Global Fully Automated Blood Grouping System Market Size, Growth & Revenue 2025-2034

Global Fully Automated Blood Grouping System Market is segmented by Type (Semi-Automated Systems, Fully Automated Systems, Integrated Systems, Others), Application (Hospital Laboratories, Blood Banks, Diagnostic Centers, Research Institutes, Others), Technology (Gel Card Technology, Microplate Technology, Solid Phase Technology, Column Agglutination Technology), End-User (Public Hospitals, Private Hospitals, Diagnostic Laboratories, Blood Transfusion Centers), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Fully Automated Blood Grouping System market represents a critical segment of healthcare technology focused on automating blood typing and compatibility testing processes. These systems employ advanced technologies such as gel card, microplate, and solid-phase to deliver rapid, accurate, and reliable blood group identification and antibody screening. The market's scope includes semi-automated, fully automated, and integrated systems tailored for hospital laboratories, blood banks, diagnostic centers, and research institutions. Automation minimizes manual errors, expedites blood processing, and enhances transfusion safety, which is paramount given the increasing demand for blood transfusions and rising awareness about patient safety worldwide. The market's relevance extends to improving operational efficiency and supporting complex clinical workflows, making it essential for modern healthcare infrastructure and diagnostic advancements.

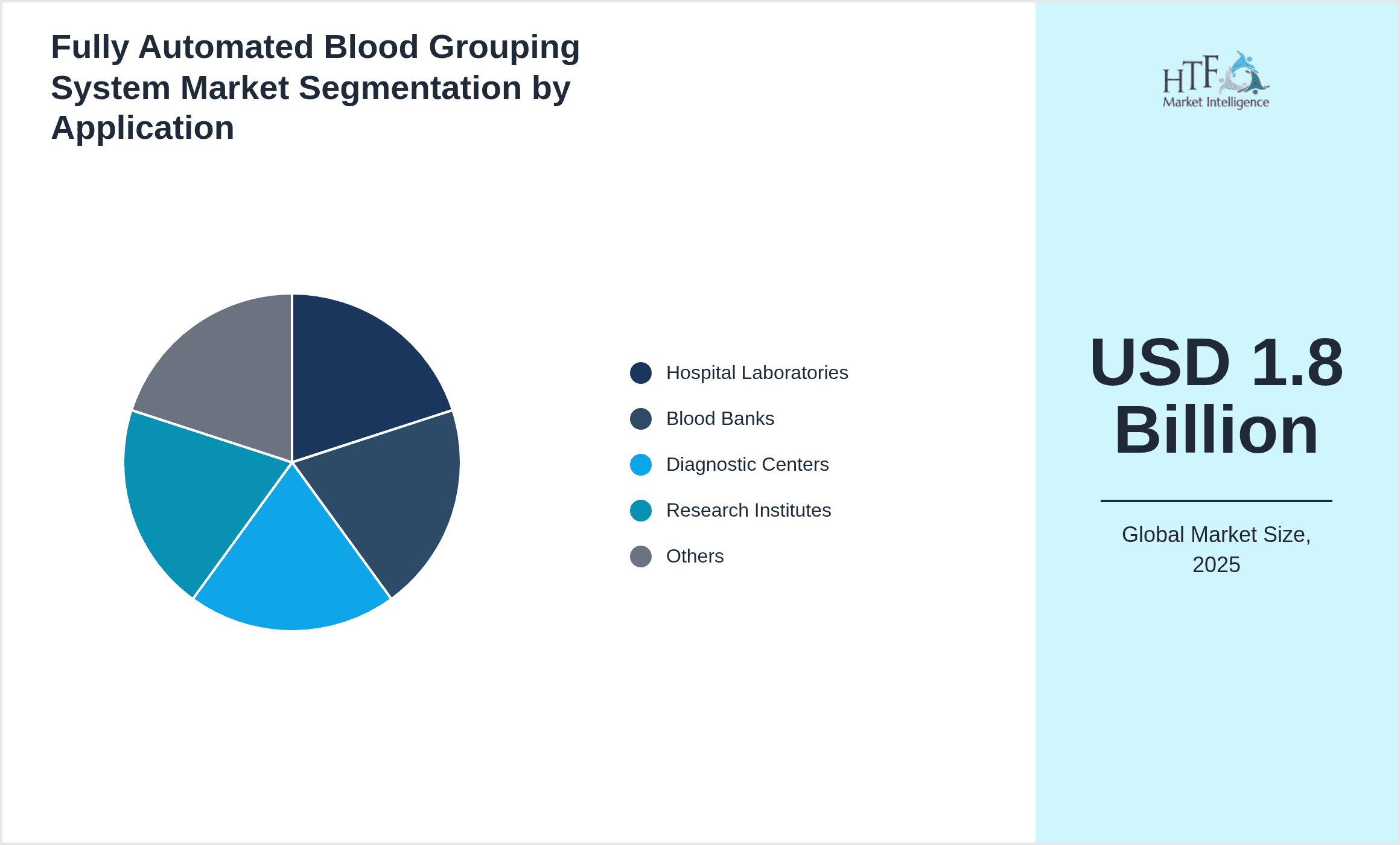

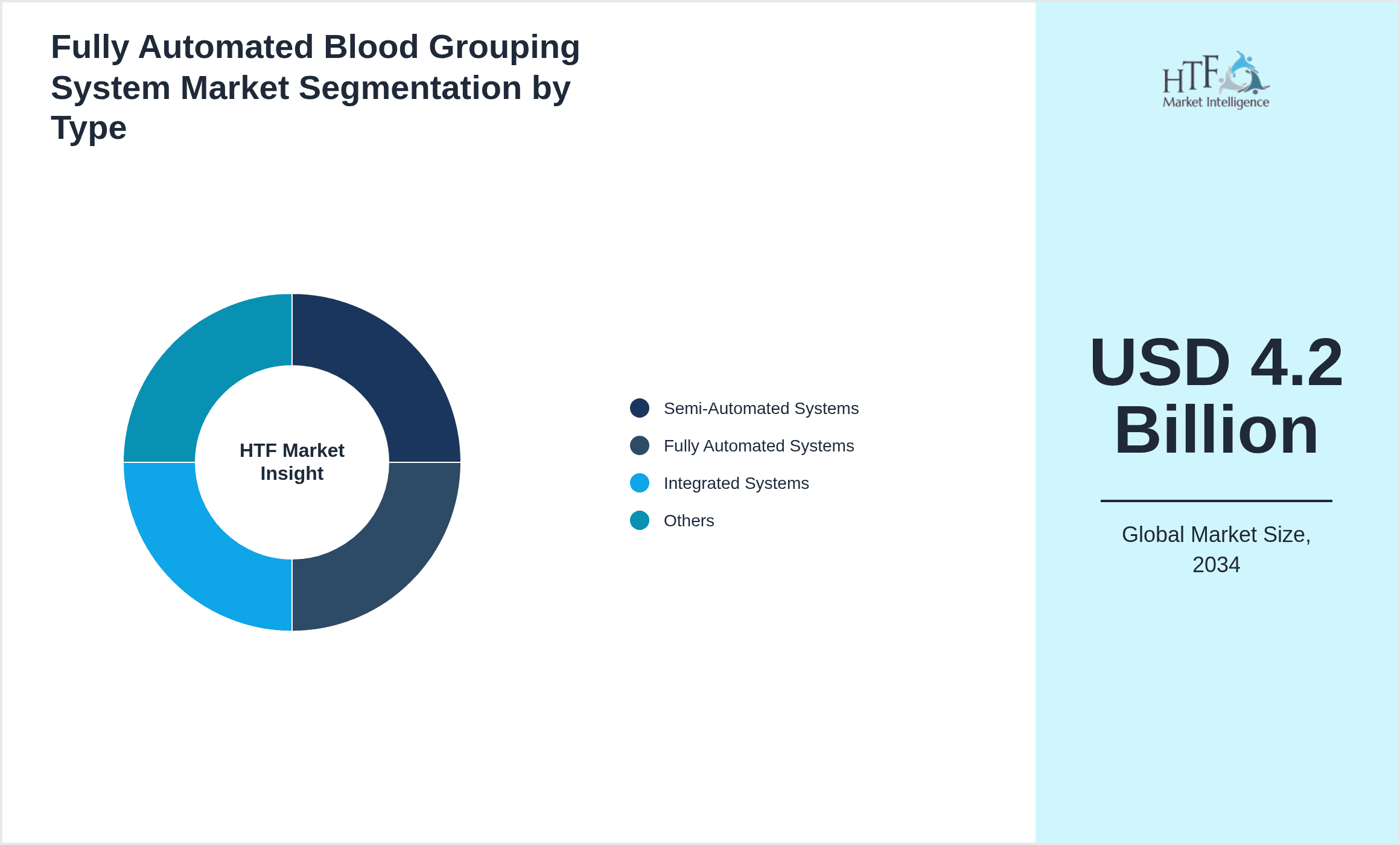

- •The market is projected to grow from a base size of USD 1.8 billion in 2025 to USD 4.2 billion by 2034 at a CAGR of 9.4%. North America currently dominates the market with a 35% share, driven by advanced healthcare infrastructure and adoption of cutting-edge technologies. Asia-Pacific is the fastest-growing region, exhibiting a CAGR of 12.6% fueled by rising healthcare investments and expanding blood transfusion services. Fully Automated Systems lead product types in market share and revenue, while Integrated Systems demonstrate the highest growth potential. Key applications include hospital laboratories and blood banks, which collectively command significant revenue streams. Increasing demand for safe blood transfusion and technological innovations are primary growth catalysts.

- •This market offers substantial value propositions across healthcare providers, blood banks, and diagnostic centers by enhancing accuracy, reducing turnaround times, and improving workflow efficiencies. Strategic importance lies in its potential to reduce transfusion-related complications and support large-scale blood management programs globally. Stakeholders benefit from innovations that integrate automation with data management, enabling streamlined blood typing and compatibility testing. The evolving regulatory landscape and growing investments in healthcare infrastructure further amplify market opportunities, positioning the Global Fully Automated Blood Grouping System market as a vital contributor to improved patient outcomes and healthcare delivery.

Competitive Landscape

Companies in the Global Fully Automated Blood Grouping System market adopt diverse strategies to maintain and enhance their market positions. These include forming strategic partnerships with healthcare providers and distributors to expand global reach and improve service networks. Product innovation remains a central focus, with firms investing in R&D to develop integrated and high-throughput systems that meet evolving clinical demands. Adoption of cutting-edge technologies such as AI-driven analytics and IoT connectivity enhances system capabilities and user experience. Market players pursue mergers and acquisitions to consolidate capabilities and expand product portfolios. Geographic expansion into emerging markets is prioritized to capitalize on rising healthcare investments and unmet clinical needs. Competitive pricing strategies and comprehensive customer support further differentiate offerings. Companies also emphasize compliance with stringent regulatory standards and certification to build trust and facilitate market access. These approaches collectively drive sustained growth and competitive resilience in a dynamic market environment.

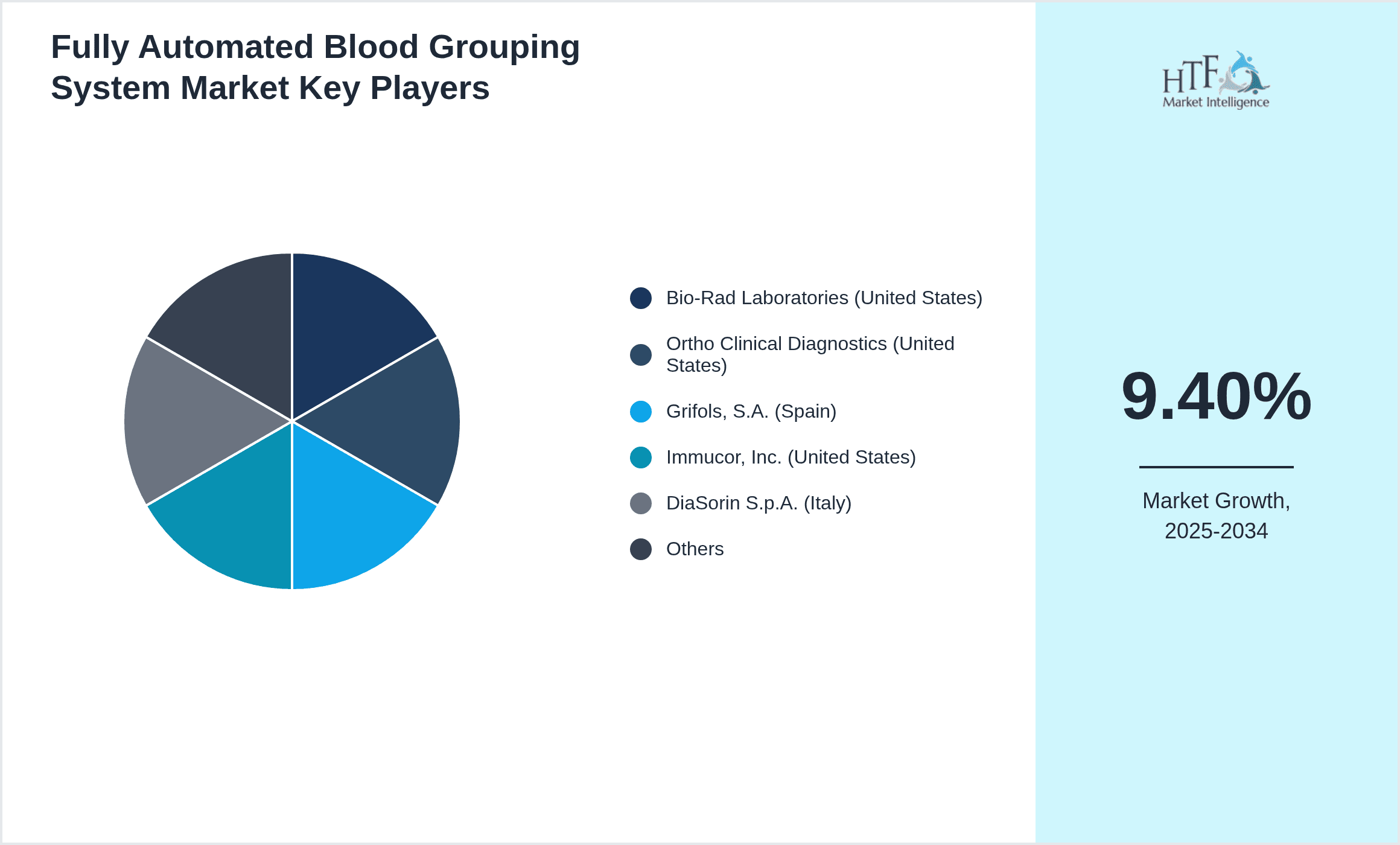

Leading Companies in Fully Automated Blood Grouping System Market

- •Bio-Rad Laboratories (United States)

- •Ortho Clinical Diagnostics (United States)

- •Grifols, S.A. (Spain)

- •Immucor, Inc. (United States)

- •DiaSorin S.p.A. (Italy)

- •Sartorius AG (Germany)

- •Siemens Healthineers (Germany)

- •Haemonetics Corporation (United States)

- •Thermo Fisher Scientific (United States)

- •Abbott Laboratories (United States)

- •Becton Dickinson and Company (United States)

- •Tecan Group Ltd. (Switzerland)

- •Helena Laboratories (United States)

- •BioMérieux SA (France)

- •Fresenius SE & Co. KGaA (Germany)

- •Sysmex Corporation (Japan)

- •PerkinElmer, Inc. (United States)

- •Luminex Corporation (United States)

- •Orgentec Diagnostika GmbH (Germany)

- •Agilent Technologies, Inc. (United States)

Market Breakdown

- •By Type

- ◦Semi-Automated Systems

- ◦Fully Automated Systems

- ◦Integrated Systems

- ◦Others

- •By Application

- ◦Hospital Laboratories

- ◦Blood Banks

- ◦Diagnostic Centers

- ◦Research Institutes

- ◦Others

- •By Technology

- ◦Gel Card Technology

- ◦Microplate Technology

- ◦Solid Phase Technology

- ◦Column Agglutination Technology

- •By End-User

- ◦Public Hospitals

- ◦Private Hospitals

- ◦Diagnostic Laboratories

- ◦Blood Transfusion Centers

Growth Dynamics

The Global Fully Automated Blood Grouping System market experiences robust growth propelled by increasing demand for rapid and accurate blood typing solutions in healthcare settings. Rising prevalence of chronic diseases and surgical procedures amplifies the need for safe transfusion services, stimulating market expansion. Technological advancements introducing integrated platforms with enhanced throughput and connectivity foster adoption among clinical laboratories. Government initiatives promoting blood safety and modernization of healthcare infrastructure in emerging economies support market growth. The surge in blood donation drives and awareness campaigns further increases demand. Prominent companies actively introduce innovative systems with artificial intelligence and data analytics capabilities to optimize workflow and reduce errors. Strategic collaborations between manufacturers and healthcare providers improve accessibility and service delivery. The cumulative effect of these factors consolidates market growth globally, with Asia-Pacific emerging as a key growth region due to expanding healthcare expenditure and infrastructure development.

Market Trends

Future trends in the Global Fully Automated Blood Grouping System market center on the integration of digital technologies and artificial intelligence to enhance diagnostic accuracy and operational efficiency. Adoption of cloud-based data management and real-time reporting is increasing, enabling seamless interoperability within healthcare networks. Miniaturization and portability of blood grouping systems offer point-of-care testing opportunities, expanding usage beyond traditional laboratories. Emphasis on personalized medicine and precision transfusion aligns with innovations in antibody detection and rare blood group identification. Market players are investing in developing multifunctional platforms capable of performing multiple immunohematology tests, streamlining laboratory workflows. Increasing collaborations between technology firms and healthcare institutions accelerate innovation cycles. Continuous improvements in reagent quality and automation software further support trend momentum. These developments collectively position the market for sustained expansion and improved patient safety outcomes worldwide.

Market Opportunities

Expansion into emerging markets presents significant growth opportunities for the Fully Automated Blood Grouping System sector, driven by increasing healthcare spending and modernization of diagnostic facilities. Rising demand for rapid, high-throughput blood typing in populous regions creates avenues for market penetration. Integration of AI-powered analytics and machine learning algorithms into blood grouping platforms offers prospects for enhanced diagnostic precision and predictive capabilities. Development of portable and user-friendly systems tailored for remote or resource-limited settings unlocks new application segments. Strategic partnerships with regional distributors and blood banks facilitate market access and customer engagement. Regulatory approvals and reimbursement policies improving in developing countries also catalyze growth potential. Furthermore, increasing focus on research and development to accommodate rare blood group detection and multiplex testing expands product portfolios and application scope. These factors collectively create a conducive environment for sustained innovation and market expansion.

Market Challenges

Key challenges faced by the Global Fully Automated Blood Grouping System market include high initial capital investment and maintenance costs, which limit adoption, especially among smaller healthcare facilities and in emerging economies. Variability in regulatory frameworks across regions complicates market entry and prolongs product launch timelines. Technical complexity and need for skilled personnel to operate sophisticated automated systems pose operational barriers. Compatibility issues between different automated platforms and laboratory information systems sometimes hinder seamless integration. Supply chain disruptions and delays in reagent availability impact consistent system performance. Recent incidents involving system malfunctions have heightened concerns about reliability and data accuracy, emphasizing the need for stringent quality control. Competition from manual and semi-automated methods in cost-sensitive markets also restrains growth. These challenges necessitate continued innovation in cost-effective, user-friendly solutions and harmonization of regulatory standards to facilitate wider adoption.

Regulatory Framework

In the last five years, key regulatory frameworks impacting the Fully Automated Blood Grouping System market include the U.S. Food and Drug Administration's updated guidance on in vitro diagnostic devices, emphasizing rigorous validation and post-market surveillance to ensure safety and efficacy. The European Union's In Vitro Diagnostic Regulation introduced stricter requirements for clinical evidence and quality management systems, affecting market access across member states. Additionally, initiatives such as the Medical Device Single Audit Program promote harmonization of audits to streamline compliance globally. Emerging markets have enhanced regulatory oversight by adopting standards aligned with international best practices to safeguard blood transfusion services. These regulations collectively drive manufacturers to maintain high product quality, implement robust clinical validation, and ensure traceability, thereby reinforcing patient safety and fostering market trust.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Official company websites, Industry reports, Regulatory agencies

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 4.2 Billion |

| CAGR | 9.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9% |

| Scope of Report | Market is segmented by Type (Semi-Automated Systems, Fully Automated Systems, Integrated Systems, Others), Application (Hospital Laboratories, Blood Banks, Diagnostic Centers, Research Institutes, Others), Technology (Gel Card Technology, Microplate Technology, Solid Phase Technology, Column Agglutination Technology), End-User (Public Hospitals, Private Hospitals, Diagnostic Laboratories, Blood Transfusion Centers) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Bio-Rad Laboratories (United States), Ortho Clinical Diagnostics (United States), Grifols, S.A. (Spain), Immucor, Inc. (United States), DiaSorin S.p.A. (Italy), Sartorius AG (Germany), Siemens Healthineers (Germany), Haemonetics Corporation (United States), Thermo Fisher Scientific (United States), Abbott Laboratories (United States), Becton Dickinson and Company (United States), Tecan Group Ltd. (Switzerland), Helena Laboratories (United States), BioMérieux SA (France), Fresenius SE & Co. KGaA (Germany), Sysmex Corporation (Japan), PerkinElmer, Inc. (United States), Luminex Corporation (United States), Orgentec Diagnostika GmbH (Germany), Agilent Technologies, Inc. (United States) |

Global Fully Automated Blood Grouping System Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.