North America Automotive Performance Part Market Size, Growth & Revenue 2024-2034

North America Automotive Performance Part Market is segmented by Application (Engine Enhancement, Suspension Systems, Exhaust Systems, Brake Systems, Transmission Components), Type (Mechanical Parts, Electronic Parts, Aerodynamic Components, Exhaust Components, Suspension Components), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Automotive Performance Part market is a dynamic segment within the automotive aftermarket and OEM sectors, focusing on components that enhance vehicle performance, safety, and aesthetics. Encompassing mechanical parts, electronic modules, aerodynamic components, exhaust systems, brake parts, and transmission upgrades, the market serves a wide range of vehicles including passenger cars, commercial vehicles, and specialty automobiles. The primary purpose of this market is to provide vehicle owners and automotive enthusiasts with parts that improve speed, handling, fuel efficiency, and durability. The market operates across the United States, Canada, and Mexico, reflecting regional demand influenced by motorsports culture, increased vehicle personalization, and technological advancements in automotive engineering. Key market drivers include rising disposable incomes, growing automotive aftermarket activities, and stringent emissions regulations promoting advanced performance parts. The scope also covers distribution channels such as specialty retailers, online platforms, and direct OEM sales, making the market a critical component of the automotive industry ecosystem in North America.

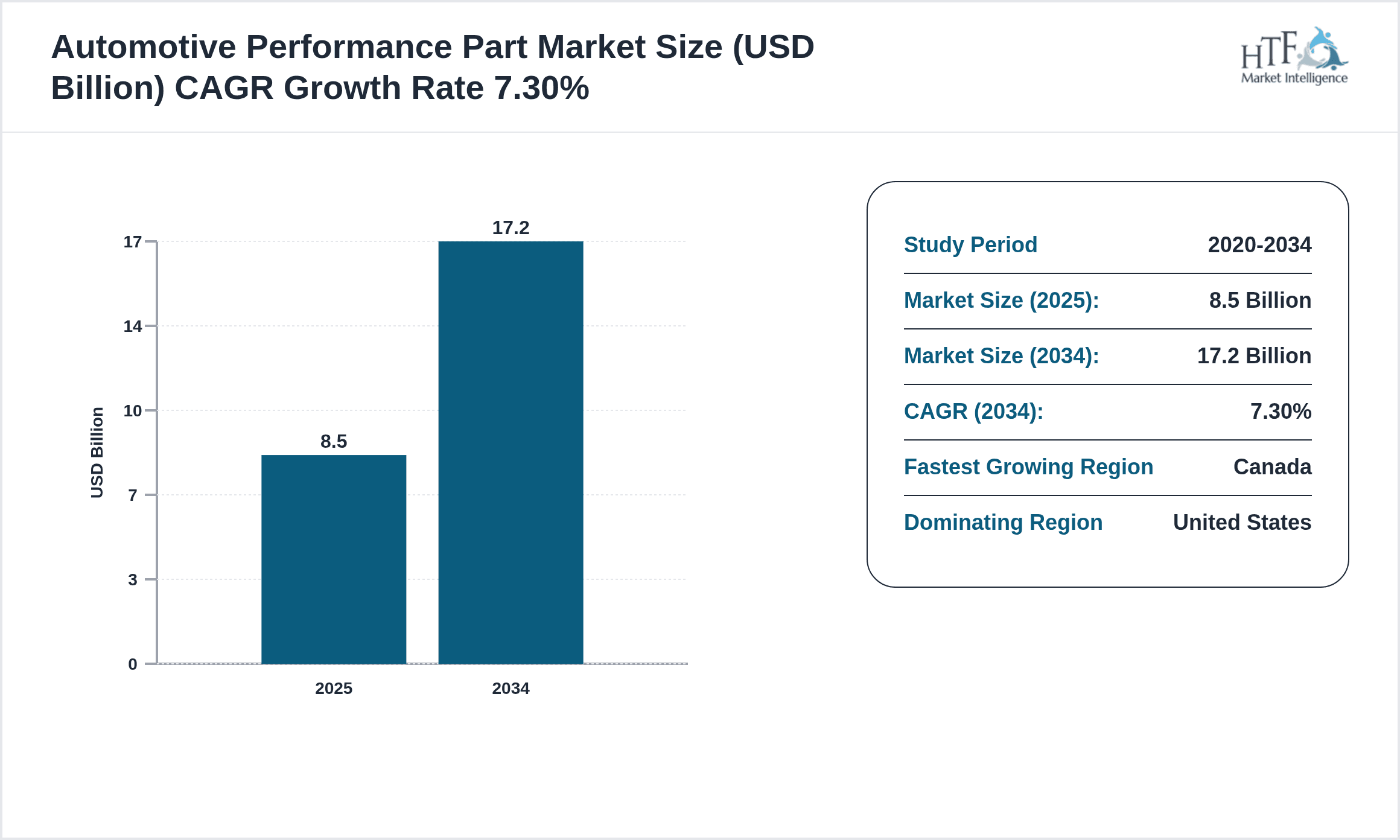

- •Key highlights of the North America Automotive Performance Part market include a base market size of USD 8.5 Billion in 2024, projected to reach USD 17.2 Billion by 2034, exhibiting a robust CAGR of 7.3%. The market growth is fueled by increasing vehicle customization trends and adoption of advanced electronic performance parts. The United States dominates the market with a 65% share, while Canada emerges as the fastest-growing country with a CAGR of 9.1%. Mechanical parts remain the leading product type, but electronic parts show the fastest growth, reflecting innovation in vehicle performance technology. Engine enhancement and suspension systems are the most significant application segments, capturing the majority of demand across North America. This growth is supported by a thriving motorsports culture, rising disposable income, and expanding aftermarket distribution networks.

- •The North America Automotive Performance Part market holds strategic importance for automotive manufacturers, aftermarket suppliers, and vehicle owners seeking enhanced driving experiences. It offers value through performance improvements, fuel efficiency gains, and compliance with environmental standards. Stakeholders benefit from emerging opportunities in electronic and aerodynamic parts driven by technological advancements. The market also supports automotive service industries and specialty retailers, fostering economic growth. As regulatory frameworks evolve, the market adapts with innovative, compliant products that meet consumer demands. This sector’s growth underscores its critical role in vehicle personalization, motorsports, and sustainability efforts within the North American automotive landscape.

Competitive Landscape

The North America Automotive Performance Part market exhibits intense competition driven by innovation, brand reputation, and distribution capabilities. Key players engage in continuous product development to offer advanced mechanical and electronic components that meet evolving vehicle performance demands and regulatory standards. Market rivalry is characterized by strategic partnerships, technology integrations, and frequent product launches to capture diverse customer segments, including motorsports enthusiasts and aftermarket consumers. Companies leverage proprietary technologies and extensive dealer networks to maintain market share and enhance customer loyalty. Pricing strategies vary to balance affordability with premium quality offerings, while geographic expansion within North America intensifies competition. Additionally, mergers and acquisitions serve as crucial growth tactics to consolidate market position and broaden product portfolios. Overall, the competitive environment fosters rapid innovation, efficient supply chain management, and customer-centric solutions, ensuring sustained market growth and dynamic industry evolution.

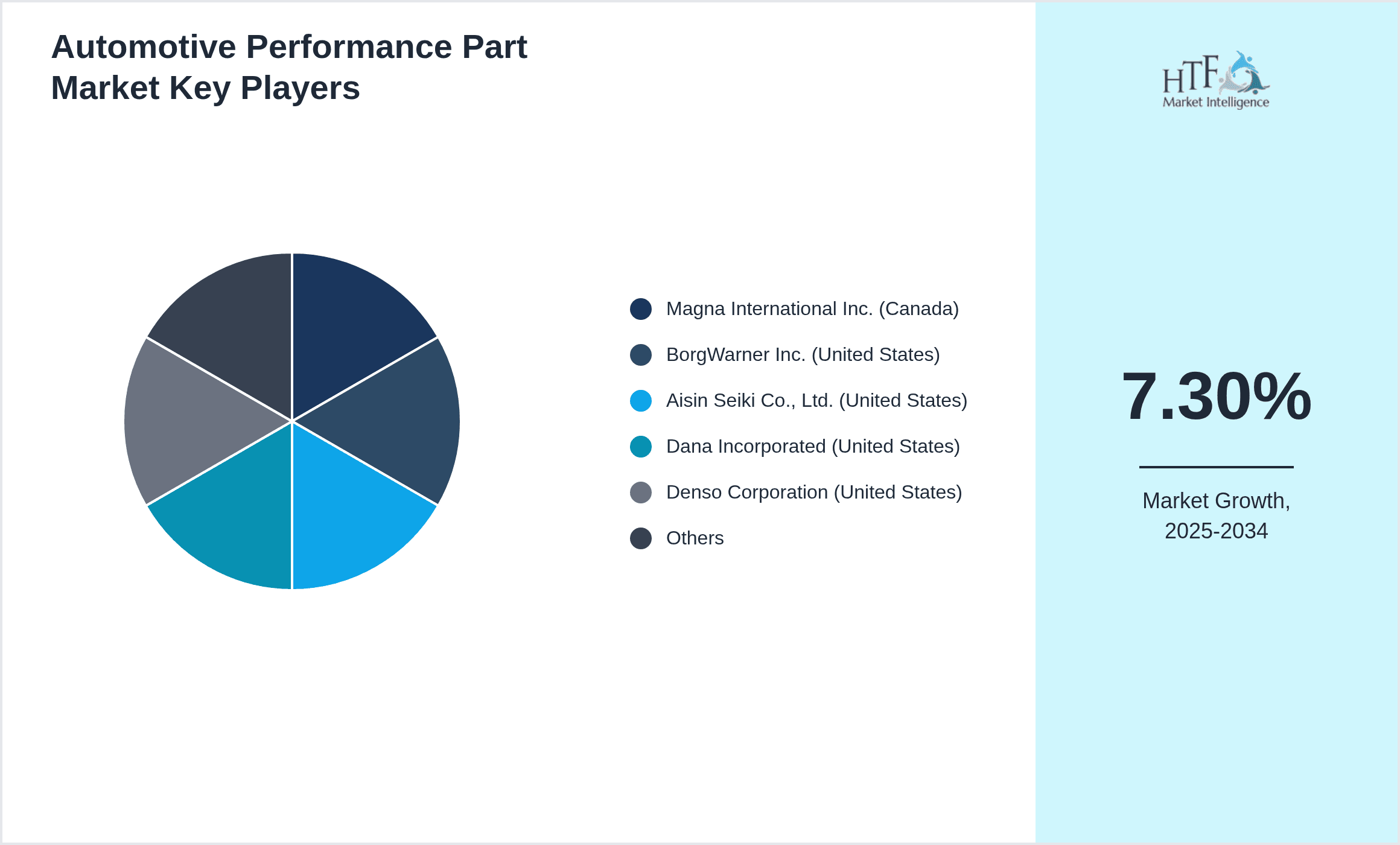

Leading Companies in North America Automotive Performance Part Market

- •Magna International Inc. (Canada)

- •BorgWarner Inc. (United States)

- •Aisin Seiki Co., Ltd. (United States)

- •Dana Incorporated (United States)

- •Denso Corporation (United States)

- •Edelbrock LLC (United States)

- •Continental AG (United States)

- •HKS Co., Ltd. (United States)

- •Holley Performance Products (United States)

- •Mopar (United States)

- •Delphi Technologies (United States)

- •TRW Automotive Holdings Corp. (United States)

- •Federal-Mogul LLC (United States)

- •Garrett Motion Inc. (United States)

- •Sachs Automotive Products (United States)

- •K&N Engineering, Inc. (United States)

- •Bilstein Group (United States)

- •Borla Performance Industries (United States)

- •Eibach Springs (United States)

- •Injen Technology (United States)

- •MSD Ignition (United States)

- •KW Automotive (United States)

- •Roush Performance (United States)

- •Remus USA (United States)

- •APR Performance (United States)

Market Breakdown

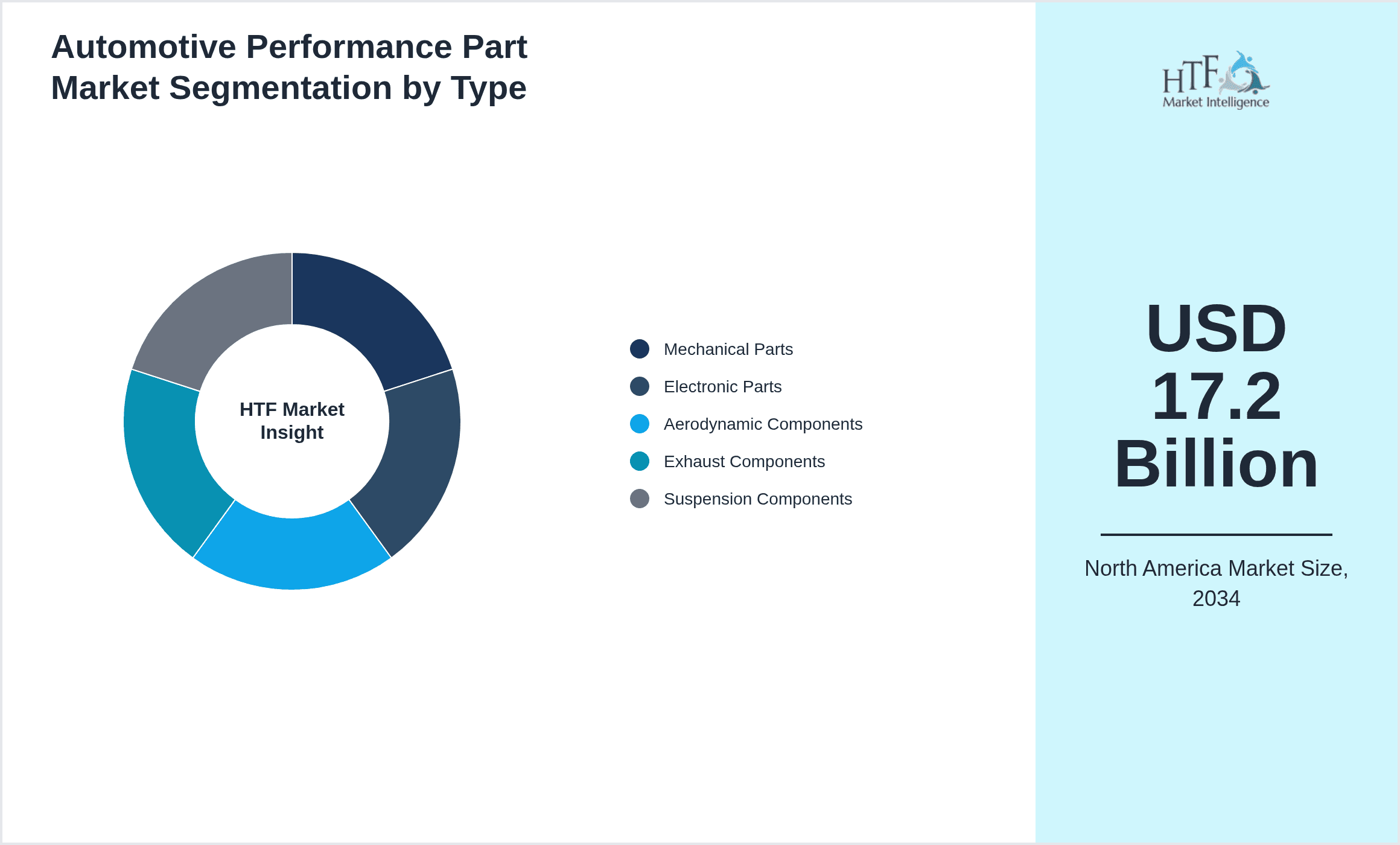

- •By Type

- ◦Mechanical Parts

- ◦Electronic Parts

- ◦Aerodynamic Components

- ◦Exhaust Components

- ◦Suspension Components

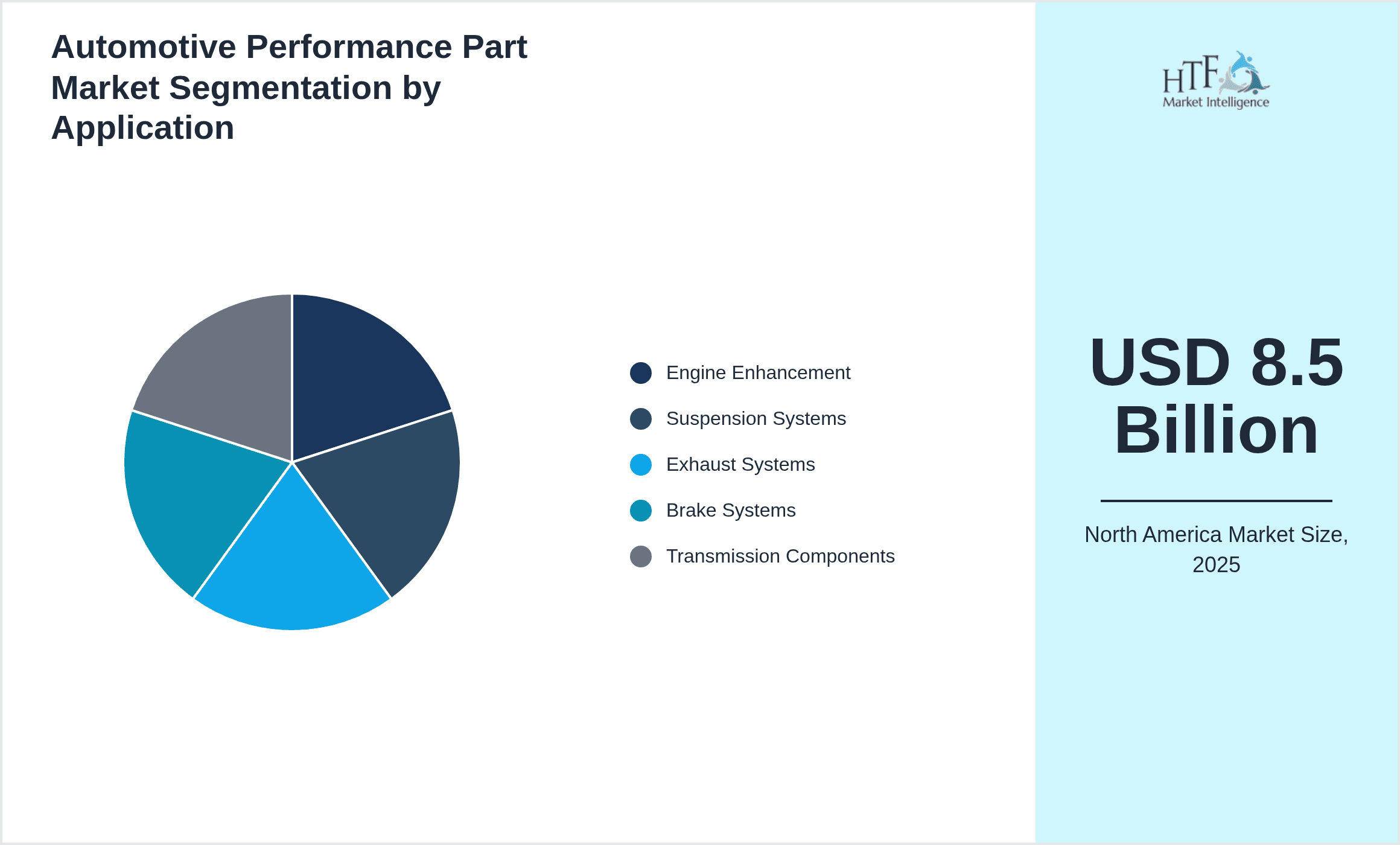

- •By Application

- ◦Engine Enhancement

- ◦Suspension Systems

- ◦Exhaust Systems

- ◦Brake Systems

- ◦Transmission Components

- •By Distribution Channel

- ◦Specialty Retailers

- ◦Online Platforms

- ◦Direct OEM Sales

- ◦Automotive Workshops

- •By Vehicle Type

- ◦Passenger Cars

- ◦Light Commercial Vehicles

- ◦Heavy Commercial Vehicles

- ◦Motorsport Vehicles

Growth Dynamics

- •The North America Automotive Performance Part market is propelled by rising consumer interest in vehicle customization and performance upgrades, particularly among younger demographics and motorsports enthusiasts. Increasing disposable income and vehicle ownership rates further stimulate aftermarket demand. Moreover, technological advancements in electronic components, such as engine control units and performance sensors, contribute to market expansion by enhancing vehicle efficiency and driving experience. The growing trend of eco-friendly performance parts aligns with environmental regulations, promoting sustainable product development. Furthermore, expanding e-commerce platforms ease access to performance parts, enabling wider market penetration. Investments in R&D to develop lightweight and durable materials also support growth by improving vehicle speed and fuel economy. Collectively, these factors create a favorable environment fostering robust market growth through 2034.

- •The market is witnessing increasing adoption of advanced technologies including electronic control modules, telemetry systems, and aerodynamic enhancements that improve vehicle efficiency and performance. Integration of IoT and smart sensors enables real-time monitoring and tuning, appealing to performance-focused consumers. Additionally, manufacturers are focusing on lightweight composite materials that reduce vehicle weight and enhance speed without compromising safety. The rise of motorsports and automotive enthusiast communities drives innovation and creates demand for specialized performance parts. Evolving consumer preferences toward electric and hybrid vehicles are prompting development of compatible performance components. Enhanced online sales channels and digital marketing strategies are also reshaping market dynamics by increasing product accessibility and customization options. These trends collectively position the market for sustained innovation-led growth.

- •Market growth faces challenges from stringent emissions and safety regulations that limit certain high-performance modifications. Compliance costs associated with environmental standards can increase product prices, potentially limiting consumer affordability. Supply chain disruptions and raw material price volatility also restrict consistent product availability. Furthermore, the rising popularity of electric vehicles introduces uncertainties, as traditional performance parts may not be compatible or require significant redesign. Counterfeit products and lack of standardization in the aftermarket pose risks to brand reputation and customer trust. Additionally, fluctuating fuel prices and economic downturns may reduce discretionary spending on performance upgrades. These restraints necessitate strategic innovation and regulatory alignment to sustain market momentum in North America.

- •Significant opportunities exist in expanding e-commerce platforms that provide broad market access to niche performance parts, enabling small manufacturers and aftermarket suppliers to reach new customer bases efficiently. The growing electric and hybrid vehicle segment offers untapped potential for developing specialized performance components compatible with alternative powertrains. Collaborations between OEMs and aftermarket suppliers can facilitate co-development of high-quality parts that meet regulatory requirements and consumer expectations. Additionally, increasing motorsport events and enthusiast communities create demand for advanced tuning and customization products. Geographic expansion into underserved North American regions and the rise of personalized vehicle experiences further enhance market potential. Investment in sustainable materials and eco-friendly performance solutions also presents avenues for differentiation and long-term growth.

- •The North America Automotive Performance Part market faces challenges including high product development costs driven by advanced technology integration and regulatory compliance. Intense competition among established players and new entrants pressures profit margins and necessitates continuous innovation. The complexity of adapting performance parts to diverse vehicle models and emerging electric vehicles adds technical hurdles. Supply chain disruptions and raw material shortages impact production timelines and cost structures. Moreover, consumer concerns about warranty voidance and vehicle safety limit adoption of aftermarket modifications. Regulatory uncertainty regarding emissions and safety standards may delay product launches or restrict market access. Addressing counterfeit parts and ensuring product authenticity remain critical to maintaining customer trust and brand reputation in a competitive landscape.

Market Trends

- •The North America Automotive Performance Part market is increasingly embracing digital transformation, with manufacturers leveraging e-commerce and digital marketing to reach performance enthusiasts directly. This shift enhances customer engagement, personalization, and aftersales support, fostering brand loyalty and expanding market reach. Additionally, advanced electronic performance parts integrating IoT and smart sensor technologies are gaining traction, enabling real-time vehicle optimization and diagnostics. Environmental sustainability is influencing product development trends, with growing demand for lightweight, eco-friendly materials and components compatible with electric and hybrid vehicles. Furthermore, collaborations between OEMs and aftermarket suppliers are becoming common to develop innovative, compliant products. The rise of motorsports and automotive customization culture continues to drive demand for specialized, high-quality performance parts. These trends collectively shape a technologically advanced, customer-focused, and environmentally conscious market landscape.

- •Emerging trends include the rapid adoption of additive manufacturing technologies such as 3D printing to produce customized performance parts, reducing lead times and costs. Integration of artificial intelligence and machine learning algorithms in performance tuning software is enabling predictive maintenance and optimized vehicle settings. Market players are increasingly focusing on developing performance components tailored for electric vehicles, addressing unique powertrain and cooling system requirements. Subscription-based performance part services and modular upgrade kits are gaining popularity, offering flexibility and affordability. Additionally, there is a growing emphasis on sustainable sourcing and circular economy principles, encouraging recycling and reuse of automotive components. These innovations are transforming the performance parts market into a more agile, tech-driven, and sustainable ecosystem.

- •Strategic industry moves include partnerships between automotive aftermarket suppliers and technology firms to co-develop smart performance parts integrating connectivity and telematics. Companies are investing in R&D centers specializing in electric and hybrid vehicle performance upgrades. The introduction of eco-friendly exhaust and emission control systems aligns with regulatory demands and consumer preferences. Moreover, several market leaders have launched digital platforms offering virtual customization and augmented reality-based fitting simulations, enhancing customer experience. These initiatives demonstrate a market-wide commitment to innovation, compliance, and enhanced user engagement. Market players are also expanding geographically within North America, targeting emerging urban and suburban areas with growing automotive aftermarket demand. These strategic trends are driving competitive advantage and market expansion.

- •The increasing digitalization of the automotive aftermarket is streamlining inventory management, order processing, and customer relationship management through cloud-based platforms and AI analytics. Sustainability considerations are influencing material choices, with bio-based composites and recyclable metals gaining adoption in performance parts manufacturing. Enhanced collaboration among suppliers, OEMs, and distributors fosters integrated supply chains, improving efficiency and reducing time-to-market. Additionally, the rise of social media and influencer marketing is shaping consumer preferences and accelerating product adoption among younger demographics. Demand for modular and easily installable performance upgrades is rising, facilitating DIY customization. These trends reflect a convergence of technology, sustainability, and consumer-centric approaches transforming market operations and growth trajectories.

- •Collaborative ecosystems are forming between aftermarket brands, tuning shops, and motorsport organizations to co-create specialized performance solutions and promote brand visibility. Strategic alliances with logistics providers enhance product distribution efficiency across North America’s diverse geographic landscape. Consumer preferences are shifting towards integrated performance packages combining mechanical and electronic upgrades for holistic vehicle enhancement. Market segmentation is becoming more refined, targeting specific vehicle types and driving styles through tailored product offerings. Value chain evolution includes increased direct-to-consumer sales and personalized service models. These collaborative and consumer-driven trends are fostering innovation, market penetration, and enhanced competitive positioning.

- •The future direction of the North America Automotive Performance Part market includes disruptive innovations such as AI-powered vehicle tuning, blockchain-based supply chain transparency, and advanced materials like graphene composites. Market players are exploring augmented and virtual reality tools for customer education and product customization. The transition to electric and autonomous vehicles presents both challenges and opportunities for performance upgrades, necessitating new product development and market strategies. Emerging business models including performance part-as-a-service and subscription offerings are anticipated to gain traction. Overall, the market is poised for technological convergence, sustainability integration, and enhanced user experience innovations shaping long-term growth.

Market Opportunities

- •The North America Automotive Performance Part market offers significant growth potential through expansion of e-commerce channels, enabling access to wider customer segments and reducing traditional distribution bottlenecks. Leveraging data analytics and AI for personalized marketing and product recommendations can enhance customer acquisition and retention. Growth opportunities also lie in developing electric vehicle-compatible performance parts, addressing a rapidly expanding vehicle segment with unique technical requirements. Collaborations with OEMs to co-develop certified performance upgrades can create trusted product lines that address warranty and regulatory concerns. Geographic expansion into underserved markets within the region presents untapped demand. Investment in sustainable and lightweight materials aligns with consumer preferences and regulatory trends, offering differentiation and market leadership potential. Additionally, motorsports sponsorships and events provide platforms for brand visibility and product validation fostering market penetration.

- •Emerging market segments such as off-road and specialty vehicles represent lucrative opportunities for performance part innovations tailored to rugged use and enhanced durability. Integration of smart technologies and IoT in performance parts opens avenues for new product categories and service models, including predictive maintenance and remote tuning. The rise of vehicle subscription services and shared mobility creates demand for modular, easily upgradeable performance components. Strategic acquisitions of niche technology startups can accelerate innovation and portfolio diversification. Furthermore, increasing focus on vehicle safety performance enhancements offers prospects for brake and suspension system upgrades. These opportunities enable market players to broaden offerings, capture new customer bases, and strengthen competitive advantage in North America.

- •Investment opportunities abound in developing aftermarket diagnostic and tuning software compatible with diverse vehicle models, enhancing performance customization capabilities. Partnerships with digital platforms and automotive communities can facilitate product promotion and consumer engagement. Expanding product lines to include sustainable and recyclable components aligns with environmental regulations and growing consumer consciousness. Enhancing direct-to-consumer sales channels supported by virtual fitting and customization tools can improve customer experience and conversion rates. Additionally, geographic diversification into emerging urban centers with rising vehicle ownership can drive market volume growth. These strategic avenues provide multiple pathways for revenue growth and innovation leadership in the North American automotive performance parts sector.

- •Geographic expansion within North America, especially targeting Canada and Mexico, offers substantial growth potential due to increasing vehicle ownership and aftermarket awareness. Development of performance parts for electric and hybrid vehicles addresses emerging market needs and regulatory compliance. Customized product offerings for niche vehicle types such as motorsport and off-road increase market segmentation and consumer appeal. Strategic alliances with automotive service providers and tuning shops can facilitate product adoption and aftersales support. Furthermore, leveraging digital marketing and social media influencers can enhance brand visibility and consumer trust. These opportunities support market diversification and sustained growth trajectories.

- •The development of modular and upgradeable performance kits presents an opportunity to simplify vehicle modifications, appealing to both DIY enthusiasts and professional tuners. Collaborations with motorsport teams for product development and testing enhance credibility and innovation. Expanding warranty-backed performance parts can alleviate consumer concerns regarding vehicle safety and reliability. Investment in supply chain innovations including just-in-time inventory and regional warehouses improves distribution efficiency and customer satisfaction. Additionally, exploring emerging materials such as carbon fiber composites can lead to high-performance, lightweight components with premium market positioning. These strategic initiatives position market players to capitalize on evolving consumer preferences and technological advancements.

- •Partnerships and acquisitions of technology startups specializing in AI, IoT, and advanced materials can accelerate product innovation and market responsiveness. Expanding aftermarket services such as installation, tuning, and maintenance through digital platforms enhances customer engagement and revenue streams. Development of eco-friendly performance parts aligned with tightening emissions regulations offers differentiation and regulatory compliance benefits. Geographic targeting of metropolitan areas with high vehicle modification rates can optimize marketing and sales efforts. The rise of connected vehicles enables integration of performance parts with vehicle telematics and diagnostics, creating value-added services. These opportunities collectively enable sustainable growth and competitive differentiation in the North American automotive performance parts market.

- •Anticipated regulatory changes promoting cleaner emissions and vehicle safety standards create long-term demand for innovative performance parts that comply with new requirements. Market players can leverage this by investing in R&D for advanced exhaust systems, lightweight components, and electronic control modules. Growth in motorsports and automotive enthusiast communities will continue to drive demand for specialized, high-quality performance upgrades. Expanding digital marketplaces and global supply chain integration facilitate efficient product distribution and market access. Furthermore, societal trends favoring vehicle personalization and sustainability provide a favorable backdrop for introducing novel performance solutions. These factors collectively present strategic growth opportunities for market participants.

Market Challenges

- •The North America Automotive Performance Part market faces significant challenges from stringent regulatory frameworks that impose strict emissions and safety standards, limiting design and material options for performance parts. Compliance with these regulations increases development costs and extends time-to-market, affecting profitability. Supply chain disruptions, exacerbated by global events and raw material shortages, create production delays and cost volatility. Additionally, the rise of electric vehicles introduces technical challenges as traditional performance parts may not be compatible, requiring substantial redesign and investment. Counterfeit and substandard aftermarket parts pose risks to brand reputation and consumer safety, necessitating rigorous quality control and authentication measures. Economic fluctuations impacting consumer discretionary spending also constrain market growth, as performance upgrades are often non-essential expenditures. These challenges require strategic innovation, regulatory alignment, and operational resilience to maintain competitiveness.

- •Technical complexity in integrating advanced electronics and smart technologies into performance parts presents development and manufacturing hurdles. Diverse vehicle models and rapid technological changes demand flexible, adaptable product designs, increasing R&D investment. The high cost of premium materials and technologies may limit market penetration among price-sensitive consumers. Intense competition from established brands and emerging players pressures pricing and market share. Additionally, warranty concerns and potential vehicle damage deter some consumers from aftermarket modifications. Geographic disparities in aftermarket infrastructure and consumer awareness create uneven market development across North America. Finally, cybersecurity risks associated with connected performance parts require robust safeguards to protect vehicle systems and user data. Addressing these multifaceted challenges is critical for sustainable market growth.

- •Real-world examples include delays in launching electronic control units due to evolving emissions compliance standards, and supply chain bottlenecks impacting delivery of lightweight suspension components. Some companies face legal challenges linked to counterfeit part distribution affecting brand image. The shifting regulatory landscape around electric vehicle modifications demands rapid innovation cycles to stay relevant. Pricing pressures from low-cost imports and aftermarket alternatives challenge profitability. Additionally, consumer skepticism regarding the impact of performance parts on vehicle warranty and insurance has slowed adoption rates. To mitigate these challenges, industry players are investing in quality assurance, customer education, and strategic partnerships. Nonetheless, overcoming these barriers requires continuous adaptation and proactive market strategies.

- •Cost structures are strained by the need for advanced materials, compliance testing, and technology integration, leading to higher retail prices that may limit consumer access. Price sensitivity in certain North American markets necessitates balancing quality with affordability. Competitive pricing strategies can erode margins, especially for small and mid-sized manufacturers. Additionally, economic downturns and fluctuating fuel prices influence consumer spending on non-essential automotive upgrades. Maintaining profitability while investing in innovation and regulatory compliance remains a delicate challenge. Market players need to optimize operations, leverage economies of scale, and explore value-added services to sustain financial health in a competitive environment.

- •Regulatory compliance complexities arise from varying standards across the United States, Canada, and Mexico, requiring tailored product certifications and testing. Uncertainties in policy enforcement timelines hinder long-term planning and investment. Standardization issues in aftermarket part specifications impede interoperability and quality assurance. Trade policies and tariffs affect cost structures and supply chain decisions. Navigating these regulatory frameworks demands dedicated resources and expertise, impacting smaller players disproportionately. Collaboration with regulatory bodies and industry associations is essential to shape favorable policies and ensure market stability. Addressing regulatory challenges effectively is critical for sustained growth and market access in North America.

- •Market saturation in key urban centers intensifies competition, making differentiation through innovation and brand loyalty imperative. Limited availability of skilled technicians and infrastructure for installation and maintenance affects customer satisfaction and adoption rates. Differentiating products in a crowded marketplace requires continuous innovation and strong marketing efforts. The presence of counterfeit products undermines consumer confidence and poses safety risks. Managing complex supply chains across a vast geographic region entails logistical challenges and cost management. Talent shortages in R&D and technical fields may slow innovation. Overcoming these operational challenges is vital for maintaining competitive advantage and ensuring market growth.

- •Supply chain disruptions due to geopolitical tensions, natural disasters, or pandemics affect raw material availability and transportation reliability. Talented workforce shortages in engineering and manufacturing sectors constrain capacity expansion and innovation. Infrastructure gaps in certain North American regions limit efficient distribution and service delivery. Managing inventory levels to balance demand fluctuations against storage costs remains challenging. Cybersecurity threats targeting connected automotive parts require investment in robust protection measures. Addressing these multifaceted challenges necessitates strategic planning, investment in technology, and collaboration with partners to build resilient operations capable of adapting to evolving market conditions.

Regulatory Framework

- •Between 2019 and 2024, North America implemented several regulations impacting automotive performance parts, including updates to the Environmental Protection Agency (EPA) emission standards that require stricter control of aftermarket exhaust and engine components. These regulations mandate compliance with emission limits to reduce pollutants without compromising performance. The National Highway Traffic Safety Administration (NHTSA) introduced enhanced safety standards for brake and suspension parts, ensuring aftermarket products meet OEM-equivalent performance. Canada’s Motor Vehicle Safety Act was updated to align with stricter emissions and safety requirements, affecting part certification and market access. Mexico introduced new regulations targeting counterfeit automotive parts to improve consumer safety and market integrity. These regulatory developments necessitate rigorous testing, certification, and quality control by manufacturers and distributors, influencing product design and market entry strategies across North America.

- •Enforcement mechanisms include mandatory product certification, regular audits, and penalties for non-compliance, with increased collaboration between regulatory agencies and customs authorities to prevent illegal imports. Industry stakeholders have responded by adopting advanced compliance protocols and investing in R&D for eco-friendly and safe performance parts. These regulations have prompted innovation in emission-reducing technologies and safer braking systems. Manufacturers must maintain detailed documentation and traceability for aftermarket parts, aligning with evolving regulatory expectations. The regulatory landscape fosters a market environment prioritizing consumer safety, environmental sustainability, and product reliability in North America.

- •Safety standards introduced between 2019 and 2024 require stringent testing for durability and performance under varied operating conditions, influencing design and manufacturing processes. Environmental norms encourage development of lightweight and recyclable materials to reduce vehicle weight and emissions. Operational guidelines emphasize proper installation and maintenance instructions to ensure aftermarket parts do not compromise vehicle integrity. These regulatory requirements have led to increased collaboration between OEMs and aftermarket suppliers to develop compliant performance parts. The evolving policy environment supports sustainable growth while safeguarding consumer interests and environmental health.

- •Country-specific mandates include the California Air Resources Board (CARB) regulations, which impose additional emission control requirements within California and neighboring states, affecting part design and sales strategies. Canada’s provincial regulations similarly influence product compliance and market practices. Mexico’s adoption of international standards for automotive parts certification enhances market transparency and safety. Timelines for implementation vary, with phased compliance deadlines providing manufacturers time to adapt. These mandates require ongoing monitoring and alignment by market participants to maintain access across North America.

- •Government initiatives include incentive programs promoting adoption of environmentally friendly automotive technologies and support for R&D in advanced performance parts. Industry associations collaborate with regulatory bodies to develop best practices and compliance frameworks. Public awareness campaigns emphasize the importance of certified aftermarket parts to enhance vehicle safety and reduce environmental impact. These policy frameworks create an enabling environment for innovation and responsible market development within the North American automotive performance parts sector.

Market Intelligence

- •15th March 2024, Magna International Inc. launched a new line of lightweight, high-performance suspension components designed specifically for electric vehicles, aiming to improve handling and energy efficiency. This innovative product line integrates advanced composite materials and smart sensors to provide real-time performance data to drivers and service centers. Targeted at North American automotive manufacturers and aftermarket suppliers, the launch aligns with increasing demand for EV-compatible performance parts and regulatory compliance. Magna’s strategic objective is to capture the growing EV segment while addressing performance and sustainability simultaneously, strengthening its competitive position in the North American market. The products are available through both OEM partnerships and specialty retailers, enhancing accessibility.

- •22nd November 2023, Holley Performance Products introduced an advanced electronic fuel injection system featuring adaptive learning technology, capable of optimizing engine performance across diverse vehicle models. This system utilizes AI algorithms to adjust fuel delivery dynamically, improving fuel efficiency and reducing emissions without sacrificing power. Positioned for the North American aftermarket and motorsports segments, the product reflects Holley’s commitment to innovation and meeting stringent emission regulations. The launch is expected to accelerate adoption of electronic performance parts, offering tuners and vehicle owners enhanced customization and control. Holley aims to leverage this technology to expand its market share and respond to evolving consumer preferences in the automotive performance sector.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.5 Billion |

| Forecast Year Market Size | USD 17.2 Billion |

| CAGR | 7.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.1% |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Magna International Inc. (Canada), BorgWarner Inc. (United States), Aisin Seiki Co., Ltd. (United States), Dana Incorporated (United States), Denso Corporation (United States), Edelbrock LLC (United States), Continental AG (United States), HKS Co., Ltd. (United States), Holley Performance Products (United States), Mopar (United States), Delphi Technologies (United States), TRW Automotive Holdings Corp. (United States), Federal-Mogul LLC (United States), Garrett Motion Inc. (United States), Sachs Automotive Products (United States), K&N Engineering, Inc. (United States), Bilstein Group (United States), Borla Performance Industries (United States), Eibach Springs (United States), Injen Technology (United States), MSD Ignition (United States), KW Automotive (United States), Roush Performance (United States), Remus USA (United States), APR Performance (United States) |

North America Automotive Performance Part Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.