South America Fuel Trucks Market Size, Growth & Revenue 2024-2034

South America Fuel Trucks Market is segmented by Type (Tanker Trucks, Vacuum Fuel Trucks, Fuel Bowser Trucks, Fuel Tank Trailers, Refueling Trucks), Application (Petroleum Transportation, Aviation Fuel Supply, Marine Fueling, Industrial Fuel Delivery, Retail Fuel Distribution), and Geography (Brazil, Argentina, Chile, Peru, Colombia, Rest of South America)

Pricing

Report Overview

Executive Summary

- •The South America Fuel Trucks market comprises vehicles tailored to transport and deliver fuel products safely and efficiently. It includes tanker trucks, vacuum fuel trucks, fuel bowser trucks, fuel tank trailers, and refueling trucks serving applications like petroleum transport, aviation fueling, marine fuel delivery, and industrial fuel distribution. This market plays a pivotal role in supporting energy infrastructure across countries such as Brazil, Argentina, Chile, Peru, and Colombia, addressing the region's growing energy demands and logistics challenges.

- •Key market highlights include a projected CAGR of 9.5% from 2024 to 2034, driven by increasing fuel consumption, infrastructural expansion, and technological innovation in fuel truck design. Brazil dominates the market with 40% share, while Argentina exhibits the highest growth rate of 12.3%. Tanker trucks lead product types, followed by fuel bowser trucks as the fastest-growing segment.

- •The market presents significant value propositions by enhancing fuel transportation safety and efficiency, critical for industries like oil & gas, aviation, and marine. Stakeholders benefit from improvements in vehicle technology, regulatory compliance, and expanding fuel distribution networks, underscoring the strategic importance of fuel trucks within South America’s energy logistics landscape.

Competitive Landscape

The South America Fuel Trucks market exhibits high competitive intensity marked by the presence of both global manufacturers and regional specialists. Market players differentiate through innovation in truck design focused on fuel safety, capacity, and environmental compliance. Strategic partnerships and localized manufacturing enhance regional adaptability and cost efficiency. Competition also centers on expanding service networks and after-sales support to cater to diverse geographic and industrial demands. The rivalry drives continuous product enhancements and technology adoption such as telematics and emission control systems. Barriers to entry include stringent regulatory standards and capital-intensive manufacturing processes, which favor established players. Future competition is expected to intensify with increasing demand for eco-friendly and technologically advanced fuel trucks.

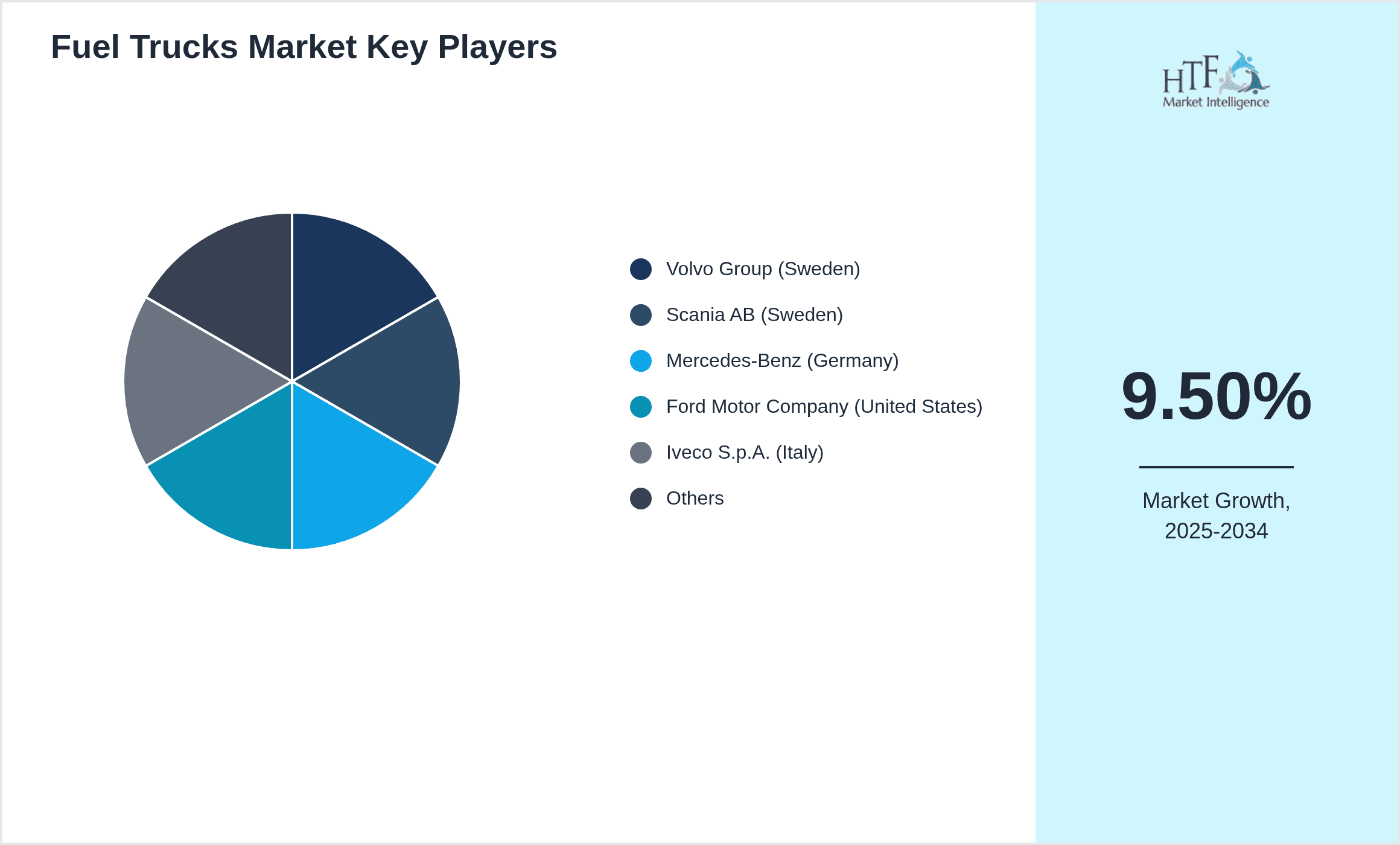

Leading Companies in South America Fuel Trucks Market

- •Volvo Group (Sweden)

- •Scania AB (Sweden)

- •Mercedes-Benz (Germany)

- •Ford Motor Company (United States)

- •Iveco S.p.A. (Italy)

- •TATA Motors (India)

- •Freightliner Trucks (United States)

- •Hino Motors (Japan)

- •Dongfeng Motor Corporation (China)

- •Foton Motor (China)

- •MAN Truck & Bus (Germany)

- •Kenworth Truck Company (United States)

- •Mack Trucks (United States)

- •Peterbilt Motors Company (United States)

- •Navistar International (United States)

- •Ashok Leyland (India)

- •Sinotruk (China)

- •Isuzu Motors (Japan)

- •PACCAR Inc. (United States)

- •Triton Group (Brazil)

- •Randon S.A. (Brazil)

- •Agrale (Brazil)

- •Marcopolo S.A. (Brazil)

- •CAIO Induscar (Brazil)

- •CNH Industrial (United Kingdom/Netherlands)

Market Breakdown

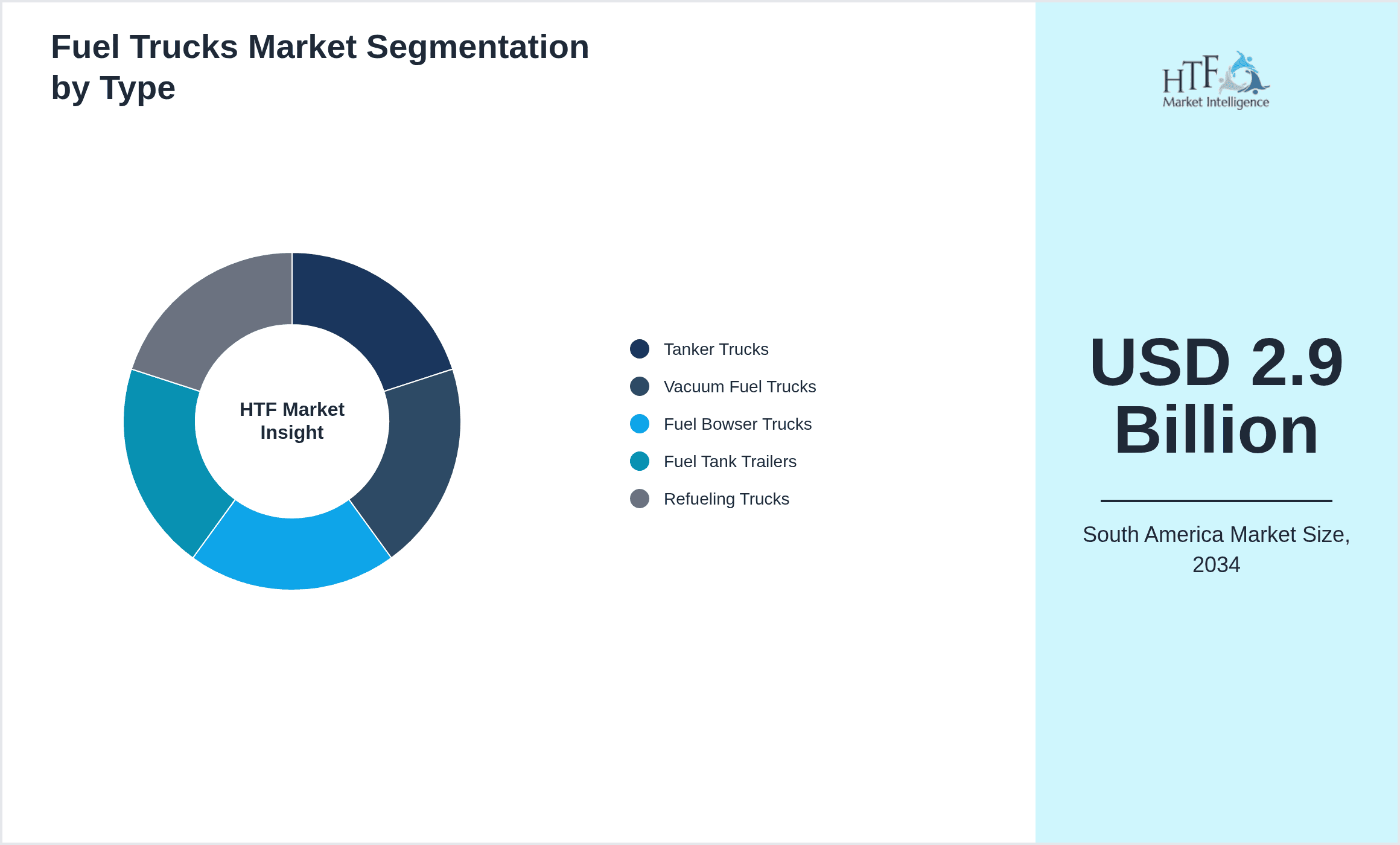

- •By Type

- ◦Tanker Trucks

- ◦Vacuum Fuel Trucks

- ◦Fuel Bowser Trucks

- ◦Fuel Tank Trailers

- ◦Refueling Trucks

- •By Application

- ◦Petroleum Transportation

- ◦Aviation Fuel Supply

- ◦Marine Fueling

- ◦Industrial Fuel Delivery

- ◦Retail Fuel Distribution

- •By End User

- ◦Oil & Gas Companies

- ◦Airports and Airlines

- ◦Shipping Ports

- ◦Manufacturing Industries

- ◦Fuel Retailers

- •By Distribution Channel

- ◦Direct Sales

- ◦Dealerships

- ◦Fleet Leasing

- ◦Online Platforms

Growth Dynamics

- •Increasing fuel demand driven by expanding industrial activities and transportation needs across South America fuels market growth. Infrastructure investments in oil & gas and aviation sectors necessitate advanced fuel trucks to ensure efficient fuel delivery. Government initiatives promoting energy distribution safety and environmental compliance further stimulate adoption of technologically advanced fuel trucks. Additionally, urbanization and economic growth in Brazil and Argentina create rising demand for reliable fuel transportation, boosting market expansion.

- •The growing emphasis on vehicle telematics and emission control technologies enhances operational efficiency and regulatory compliance. Manufacturers innovate with fuel-efficient engines and eco-friendly materials, attracting environmentally conscious buyers. Expansion of fuel retail networks and increasing fleet modernization programs contribute to sustained demand. These factors collectively underpin the upward trajectory of the South America Fuel Trucks market over the forecast period.

- •Increasing trade activities within South American countries and with global partners lead to higher fuel transportation volumes. Integration of digital platforms for fleet management optimizes route planning and fuel usage, reducing operational costs. Strategic partnerships between truck manufacturers and fuel companies support customized solutions catering to diverse applications including aviation and marine fueling, broadening the market scope.

- •The growing replacement cycle of aging fuel trucks with modern, compliant vehicles presents significant growth opportunities. Furthermore, rising demand for specialized trucks capable of handling various fuel types, including biofuels and aviation fuel, drives product diversification. These dynamics, combined with rising investments in renewable fuel infrastructure, positively impact market growth.

- •The COVID-19 pandemic initially disrupted supply chains and delayed new vehicle purchases; however, recovery in industrial and transportation sectors has accelerated demand. Increased focus on fuel delivery reliability to support economic rebound highlights the strategic importance of fuel trucks, reinforcing market growth drivers in the medium to long term.

Market Trends

- •Adoption of green technologies such as electric and hybrid fuel trucks is gaining traction to meet stringent emission regulations and sustainability goals. Leading manufacturers are investing in R&D for alternative fuel vehicles tailored to South American infrastructure realities. This trend reflects a broader shift towards environmentally responsible fuel transportation solutions.

- •Increased integration of telematics and IoT-enabled fleet management systems enhances real-time monitoring, predictive maintenance, and route optimization. These digital innovations improve operational transparency and reduce downtime, offering competitive advantages to fleet operators.

- •Customization of fuel trucks to accommodate diverse fuel types including diesel, gasoline, biofuels, and aviation fuel aligns with expanding energy portfolios in South America. Manufacturers collaborate closely with end-users to develop specialized vehicles that address specific application needs.

- •Rising demand for modular and multi-compartment fuel trucks facilitates simultaneous transportation of different fuel grades, improving delivery efficiency and reducing costs. This innovation is particularly relevant for retail fuel distribution networks expanding in remote and urban regions.

- •Strategic alliances between truck manufacturers and logistics providers are shaping ecosystem development, enabling comprehensive fuel delivery solutions that integrate vehicle supply, maintenance, and fleet management services.

Market Opportunities

- •Expanding infrastructure development projects across Brazil, Argentina, and Chile create robust demand for fuel trucks capable of supporting large-scale petroleum and industrial fuel transportation, presenting lucrative growth avenues for manufacturers and service providers.

- •Emerging fuel types such as biodiesel and ethanol in South America open opportunities for specialized fuel trucks designed to handle alternative fuels, tapping into evolving energy consumption patterns and environmental regulations.

- •Technological innovations including electric fuel trucks and advanced telematics systems offer investment potential for companies focusing on sustainability and operational efficiency, aligning with global trends and regional regulatory frameworks.

- •Increasing demand for fleet modernization and replacement in South America drives opportunities for aftermarket services, including maintenance, refurbishment, and retrofitting of fuel trucks with latest safety and emission technologies.

- •Cross-border trade and regional integration initiatives in South America enhance fuel distribution networks, creating demand for versatile fuel trucks capable of efficient logistics across diverse terrains and regulatory environments.

Market Challenges

- •High capital expenditure and operational costs associated with advanced fuel trucks limit adoption among small and medium-sized enterprises, constraining market penetration in certain South American segments.

- •Stringent and varying regulatory standards across South American countries create compliance complexities for manufacturers and operators, impacting production timelines and cost structures.

- •Limited infrastructure in remote and rural areas poses logistical challenges for fuel truck operations, affecting delivery efficiency and increasing maintenance requirements due to difficult terrain.

- •Volatility in fuel prices and economic uncertainties in the region influence investment decisions in fleet expansion and modernization, causing market fluctuations and planning difficulties.

- •Shortage of skilled drivers and maintenance personnel trained for specialized fuel trucks hinders operational efficiency and safety compliance, necessitating investment in workforce development.

Regulatory Framework

- •Between 2020 and 2024, South American countries have implemented stricter vehicle emission standards aligned with global environmental commitments, compelling fuel truck manufacturers to adopt cleaner technologies and emission control systems.

- •Mandatory compliance with fuel transportation safety regulations, including tank design, spill prevention, and emergency response protocols, has been reinforced across Brazil, Argentina, and Chile, affecting manufacturing and operational practices.

- •Introduction of periodic vehicle inspection and certification schemes ensures ongoing adherence to safety and environmental norms, impacting fleet maintenance cycles and operational costs.

- •Government incentives promoting adoption of eco-friendly vehicles, including tax rebates and subsidies for electric and hybrid fuel trucks, have been introduced in select South American countries to encourage sustainable transport solutions.

- •Cross-border transport regulations under regional trade agreements harmonize safety and operational standards for fuel trucks, facilitating smoother logistics and market integration within South America.

Market Intelligence

- •In March 2023, Volvo Group launched a new line of fuel-efficient tanker trucks in Brazil featuring advanced telematics and emission reduction technologies aimed at meeting the latest regulatory standards and improving operational efficiency for South American fuel distributors. This product introduction marks a significant step toward greener fuel transportation solutions in the region. Source: Volvo Group Official Press Release.

- •In October 2024, Randon S.A., a Brazilian manufacturer, announced a strategic partnership with a leading logistics company to develop customized fuel bowser trucks designed specifically for marine and aviation fueling applications in Argentina and Chile. This collaboration aims to expand market reach and offer tailored solutions addressing regional operational challenges. Source: Randon S.A. Corporate Announcement.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •In June 2023, CNH Industrial completed the acquisition of a Brazilian fuel truck manufacturing startup specializing in electric and hybrid refueling vehicles. This acquisition strengthens CNH Industrial’s portfolio in sustainable fuel transportation and enhances its technological capabilities to meet evolving South American market demands. The deal is expected to accelerate innovation and expand CNH’s footprint in the region’s growing green logistics segment.

- •In September 2024, Volvo Group acquired a majority stake in a Chilean logistics company providing specialized fuel delivery services across South America. This strategic move aims to integrate Volvo’s advanced fuel truck technologies with established regional logistics networks, enhancing service quality and operational efficiency while consolidating market position across key South American countries.

Recent Industry News

- •On 15th January 2022, Mercedes-Benz introduced its latest range of fuel tank trailers equipped with advanced safety features and optimized fuel capacity targeting the South American petroleum transportation sector. These trailers are designed to improve fuel delivery efficiency and comply with emerging regional safety regulations. Source: Mercedes-Benz Official Website.

- •On 10th August 2023, TATA Motors expanded its South American operations by opening a new assembly plant in Argentina focused on producing fuel bowser trucks tailored to regional market specifications, aiming to meet rising demand driven by infrastructure growth. Source: TATA Motors Corporate News.

- •On 20th November 2024, Freightliner Trucks announced the launch of a telematics-enabled refueling truck model in Brazil, integrating real-time fuel monitoring and route optimization to enhance logistics efficiency for aviation and marine fuel supply chains. Source: Freightliner Trucks Press Release.

- •On 5th May 2023, Iveco S.p.A. formed a strategic alliance with a leading South American fuel retailer to co-develop customized tanker trucks with modular compartments designed for multi-fuel transport, improving delivery flexibility and reducing operational costs. Source: Iveco Company Announcement.

Market Statistics

- •CAGR by 2034: 9.5%

- •Market Size by 2034: USD 2.9 Billion

- •Market Size in 2025: USD 1.35 Billion

- •Dominating Type: Tanker Trucks

- •Next-Following Type: Fuel Bowser Trucks

- •Dominating Application: Petroleum Transportation

- •Next-Following Application: Aviation Fuel Supply

- •Dominating Region: Brazil

- •Second-Leading Region: Argentina

- •Region with Highest Growth Rate: Argentina

- •Dominating Country: Brazil

Market Share Table

- •Market Share (%) by Type: Tanker Trucks 55%, Fuel Bowser Trucks 25%

- •Market Share (%) by Application: Petroleum Transportation 60%, Aviation Fuel Supply 20%

- •Growth Rate (%) by Type: Tanker Trucks 8.7%, Fuel Bowser Trucks 11.5%

- •Growth Rate (%) by Application: Petroleum Transportation 9.0%, Aviation Fuel Supply 10.2%

Top Companies Profiled in South America Fuel Trucks Market

- •Volvo Group (Sweden)

- •Scania AB (Sweden)

- •Mercedes-Benz (Germany)

- •Ford Motor Company (United States)

- •Iveco S.p.A. (Italy)

Regional Outlook

The Brazil currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Argentina is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Brazil

- Argentina

- Chile

- Peru

- Colombia

- Rest of South America

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 2.9 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Regions Covered | Brazil, Argentina, Chile, Peru, Colombia, Rest of South America |

| Key Companies | Volvo Group (Sweden), Scania AB (Sweden), Mercedes-Benz (Germany), Ford Motor Company (United States), Iveco S.p.A. (Italy), TATA Motors (India), Freightliner Trucks (United States), Hino Motors (Japan), Dongfeng Motor Corporation (China), Foton Motor (China), MAN Truck & Bus (Germany), Kenworth Truck Company (United States), Mack Trucks (United States), Peterbilt Motors Company (United States), Navistar International (United States), Ashok Leyland (India), Sinotruk (China), Isuzu Motors (Japan), PACCAR Inc. (United States), Triton Group (Brazil), Randon S.A. (Brazil), Agrale (Brazil), Marcopolo S.A. (Brazil), CAIO Induscar (Brazil), CNH Industrial (United Kingdom/Netherlands) |

South America Fuel Trucks Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.