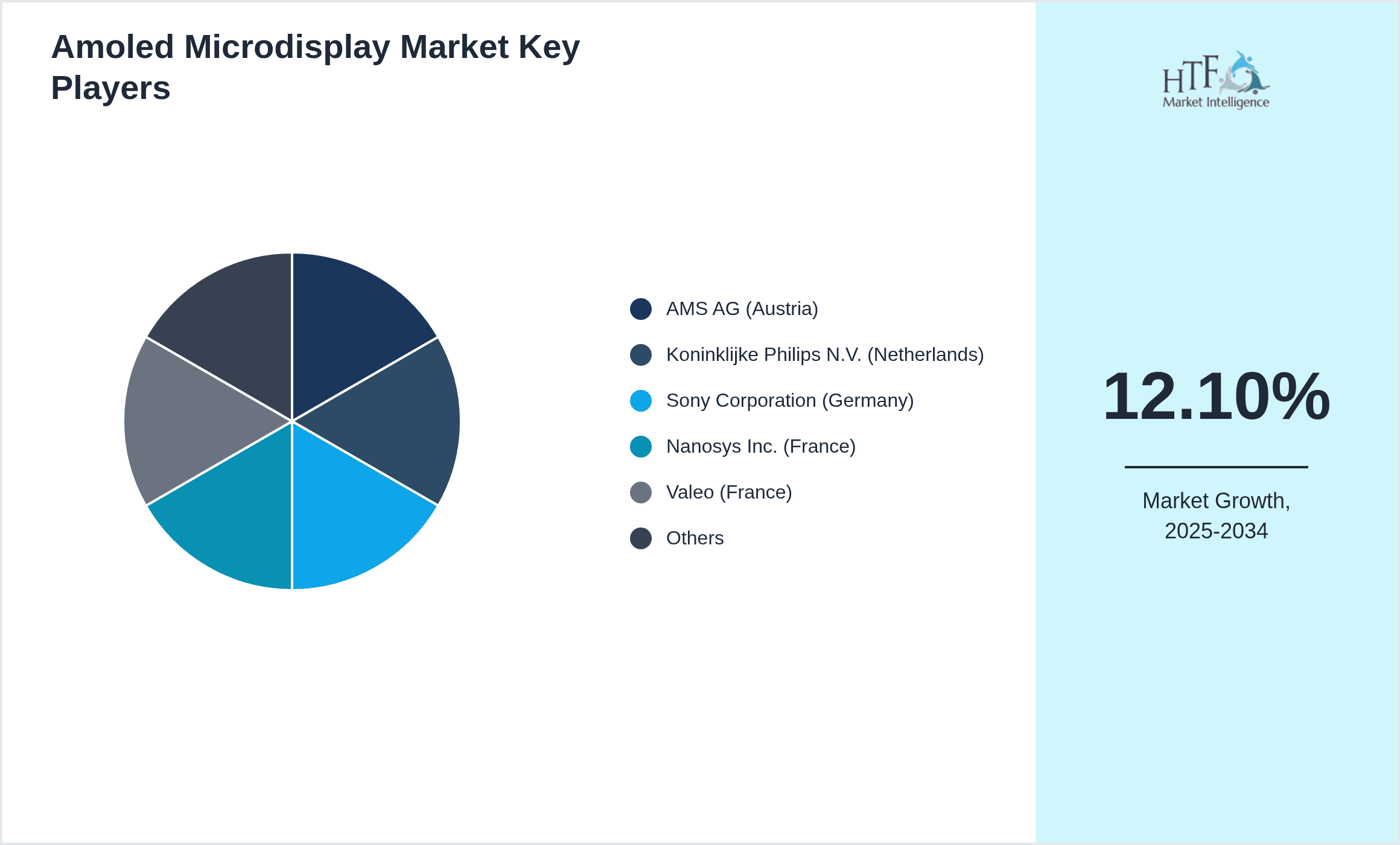

The competitive landscape of the Europe Amoled Microdisplay Market is characterized by intense rivalry among a mix of global leaders and innovative regional players. Companies compete primarily on technological innovation, product quality, and customization capabilities to serve diverse applications such as AR/VR, wearables, and defense. Strategic partnerships and collaborations are common to accelerate R&D and market penetration, while mergers and acquisitions help consolidate market position and expand technological portfolios. Pricing strategies balance between premium performance offerings and cost-effective solutions to address varying customer segments. Distribution channels are optimized for efficient delivery to OEMs and integrators, supported by localized manufacturing hubs across Europe. Intellectual property and patent portfolios play a critical role in maintaining competitive advantage. The market also experiences pressure from emerging technologies such as microLED and OLED variants, pushing players to continuously innovate and invest in next-generation AMOLED microdisplays. Regulatory compliance and sustainability considerations further influence strategic decision-making and competitive dynamics within the region.

Leading Companies in Amoled Microdisplay Market

- •AMS AG (Austria)

- •Koninklijke Philips N.V. (Netherlands)

- •Sony Corporation (Germany)

- •Nanosys Inc. (France)

- •Valeo (France)

- •Himax Technologies (UK)

- •Kopin Corporation (Germany)

- •LG Display Europe (Belgium)

- •Microoled (France)

- •eMagin Corporation (UK)

- •Carl Zeiss AG (Germany)

- •Syndiant (Ireland)

- •JDI Europe (UK)

- •BOE Technology Group (Germany)

- •Panasonic Europe (Germany)

- •Samsung Display Europe (Germany)

- •Innolux Corporation (France)

- •Visteon Corporation (UK)

- •Epistar Europe (Germany)

- •Seiko Epson Corporation (UK)

- •Canon Europe (UK)

- •Sharp Corporation (Germany)

- •Sony Europe (France)

- •AU Optronics Europe (Germany)

- •Toshiba Europe (UK)

Market Breakdown

- •By Amoled Microdisplay Type

- ◦Active Matrix Amoled Microdisplays

- ◦Passive Matrix Amoled Microdisplays

- ◦Flexible Amoled Microdisplays

- ◦Transparent Amoled Microdisplays

- ◦Monochrome Amoled Microdisplays

- •By Application Segment

- ◦Augmented Reality (AR) Displays

- ◦Virtual Reality (VR) Displays

- ◦Wearable Devices

- ◦Military & Defense Displays

- ◦Consumer Electronics

- •By Display Technology

- ◦Rigid AMOLED Technology

- ◦Flexible AMOLED Technology

- ◦Transparent AMOLED Technology

- •By End-User Industry

- ◦Healthcare & Medical Devices

- ◦Automotive Industry

- ◦Gaming & Entertainment

- ◦Industrial & Commercial Applications

Growth Dynamics

- •Europe’s Amoled Microdisplay Market growth is primarily driven by increasing adoption of augmented reality and virtual reality technologies across consumer electronics and industrial sectors. Rising consumer demand for immersive gaming experiences and advanced visualization tools in healthcare and automotive industries significantly fuels market expansion. Additionally, advancements in flexible AMOLED technology enable innovative form factors, broadening application scopes. Government investments in digital infrastructure and support for innovation also contribute to accelerating growth. The emphasis on energy-efficient, high-resolution displays aligns with evolving environmental regulations, further stimulating market adoption and R&D activity.

- •The market is benefiting from an upsurge in wearable device usage, driven by health monitoring and fitness tracking trends. Flexible AMOLED microdisplays facilitate sleek, lightweight designs, meeting consumer preferences for convenience and aesthetics. Integration of AMOLED microdisplays in military and defense systems for enhanced situational awareness and night vision capabilities adds to demand. Collaborative efforts between technology providers and OEMs result in faster product development cycles and market penetration. The growing e-commerce sector in Europe also boosts distribution and accessibility of AMOLED-based devices, reinforcing market momentum.

- •Technological innovations such as transparent and foldable AMOLED microdisplays are opening new avenues in automotive heads-up displays and smart glasses, expanding market applications. Research focusing on improving display lifespan and reducing production costs enhances market attractiveness. The increasing presence of startups and SMEs investing in AMOLED microdisplay R&D fosters competitive diversity and rapid technology diffusion. Cross-industry adoption, including healthcare, defense, and entertainment, diversifies revenue streams and mitigates market risks. Overall, technological progress and diversified applications form the backbone of sustained market growth in Europe.

- •Regulatory support for energy-efficient electronics and European Union initiatives promoting sustainable manufacturing practices positively impact market dynamics. Companies are incentivized to develop environmentally friendly AMOLED products that comply with strict emission and waste management standards. This regulatory environment encourages innovation in materials and production processes, leading to better-quality, compliant microdisplays. Furthermore, intellectual property protection frameworks in Europe safeguard technological advancements, promoting investments in cutting-edge AMOLED innovations.

- •The rising consumer awareness about device performance and display quality influences purchasing decisions strongly, favoring AMOLED microdisplays. Enhanced user experiences with richer colors, higher contrast, and faster response times drive preference over traditional display technologies. The competitive landscape encourages companies to improve product differentiation through innovative display features and customization options. Economic recovery post-pandemic and increasing disposable incomes across European countries further support consumer spending on premium electronic devices incorporating AMOLED microdisplays.

Market Trends

- •A notable trend in the Europe Amoled Microdisplay Market is the accelerating integration of flexible AMOLED technology in wearable and foldable consumer devices. This trend aligns with consumer demand for compact, lightweight, and ergonomically designed electronics. Companies are investing heavily in flexible substrate materials and manufacturing techniques to enhance display durability and performance. This shift is reshaping product design paradigms and enabling innovative user interfaces across applications.

- •The increasing convergence of AR and VR with artificial intelligence and IoT technologies is fostering smart display solutions with adaptive features. This includes context-aware brightness control, gesture recognition, and immersive content delivery, enhancing user engagement. European tech firms are spearheading research in these domains, leveraging AMOLED microdisplays as core components in next-generation devices.

- •Sustainability is emerging as a critical market trend, with manufacturers focusing on eco-friendly materials and energy-efficient AMOLED microdisplays. Regulatory pressures and consumer expectations drive adoption of green manufacturing practices. This trend is influencing supply chain decisions and promoting circular economy initiatives within the display industry.

- •Collaborations between display manufacturers and semiconductor companies are intensifying to optimize AMOLED microdisplay integration with advanced chipsets. This partnership facilitates improved display performance, reduced latency, and enhanced power management, vital for AR/VR and wearable applications. Such strategic alliances are shaping competitive dynamics and accelerating technology adoption.

- •The Europe market is witnessing diversification of applications beyond traditional electronics into sectors like automotive HUDs and medical imaging devices. This expansion is driven by the unique advantages of AMOLED microdisplays in delivering high contrast and low latency visuals under varied environmental conditions. Companies are tailoring products to meet sector-specific requirements, fueling market evolution.

- •Investment in miniaturization and resolution enhancement of AMOLED microdisplays continues to be a focal trend. Improving pixel density while maintaining low power consumption is critical for competitive differentiation. This trend drives continuous innovation in display architecture and materials science within Europe's AMOLED ecosystem.

- •The rise of local manufacturing initiatives in Europe aims to reduce dependency on imports and improve supply chain resilience. Governments and private stakeholders are supporting domestic AMOLED production capabilities, fostering regional economic growth and technological sovereignty.

Market Opportunities

- •Advancements in flexible AMOLED microdisplays present significant growth opportunities for manufacturers targeting wearable and foldable device markets. The ability to conform to diverse form factors opens new product categories and user experiences, enabling companies to capture emerging consumer segments. Innovation in flexible substrates and encapsulation technologies can reduce production costs and improve durability, enhancing competitive positioning.

- •Expanding applications in military and defense sectors for night vision, heads-up displays, and situational awareness systems offer lucrative opportunities. With increasing defense budgets and modernization programs across Europe, AMOLED microdisplay suppliers can capitalize on demand for rugged, high-performance display solutions tailored to harsh operational environments.

- •Growth in medical imaging and healthcare wearables utilizing AMOLED microdisplays offers a promising avenue for market expansion. Enhanced visualization capabilities and compact designs improve diagnostic accuracy and patient monitoring, creating demand for specialized display technologies. Collaborations with healthcare providers and research institutions can accelerate product development and adoption.

- •Emergence of smart automotive applications such as augmented reality heads-up displays and driver assistance systems drive AMOLED microdisplay integration. The automotive industry's shift towards connected and autonomous vehicles creates demand for advanced display technologies that improve safety and user experience, providing new revenue streams.

- •The rising trend of digital transformation and Industry 4.0 initiatives across European manufacturing sectors increases demand for immersive visualization tools powered by AMOLED microdisplays. Industrial AR applications for maintenance, training, and design review expand market potential. Investments in smart factories and automation further support this growth trajectory.

- •Government incentives and funding programs promoting research and innovation in display technologies offer financial support for AMOLED microdisplay development. Participation in European Union frameworks and public-private partnerships enables companies to accelerate R&D and commercialization efforts, reducing market entry barriers.

- •Increasing consumer preference for premium electronic devices with superior display quality creates opportunities for differentiation through AMOLED microdisplay features such as high contrast, color accuracy, and energy efficiency. Leveraging brand reputation and marketing strategies focused on display performance can enhance market share.

Market Challenges

- •High manufacturing costs associated with AMOLED microdisplays, especially flexible and transparent variants, pose significant barriers to widespread adoption. Complex fabrication processes, expensive raw materials, and yield challenges increase product pricing, limiting penetration in cost-sensitive segments. Addressing these cost issues requires technological innovation and scale economies.

- •Supply chain disruptions and dependency on key component suppliers affect production continuity and delivery timelines. European manufacturers face challenges securing consistent quality and volume of OLED materials and substrates, impacting market growth. Geopolitical tensions and logistics constraints exacerbate these vulnerabilities.

- •Technical limitations such as limited display lifespan, susceptibility to burn-in, and degradation under high brightness conditions restrict AMOLED microdisplay performance. These issues necessitate ongoing R&D investment to improve durability and reliability, influencing product acceptance in critical applications like medical and defense sectors.

- •Stringent regulatory requirements related to environmental sustainability, chemical usage, and electronic waste management impose compliance burdens on manufacturers. Navigating diverse European country-specific regulations increases operational complexities and costs, requiring robust compliance frameworks and reporting mechanisms.

- •The competitive threat from alternative display technologies such as microLED and advanced LCDs challenges AMOLED microdisplay market share. These alternatives offer benefits like longer lifespan and cost advantages in certain applications, compelling AMOLED vendors to accelerate innovation and differentiation strategies.

- •Talent shortages in specialized OLED manufacturing and materials science constrain capacity expansion and innovation in Europe. Attracting and retaining skilled professionals is critical to sustaining technological leadership and meeting growing market demand.

- •Market fragmentation and diverse customer requirements across European countries complicate standardization and scale efficiencies. Tailoring products to varied regulatory and consumer preferences demands flexible manufacturing and agile business models, increasing complexity.

Regulatory Framework

- •Between 2020 and 2025, the European Union implemented the Restriction of Hazardous Substances (RoHS) Directive updates, imposing stricter limits on hazardous chemicals in electronic displays, including AMOLED microdisplays. These regulations require manufacturers to comply with material restrictions, influencing product design and supply chain management, thereby enhancing environmental sustainability.

- •The Waste Electrical and Electronic Equipment (WEEE) Directive revisions enforced between 2021 and 2025 mandate improved collection, recycling, and recovery targets for electronic devices across Europe. AMOLED microdisplay producers and distributors must adhere to these requirements, promoting circular economy practices and reducing e-waste generation.

- •Energy-related Products (ErP) Directive updates in 2023 introduced efficiency standards for electronic display devices, encouraging development of energy-saving AMOLED microdisplays. Compliance with these standards is critical for market access and aligns with Europe’s climate goals.

- •Country-specific mandates such as Germany’s ElektroG and France’s DEEE regulations complement EU directives by enforcing stricter electronic waste handling and producer responsibilities. These policies impact manufacturing and distribution strategies for AMOLED microdisplays within these countries.

- •The European Green Deal framework fosters innovation through funding and policy support targeting sustainable electronic manufacturing. Initiatives launched between 2022 and 2025 facilitate research into eco-friendly display materials and production methods, enhancing the AMOLED microdisplay market’s alignment with environmental objectives.

Market Intelligence

- •15th January 2025, AMS AG announced the launch of a new flexible AMOLED microdisplay series designed for next-generation wearable devices, featuring reduced power consumption and enhanced durability. This launch addresses rising demand in healthcare and fitness tracking markets across Europe, positioning AMS AG as a technological leader. The displays integrate advanced encapsulation materials that improve lifespan under dynamic bending conditions. This initiative reflects AMS AG's strategic focus on innovation and sustainability, aiming to capture expanding wearable segments. Source: Official AMS AG Press Release

- •10th March 2025, Microoled unveiled a high-resolution transparent AMOLED microdisplay tailored for automotive heads-up display applications. The product offers superior contrast and visibility under varying lighting conditions, meeting stringent automotive industry standards. The innovation enables enhanced driver safety and user interaction with augmented reality overlays. Microoled’s collaboration with leading European automotive manufacturers underpins commercialization efforts, reinforcing market position. This launch exemplifies the convergence of display technology with automotive digital transformation trends. Source: Microoled Corporate Announcement

- •22nd May 2025, Koninklijke Philips N.V. announced a strategic partnership with a major European semiconductor company to develop integrated AMOLED microdisplay solutions for AR and VR devices. This collaboration aims to accelerate product development cycles and optimize display-chipset performance, enhancing user experience. The partnership leverages combined expertise in optics and semiconductor technology, targeting consumer electronics and industrial applications. This initiative is expected to strengthen Philips’ market presence and foster innovation in Europe’s AMOLED ecosystem. Source: Philips Official News

- •5th August 2025, Sony Corporation launched an advanced monochrome AMOLED microdisplay optimized for military night vision systems. The product features enhanced brightness and contrast with low power consumption suitable for tactical applications. Sony’s investment in this niche reflects growing defense sector demand in Europe for high-performance, compact display solutions. The launch is part of a broader strategy to expand Sony’s footprint in specialized display markets, providing technological differentiation and competitive advantage. Source: Sony Corporate Release

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.2 Billion |

| CAGR | 12.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Scope of Report | Market is segmented by Amoled Microdisplay Type (Active Matrix Amoled Microdisplays, Passive Matrix Amoled Microdisplays, Flexible Amoled Microdisplays, Transparent Amoled Microdisplays, Monochrome Amoled Microdisplays), Application Segment (Augmented Reality (AR) Displays, Virtual Reality (VR) Displays, Wearable Devices, Military & Defense Displays, Consumer Electronics), Display Technology (Rigid AMOLED Technology, Flexible AMOLED Technology, Transparent AMOLED Technology), End-User Industry (Healthcare & Medical Devices, Automotive Industry, Gaming & Entertainment, Industrial & Commercial Applications) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | AMS AG (Austria), Koninklijke Philips N.V. (Netherlands), Sony Corporation (Germany), Nanosys Inc. (France), Valeo (France), Himax Technologies (UK), Kopin Corporation (Germany), LG Display Europe (Belgium), Microoled (France), eMagin Corporation (UK), Carl Zeiss AG (Germany), Syndiant (Ireland), JDI Europe (UK), BOE Technology Group (Germany), Panasonic Europe (Germany), Samsung Display Europe (Germany), Innolux Corporation (France), Visteon Corporation (UK), Epistar Europe (Germany), Seiko Epson Corporation (UK), Canon Europe (UK), Sharp Corporation (Germany), Sony Europe (France), AU Optronics Europe (Germany), Toshiba Europe (UK) |

Europe Amoled Microdisplay Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.