Global Power Conversion Technologies Market Size, Growth & Revenue 2024-2034

Global Power Conversion Technologies Market is segmented by Application (Renewable Energy, Industrial Automation, Consumer Electronics, Electric Vehicles, Telecommunications), Type (AC-DC Converters, DC-DC Converters, Inverters, Rectifiers, Others), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Power Conversion Technologies market comprises devices and systems that convert electrical power efficiently across various formats to serve diverse industries including renewable energy, electric vehicles, telecommunications, consumer electronics, and industrial automation. This market includes AC-DC converters, DC-DC converters, inverters, and rectifiers, along with supporting control hardware and software, aimed at optimizing energy use and enhancing system reliability.

- •Key market highlights include a robust CAGR of 9.5% projected through 2034, driven by increasing adoption of renewable energy sources, proliferation of electric vehicles, and growing demand for energy-efficient industrial and consumer applications worldwide.

- •The market offers significant value propositions by enabling reduced energy losses, supporting sustainability goals, and facilitating smart grid integration, making it strategically important for stakeholders in energy, transportation, and electronics sectors.

Competitive Landscape

The Global Power Conversion Technologies market exhibits intense competition characterized by rapid technological innovation, strategic partnerships, and diversified product portfolios. Leading players focus on enhancing efficiency, miniaturization, and integration of power conversion components to meet stringent regulatory standards and customer expectations. Market rivalry is heightened by the influx of new entrants specializing in semiconductor advancements and energy management solutions. Companies leverage mergers, acquisitions, and collaborations to expand geographic reach and technology capabilities while differentiating through price competitiveness and service excellence. Innovation in wide bandgap semiconductors and digital control systems serve as key competitive levers driving market leadership and shaping future industry dynamics.

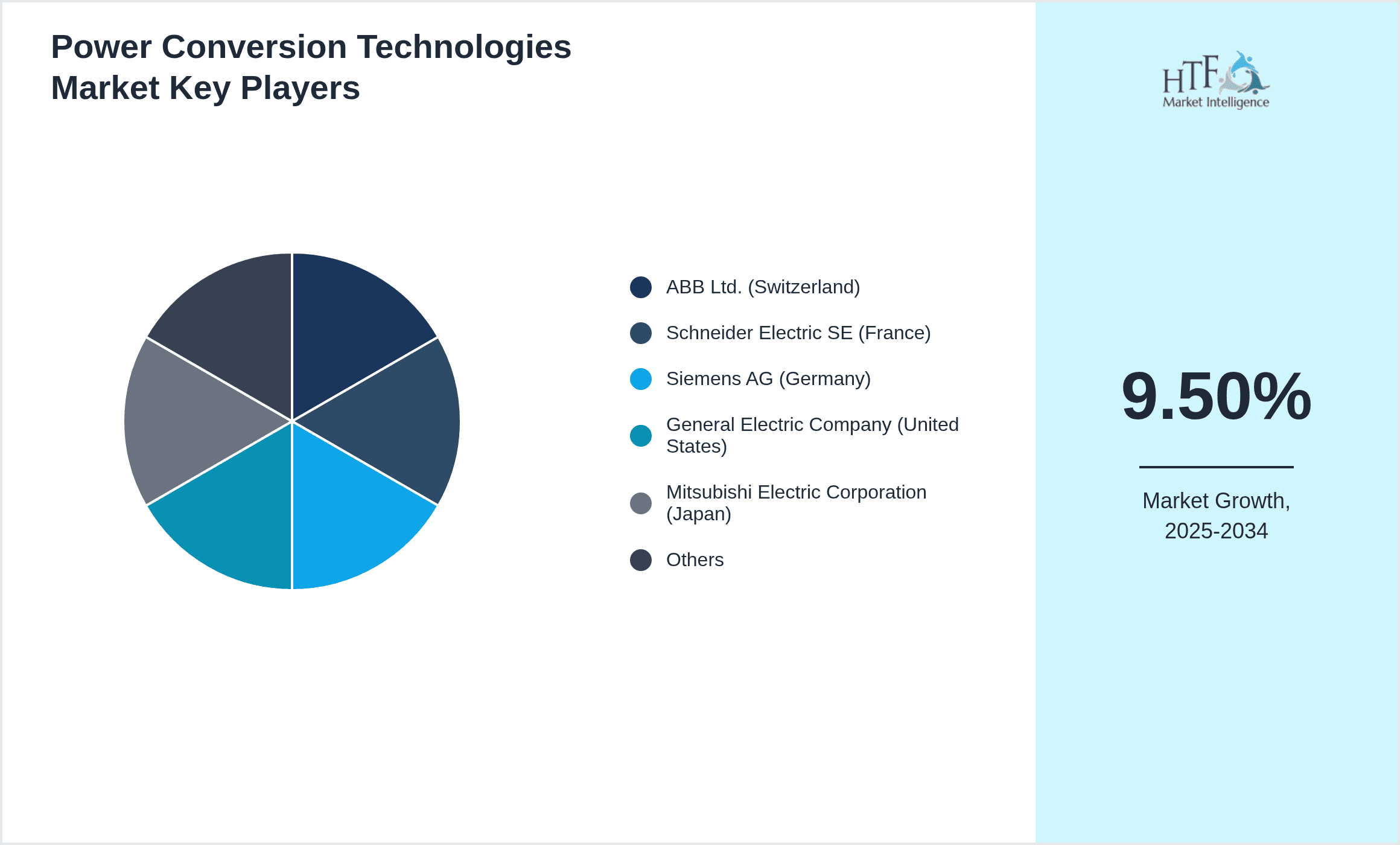

Leading Companies in Power Conversion Technologies Market

- •ABB Ltd. (Switzerland)

- •Schneider Electric SE (France)

- •Siemens AG (Germany)

- •General Electric Company (United States)

- •Mitsubishi Electric Corporation (Japan)

- •Infineon Technologies AG (Germany)

- •Texas Instruments Incorporated (United States)

- •Fuji Electric Co., Ltd. (Japan)

- •ON Semiconductor Corporation (United States)

- •Toshiba Corporation (Japan)

- •Delta Electronics, Inc. (Taiwan)

- •Cree, Inc. (United States)

- •Hitachi, Ltd. (Japan)

- •NXP Semiconductors N.V. (Netherlands)

- •STMicroelectronics N.V. (Switzerland)

- •Eaton Corporation plc (Ireland)

- •Power Integrations, Inc. (United States)

- •Vicor Corporation (United States)

- •ABB Power Grids AG (Switzerland)

- •Analog Devices, Inc. (United States)

- •Emerson Electric Co. (United States)

- •Nidec Corporation (Japan)

- •Rohm Semiconductor (Japan)

- •Panasonic Corporation (Japan)

- •Hitachi Energy Ltd. (Switzerland)

Market Breakdown

- •By Type

- ◦AC-DC Converters

- ◦DC-DC Converters

- ◦Inverters

- ◦Rectifiers

- ◦Others

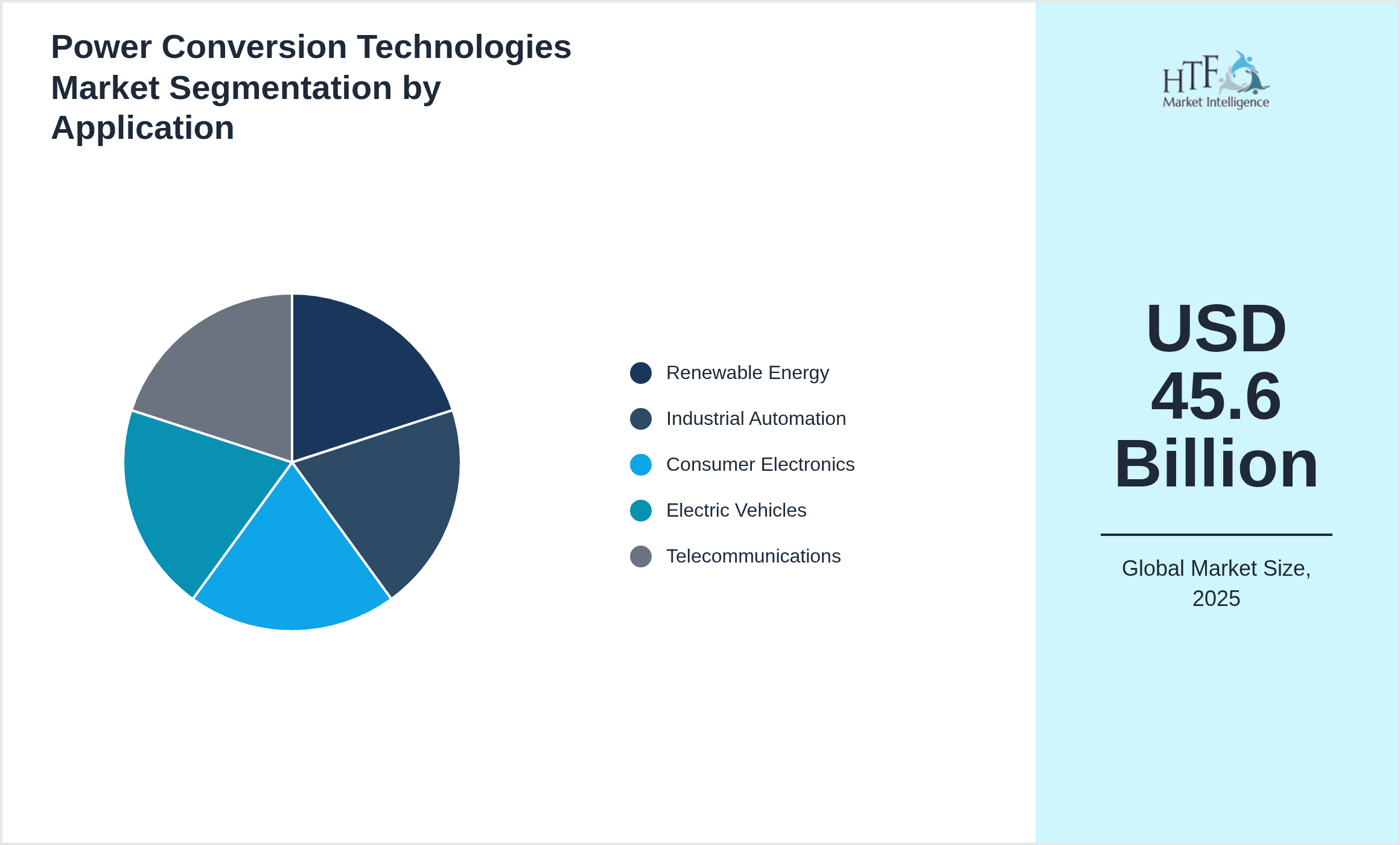

- •By Application

- ◦Renewable Energy

- ◦Industrial Automation

- ◦Consumer Electronics

- ◦Electric Vehicles

- ◦Telecommunications

- •By End User

- ◦Utilities

- ◦Manufacturing

- ◦Automotive

- ◦Residential

- ◦Commercial

- •By Technology

- ◦Silicon (Si)-based

- ◦Silicon Carbide (SiC)

- ◦Gallium Nitride (GaN)

- ◦Other Wide Bandgap Semiconductors

Growth Drivers

- •Rising global deployment of renewable energy systems such as solar and wind drives demand for efficient power conversion technologies to optimize energy harvesting and grid integration.

- •Accelerated adoption of electric vehicles worldwide increases the need for advanced inverters and converters to support battery management and charging infrastructure.

- •Technological advancements in wide bandgap semiconductors like SiC and GaN enable higher efficiency and thermal performance, fueling market expansion.

- •Stringent energy efficiency regulations across major economies compel industries to upgrade legacy power conversion systems, boosting market growth.

- •Digitalization and smart grid initiatives promote integration of intelligent power converters with real-time monitoring and control capabilities, enhancing demand.

Market Trends

- •Increasing integration of artificial intelligence and machine learning in power conversion devices for predictive maintenance and optimized performance.

- •Shift towards modular and compact converter designs to support space-constrained applications in electric vehicles and consumer electronics.

- •Growing preference for wide bandgap semiconductor-based converters due to superior efficiency and miniaturization benefits compared to traditional silicon-based solutions.

- •Expansion of power conversion technology applications in emerging sectors such as data centers and 5G infrastructure to meet high power quality standards.

- •Increasing collaboration between semiconductor manufacturers and system integrators to accelerate innovation and customized solutions.

Market Restraints

- •High initial capital expenditure for advanced power conversion systems limits adoption among small and medium enterprises, especially in developing regions.

- •Complexity in integrating new semiconductor materials with existing infrastructure poses technical challenges and slows market penetration.

- •Volatility in raw material prices, particularly for silicon carbide and gallium nitride, impacts manufacturing costs and pricing strategies.

- •Lack of standardization in power conversion technologies across different applications increases design and compatibility challenges.

- •Supply chain disruptions and component shortages affect timely delivery and scalability of power conversion products globally.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present significant growth potential due to rapid industrialization and infrastructure development.

- •Expansion of electric vehicle charging infrastructure offers new avenues for power conversion technology deployment and innovation.

- •Development of next-generation wide bandgap semiconductor devices enables entry into high-performance computing and aerospace sectors.

- •Increasing investments in smart grid and microgrid projects create demand for advanced power conversion solutions integrated with IoT and cloud platforms.

- •Collaborations between technology providers and end-users foster tailored solutions, enhancing customer retention and market share.

Market Challenges

- •Adapting to rapid technological changes requires continuous R&D investment, posing financial risks for smaller companies in the market.

- •Intense competition from low-cost manufacturers, particularly in Asia, pressures profit margins for established players in developed markets.

- •Ensuring cybersecurity and data integrity in smart power conversion systems remains a critical challenge amid increasing digitalization.

- •Navigating diverse regulatory landscapes across global regions complicates compliance and product certification processes.

- •Talent acquisition and retention in specialized semiconductor and power electronics domains limit innovation capacity for some companies.

Regulatory Framework

- •Between 2023 and 2024, major regions including North America and Europe introduced stricter energy efficiency standards for power conversion devices, mandating compliance with updated IEC and DOE regulations, thereby accelerating adoption of advanced technologies.

- •Environmental regulations focusing on reduction of hazardous substances in electronic components have impacted manufacturing processes, enforcing RoHS and REACH compliance across global markets.

- •Grid interconnection standards evolved to include requirements for inverter-based renewable systems, promoting grid stability and harmonization in Europe and Asia-Pacific regions.

- •Government incentives for renewable energy and electric vehicle sectors support deployment of compliant power conversion technologies, particularly in North America and Asia-Pacific.

- •Safety certification updates from UL and IEC have tightened testing protocols for converters and inverters, ensuring higher reliability and consumer protection.

Industry Insights

- •In March 2024, Schneider Electric launched a new line of high-efficiency inverters integrating silicon carbide technology aimed at enhancing renewable energy system performance globally. This innovation supports higher power density and reduced energy loss, positioning Schneider Electric as a pioneer in next-generation power conversion solutions with strong market appeal across utilities and industrial sectors.

- •In November 2023, Infineon Technologies unveiled a breakthrough GaN-based DC-DC converter platform designed for electric vehicle applications, offering improved thermal management and compact size. This advancement is expected to accelerate EV adoption by reducing charging times and improving battery efficiency, reinforcing Infineon's leadership in semiconductor innovation within the power electronics market.

Mergers & Acquisitions

- •In July 2024, ABB Ltd. completed the acquisition of a leading silicon carbide semiconductor manufacturer, enhancing its portfolio of power conversion components with advanced wide bandgap technologies. This strategic move enables ABB to strengthen its position in renewable energy and electric vehicle markets by offering more efficient and compact power electronic solutions, supporting long-term growth and innovation.

- •In February 2025, Texas Instruments Incorporated acquired a specialized inverter control software company to expand its capabilities in digital power management. This acquisition allows Texas Instruments to integrate advanced control algorithms with its hardware solutions, providing customers with improved energy efficiency and system intelligence across industrial automation and consumer electronics segments.

Recent Industry News

- •15th January 2025, General Electric Company announced a strategic partnership with a leading solar energy firm to co-develop advanced AC-DC converters optimized for large-scale photovoltaic installations. The collaboration aims to enhance energy conversion efficiency and grid stability, accelerating renewable energy adoption globally. This partnership leverages GE's extensive expertise in power systems and the partner’s solar technology innovations to address growing demand in emerging markets. Source: Official press release

- •10th March 2025, Mitsubishi Electric Corporation launched a new series of compact, high-efficiency inverters tailored for electric vehicle charging stations. These inverters incorporate silicon carbide technology to deliver reduced heat generation and higher power density, supporting faster charging and improved durability. The product rollout aligns with rising EV infrastructure investments worldwide, positioning Mitsubishi Electric as a key supplier in this sector. Source: Company website

- •22nd May 2025, Siemens AG expanded its manufacturing facility in Europe to increase production capacity of DC-DC converters used in industrial automation and telecommunications. The expansion reflects rising demand for reliable power conversion solutions that support Industry 4.0 initiatives and 5G network deployment. Siemens plans to integrate advanced automation and quality control technologies to ensure product excellence and supply chain resilience. Source: Industry publication

- •5th July 2025, ON Semiconductor Corporation announced the launch of a new wide bandgap semiconductor production line, significantly enhancing its ability to meet growing market needs for power conversion components in electric vehicles and renewable energy systems. This expansion is expected to reduce lead times and lower costs, strengthening ON Semiconductor’s competitive position and supporting global sustainability goals. Source: Official company announcement

Market Statistics

- •CAGR by 2034: 9.5%

- •Market Size by 2034: USD 112.5 Billion

- •Market Size in 2025: USD 50.1 Billion

- •Dominating Type: AC-DC Converters

- •Next-following Type: Inverters

- •Dominating Application: Renewable Energy

- •Next-following Application: Electric Vehicles

- •Dominating Region: North America

- •Second-leading Region: Europe

- •Region with Highest Growth Rate: Asia-Pacific

- •Dominating Country: United States

Market Share Table

- •Market Share (%) Comparison:

- ◦AC-DC Converters: 38%

- ◦Inverters: 28%

- •Market Share (%) by Application:

- ◦Renewable Energy: 34%

- ◦Electric Vehicles: 26%

- •Growth Rate (%) by Type:

- ◦AC-DC Converters: 8.7%

- ◦Inverters: 11.2%

- •Growth Rate (%) by Application:

- ◦Renewable Energy: 9.0%

- ◦Electric Vehicles: 12.5%

Top 5 Global Players

- •ABB Ltd. (Switzerland)

- •Schneider Electric SE (France)

- •Siemens AG (Germany)

- •General Electric Company (United States)

- •Mitsubishi Electric Corporation (Japan)

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.6 Billion |

| Forecast Year Market Size | USD 112.5 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | ABB Ltd. (Switzerland), Schneider Electric SE (France), Siemens AG (Germany), General Electric Company (United States), Mitsubishi Electric Corporation (Japan), Infineon Technologies AG (Germany), Texas Instruments Incorporated (United States), Fuji Electric Co., Ltd. (Japan), ON Semiconductor Corporation (United States), Toshiba Corporation (Japan), Delta Electronics, Inc. (Taiwan), Cree, Inc. (United States), Hitachi, Ltd. (Japan), NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland), Eaton Corporation plc (Ireland), Power Integrations, Inc. (United States), Vicor Corporation (United States), ABB Power Grids AG (Switzerland), Analog Devices, Inc. (United States), Emerson Electric Co. (United States), Nidec Corporation (Japan), Rohm Semiconductor (Japan), Panasonic Corporation (Japan), Hitachi Energy Ltd. (Switzerland) |

Global Power Conversion Technologies Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.