North America Aluminum Alloy Automotive Die Castings Market Size, Growth & Revenue 2025-2034

North America Aluminum Alloy Automotive Die Castings Market is segmented by Alloy Type (ADC12 Aluminum Alloy, A356 Aluminum Alloy, A380 Aluminum Alloy, 6061 Aluminum Alloy, Other Aluminum Alloys), Automotive Application (Engine Components, Transmission Components, Structural Parts, Chassis Components, Electrical Components), Casting Process Technology (High Pressure Die Casting, Low Pressure Die Casting, Gravity Die Casting, Squeeze Casting), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

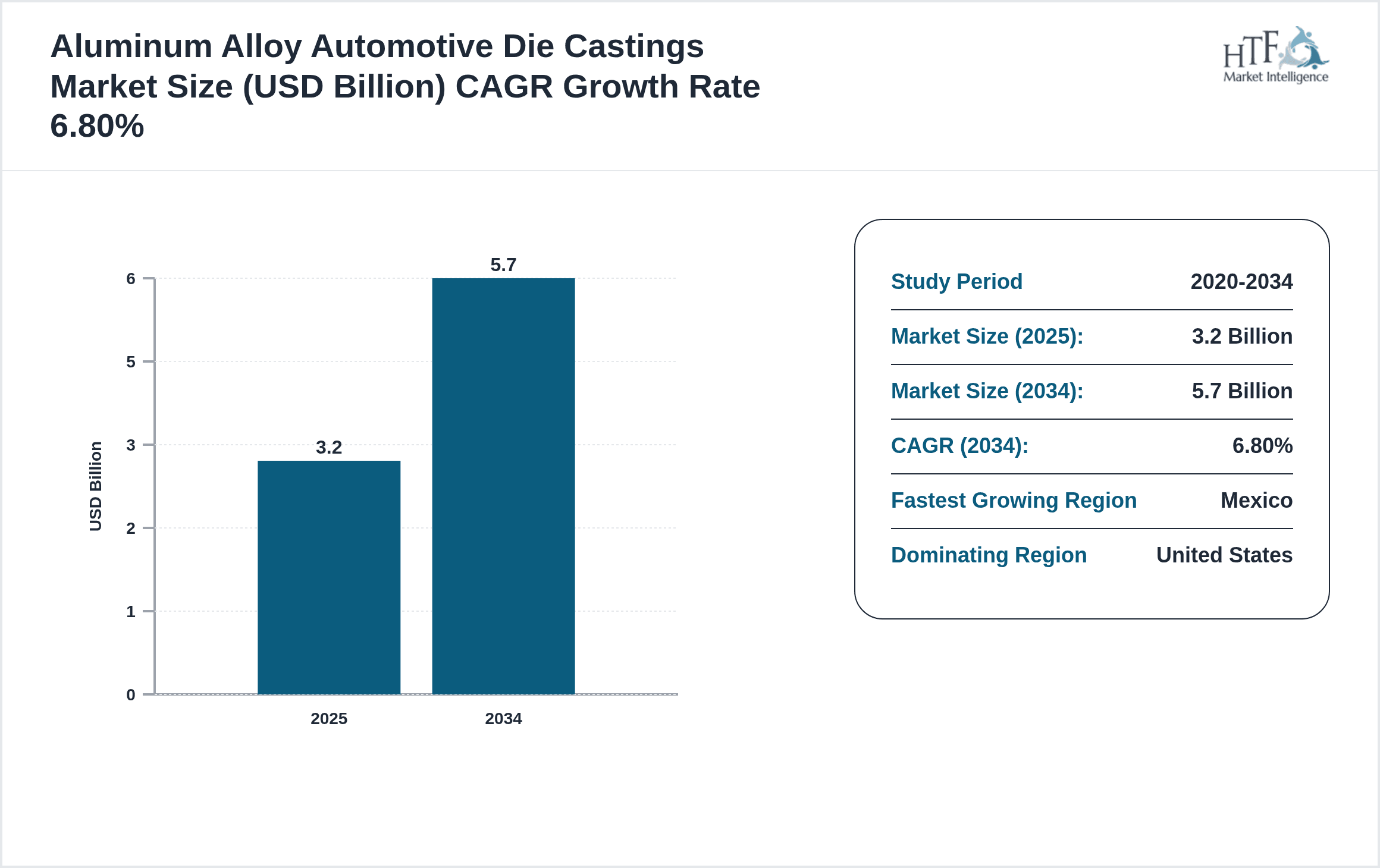

- •The North America Aluminum Alloy Automotive Die Castings market is a vital segment of the automotive manufacturing industry, focusing on producing lightweight, high-strength aluminum components through die casting technology. This market includes diverse alloy types such as ADC12, A356, A380, and 6061, which are engineered to meet stringent automotive performance, safety, and environmental standards. The components manufactured serve critical functions across engine, transmission, chassis, structural, and electrical applications, contributing significantly to vehicle weight reduction and enhanced fuel economy. Increasing adoption of aluminum alloys is propelled by regulatory mandates on emission reduction and the automotive industry's shift towards electric and hybrid vehicles, where lightweight materials are paramount. The market base size in 2025 stands at USD 3.2 billion, forecasted to grow at a CAGR of 6.8% through 2034, reaching USD 5.7 billion. The United States dominates the regional market due to its robust automotive manufacturing infrastructure, while Mexico is the fastest growing country owing to expanding manufacturing investments and export activities. Key players in this market deploy advanced die casting technologies and focus on innovation for improved product quality and cost efficiency. Challenges such as high raw material costs and complex manufacturing processes persist but are mitigated by ongoing technological advancements and strategic partnerships. Overall, the North America Aluminum Alloy Automotive Die Castings market represents a growth-oriented landscape driven by automotive lightweighting trends, evolving vehicle architectures, and stringent emission regulations.

- •The market highlights include a solid growth trajectory with a CAGR of 6.8% between 2025 and 2034, driven by the accelerating demand for aluminum die castings in passenger and commercial vehicles. The increasing penetration of electric vehicles (EVs) in North America further amplifies demand for lightweight aluminum components to extend battery range and efficiency. Market drivers such as regulatory pressure on fuel economy, rising adoption of advanced aluminum alloys like 6061, and the expansion of automotive manufacturing hubs in Mexico support robust market expansion. The competitive landscape is shaped by established die casting manufacturers and automotive component suppliers investing in capacity addition and process innovations to reduce cycle time and improve surface finish. The market’s strategic importance is underscored by its contribution to sustainability goals and cost optimization in vehicle production, making it a critical focus area for automakers and suppliers alike.

- •This market offers substantial value propositions to stakeholders across the automotive value chain, including OEMs, Tier-1 suppliers, and raw material providers. The lightweight nature of aluminum die castings facilitates compliance with stringent emission norms while enhancing vehicle performance and safety. Investors and manufacturers gain strategic advantage by leveraging innovations in alloy composition and die casting processes, enabling production of complex geometries with superior mechanical properties. The North America region’s well-established automotive ecosystem, complemented by free trade agreements and growing EV adoption, creates lucrative opportunities for growth and expansion. Furthermore, the integration of Industry 4.0 technologies in die casting operations enhances productivity, quality control, and sustainability, fortifying the market’s future outlook.

Competitive Landscape

The competitive environment of the North America Aluminum Alloy Automotive Die Castings market is marked by intense rivalry among established global die casting firms and regional specialists. Key competitive strategies include continuous technological innovation to improve casting precision, reduce cycle times, and develop high-performance aluminum alloys tailored for automotive applications. Market participants focus on strategic partnerships and collaborations with automakers to co-develop components aligned with evolving vehicle architectures, especially electric and autonomous vehicles. Mergers and acquisitions play a pivotal role in consolidating market share, expanding geographical footprint, and enhancing product portfolios. Pricing strategies are influenced by raw material cost fluctuations and competitive bids from OEMs seeking cost-effective lightweighting solutions. The adoption of Industry 4.0 practices and automation in manufacturing processes provides competitive advantages through improved operational efficiency and product quality. Regional competition is pronounced between the United States and Mexico, driven by manufacturing incentives, labor cost differentials, and export capabilities. Future competitive trends suggest increased emphasis on sustainability, recyclability of aluminum alloys, and integration of digital casting simulation technologies to optimize product development and reduce time-to-market.

Prominent Players in North America Aluminum Alloy Automotive Die Castings Market

- •Alcoa Corporation (United States)

- •Constellium SE (United States)

- •Nemak, S.A.B. de C.V. (Mexico)

- •Ryobi Die Casting Inc. (United States)

- •Wisconsin Aluminum Foundry Group (United States)

- •Gonzalez Die Casting Co. Inc. (United States)

- •SHILOH Industries, Inc. (United States)

- •Dynacast International Inc. (United States)

- •Metals USA (United States)

- •Signicast Investment Casting Group (United States)

- •Honsel North America Inc. (United States)

- •Pace Industries (United States)

- •Aleris International Inc. (United States)

- •Maudlin Products Inc. (United States)

- •Teksid Aluminum (United States)

- •Howmet Aerospace Inc. (United States)

- •Harvey Aluminum (United States)

- •Cedar Creek Aluminum (United States)

- •Dynacast (United States)

- •Bocar Group (Mexico)

- •Pillar Technologies Inc. (Canada)

- •ALMCO Group (Canada)

- •Lindsay Manufacturing (United States)

- •Kent Automotive (United States)

- •CNC Automation Inc. (United States)

Market Breakdown

- •By Alloy Type

- ◦ADC12 Aluminum Alloy

- ◦A356 Aluminum Alloy

- ◦A380 Aluminum Alloy

- ◦6061 Aluminum Alloy

- ◦Other Aluminum Alloys

- •By Automotive Application

- ◦Engine Components

- ◦Transmission Components

- ◦Structural Parts

- ◦Chassis Components

- ◦Electrical Components

- •By Casting Process Technology

- ◦High Pressure Die Casting

- ◦Low Pressure Die Casting

- ◦Gravity Die Casting

- ◦Squeeze Casting

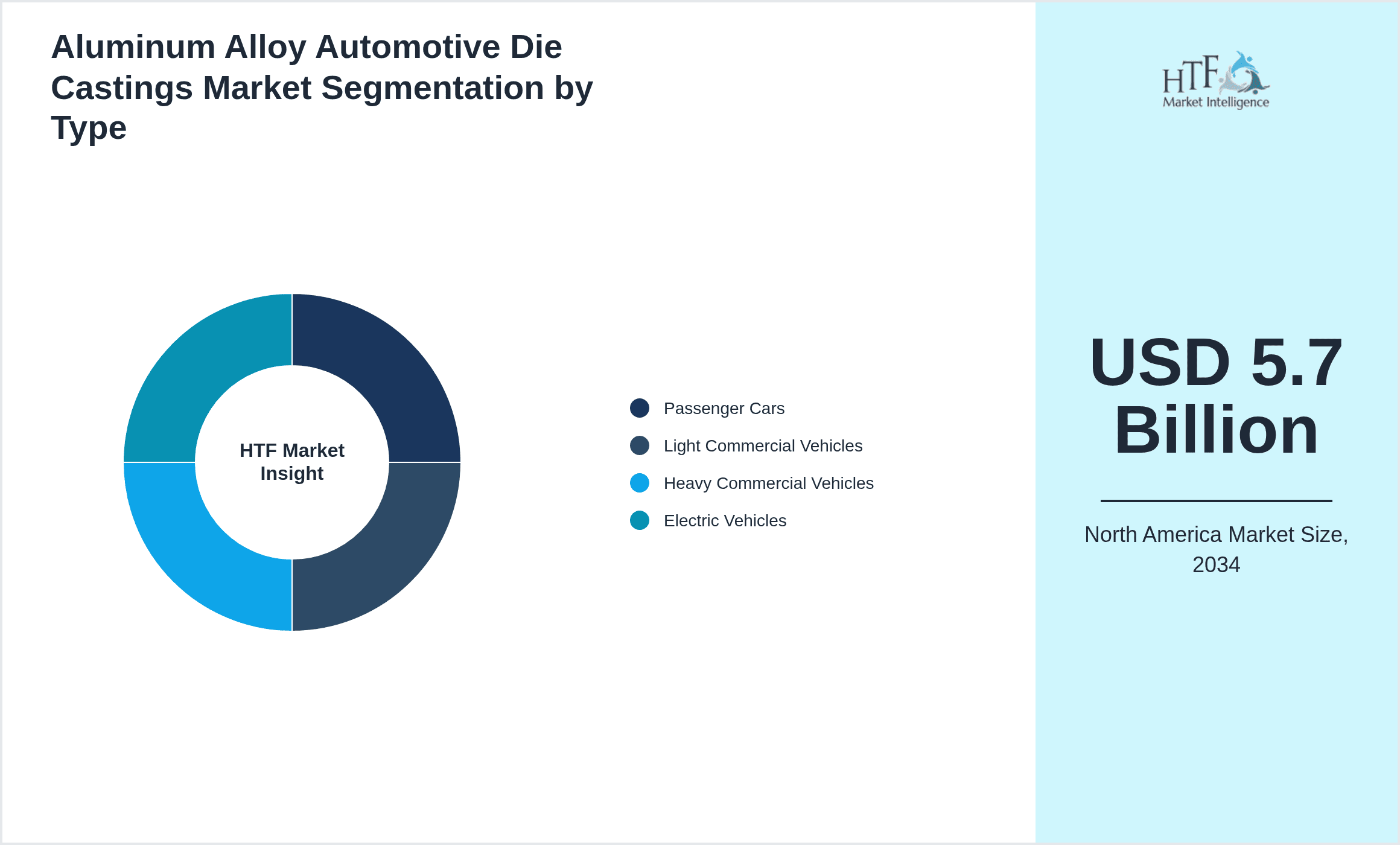

- •By Vehicle Type

- ◦Passenger Cars

- ◦Light Commercial Vehicles

- ◦Heavy Commercial Vehicles

- ◦Electric Vehicles

Growth Dynamics

The North America Aluminum Alloy Automotive Die Castings market is propelled by increasing demand for lightweight automotive components to improve fuel efficiency and reduce emissions. Regulatory mandates such as the Corporate Average Fuel Economy (CAFE) standards drive automakers to adopt aluminum alloys in engine and structural parts. Technological advancements in die casting processes, including high-pressure and squeeze casting, enable production of complex, high-strength parts at scale, enhancing market growth. The rising penetration of electric vehicles in the region necessitates lightweight battery housings and chassis components, further expanding aluminum die casting usage. Additionally, cost optimization efforts and supply chain localization by manufacturers support increased adoption of aluminum alloys over traditional steel. The expansion of automotive manufacturing hubs in Mexico, supported by favorable trade agreements, also contributes to growth momentum. Market players investing in R&D to develop new alloys and process innovations strengthen the market’s competitive edge and growth prospects.

Market Trends

A prominent trend in the North America Aluminum Alloy Automotive Die Castings market is the increasing integration of lightweight aluminum components in electric vehicles, driven by the need to maximize battery efficiency and driving range. Automakers are progressively replacing steel parts with aluminum alloys, focusing on advanced alloys like 6061 which offer superior strength-to-weight ratios. Digitalization and Industry 4.0 adoption in die casting manufacturing are enhancing process control and product quality, reducing defects and cycle times. Collaborations between alloy producers and automotive OEMs to co-develop specialized aluminum alloys tailored for specific vehicle applications are gaining traction. Furthermore, sustainability considerations are fostering innovations in recyclable aluminum alloys and energy-efficient casting processes, aligning with global emission reduction targets.

Market Opportunities

The North America Aluminum Alloy Automotive Die Castings market presents significant growth opportunities in the expanding electric vehicle segment, where lightweight and durable aluminum components are critical. Emerging applications in autonomous and connected vehicles require complex die cast parts with integrated functionalities, opening avenues for advanced casting technologies. Investment in developing new aluminum alloys with enhanced mechanical properties and corrosion resistance can capture untapped market segments. Geographical expansion into growing automotive manufacturing zones in Mexico offers opportunities for cost-effective production and export. Additionally, increasing aftermarket demand for replacement die cast components provides a steady revenue stream. Strategic partnerships and joint ventures focused on innovation and capacity expansion can accelerate market penetration and profitability.

Market Challenges

Key challenges facing the North America Aluminum Alloy Automotive Die Castings market include the volatility of aluminum raw material prices, which directly impacts manufacturing costs and profitability. The complexity of die casting processes requires significant capital investment in advanced machinery and skilled workforce, posing entry barriers for smaller players. Quality control issues such as porosity and dimensional inaccuracies can lead to increased scrap rates and warranty claims, affecting customer trust. Environmental regulations necessitate stringent adherence to emission and waste management standards during casting operations, increasing compliance costs. Furthermore, competition from alternative lightweight materials like magnesium alloys and composites presents substitution risks. Supply chain disruptions and trade policy uncertainties also pose challenges to consistent market growth.

Regulatory Framework

Between 2020 and 2025, the North America Aluminum Alloy Automotive Die Castings market has been influenced by several key regulations aimed at reducing automotive emissions and enhancing fuel economy. The Corporate Average Fuel Economy (CAFE) standards, updated in 2021, mandate stricter average fuel efficiency targets for new vehicles, encouraging the adoption of lightweight materials such as aluminum alloys. The Environmental Protection Agency (EPA) regulations enforce limits on manufacturing emissions and waste disposal during die casting operations, compelling manufacturers to implement cleaner production technologies. The Occupational Safety and Health Administration (OSHA) imposes rigorous safety standards in die casting plants to protect workers from exposure to high temperatures and molten metals. Additionally, the US Department of Energy’s initiatives promote energy-efficient manufacturing processes, incentivizing investments in advanced die casting machinery. Trade policies under the United States-Mexico-Canada Agreement (USMCA) facilitate regional supply chain integration, impacting market dynamics. Compliance with these regulations ensures sustainable growth and competitive advantage for market participants.

Market Intelligence

- •15th February 2025, Alcoa Corporation announced the launch of its new high-strength aluminum alloy ADC12 variant designed specifically for automotive die casting applications. This alloy offers enhanced tensile strength and corrosion resistance while maintaining lightweight properties crucial for electric vehicle components. The product aims to reduce vehicle weight by up to 10%, thereby improving fuel efficiency and battery range. The launch is supported by strategic collaborations with major North American automotive OEMs to integrate the alloy into engine and chassis parts. This initiative underscores Alcoa’s commitment to innovation and sustainability in the automotive supply chain. Source: Alcoa Corporation Official Press Release

- •10th June 2025, Nemak, S.A.B. de C.V. unveiled its advanced high-pressure die casting facility in Monterrey, Mexico, equipped with Industry 4.0 technologies for real-time process monitoring and quality control. The plant focuses on manufacturing aluminum alloy components for electric and commercial vehicles, aiming to increase production capacity by 25% by 2027. Nemak’s investment aligns with growing demand for lightweight automotive parts in North America and supports regional manufacturing expansion under USMCA guidelines. This development enhances Nemak’s competitive positioning and supply chain resilience. Source: Nemak Corporate Website

- •20th September 2025, Constellium SE announced a strategic partnership with a leading automotive OEM to co-develop 6061 aluminum alloy die cast components for next-generation electric vehicle platforms. The collaboration focuses on optimizing alloy composition and casting processes to achieve superior mechanical properties and manufacturing efficiency. Pilot production runs commenced at Constellium’s North American facilities, targeting commercialization by 2026. This partnership exemplifies the trend of close OEM-supplier collaboration to accelerate lightweighting and performance improvements. Source: Constellium Investor Relations

- •5th December 2025, Ryobi Die Casting Inc. completed the acquisition of a regional aluminum casting supplier in Canada, expanding its footprint and enhancing product offerings in the North American automotive market. The acquisition enables Ryobi to integrate advanced casting technologies and broaden its alloy portfolio to meet evolving automotive standards. This strategic move is expected to drive revenue growth and operational synergies, reinforcing Ryobi’s market leadership. Source: Ryobi Die Casting Press Release

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Mexico is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.2 Billion |

| Forecast Year Market Size | USD 5.7 Billion |

| CAGR | 6.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.6% |

| Scope of Report | Market is segmented by Alloy Type (ADC12 Aluminum Alloy, A356 Aluminum Alloy, A380 Aluminum Alloy, 6061 Aluminum Alloy, Other Aluminum Alloys), Automotive Application (Engine Components, Transmission Components, Structural Parts, Chassis Components, Electrical Components), Casting Process Technology (High Pressure Die Casting, Low Pressure Die Casting, Gravity Die Casting, Squeeze Casting), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Alcoa Corporation (United States), Constellium SE (United States), Nemak, S.A.B. de C.V. (Mexico), Ryobi Die Casting Inc. (United States), Wisconsin Aluminum Foundry Group (United States), Gonzalez Die Casting Co. Inc. (United States), SHILOH Industries, Inc. (United States), Dynacast International Inc. (United States), Metals USA (United States), Signicast Investment Casting Group (United States), Honsel North America Inc. (United States), Pace Industries (United States), Aleris International Inc. (United States), Maudlin Products Inc. (United States), Teksid Aluminum (United States), Howmet Aerospace Inc. (United States), Harvey Aluminum (United States), Cedar Creek Aluminum (United States), Dynacast (United States), Bocar Group (Mexico), Pillar Technologies Inc. (Canada), ALMCO Group (Canada), Lindsay Manufacturing (United States), Kent Automotive (United States), CNC Automation Inc. (United States) |

North America Aluminum Alloy Automotive Die Castings Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.