North America Tungsten Hexafluoride Market Scope & Changing Dynamics 2024-2034

North America Tungsten Hexafluoride Market is segmented by Type (Ultra-Pure Grade Tungsten Hexafluoride, Technical Grade Tungsten Hexafluoride, Industrial Grade Tungsten Hexafluoride, Electronic Grade Tungsten Hexafluoride, Reagent Grade Tungsten Hexafluoride), Application (Semiconductor Manufacturing, Chemical Processing, Optical Coatings, Research & Development, Others), End-User Industry (Electronics & Semiconductor Industry, Chemical Industry, Optical Industry, Academic & Research Institutions), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Sales Platforms), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

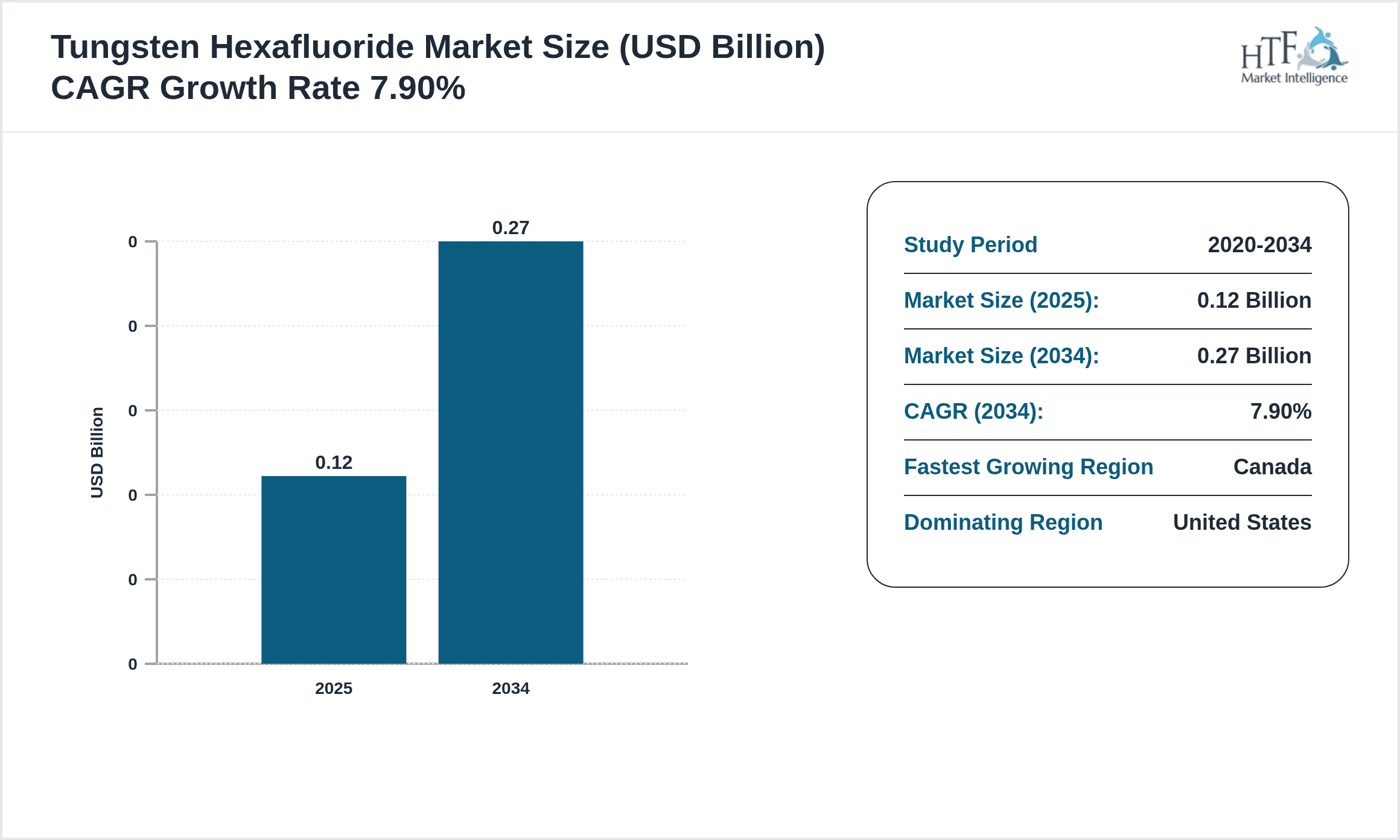

- •The North America Tungsten Hexafluoride Market represents a specialized chemical sector focused on the production, supply, and consumption of tungsten hexafluoride (WF6) within the United States, Canada, and Mexico. Tungsten hexafluoride is a volatile inorganic compound extensively utilized for its etching and deposition properties in semiconductor manufacturing, chemical processing, and optical coatings. The market boundaries cover various product grades such as ultra-pure, technical, industrial, electronic, and reagent grades, catering to diverse industrial applications. This market is driven by the flourishing semiconductor industry, which demands high-purity WF6 for chemical vapor deposition processes essential in integrated circuit fabrication. Additionally, the market’s scope includes R&D applications and emerging chemical uses, reflecting a broad industrial reliance on WF6. Industry participants are increasingly adopting sustainable production techniques and expanding their product portfolios to meet stringent regulatory standards and evolving customer requirements. The North American market benefits from advanced infrastructure and significant R&D investments, positioning it as a critical region for tungsten hexafluoride production and consumption. As technology adoption accelerates across electronics and chemical industries, the market is poised for substantial growth over the next decade, supported by innovation and strategic collaborations.

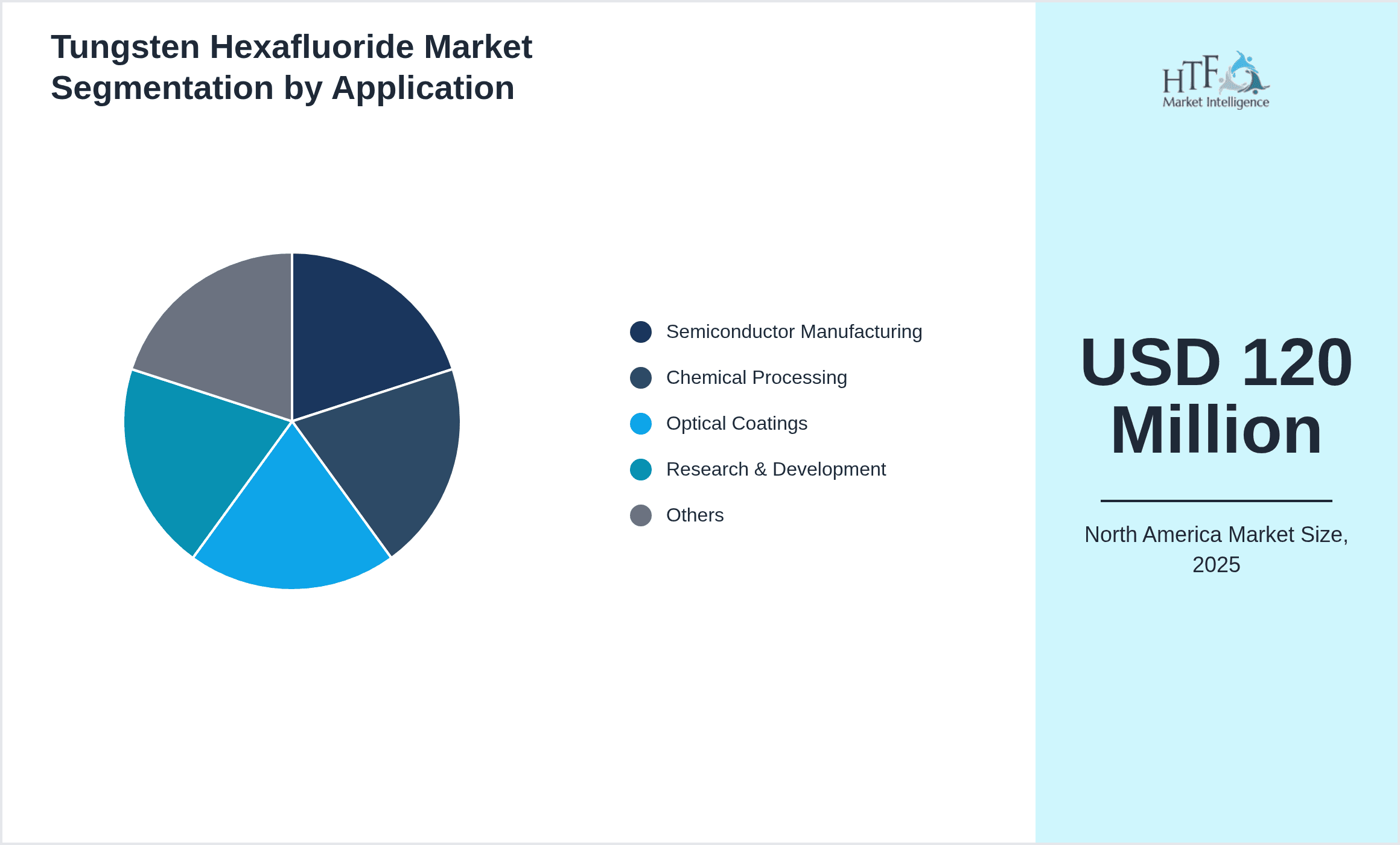

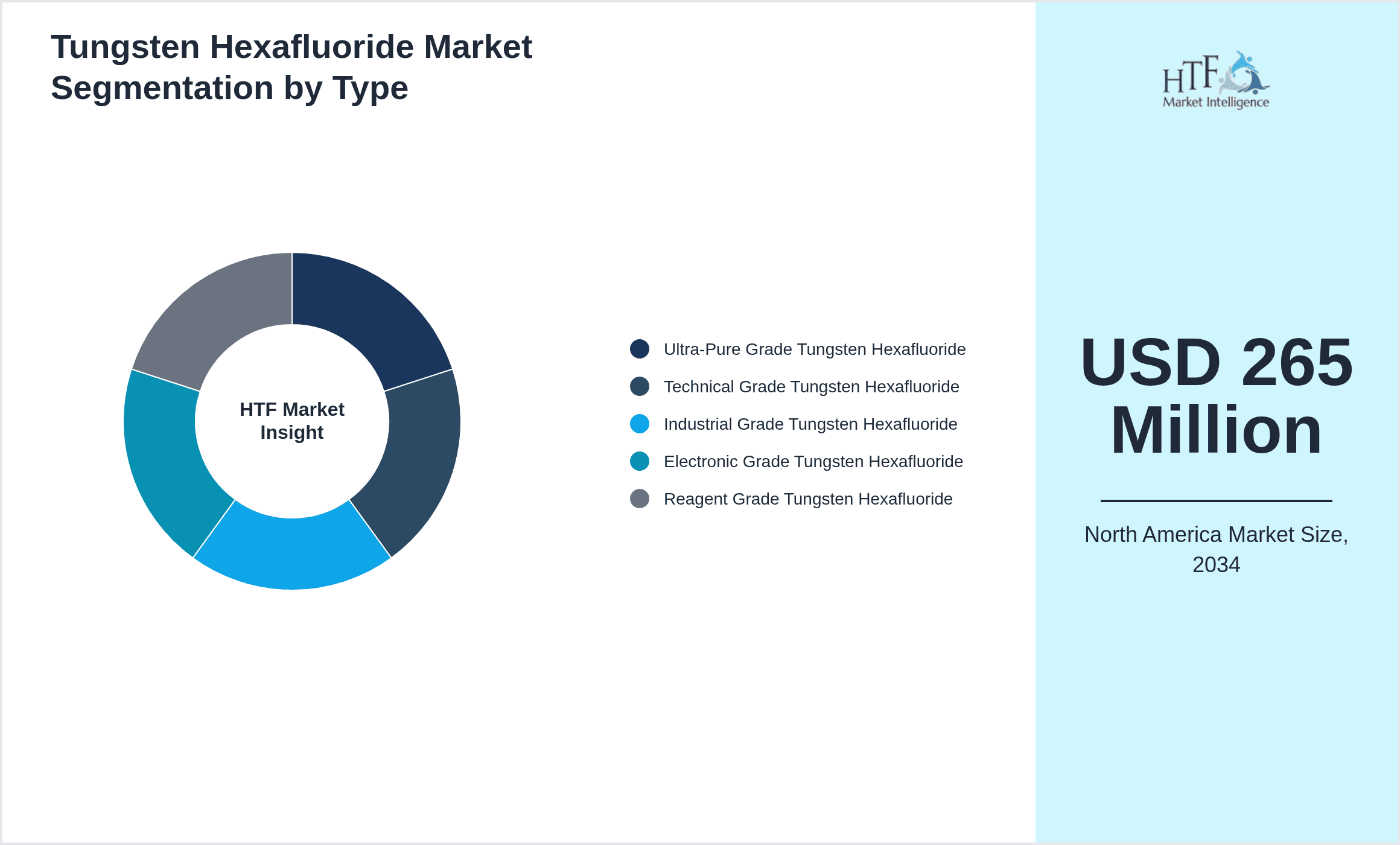

- •Key market highlights include a base market size of USD 120 Million in 2024, projected to grow to USD 265 Million by 2034, exhibiting a compound annual growth rate (CAGR) of approximately 7.9%. The United States dominates the regional market with a 60% share, driven by its extensive semiconductor manufacturing capacity and chemical processing industries. Canada represents the fastest-growing country within North America, with an anticipated CAGR of 11.2%, attributed to expanding electronics manufacturing and investments in advanced material research. Ultra-pure grade tungsten hexafluoride leads the product segment due to its critical role in semiconductor applications, while electronic grade is the fastest growing owing to emerging high-tech industries. Application-wise, semiconductor manufacturing holds the largest market share, followed by chemical processing. Market dynamics are influenced by technological advancements, stringent environmental regulations, and rising demand for electronic devices, making tungsten hexafluoride a vital industrial chemical in North America.

- •The North America Tungsten Hexafluoride Market offers significant value propositions to semiconductor manufacturers, chemical processors, and research institutions by providing essential high-purity chemicals necessary for advanced technological applications. The market’s strategic importance lies in supporting the region’s technology-driven industries, contributing to innovation in electronics, optics, and chemical synthesis. By ensuring a reliable supply of various WF6 grades, market participants enable efficient manufacturing processes, improved product quality, and compliance with environmental and safety standards. Additionally, the market supports regional economic growth through job creation, R&D investments, and collaborations with technology providers. Stakeholders including manufacturers, distributors, and end-users benefit from ongoing advancements and tailored solutions, positioning the market as a cornerstone for sustainable industrial progress in North America.

Competitive Landscape

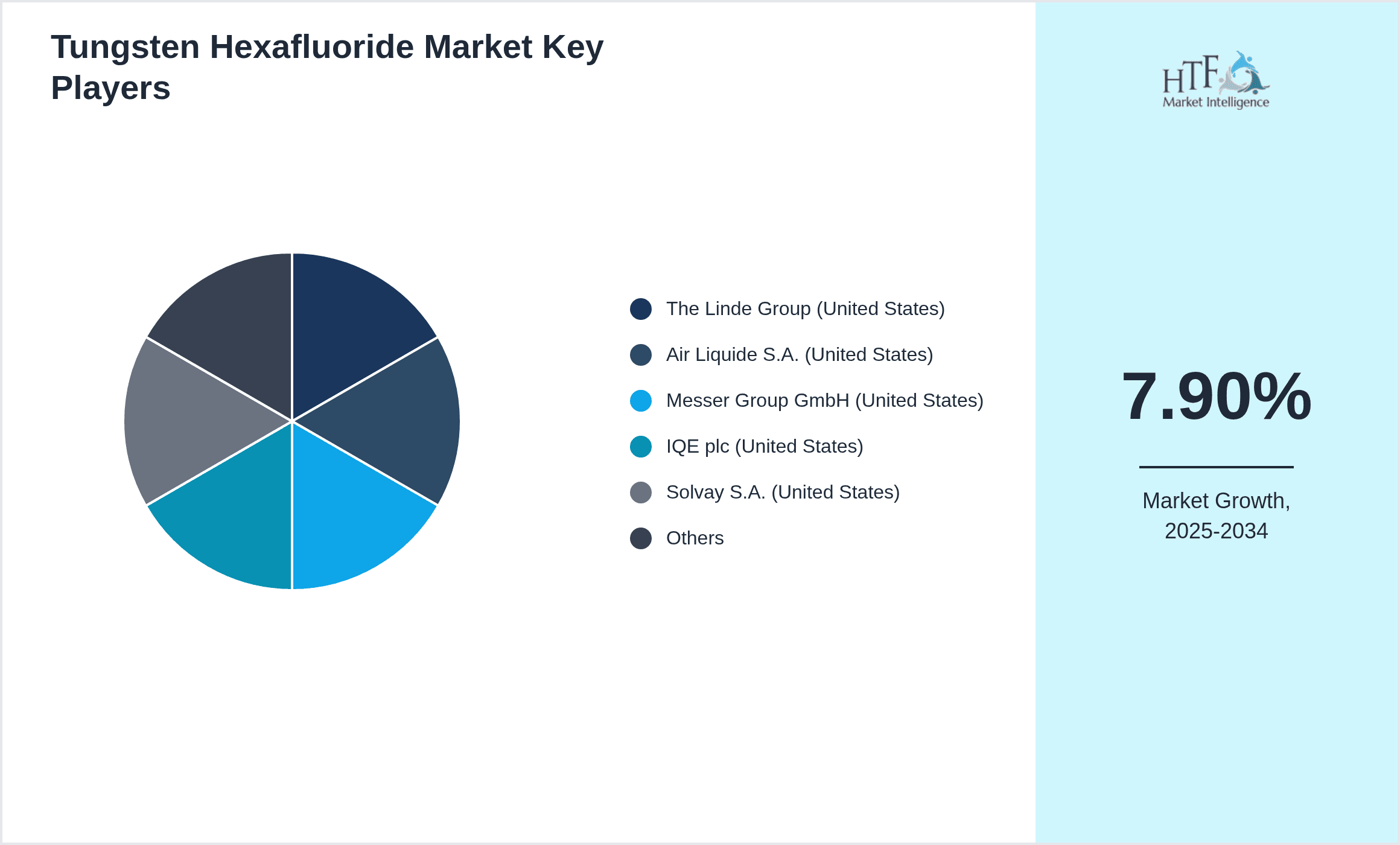

The competitive landscape of the North America Tungsten Hexafluoride Market is characterized by a mix of multinational chemical corporations, regional specialty chemical producers, and emerging technology innovators. Market players compete through continuous innovation in product purity, cost optimization, and process efficiency, aiming to cater to the stringent requirements of semiconductor and chemical processing industries. Strategic partnerships and collaborations with semiconductor fabs and research institutions are common, enabling customization and rapid product development. Companies focus on expanding production capacities and geographic reach within North America to capture growing demand. Pricing strategies are influenced by raw material costs and regulatory compliance expenses, while differentiation is achieved through superior product quality and technical support. The rivalry intensifies as new entrants leverage advanced manufacturing technologies and sustainable practices. Market entry barriers include high capital investment, regulatory approvals, and the need for specialized production facilities. Future competitive trends indicate increasing consolidation, adoption of green chemistry principles, and integration of digital manufacturing technologies to enhance supply chain responsiveness and product traceability.

Leading Companies in Tungsten Hexafluoride Market

- •The Linde Group (United States)

- •Air Liquide S.A. (United States)

- •Messer Group GmbH (United States)

- •IQE plc (United States)

- •Solvay S.A. (United States)

- •Honeywell International Inc. (United States)

- •Taiyo Nippon Sanso Corporation (United States)

- •Mitsubishi Chemical Corporation (United States)

- •Matheson Tri-Gas, Inc. (United States)

- •Showa Denko K.K. (United States)

- •Air Products and Chemicals, Inc. (United States)

- •Dongwoo Fine-Chem Co., Ltd. (United States)

- •Heraeus Holding GmbH (United States)

- •Linde Canada ULC (Canada)

- •Air Liquide Canada Inc. (Canada)

- •Messer Canada Inc. (Canada)

- •Taiyo Nippon Sanso Corporation Canada (Canada)

- •Matheson Tri-Gas Canada (Canada)

- •Praxair Canada Inc. (Canada)

- •Air Products Canada Ltd. (Canada)

- •Messer Mexico (Mexico)

- •Air Liquide Mexico (Mexico)

- •Praxair Mexico (Mexico)

- •Linde Mexico (Mexico)

- •Air Products Mexico (Mexico)

Market Breakdown

- •By Type

- ◦Ultra-Pure Grade Tungsten Hexafluoride

- ◦Technical Grade Tungsten Hexafluoride

- ◦Industrial Grade Tungsten Hexafluoride

- ◦Electronic Grade Tungsten Hexafluoride

- ◦Reagent Grade Tungsten Hexafluoride

- •By Application

- ◦Semiconductor Manufacturing

- ◦Chemical Processing

- ◦Optical Coatings

- ◦Research & Development

- ◦Others

- •By End-User Industry

- ◦Electronics & Semiconductor Industry

- ◦Chemical Industry

- ◦Optical Industry

- ◦Academic & Research Institutions

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Sales Platforms

Growth Dynamics

The North America Tungsten Hexafluoride market is propelled by the rapid expansion of the semiconductor manufacturing industry, which demands ultra-pure WF6 for chemical vapor deposition processes essential in integrated circuit fabrication. Increasing investments in advanced electronics and microchip production facilities augment demand significantly. Additionally, growing chemical processing applications utilizing WF6 as a fluorinating agent contribute to market growth. The push towards miniaturization and higher device performance drives the need for high-purity grades, stimulating innovation in product formulations. Furthermore, government incentives supporting semiconductor fabrication plants in the United States and Canada bolster market expansion. The increasing adoption of tungsten hexafluoride in optical coating technologies for lenses and mirrors also creates new growth avenues. Combined with rising R&D activities focusing on novel WF6 applications, these factors collectively fuel steady market growth throughout the forecast period.

Market Trends

A major trend in the North America Tungsten Hexafluoride market is the increasing focus on ultra-high purity WF6 production driven by semiconductor industry requirements. Manufacturers are adopting advanced purification technologies to meet stringent quality standards. Another notable trend is the integration of sustainable and environmentally responsible manufacturing processes to comply with tightening regulations and reduce hazardous emissions. The regional market is witnessing strategic collaborations between chemical producers and semiconductor fabs to co-develop customized WF6 grades tailored for specific applications. The rise of electric vehicle production and 5G infrastructure deployment further stimulates demand for advanced semiconductor components, indirectly benefiting WF6 consumption. Digitalization and automation in chemical manufacturing plants improve operational efficiency and enable real-time quality monitoring. These evolving market trends collectively reshape the competitive landscape and product development strategies in North America’s tungsten hexafluoride sector.

Market Opportunities

Significant opportunities in the North America Tungsten Hexafluoride Market arise from the expanding semiconductor fabrication capacity, especially with new fab constructions in the United States and Canada. The growing demand for next-generation electronics and IoT devices necessitates specialized WF6 grades, opening avenues for product innovation and premium offerings. Additionally, untapped applications in emerging chemical synthesis and optical equipment manufacturing present growth potential. Strategic partnerships with research institutions enable the development of novel WF6-based processes, creating market differentiation. The shift towards greener production technologies offers opportunities for companies investing in sustainable manufacturing methods. Geographic expansion within the region, particularly enhancing distribution networks in Mexico, can capture rising demand in industrial sectors. Furthermore, increasing government funding for advanced materials research supports market growth through collaborative projects and technology commercialization.

Market Challenges

The North America Tungsten Hexafluoride Market faces challenges related to the high cost of raw materials and complex purification processes required to achieve ultra-high purity standards. Regulatory compliance concerning hazardous chemical handling and environmental emissions imposes stringent operational constraints, increasing production costs. Supply chain disruptions and volatility in tungsten ore availability affect market stability. Additionally, the specialized nature of WF6 production demands substantial capital investment and technical expertise, limiting new entrants. Market growth is also hindered by competition from alternative fluorinating agents and evolving semiconductor manufacturing technologies that may reduce WF6 dependency. Fluctuating demand cycles in end-use industries such as electronics and chemical manufacturing introduce market unpredictability. Intellectual property protections and geopolitical factors influencing trade policies further complicate market dynamics, necessitating robust risk management strategies by market participants.

Regulatory Framework

Between 2019 and 2024, North America witnessed the implementation of several regulations impacting the tungsten hexafluoride market. The U.S. Environmental Protection Agency (EPA) enhanced its standards on hazardous air pollutants and chemical storage, requiring manufacturers to adopt advanced containment and emission control technologies. Canada’s Environmental Protection Act mandates rigorous reporting and compliance for fluorinated chemical substances, influencing WF6 handling and transportation protocols. Mexico introduced updated chemical safety regulations aligning with international standards, emphasizing worker safety and environmental protection. These regulations collectively elevate production costs but improve safety and sustainability. Industry players have responded by investing in cleaner technologies and process optimizations to meet compliance while maintaining market competitiveness. Ongoing regulatory developments continue to shape operational practices and product innovations in the North American tungsten hexafluoride industry.

Market Intelligence

- •15th January 2024, Air Liquide S.A. announced the launch of a new ultra-pure tungsten hexafluoride grade designed specifically for next-generation semiconductor manufacturing. This product features enhanced purity levels exceeding 99.9999%, optimized for advanced chemical vapor deposition processes. The launch aims to support semiconductor fabs focusing on 3nm and smaller node technologies, strengthening Air Liquide’s position in North America. The company emphasized the product’s low impurity profile and improved supply chain reliability, targeting major clients in the United States and Canada. This innovation aligns with increasing demand for high-performance materials in the region’s growing semiconductor sector. Source: Official Air Liquide Press Release

- •22nd July 2024, Linde Canada ULC expanded its tungsten hexafluoride production facility in Ontario, increasing capacity by 30% to meet rising demand from the electronics and chemical industries. The expansion included installation of state-of-the-art purification systems and emission control technologies adhering to Canadian environmental standards. Linde highlighted the investment as part of its strategic plan to strengthen supply chain resilience and improve delivery timelines across North America. The facility now supports a broader range of WF6 grades, including electronic and reagent grades, catering to diverse industrial applications. This development is expected to enhance Linde’s market share and foster innovation collaboration with regional semiconductor manufacturers. Source: Linde Canada Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 120 Million |

| Forecast Year Market Size | USD 265 Million |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Type (Ultra-Pure Grade Tungsten Hexafluoride, Technical Grade Tungsten Hexafluoride, Industrial Grade Tungsten Hexafluoride, Electronic Grade Tungsten Hexafluoride, Reagent Grade Tungsten Hexafluoride), Application (Semiconductor Manufacturing, Chemical Processing, Optical Coatings, Research & Development, Others), End-User Industry (Electronics & Semiconductor Industry, Chemical Industry, Optical Industry, Academic & Research Institutions), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Sales Platforms) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | The Linde Group (United States), Air Liquide S.A. (United States), Messer Group GmbH (United States), IQE plc (United States), Solvay S.A. (United States), Honeywell International Inc. (United States), Taiyo Nippon Sanso Corporation (United States), Mitsubishi Chemical Corporation (United States), Matheson Tri-Gas, Inc. (United States), Showa Denko K.K. (United States), Air Products and Chemicals, Inc. (United States), Dongwoo Fine-Chem Co., Ltd. (United States), Heraeus Holding GmbH (United States), Linde Canada ULC (Canada), Air Liquide Canada Inc. (Canada), Messer Canada Inc. (Canada), Taiyo Nippon Sanso Corporation Canada (Canada), Matheson Tri-Gas Canada (Canada), Praxair Canada Inc. (Canada), Air Products Canada Ltd. (Canada), Messer Mexico (Mexico), Air Liquide Mexico (Mexico), Praxair Mexico (Mexico), Linde Mexico (Mexico), Air Products Mexico (Mexico) |

North America Tungsten Hexafluoride Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.