Global Musculoskeletal Pain Treatment Market Size, Growth & Revenue 2024-2034

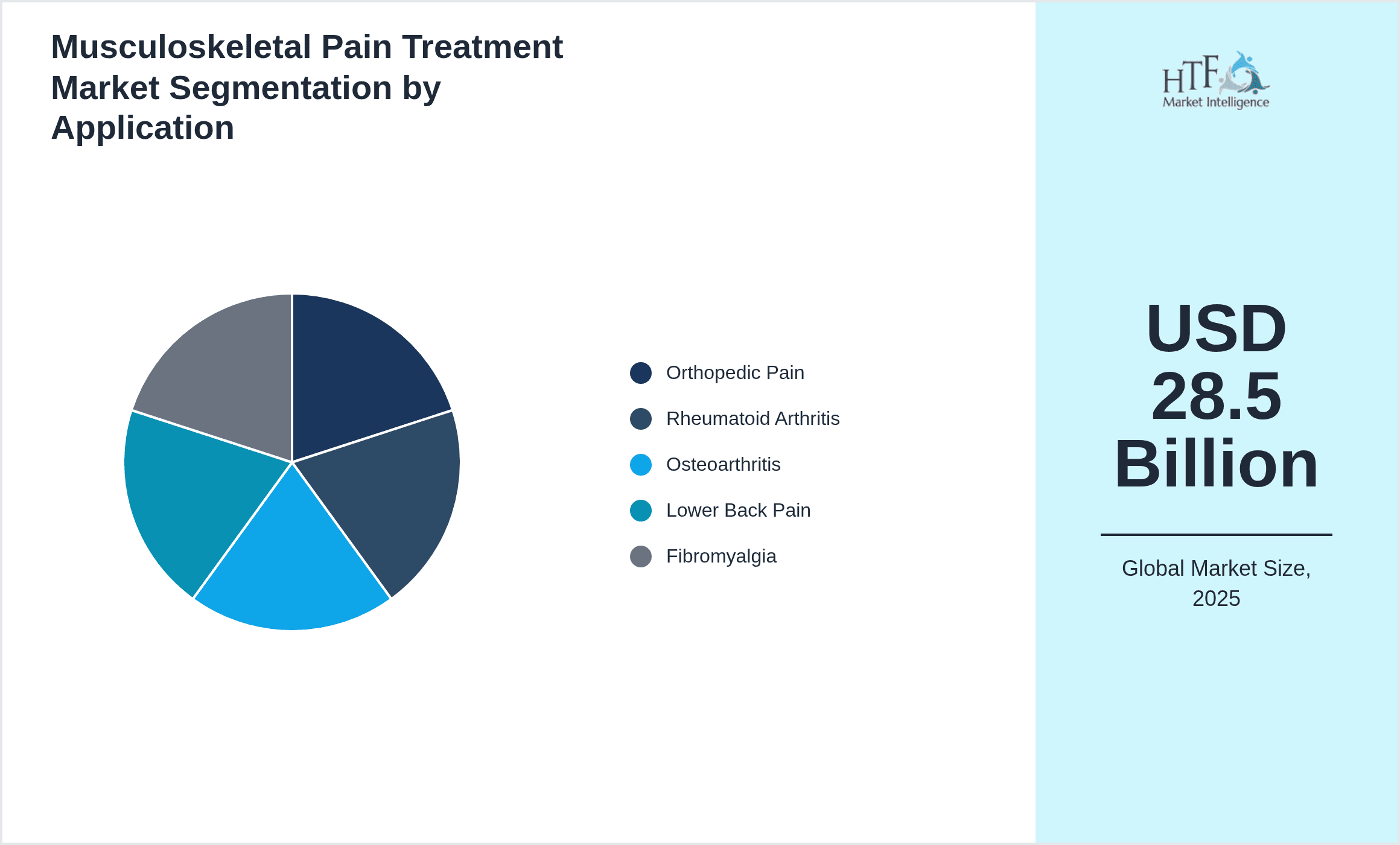

Global Musculoskeletal Pain Treatment Market is segmented by Treatment Type (Pharmacological Treatments (NSAIDs, Opioids, Analgesics), Non-Pharmacological Therapies (Physical Therapy, Acupuncture, Chiropractic Care), Surgical Interventions (Joint Replacement, Arthroscopy, Minimally Invasive Surgery), Biologics (Monoclonal Antibodies, Regenerative Medicine), Others (Complementary and Alternative Medicine)), Application Area (Orthopedic Pain, Rheumatoid Arthritis, Osteoarthritis, Lower Back Pain, Fibromyalgia), End User (Hospitals, Clinics, Outpatient Care Centers, Home Healthcare), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacy, Direct Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global musculoskeletal pain treatment market represents a vital segment within healthcare focused on managing pain arising from disorders such as osteoarthritis, rheumatoid arthritis, lower back pain, and fibromyalgia. This market comprises a broad range of treatment types including pharmacological options like NSAIDs and opioids, non-pharmacological therapies such as physiotherapy and acupuncture, surgical interventions involving joint replacements and minimally invasive techniques, as well as biologics including monoclonal antibodies and regenerative therapies. The industry serves diverse healthcare settings ranging from hospitals to outpatient clinics and homecare, addressing both acute and chronic pain management needs. Increasing prevalence of musculoskeletal conditions due to aging populations and lifestyle factors, coupled with technological advancements and rising healthcare expenditure globally, fuel market growth. Key characteristics include innovation in personalized therapies and integration of multidisciplinary medical approaches, with the market scope covering product development, therapeutic services, and supportive care technologies worldwide.

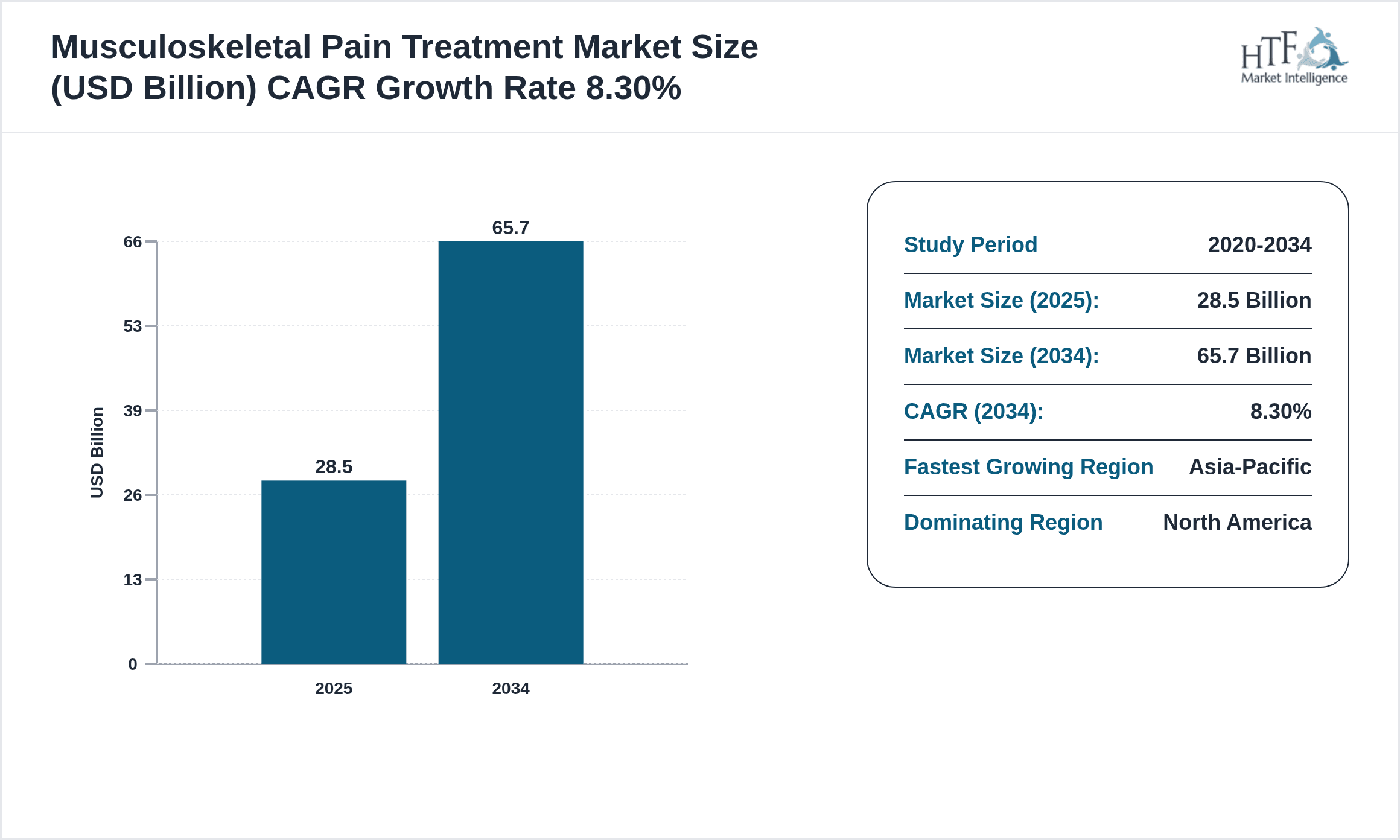

- •The market is projected to grow from USD 28.5 Billion in 2024 to USD 65.7 Billion by 2034, reflecting a CAGR of 8.3%. North America currently dominates with a 35% market share driven by advanced healthcare infrastructure and high adoption rates of innovative therapies. Asia-Pacific is the fastest-growing region, expanding at 11.2% CAGR due to increasing awareness, improving healthcare access, and rising prevalence of musculoskeletal disorders. Pharmacological treatments remain the largest segment, while biologics represent the fastest-growing product type, driven by advancements in biotechnology and personalized medicine. Key applications include orthopedic pain and osteoarthritis, with growing demand for non-invasive and combination therapies. Market dynamics are influenced by regulatory frameworks, reimbursement policies, and evolving patient preferences towards minimally invasive and integrative pain management solutions.

- •This market holds strategic importance for pharmaceutical companies, medical device manufacturers, biotechnology firms, healthcare providers, and payers. It offers significant value propositions through improved patient outcomes, enhanced quality of life, and reduction of healthcare costs associated with chronic pain management. Innovations in biologics and regenerative therapies open new avenues for disease-modifying treatments, while digital health tools and telemedicine expand access and monitoring capabilities. Stakeholders benefit from understanding regional market nuances, competitive landscapes, and regulatory trends to optimize product development, market entry, and investment strategies. The market’s growth trajectory underscores its critical role in addressing the global burden of musculoskeletal diseases, facilitating advancements in clinical care and therapeutic innovation across diverse healthcare ecosystems.

Competitive Landscape

The global musculoskeletal pain treatment market is highly competitive with numerous multinational pharmaceutical and medical device companies vying for market share through innovation, strategic partnerships, and geographic expansion. Companies focus heavily on research and development to introduce advanced biologics and minimally invasive surgical solutions that differentiate their product portfolios. Competitive strategies include mergers and acquisitions to consolidate market presence and expand therapeutic offerings. Pricing strategies are balanced with reimbursement policies to ensure accessibility and profitability. Distribution channels vary from hospital procurement to retail pharmacies and direct-to-consumer digital platforms. Innovation in drug delivery systems and personalized treatment approaches contribute to sustained rivalry. Market entry barriers such as regulatory approvals and high R&D costs limit new entrants, while established players leverage strong brand recognition and extensive distribution networks. Future trends suggest increasing collaboration between biotech firms and traditional pharma, emphasizing integrated care models to enhance patient outcomes and strengthen competitive positioning.

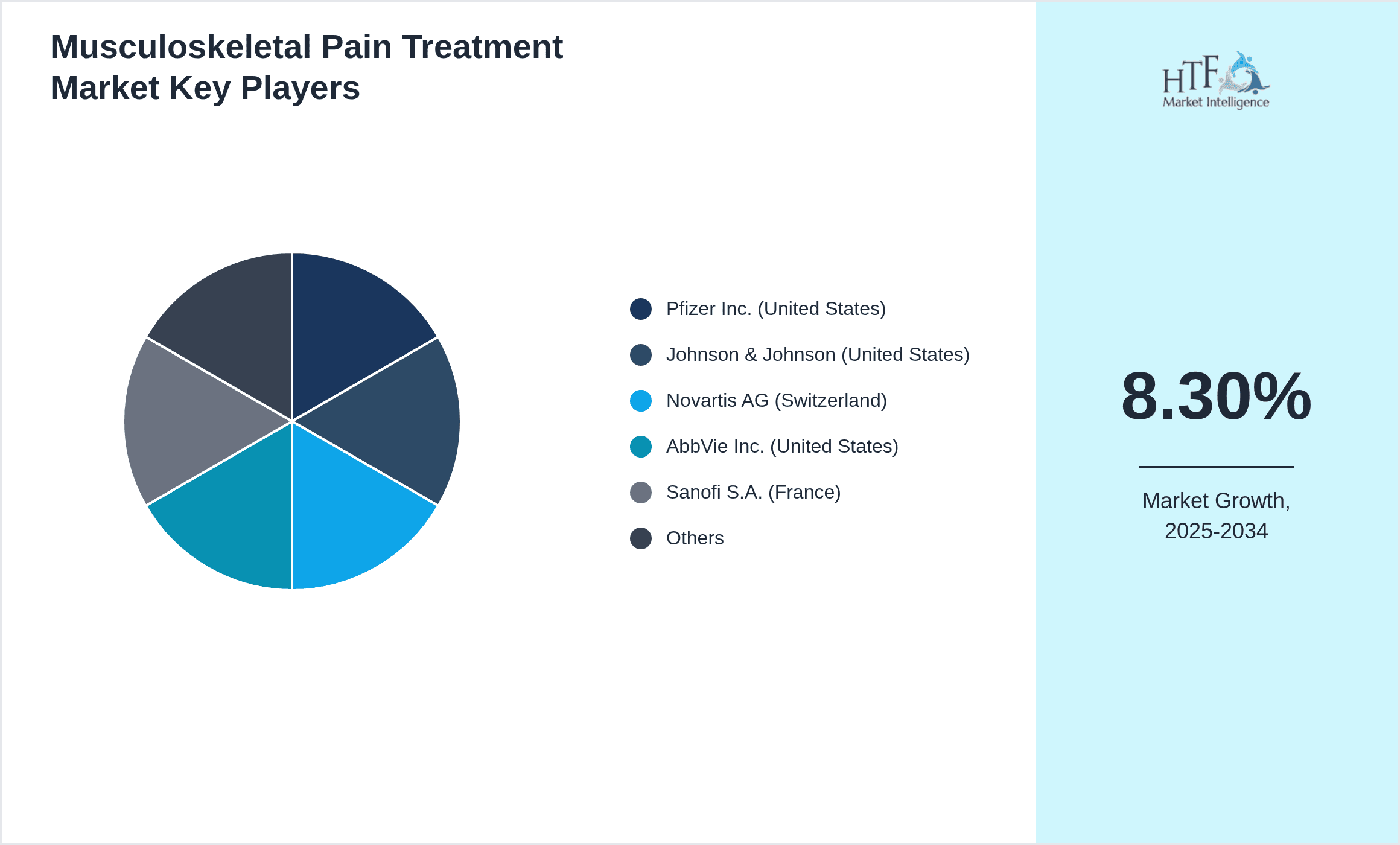

Leading Companies in Musculoskeletal Pain Treatment Market

- •Pfizer Inc. (United States)

- •Johnson & Johnson (United States)

- •Novartis AG (Switzerland)

- •AbbVie Inc. (United States)

- •Sanofi S.A. (France)

- •Amgen Inc. (United States)

- •Medtronic plc (Ireland)

- •Bristol-Myers Squibb Company (United States)

- •Eli Lilly and Company (United States)

- •Stryker Corporation (United States)

- •Roche Holding AG (Switzerland)

- •Hoffmann-La Roche Ltd. (Switzerland)

- •Zimmer Biomet Holdings, Inc. (United States)

- •Takeda Pharmaceutical Company Limited (Japan)

- •Mitsubishi Tanabe Pharma Corporation (Japan)

- •Bayer AG (Germany)

- •Smith & Nephew plc (United Kingdom)

- •Ipsen S.A. (France)

- •Regeneron Pharmaceuticals, Inc. (United States)

- •Biogen Inc. (United States)

- •MediWound Ltd. (Israel)

- •Horizon Therapeutics plc (Ireland)

- •United Therapeutics Corporation (United States)

- •Fresenius SE & Co. KGaA (Germany)

- •CONMED Corporation (United States)

Market Breakdown

- •By Treatment Type

- ◦Pharmacological Treatments (NSAIDs, Opioids, Analgesics)

- ◦Non-Pharmacological Therapies (Physical Therapy, Acupuncture, Chiropractic Care)

- ◦Surgical Interventions (Joint Replacement, Arthroscopy, Minimally Invasive Surgery)

- ◦Biologics (Monoclonal Antibodies, Regenerative Medicine)

- ◦Others (Complementary and Alternative Medicine)

- •By Application Area

- ◦Orthopedic Pain

- ◦Rheumatoid Arthritis

- ◦Osteoarthritis

- ◦Lower Back Pain

- ◦Fibromyalgia

- •By End User

- ◦Hospitals

- ◦Clinics

- ◦Outpatient Care Centers

- ◦Home Healthcare

- •By Distribution Channel

- ◦Hospital Pharmacies

- ◦Retail Pharmacies

- ◦Online Pharmacy

- ◦Direct Sales

Growth Dynamics

- •Rising prevalence of musculoskeletal disorders globally, particularly among aging populations, is a primary growth driver. Chronic conditions such as osteoarthritis and rheumatoid arthritis require long-term management, increasing demand for diverse treatment options. Advances in biologics and regenerative medicine offer disease-modifying potentials, attracting significant investments. Additionally, increasing healthcare expenditure and improved access in emerging markets further propel growth. Patient awareness and preference for minimally invasive procedures contribute to expansion of non-pharmacological and surgical treatment segments. Technological innovations, including digital therapeutics and tele-rehabilitation, enhance treatment efficacy and patient compliance, reinforcing market momentum.

- •The market is shaped by evolving trends such as integration of personalized medicine leveraging genomic insights to tailor therapies, and the growing adoption of biologics for targeted immune modulation. Digital health technologies, including wearable devices and remote monitoring platforms, are increasingly incorporated into treatment regimens to optimize outcomes. There is also a rising emphasis on multimodal pain management combining pharmacological and non-pharmacological interventions. Sustainability and patient-centric care models are influencing product development strategies. Additionally, partnerships between biotech firms and traditional pharmaceutical companies facilitate accelerated innovation and market penetration.

- •Market growth faces restraints from stringent regulatory pathways, high costs associated with biologics and advanced surgical procedures, and concerns about opioid dependency and side effects limiting pharmacological use. Reimbursement challenges, particularly in developing regions, restrict access to innovative therapies. Variability in healthcare infrastructure and provider expertise across geographies impacts adoption rates. Moreover, the complexity of musculoskeletal disorders and heterogeneous patient responses pose challenges for standardized treatment protocols. These factors collectively constrain market expansion despite rising demand.

- •There are significant opportunities to expand in emerging economies due to increasing healthcare investments and growing awareness of musculoskeletal health. Development of novel biologics and regenerative therapies that provide long-term disease modification can capture unmet clinical needs. Digital therapeutics and telemedicine offer scalable solutions to improve patient monitoring and adherence, particularly in remote areas. Furthermore, partnerships and licensing agreements can facilitate rapid market entry and broaden treatment offerings. Innovations in minimally invasive surgical techniques also present growth avenues by reducing recovery times and improving patient satisfaction.

- •Challenges include navigating complex regulatory environments that vary by region, which can delay product approvals and market entry. High research and development costs, coupled with competitive pricing pressures, impact profitability. Supply chain disruptions, especially for biologics requiring cold chain logistics, affect availability. Addressing opioid crisis concerns necessitates cautious pharmacological prescribing and development of safer alternatives. Additionally, educating healthcare providers and patients about novel therapies requires sustained efforts to overcome skepticism and ensure widespread adoption.

Market Trends

- •The increasing adoption of biologics such as monoclonal antibodies and regenerative therapies is revolutionizing musculoskeletal pain treatment by targeting underlying inflammatory processes rather than solely managing symptoms. This trend is supported by advances in biotechnology and personalized medicine approaches.

- •Digital health integration, including wearable sensors and tele-rehabilitation platforms, is becoming prevalent to enhance patient engagement and real-time monitoring of treatment efficacy, enabling tailored interventions and improved compliance.

- •There is a growing preference for minimally invasive surgical procedures, such as arthroscopy and robot-assisted surgeries, which reduce recovery times and complications, leading to better patient outcomes and lower healthcare costs.

- •Multimodal treatment approaches combining pharmacological, non-pharmacological, and surgical therapies are gaining traction to address complex musculoskeletal pain through holistic and patient-centric care models.

- •Collaborations between pharmaceutical companies and technology firms are fostering innovation in drug delivery systems and digital therapeutics, expanding the scope of effective musculoskeletal pain management solutions.

- •Sustainability initiatives focusing on reducing environmental impact of manufacturing and packaging processes are influencing product development strategies within the market.

- •Emerging markets are witnessing accelerated adoption of advanced therapies due to rising healthcare infrastructure investments and increasing prevalence of musculoskeletal disorders associated with lifestyle changes.

Market Opportunities

- •Emerging economies offer vast growth potential due to increasing incidence of musculoskeletal conditions and expanding healthcare access. Targeting these regions with cost-effective and localized solutions can drive market expansion.

- •Development and commercialization of novel biologics and regenerative medicines that modify disease progression represent promising opportunities to address unmet clinical needs and command premium pricing.

- •Integration of digital health tools such as telemedicine and wearable monitoring devices allows for improved patient management and treatment adherence, opening new revenue streams and enhancing care delivery.

- •Strategic partnerships and licensing agreements between biotechnology startups and established pharmaceutical companies can accelerate innovation cycles and broaden therapeutic portfolios.

- •Advancements in minimally invasive surgical technologies enable providers to offer safer and more efficient procedures, attracting patient preference and reducing hospital stays.

- •Personalized medicine approaches leveraging genomic and biomarker data provide opportunities for targeted therapies with improved efficacy and reduced side effects.

- •Expansion into home healthcare and outpatient settings for musculoskeletal pain management services can capitalize on shifting patient preferences and cost containment efforts.

Market Challenges

- •Stringent regulatory requirements across different regions impose significant compliance costs and lengthy approval timelines, delaying product launches and limiting market access.

- •High costs associated with advanced biologics and surgical interventions restrict affordability and reimbursement, particularly in low- and middle-income countries.

- •Concerns over opioid misuse and dependency have led to tighter regulations and reduced prescriptions, challenging pharmacological pain management strategies.

- •Fragmented healthcare infrastructure and variability in provider expertise across geographies hinder uniform adoption of innovative treatments and best practices.

- •Supply chain complexities, especially for temperature-sensitive biologic products, increase risks of disruptions and impact treatment continuity.

- •Educating healthcare professionals and patients about new treatment modalities requires sustained efforts to overcome skepticism and ensure informed decision-making.

- •Market saturation in developed regions intensifies competition, pressuring pricing and necessitating continuous innovation to maintain differentiation.

Regulatory Framework

- •Between 2020 and 2024, regulatory agencies worldwide have increasingly emphasized stringent clinical trial requirements and post-market surveillance for musculoskeletal pain treatments to ensure safety and efficacy, impacting approval timelines and market entry strategies.

- •New guidelines introduced for biologics, including biosimilars, mandate comprehensive comparability studies and risk management plans, influencing product development and commercialization approaches.

- •Several regions have implemented opioid stewardship programs and prescription monitoring policies to mitigate abuse risks, affecting pharmacological treatment protocols and prescribing behaviors.

- •Regulatory frameworks for digital health solutions, such as telemedicine platforms and wearable devices, have evolved to incorporate data privacy, cybersecurity, and interoperability standards, facilitating safer market adoption.

- •Government initiatives promoting access to affordable musculoskeletal care, including reimbursement reforms and public health campaigns, have shaped market dynamics by enhancing treatment accessibility and encouraging innovation.

Market Intelligence

- •12th January 2024, Pfizer Inc. launched a novel biologic therapy targeting inflammatory pathways for osteoarthritis pain management, featuring enhanced specificity and reduced side effects. The product aims to offer an alternative to traditional NSAIDs and opioids, with clinical trials demonstrating significant pain relief and improved joint function. Pfizer’s strategic focus on personalized medicine and regenerative therapies underpins this launch, targeting a large patient population with unmet needs globally. The introduction is expected to strengthen Pfizer’s portfolio in musculoskeletal care and drive market growth in biologics. Source: Pfizer Official Press Release

- •23rd August 2023, Johnson & Johnson announced a strategic partnership with a leading digital health firm to develop integrated tele-rehabilitation solutions for musculoskeletal pain patients. The collaboration focuses on combining therapeutic exercise protocols with remote monitoring technologies to enhance patient adherence and outcomes. This initiative aligns with global trends toward digital healthcare adoption and personalized treatment plans, aiming to expand access in both developed and emerging markets. Johnson & Johnson plans to leverage its extensive healthcare network to commercialize these solutions effectively. Source: Johnson & Johnson Corporate News

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 28.5 Billion |

| Forecast Year Market Size | USD 65.7 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.8% |

| Scope of Report | Market is segmented by Treatment Type (Pharmacological Treatments (NSAIDs, Opioids, Analgesics), Non-Pharmacological Therapies (Physical Therapy, Acupuncture, Chiropractic Care), Surgical Interventions (Joint Replacement, Arthroscopy, Minimally Invasive Surgery), Biologics (Monoclonal Antibodies, Regenerative Medicine), Others (Complementary and Alternative Medicine)), Application Area (Orthopedic Pain, Rheumatoid Arthritis, Osteoarthritis, Lower Back Pain, Fibromyalgia), End User (Hospitals, Clinics, Outpatient Care Centers, Home Healthcare), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacy, Direct Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Pfizer Inc. (United States), Johnson & Johnson (United States), Novartis AG (Switzerland), AbbVie Inc. (United States), Sanofi S.A. (France), Amgen Inc. (United States), Medtronic plc (Ireland), Bristol-Myers Squibb Company (United States), Eli Lilly and Company (United States), Stryker Corporation (United States), Roche Holding AG (Switzerland), Hoffmann-La Roche Ltd. (Switzerland), Zimmer Biomet Holdings, Inc. (United States), Takeda Pharmaceutical Company Limited (Japan), Mitsubishi Tanabe Pharma Corporation (Japan), Bayer AG (Germany), Smith & Nephew plc (United Kingdom), Ipsen S.A. (France), Regeneron Pharmaceuticals, Inc. (United States), Biogen Inc. (United States), MediWound Ltd. (Israel), Horizon Therapeutics plc (Ireland), United Therapeutics Corporation (United States), Fresenius SE & Co. KGaA (Germany), CONMED Corporation (United States) |

Global Musculoskeletal Pain Treatment Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.