China Propylene Oxide Market Size, Growth & Revenue 2025-2034

China Propylene Oxide Market is segmented by Type (Liquid Propylene Oxide, Gas Propylene Oxide, Other Types), Application (Polyurethane Foams, Propylene Glycol, Epichlorohydrin, Surfactants, Others), End User (Automotive, Construction, Electronics, Packaging, Textiles), Production Technology (Chlorohydrin Process, Hydroperoxide Process, Other Technologies), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Propylene Oxide Market is a critical segment of the country's chemical manufacturing industry, involved in producing a versatile chemical intermediate used in many end-use applications such as polyurethane foams, propylene glycol, and surfactants. The market encompasses multiple production technologies including the chlorohydrin and hydroperoxide processes, which underpin the supply chain dynamics and product quality. Regional production hubs like East China dominate the landscape due to established infrastructure and proximity to downstream industries. This market is influenced by regulatory frameworks, technological advancements, and growing demand from automotive, construction, electronics, and packaging sectors, reflecting China's broader industrial growth and sustainability goals. Market participants focus on innovation in production efficiency, cost-effectiveness, and environmental compliance to maintain competitive advantage. The market is anticipated to expand steadily, driven by increasing industrial applications and government support aimed at green chemical production.

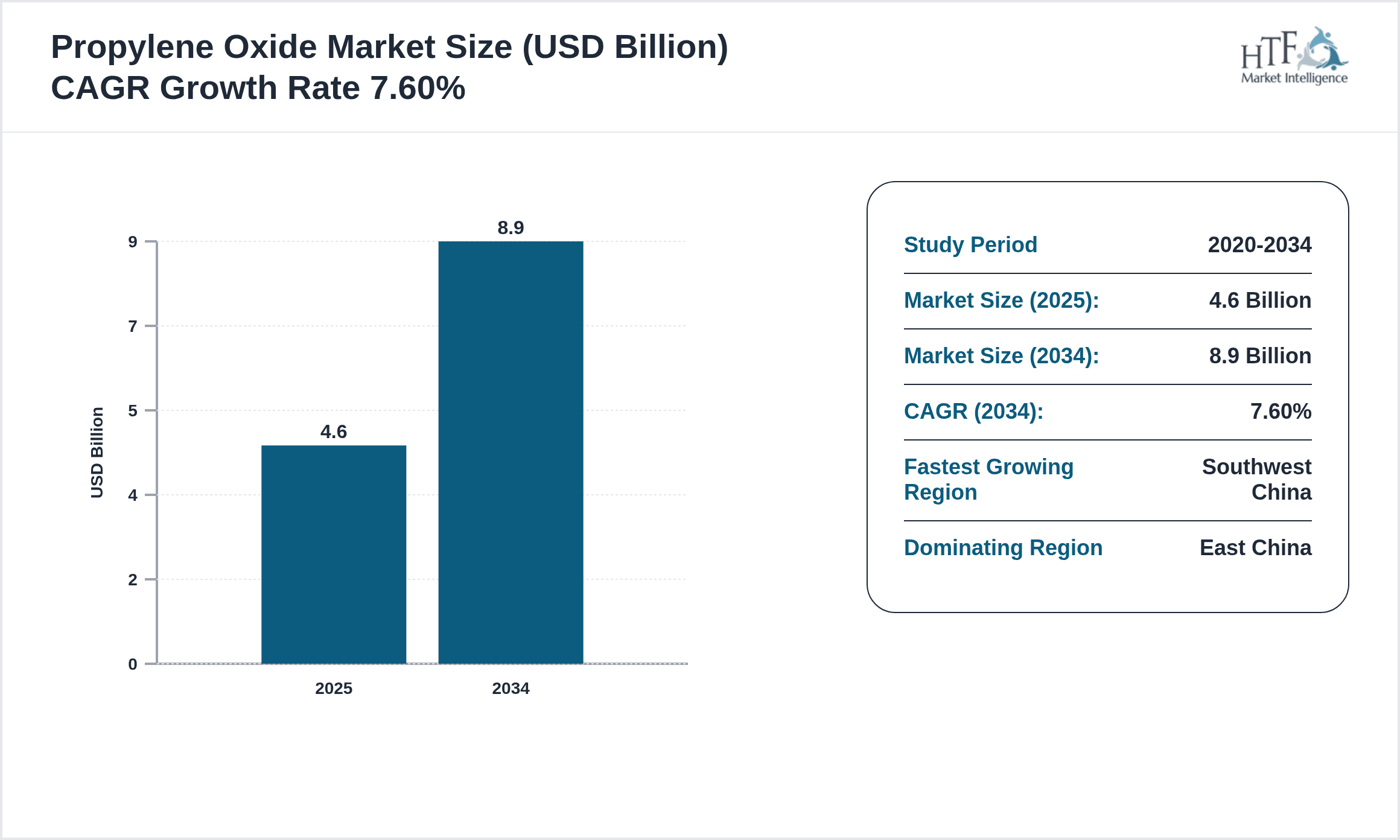

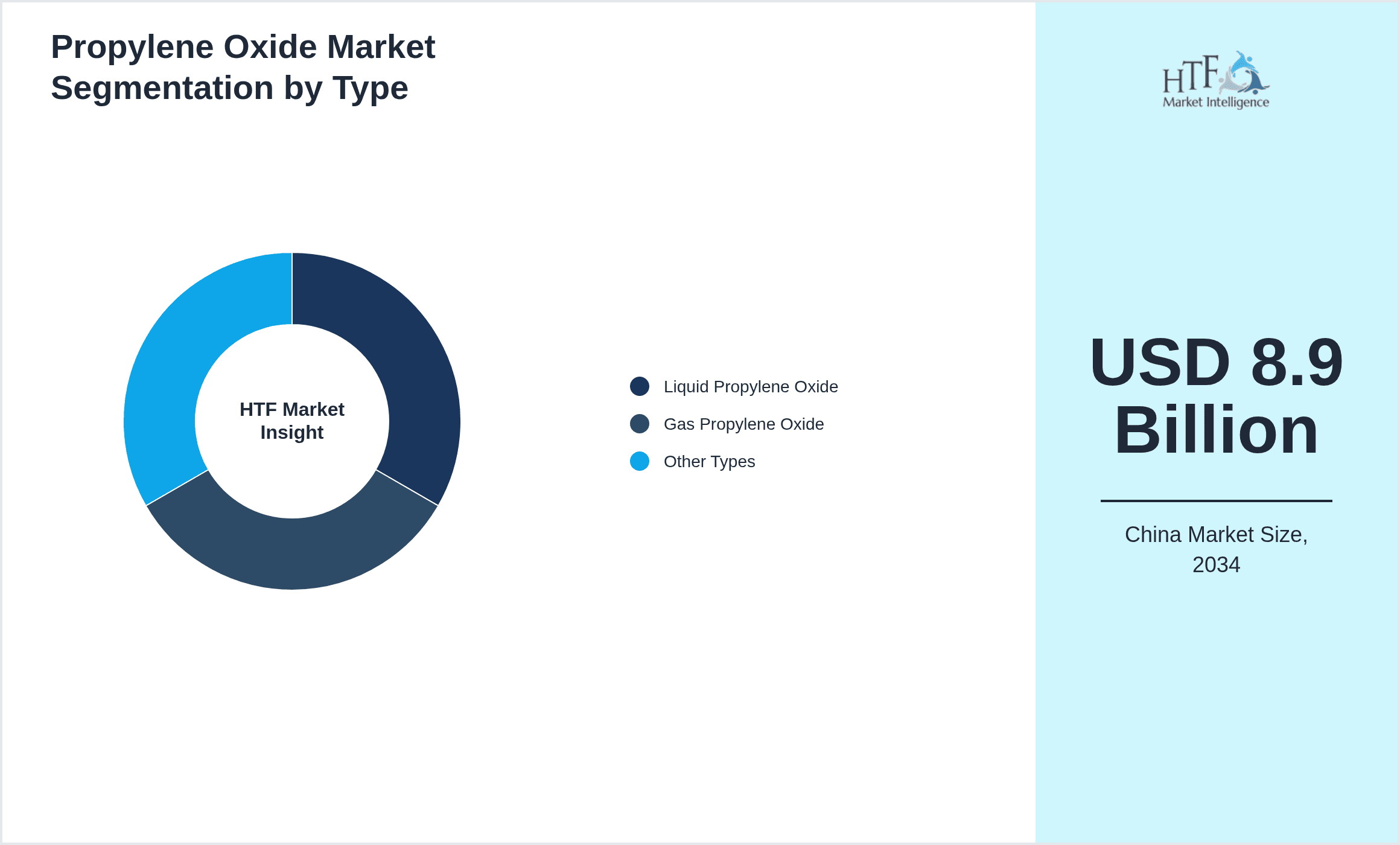

- •China’s propylene oxide market is valued at USD 4.6 billion in 2025 and is forecast to reach USD 8.9 billion by 2034, reflecting a robust CAGR of 7.6%. East China holds the largest market share at 35%, with Southwest China emerging as the fastest growing region at a CAGR of 9.2%. Liquid propylene oxide remains the leading product type due to its widespread industrial applications, while gas propylene oxide is gaining traction due to improved production methods. Key market drivers include government initiatives promoting chemical industry modernization, strategic partnerships between domestic and international players, and technological innovations enhancing production efficiencies. Despite challenges such as high capital costs and environmental regulations, the market outlook remains positive with significant opportunities in emerging end-use sectors and advanced production technologies.

- •The China Propylene Oxide Market presents significant value proposition for chemical manufacturers, industrial users, and investors by enabling diversified application use and fostering sustainable chemical production practices. As the backbone of polyurethane and other derivative products, it supports expanding industries such as automotive manufacturing and construction materials. Strategic importance lies in its role as a chemical intermediate that integrates advanced process technologies with evolving regulatory standards. Stakeholders benefit from ongoing innovations, regional market expansions, and evolving consumer demand patterns that align with China’s industrial growth and environmental policies. This market is positioned for long-term growth, driven by the synergy between technological advancements and a broadening application landscape.

Competitive Landscape

The China Propylene Oxide Market is characterized by intense competition among domestic chemical producers and multinational corporations aiming to capitalize on the country’s expanding industrial base. Market players emphasize technological innovation, cost efficiency, and environmental compliance to differentiate themselves. Strategic partnerships and joint ventures are common to secure feedstock supply and enhance production capacity. Competition is also driven by the adoption of advanced hydroperoxide processes, which offer cleaner and more efficient production compared to traditional chlorohydrin methods. Pricing strategies are influenced by raw material availability and government policies regulating emissions and safety standards. Regional competition among industrial zones such as East China and South China further shapes market dynamics, encouraging local investments in infrastructure and capacity expansion. Future trends point toward consolidation, increased R&D investments, and the integration of sustainable manufacturing practices as key competitive factors.

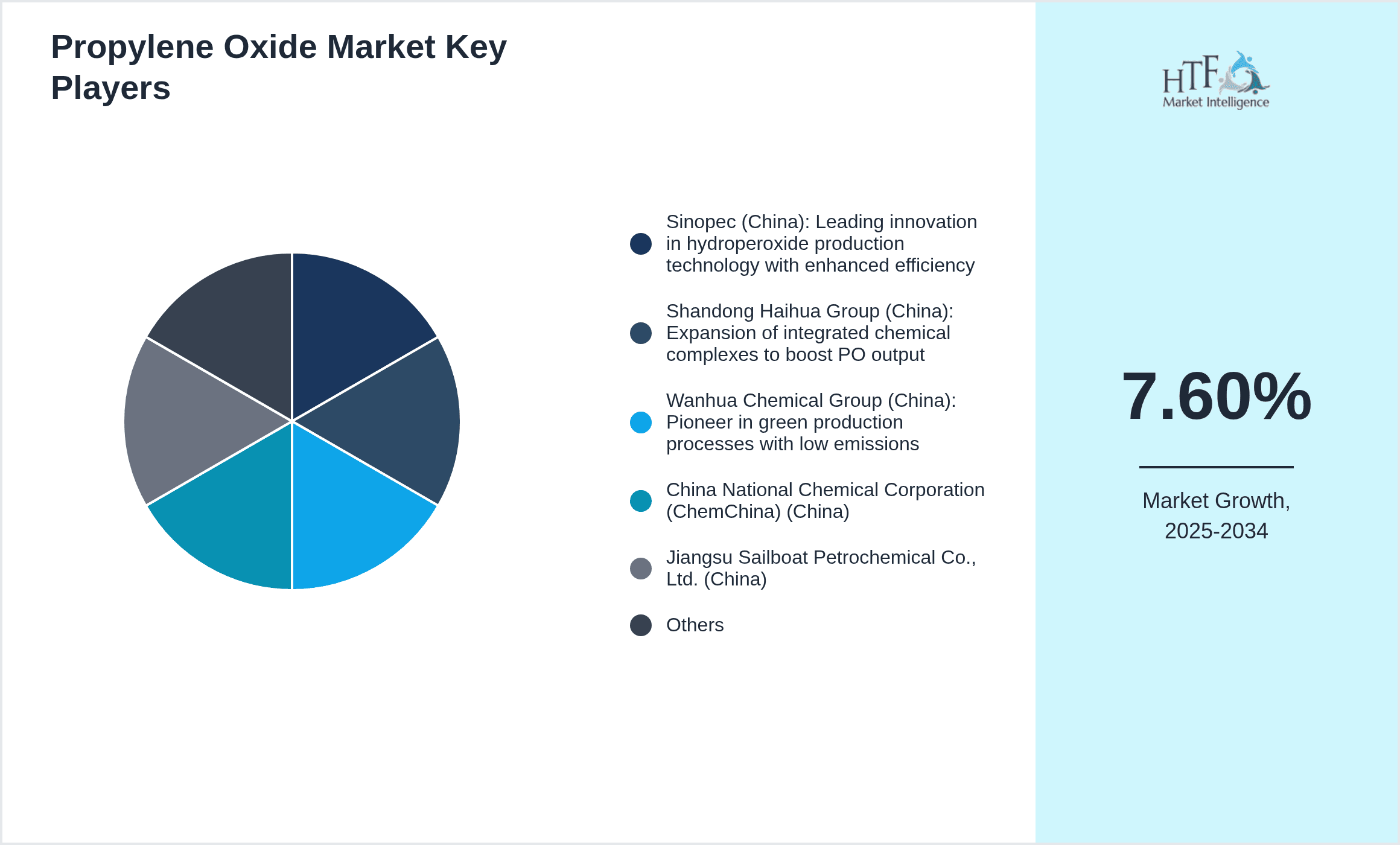

Leading Companies in China Propylene Oxide Market

- •Sinopec (China): Leading innovation in hydroperoxide production technology with enhanced efficiency

- •Shandong Haihua Group (China): Expansion of integrated chemical complexes to boost PO output

- •Wanhua Chemical Group (China): Pioneer in green production processes with low emissions

- •China National Chemical Corporation (ChemChina) (China)

- •Jiangsu Sailboat Petrochemical Co., Ltd. (China)

- •Liaoning Bora Enterprise Group Co., Ltd. (China)

- •Yantai Wanhua Polyurethanes Co., Ltd. (China)

- •Shenzhen Jinchang Chemical Co., Ltd. (China)

- •Qingdao Hengyuan Chemical Co., Ltd. (China)

- •Tianjin Bohai Chemical Industry Group Co., Ltd. (China)

- •Anhui Wanwei Group Co., Ltd. (China)

- •Zhejiang Fuchunjiang Environmental Science & Technology Co., Ltd. (China)

- •Shanghai SECCO Petrochemical Co., Ltd. (China)

- •Hebei Jinlong Chemical Co., Ltd. (China)

- •Ningbo Zhongsheng Chemical Co., Ltd. (China)

- •Suzhou Huanri Chemical Co., Ltd. (China)

- •Shandong Yulong Chemical Co., Ltd. (China)

- •Hebei Zifeng Chemical Industry Co., Ltd. (China)

- •Zhonghao Chenguang Research Institute of Chemical Industry (China)

- •China Petroleum & Chemical Co., Ltd. (China)

- •Hebei Huaao Chemical Co., Ltd. (China)

- •Lianyungang Zhongji Chemical Co., Ltd. (China)

- •Jiangsu Yangnong Chemical Group Co., Ltd. (China)

- •Shandong Hualu Hengsheng Chemical Co., Ltd. (China)

- •Zhejiang Qianjiang Petrochemical Co., Ltd. (China)

Market Breakdown

- •By Type

- ◦Liquid Propylene Oxide

- ◦Gas Propylene Oxide

- ◦Other Types

- •By Application

- ◦Polyurethane Foams

- ◦Propylene Glycol

- ◦Epichlorohydrin

- ◦Surfactants

- ◦Others

- •By End User

- ◦Automotive

- ◦Construction

- ◦Electronics

- ◦Packaging

- ◦Textiles

- •By Production Technology

- ◦Chlorohydrin Process

- ◦Hydroperoxide Process

- ◦Other Technologies

Growth Dynamics

- •Strong government support through regulations incentivizing cleaner chemical production has accelerated adoption of advanced hydroperoxide technologies, enhancing market growth.

- •Strategic partnerships between domestic chemical producers and global firms have boosted capacity expansion and technology transfer, strengthening competitive positioning.

- •Technological innovations focused on energy efficiency and emissions reduction have lowered production costs and improved operational performance across key manufacturing hubs.

- •The rising demand for polyurethane products in automotive and construction sectors is driving propylene oxide consumption, supporting sustained market expansion.

- •Increased investment in regional chemical parks, especially in East and South China, is providing infrastructure advantages and supply chain efficiencies.

- •Emerging applications such as eco-friendly surfactants and advanced packaging materials are creating new growth avenues for propylene oxide producers.

- •Government policies aimed at reducing environmental impact are encouraging manufacturers to adopt sustainable production practices, enhancing market appeal.

Market Trends

- •The shift from chlorohydrin to hydroperoxide process is a prominent trend, driven by environmental regulations and efficiency gains, supported by leading manufacturers.

- •Integration of digital technologies and automation in PO production is enhancing process control and reducing downtime, increasing operational reliability.

- •Expansion of downstream industries such as automotive polyurethane seating and insulation materials is fueling propylene oxide demand growth.

- •Sustainability initiatives have spurred development of bio-based propylene oxide alternatives and recycling technologies within China’s chemical sector.

- •Collaborative ventures between chemical producers and research institutes are accelerating innovation cycles and product development.

- •Market segmentation is becoming more specialized, with tailored PO grades for specific industrial applications gaining traction.

- •China’s regional industrial policies are encouraging localized production hubs, optimizing logistics and reducing carbon footprint.

Market Opportunities

- •Expanding the use of propylene oxide in emerging sectors like electronics and advanced packaging presents significant growth potential for producers.

- •Adoption of next-generation hydroperoxide technologies could offer cost and environmental advantages, enabling market penetration in new regions such as Southwest China.

- •Investment in R&D for bio-based propylene oxide production opens avenues for sustainable product lines aligned with global green chemistry trends.

- •Strategic expansion of integrated chemical parks in underserved sub-regions provides logistical benefits and access to regional demand centers.

- •Enhanced collaboration between government and industry to streamline regulatory approvals may expedite capacity additions and innovation rollout.

- •Development of customized PO derivatives for niche applications offers differentiation and higher-margin opportunities.

- •Growing domestic demand for eco-friendly polyurethane products supports the expansion of propylene oxide-based raw materials.

Market Challenges

- •High capital investment requirements and complex production processes limit new entrants and expansion pace in the propylene oxide market.

- •Strict environmental regulations increase compliance costs and operational complexity, particularly for chlorohydrin-based production facilities.

- •Raw material price volatility, especially for propylene feedstock, creates uncertainty in production margins and pricing strategies.

- •Infrastructure disparities between regional zones affect logistics efficiency and supply chain reliability across China.

- •Market adoption barriers exist due to fragmented downstream industries and varying quality requirements for propylene oxide derivatives.

- •Competition from imported propylene oxide and substitutes challenges domestic manufacturers’ market share and profitability.

- •Talent shortages and technical expertise gaps hinder rapid technology adoption and process optimization.

Regulatory Framework

- •The Air Pollution Prevention and Control Action Plan (2015-2025) mandates strict emission controls on chemical plants including propylene oxide producers, driving cleaner production methods since 2015.

- •China’s Environmental Protection Tax Law, implemented in 2018, imposes taxes on pollutant emissions, incentivizing manufacturers to upgrade facilities and reduce environmental impact.

- •The Chemical Industry Safety Regulations (updated 2019) require rigorous safety compliance and risk management protocols for PO production, enforcing stringent operational standards.

- •Regional policies in East China and South China promote green manufacturing zones with subsidies and support for hydroperoxide process adoption, effective since 2020.

- •Government initiatives under the 14th Five-Year Plan emphasize sustainable chemical industry development, supporting innovation and capacity expansion in environmentally friendly technologies.

Market Intelligence

- •15th March 2024, Sinopec launched a next-generation hydroperoxide production unit in East China, incorporating digital process controls and emissions reduction technology. This facility aims to increase propylene oxide output by 15% while reducing energy consumption by 10%, positioning Sinopec as a leader in sustainable chemical manufacturing. The innovation is expected to support growing demand from automotive polyurethane sectors and strengthen Sinopec’s regional supply chain. Source: Sinopec Official Press Release

- •2nd May 2024, Wanhua Chemical Group announced a strategic expansion of its integrated chemical complex in South China to include advanced PO derivative production lines. This expansion targets eco-friendly surfactants and specialty propylene glycol products, responding to increasing market demand for green chemicals. The initiative is backed by government incentives and aims to double production capacity by 2026, enhancing Wanhua’s competitive edge in premium chemical markets. Source: Wanhua Chemical Group Press Statement

- •20th August 2024, Shandong Haihua Group completed a joint venture with a European technology firm to deploy proprietary hydroperoxide catalyst systems in their North China facilities. This collaboration is set to improve PO yield by 8% and reduce hazardous waste by 12%, aligning with China’s environmental regulations. The partnership exemplifies the trend of technology transfer and localized innovation in the Chinese propylene oxide market, driving efficiency and sustainable growth. Source: Industry Publication Chemical Today

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.6 Billion |

| Forecast Year Market Size | USD 8.9 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.3% |

| Scope of Report | Market is segmented by Type (Liquid Propylene Oxide, Gas Propylene Oxide, Other Types), Application (Polyurethane Foams, Propylene Glycol, Epichlorohydrin, Surfactants, Others), End User (Automotive, Construction, Electronics, Packaging, Textiles), Production Technology (Chlorohydrin Process, Hydroperoxide Process, Other Technologies) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Sinopec (China), Shandong Haihua Group (China), Wanhua Chemical Group (China), China National Chemical Corporation (ChemChina) (China), Jiangsu Sailboat Petrochemical Co., Ltd. (China), Liaoning Bora Enterprise Group Co., Ltd. (China), Yantai Wanhua Polyurethanes Co., Ltd. (China), Shenzhen Jinchang Chemical Co., Ltd. (China), Qingdao Hengyuan Chemical Co., Ltd. (China), Tianjin Bohai Chemical Industry Group Co., Ltd. (China), Anhui Wanwei Group Co., Ltd. (China), Zhejiang Fuchunjiang Environmental Science & Technology Co., Ltd. (China), Shanghai SECCO Petrochemical Co., Ltd. (China), Hebei Jinlong Chemical Co., Ltd. (China), Ningbo Zhongsheng Chemical Co., Ltd. (China), Suzhou Huanri Chemical Co., Ltd. (China), Shandong Yulong Chemical Co., Ltd. (China), Hebei Zifeng Chemical Industry Co., Ltd. (China), Zhonghao Chenguang Research Institute of Chemical Industry (China), China Petroleum & Chemical Co., Ltd. (China), Hebei Huaao Chemical Co., Ltd. (China), Lianyungang Zhongji Chemical Co., Ltd. (China), Jiangsu Yangnong Chemical Group Co., Ltd. (China), Shandong Hualu Hengsheng Chemical Co., Ltd. (China), Zhejiang Qianjiang Petrochemical Co., Ltd. (China) |

China Propylene Oxide Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.