Global China IoT for Public Safety Market - Outlook 2020-2034

Global China IoT for Public Safety Market is segmented by Type (Connected Sensors, Network Equipment, Software Solutions, Edge Computing Devices, Cloud Platforms), Application (Emergency Response, Surveillance, Disaster Management, Traffic Monitoring, Public Health Monitoring), Deployment Model (Cloud-based, On-Premise, Hybrid), Service Type (Managed Services, Professional Services, Support and Maintenance), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global China IoT for Public Safety market focuses on delivering interconnected solutions integrating sensors, network infrastructure, software, and cloud computing to improve public safety applications such as emergency response, surveillance, and disaster management. The market facilitates enhanced situational awareness, rapid threat detection, and efficient resource deployment through real-time data monitoring and analytics.

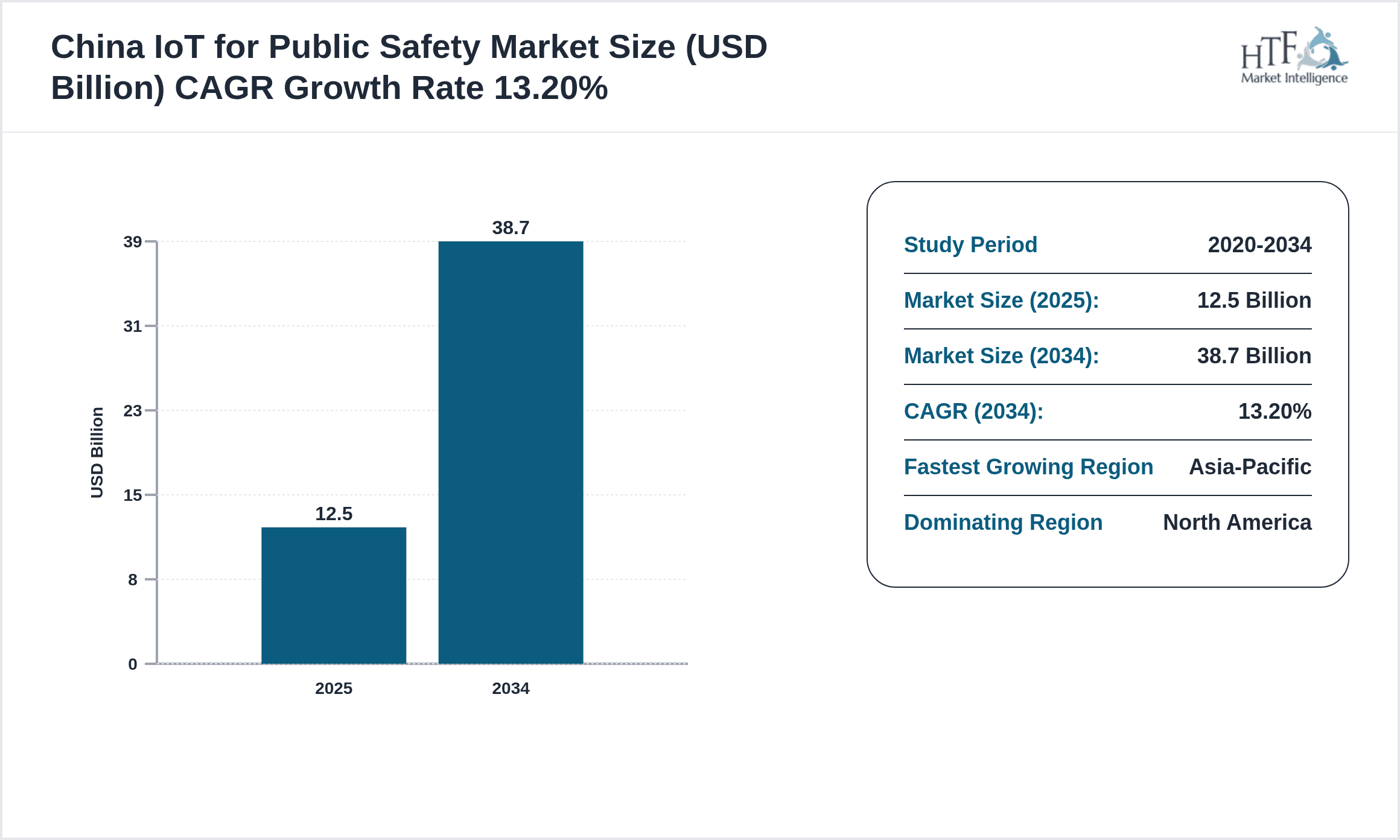

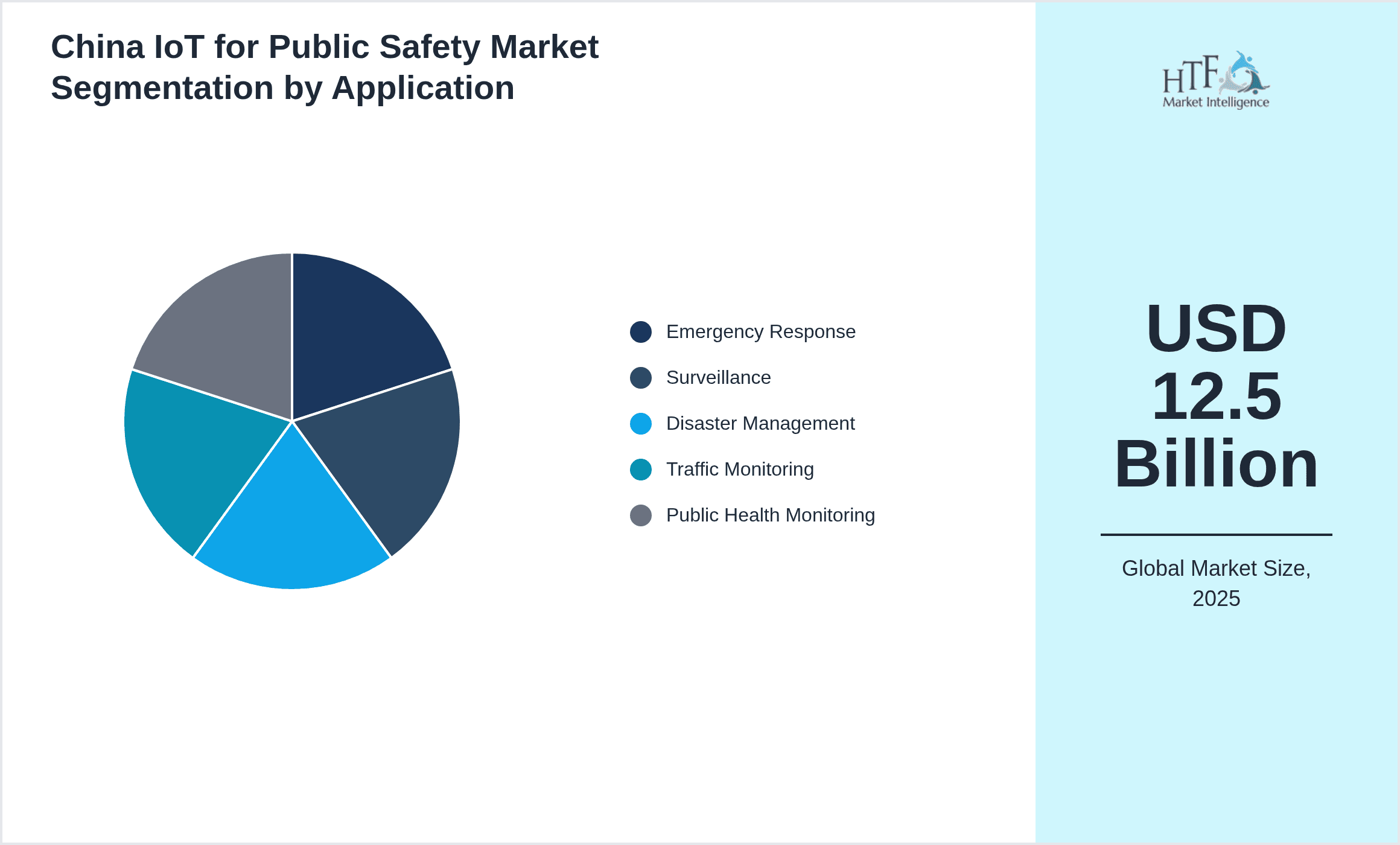

- •Key market highlights include a base market size of USD 12.5 Billion in 2025 growing to USD 38.7 Billion by 2034 at a CAGR of 13.2%, driven by rapid adoption of IoT technologies in public safety infrastructure globally, especially in North America and Asia-Pacific regions.

- •This market presents significant value propositions for governments, emergency services, healthcare agencies, and urban planners by enabling proactive public safety measures, reducing response times, and improving overall community resilience against safety threats through advanced IoT integration.

Competitive Landscape

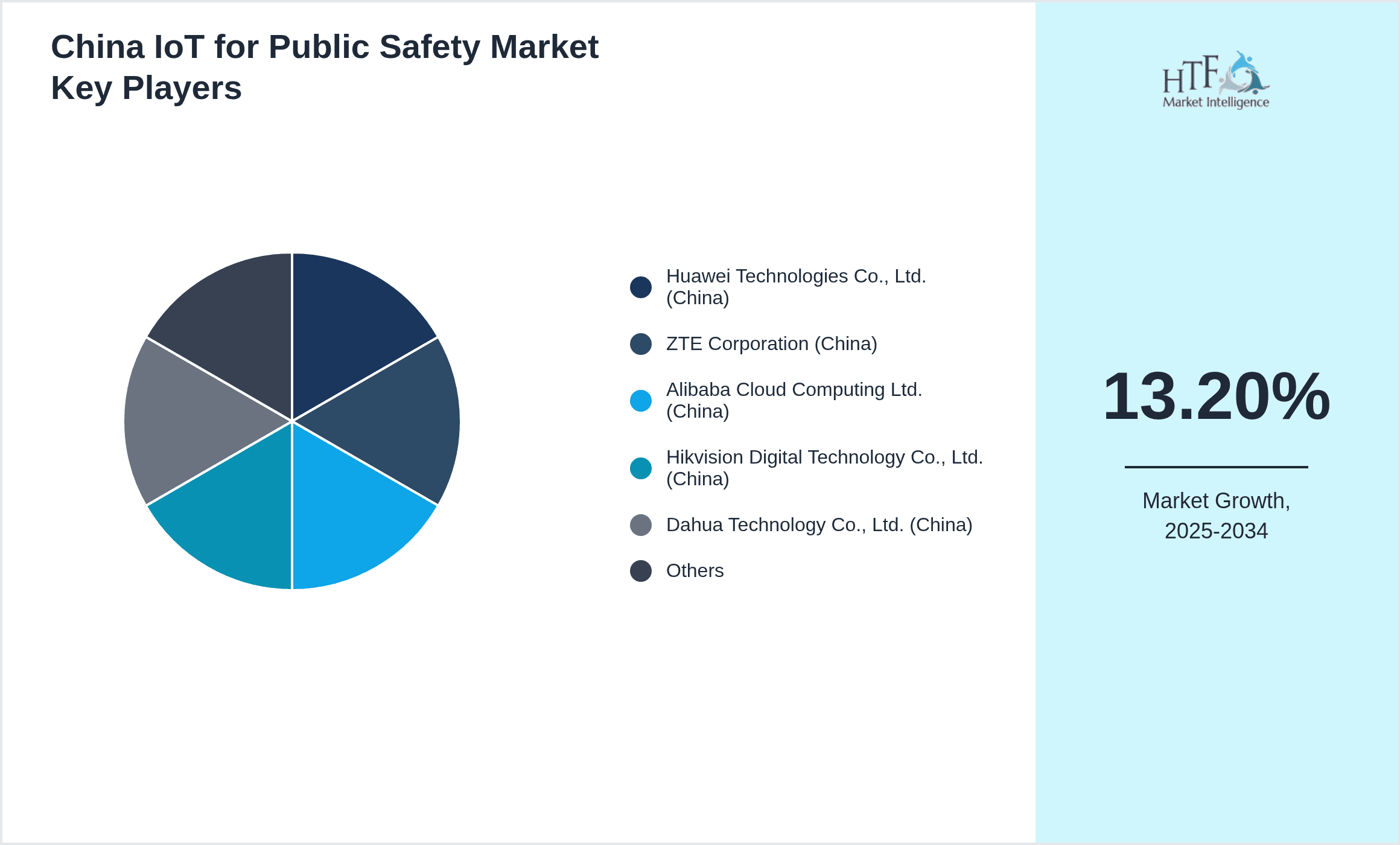

The Global China IoT for Public Safety market is characterized by intense competition among technology providers offering sensor hardware, networking equipment, software platforms, and edge computing solutions. Market players are focusing on innovation through AI integration, advanced analytics, and secure communication protocols to differentiate their offerings. Strategic partnerships and collaborations between IoT device manufacturers, cloud service providers, and public safety agencies are common to enhance solution efficacy. Additionally, mergers and acquisitions are shaping market consolidation, enabling companies to expand geographic reach and product portfolios. Pricing strategies revolve around value-added services and scalable deployment models, while regional competition is influenced by regulatory compliance and infrastructure capabilities. Future trends indicate increased investment in cybersecurity measures and interoperable platforms to advance market positioning and meet growing demand for integrated public safety IoT solutions.

Leading Companies in China IoT for Public Safety Market

- •Huawei Technologies Co., Ltd. (China)

- •ZTE Corporation (China)

- •Alibaba Cloud Computing Ltd. (China)

- •Hikvision Digital Technology Co., Ltd. (China)

- •Dahua Technology Co., Ltd. (China)

- •Tencent Holdings Ltd. (China)

- •China Mobile Communications Corporation (China)

- •China Telecom Corporation Limited (China)

- •China Unicom (Hong Kong) Limited (China)

- •SenseTime Group Limited (China)

- •Neusoft Corporation (China)

- •Inspur Group Co., Ltd. (China)

- •Sunsea AIoT Technology Co., Ltd. (China)

- •FiberHome Telecommunication Technologies Co., Ltd. (China)

- •Unisound Information Technology Co., Ltd. (China)

- •Alibaba Group Holding Limited (China)

- •JD.com, Inc. (China)

- •iFlytek Co., Ltd. (China)

- •China Electronics Technology Group Corporation (China)

- •Sugon Information Industry Co., Ltd. (China)

- •Xiaomi Corporation (China)

- •Lenovo Group Limited (China)

- •Baidu, Inc. (China)

- •Meituan Dianping (China)

- •Coolpad Group Limited (China)

Market Breakdown

- •By Type

- ◦Connected Sensors

- ◦Network Equipment

- ◦Software Solutions

- ◦Edge Computing Devices

- ◦Cloud Platforms

- •By Application

- ◦Emergency Response

- ◦Surveillance

- ◦Disaster Management

- ◦Traffic Monitoring

- ◦Public Health Monitoring

- •By Deployment Model

- ◦Cloud-based

- ◦On-Premise

- ◦Hybrid

- •By Service Type

- ◦Managed Services

- ◦Professional Services

- ◦Support and Maintenance

Growth Dynamics

The growing need for enhanced public safety infrastructure globally is driving adoption of IoT solutions, allowing real-time monitoring and faster emergency response. Increasing urbanization and rising safety concerns in megacities are key catalysts fueling market expansion. Governments worldwide are investing heavily in smart city initiatives integrating IoT for public safety, creating large-scale deployment opportunities. Technological advancements in sensor accuracy, edge computing, and AI-based analytics are enabling more effective threat detection and management, thereby accelerating market growth. Additionally, rising awareness about disaster preparedness and traffic safety is encouraging adoption across multiple public safety applications. The convergence of IoT with 5G networks further enhances connectivity and data transmission speed, supporting expansive and reliable public safety networks. These dynamics collectively underpin robust market growth through the forecast period.

Market Trends

The market is witnessing rapid integration of AI and machine learning algorithms into IoT platforms to improve predictive analytics and automated threat detection in public safety scenarios. Adoption of cloud-native architectures is increasing, enabling scalable and flexible deployment of public safety solutions. There is a notable shift towards edge computing to reduce latency and enable real-time decision-making at the device level. Furthermore, enhanced cybersecurity frameworks are being implemented to protect sensitive public safety data from evolving cyber threats. Collaborative ecosystems involving technology providers, government agencies, and emergency services are becoming prevalent to co-develop customized IoT solutions. Sustainability trends are also influencing product design, with energy-efficient sensors and eco-friendly materials gaining traction in the market.

Market Opportunities

The expanding smart city projects globally offer significant opportunities for integrating China IoT public safety technologies to enhance urban security and emergency management. Untapped markets in Latin America and the Middle East & Africa show high growth potential due to increasing infrastructure investments and rising safety concerns. Emerging applications such as public health monitoring and pandemic response are creating new demand streams for IoT-based public safety solutions. Additionally, advancements in 5G and AI open avenues for innovative product development and service offerings, increasing market penetration. Collaborations with telecom operators and cloud providers present opportunities for bundled offerings and enhanced connectivity. Growing regulatory emphasis on public safety and data security further supports market expansion by encouraging adoption of certified IoT systems.

Market Challenges

Key challenges include high initial capital expenditure for IoT infrastructure deployment and integration complexities with legacy public safety systems. Privacy concerns and data protection regulations restrict data sharing and use, potentially limiting solution capabilities. Fragmentation of standards and lack of interoperability among IoT devices hinder seamless integration and scalability. Technical limitations such as network reliability in remote areas and power constraints for sensors affect system performance. Additionally, cybersecurity risks and vulnerability to hacking pose serious threats to public safety networks, requiring robust protective measures. Market fragmentation with multiple vendors and varying solution maturity levels complicates decision-making for buyers. Addressing these challenges requires coordinated efforts across industry stakeholders and regulatory bodies to enable sustainable market growth.

Regulatory Framework

Between 2020 and 2025, several countries and regions enacted regulations to ensure the security and privacy of IoT implementations in public safety. GDPR in Europe mandates strict data privacy requirements, influencing IoT data management practices globally. The United States introduced the IoT Cybersecurity Improvement Act in 2020, establishing baseline security standards for government IoT devices, which indirectly impacts public safety device vendors worldwide. China has implemented comprehensive cybersecurity laws requiring localization and data protection for IoT networks used in critical infrastructure including public safety. These regulations necessitate compliance with encryption standards, secure authentication, and data sovereignty policies. The evolving regulatory landscape prompts vendors to incorporate compliance features into their solutions, shaping product development and market entry strategies. Additionally, governments encourage standardization efforts to foster interoperability and safety, facilitating smoother adoption of IoT public safety technologies.

Market Intelligence

- •15th January 2025, Huawei Technologies Co., Ltd. launched its advanced AI-powered public safety IoT platform integrating edge computing and 5G connectivity to enhance real-time emergency response capabilities. The platform supports multi-sensor data fusion and predictive analytics, targeting large-scale smart city deployments globally. This innovation aims to reduce response times and improve situational awareness for first responders. Huawei plans strategic partnerships with municipal governments to accelerate adoption and tailor solutions to local requirements. Source: Huawei Official Press Release

- •3rd March 2025, Alibaba Cloud Computing Ltd. introduced a cloud-native IoT security framework designed to safeguard public safety data against cyber threats. The solution incorporates blockchain technology for data integrity and uses AI-driven threat detection to monitor network anomalies. This initiative positions Alibaba Cloud as a leader in secure IoT deployments, addressing growing concerns over data breaches in public safety systems. The offering targets government agencies and critical infrastructure operators worldwide. Source: Alibaba Cloud News

- •22nd May 2025, SenseTime Group Limited announced collaboration with China Mobile Communications Corporation to develop large-scale smart surveillance networks leveraging IoT cameras and AI analytics. This partnership aims to enhance urban security monitoring and traffic management across multiple Chinese cities, with plans for international expansion. The project focuses on integrating real-time video analytics with emergency response systems to optimize public safety operations. Source: SenseTime Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 38.7 Billion |

| CAGR | 13.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.9% |

| Scope of Report | Market is segmented by Type (Connected Sensors, Network Equipment, Software Solutions, Edge Computing Devices, Cloud Platforms), Application (Emergency Response, Surveillance, Disaster Management, Traffic Monitoring, Public Health Monitoring), Deployment Model (Cloud-based, On-Premise, Hybrid), Service Type (Managed Services, Professional Services, Support and Maintenance) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Huawei Technologies Co., Ltd. (China), ZTE Corporation (China), Alibaba Cloud Computing Ltd. (China), Hikvision Digital Technology Co., Ltd. (China), Dahua Technology Co., Ltd. (China), Tencent Holdings Ltd. (China), China Mobile Communications Corporation (China), China Telecom Corporation Limited (China), China Unicom (Hong Kong) Limited (China), SenseTime Group Limited (China), Neusoft Corporation (China), Inspur Group Co., Ltd. (China), Sunsea AIoT Technology Co., Ltd. (China), FiberHome Telecommunication Technologies Co., Ltd. (China), Unisound Information Technology Co., Ltd. (China), Alibaba Group Holding Limited (China), JD.com, Inc. (China), iFlytek Co., Ltd. (China), China Electronics Technology Group Corporation (China), Sugon Information Industry Co., Ltd. (China), Xiaomi Corporation (China), Lenovo Group Limited (China), Baidu, Inc. (China), Meituan Dianping (China), Coolpad Group Limited (China) |

Global China IoT for Public Safety Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.