North America Dental Lab Market Size, Growth & Revenue 2024-2034

North America Dental Lab Market is segmented by Type (Ceramic Dental Materials, Metal Dental Materials, Resin-Based Dental Materials, Composite Dental Materials, Zirconia Dental Materials), Application (Orthodontics, Prosthodontics, Implantology, Preventive Dentistry, Cosmetic Dentistry), End-User Facility (Dental Laboratories, Dental Clinics, Hospitals, Academic & Research Institutes), Technology (Conventional Manual Fabrication, CAD/CAM Systems, 3D Printing, Digital Impressions), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

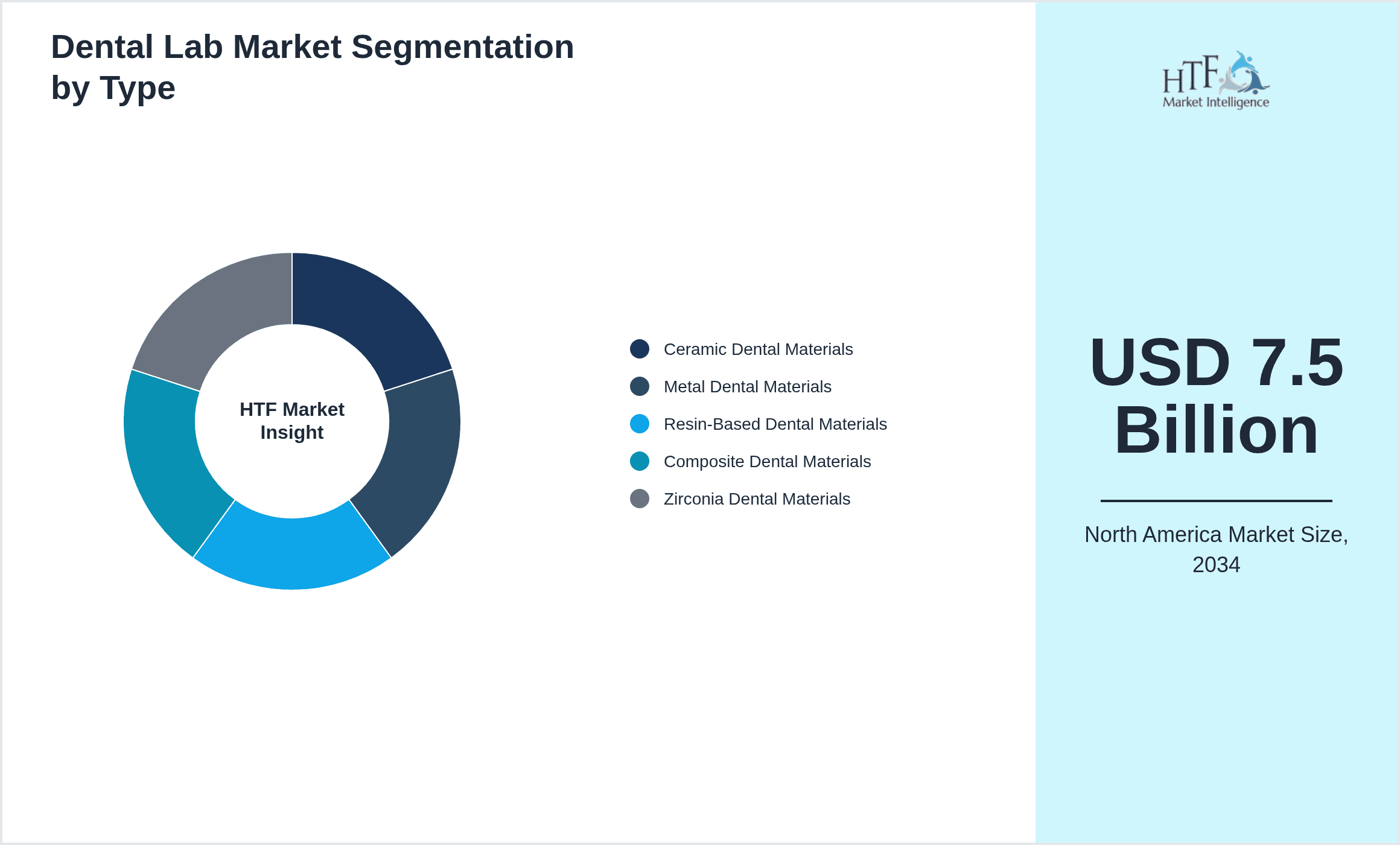

- •The North America Dental Lab market is a dynamic sector focused on the design, fabrication, and distribution of dental prosthetics and appliances essential for restorative and cosmetic dentistry. The market operates across a broad spectrum of product types including ceramic, metal, resin, composite, and zirconia materials, serving diverse applications such as orthodontics, prosthodontics, implantology, preventive dentistry, and cosmetic dentistry. The industry has evolved significantly with the integration of digital technologies like CAD/CAM systems and 3D printing, which have enhanced precision, turnaround time, and customization capabilities. This has facilitated the growth of dental labs that are increasingly adopting advanced manufacturing processes to meet rising patient expectations for aesthetic and durable dental solutions. The market is geographically concentrated in the United States, Canada, and Mexico, with the U.S. dominating in terms of market size and innovation, while Canada is experiencing rapid growth due to increased dental insurance coverage and technological adoption. Regulatory frameworks, technological innovation, and consumer preferences are shaping the evolving landscape of this market.

- •Key highlights of the North America Dental Lab market include a robust CAGR of 5.7% forecasted between 2024 and 2034, with the market size expected to reach USD 7.5 billion by 2034 from USD 4.2 billion in 2024. Ceramic dental products currently dominate the product segment, attributable to their biocompatibility and aesthetic appeal. Zirconia is emerging as the fastest growing type, driven by its superior strength and versatility in dental restorations. Orthodontics leads application segments, reflecting increased demand for corrective treatments and aesthetic dentistry. The United States holds a commanding 65% market share, supported by advanced dental infrastructure and high healthcare expenditure, while Canada’s market share is growing steadily at a 7.1% CAGR. Technological advancements such as digital impressions and 3D printing are accelerating market expansion and improving patient outcomes across the region.

- •The North America Dental Lab market presents significant value to dental professionals, manufacturers, and healthcare providers by enabling customized, high-quality dental restorations and appliances that improve patient satisfaction and oral health outcomes. Strategic importance lies in the adoption of innovative materials and digital workflows that reduce treatment time and costs while enhancing precision and aesthetics. The market’s growth is supported by increasing geriatric populations, rising prevalence of dental diseases, and growing awareness of cosmetic dentistry. Investments in research and development, along with favorable reimbursement policies in key countries, provide lucrative opportunities for stakeholders. Overall, the market’s evolution is closely linked to technological innovation, regulatory compliance, and consumer demand for advanced dental care solutions, positioning it as a critical segment within North America’s healthcare and dental services ecosystem.

Competitive Landscape

The North America Dental Lab market is characterized by intense competition among established players and emerging companies focusing on innovation, quality, and technological integration. Market leaders leverage advanced digital dentistry technologies, including CAD/CAM and 3D printing, to differentiate their offerings and improve operational efficiencies. Competition is driven by product innovation, strategic partnerships, and expansion of service portfolios to cater to evolving customer needs. Companies emphasize customization, turnaround time reduction, and cost-effectiveness to gain competitive advantage. The market also witnesses consolidation through mergers and acquisitions, enabling firms to expand geographic reach and enhance technological capabilities. Pricing strategies vary, with premium offerings targeting high-end dental practices, while value-based products cater to broader market segments. Distribution channels, including direct sales and third-party collaborations, play a crucial role in market penetration. Regional competition is marked by the dominance of U.S.-based firms, while Canadian and Mexican players focus on niche segments and local market adaptation. Future trends indicate heightened innovation and strategic collaborations to sustain growth in this competitive landscape.

Leading Companies in North America Dental Lab Market

- •Dentsply Sirona Inc. (United States)

- •Patterson Companies, Inc. (United States)

- •Henry Schein, Inc. (United States)

- •3M Company (United States)

- •Straumann Group (United States)

- •Align Technology, Inc. (United States)

- •Ivoclar Vivadent AG (United States)

- •Kulzer GmbH (United States)

- •Carestream Health, Inc. (United States)

- •Planmeca Oy (United States)

- •Zimmer Biomet Holdings, Inc. (United States)

- •Benco Dental (United States)

- •Nobel Biocare Services AG (United States)

- •Sirona Dental Systems, Inc. (United States)

- •Dental Wings, Inc. (United States)

- •American Dental Association (United States)

- •CAD-Ray Inc. (Canada)

- •Dentalcorp Holdings Ltd. (Canada)

- •Straumann Canada Ltd. (Canada)

- •Nobel Biocare Canada (Canada)

- •SmileDirectClub, Inc. (United States)

- •ClearCorrect (United States)

- •Vita North America (United States)

- •Whip Mix Corporation (United States)

- •Argen Corporation (United States)

Market Breakdown

- •By Type

- ◦Ceramic Dental Materials

- ◦Metal Dental Materials

- ◦Resin-Based Dental Materials

- ◦Composite Dental Materials

- ◦Zirconia Dental Materials

- •By Application

- ◦Orthodontics

- ◦Prosthodontics

- ◦Implantology

- ◦Preventive Dentistry

- ◦Cosmetic Dentistry

- •By End-User Facility

- ◦Dental Laboratories

- ◦Dental Clinics

- ◦Hospitals

- ◦Academic & Research Institutes

- •By Technology

- ◦Conventional Manual Fabrication

- ◦CAD/CAM Systems

- ◦3D Printing

- ◦Digital Impressions

Growth Dynamics

The North America Dental Lab market is propelled by several growth drivers, foremost among them being the rising prevalence of dental disorders and increasing dental care awareness. The growing geriatric population demands prosthodontic and implantology services, driving the need for advanced dental lab products. Additionally, technological advancements such as CAD/CAM and 3D printing enable faster, more precise production, reducing turnaround time and costs. Insurance coverage expansion in the U.S. and Canada has further increased patient access to dental services, fueling market growth. Consumer preference for aesthetic dental solutions and minimally invasive procedures enhances demand for ceramic and zirconia products. Furthermore, collaborations between dental labs and clinics foster integrated service delivery, enhancing market penetration. These factors collectively underpin sustained expansion in this specialized healthcare segment.

Market Trends

A prominent trend in the North America Dental Lab market is the integration of digital dentistry technologies, including 3D printing and CAD/CAM systems, revolutionizing dental prosthetic fabrication. This digitization enhances accuracy, customization, and efficiency, enabling labs to meet personalized patient demands. The shift toward zirconia-based restorations reflects preferences for materials combining aesthetics and durability. Additionally, sustainable and eco-friendly materials are gaining traction among labs aiming to reduce environmental impact. Tele-dentistry and remote collaboration between labs and dental practices are emerging, driven by advancements in communication technologies and demand for streamlined workflows. Furthermore, the rise of clear aligners and cosmetic dentistry is reshaping application segments, emphasizing esthetic outcomes. These trends point towards a technologically advanced, patient-centric dental lab industry focused on innovation and quality.

Market Opportunities

Opportunities in the North America Dental Lab market are abundant, primarily through adoption of emerging technologies such as AI-powered design software and enhanced 3D printing materials. Expanding dental insurance coverage in Canada and Mexico offers untapped patient segments, encouraging market entry and expansion. The growing demand for cosmetic dentistry and minimally invasive treatments provides avenues for product innovation and service differentiation. Strategic partnerships between dental labs and technology providers can accelerate digital transformation and improve market reach. Additionally, increasing dental tourism in North America opens new channels for lab services targeting international patients. Sustainability initiatives and development of biodegradable dental materials present environmental and regulatory advantages. Collectively, these opportunities enable stakeholders to capitalize on evolving market dynamics and consumer preferences.

Market Challenges

The North America Dental Lab market faces challenges including stringent regulatory requirements that increase compliance costs and delay product launches. High initial capital investment for digital equipment like CAD/CAM and 3D printers can be prohibitive for smaller labs. Fragmentation of the dental lab industry and intense competition exert pricing pressures, impacting profitability. Additionally, skilled labor shortages and the need for specialized training hinder operational efficiency. Supply chain disruptions, especially for raw materials such as zirconia and ceramics, pose risks to production continuity. Another challenge is the rising preference for in-house dental labs by large dental practices, reducing reliance on third-party labs. Addressing these challenges requires strategic investment, innovation, and collaboration to sustain market growth.

Regulatory Framework

Between 2020 and 2024, regulatory frameworks in North America have intensified, focusing on quality assurance and patient safety in dental lab products. The U.S. Food and Drug Administration (FDA) has updated guidelines for dental devices, including stricter controls on material biocompatibility and manufacturing processes. Canadian Health Authorities have implemented enhanced certification requirements for dental labs to ensure compliance with national standards. Data protection regulations related to digital dental workflows have also been strengthened, mandating secure handling of patient information. These regulations impact product development timelines and necessitate continuous monitoring to ensure market access. Compliance with evolving standards fosters trust and promotes high-quality dental lab outputs, but requires significant investment in quality management systems and staff training.

Market Intelligence

- •15th March 2024, Dentsply Sirona Inc. launched an advanced zirconia-based dental restoration material integrating AI-driven design features to improve fit and durability for prosthodontic applications. This innovation targets orthodontists and dental labs aiming for enhanced patient outcomes, reducing remakes and chair time. The product leverages digital workflows compatible with existing CAD/CAM systems, accelerating adoption across North America. Strategic objectives include expanding market share in the ceramic segment and reinforcing technological leadership in dental materials. Source: Official press release.

- •30th November 2023, Straumann Group announced a strategic partnership with a leading 3D printing company to co-develop customized implant abutments utilizing biocompatible resins. This collaboration aims to enhance implantology services by integrating additive manufacturing with digital dental workflows, reducing production time and cost. The initiative targets dental labs and clinics across the U.S. and Canada, driving growth in the implantology application segment. Source: Industry publication.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.2 Billion |

| Forecast Year Market Size | USD 7.5 Billion |

| CAGR | 5.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 5.5% |

| Scope of Report | Market is segmented by Type (Ceramic Dental Materials, Metal Dental Materials, Resin-Based Dental Materials, Composite Dental Materials, Zirconia Dental Materials), Application (Orthodontics, Prosthodontics, Implantology, Preventive Dentistry, Cosmetic Dentistry), End-User Facility (Dental Laboratories, Dental Clinics, Hospitals, Academic & Research Institutes), Technology (Conventional Manual Fabrication, CAD/CAM Systems, 3D Printing, Digital Impressions) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Dentsply Sirona Inc. (United States), Patterson Companies, Inc. (United States), Henry Schein, Inc. (United States), 3M Company (United States), Straumann Group (United States), Align Technology, Inc. (United States), Ivoclar Vivadent AG (United States), Kulzer GmbH (United States), Carestream Health, Inc. (United States), Planmeca Oy (United States), Zimmer Biomet Holdings, Inc. (United States), Benco Dental (United States), Nobel Biocare Services AG (United States), Sirona Dental Systems, Inc. (United States), Dental Wings, Inc. (United States), American Dental Association (United States), CAD-Ray Inc. (Canada), Dentalcorp Holdings Ltd. (Canada), Straumann Canada Ltd. (Canada), Nobel Biocare Canada (Canada), SmileDirectClub, Inc. (United States), ClearCorrect (United States), Vita North America (United States), Whip Mix Corporation (United States), Argen Corporation (United States) |

North America Dental Lab Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.