Europe 2G, 3G, 4G and 5G Wireless Network Infrastructure Market Scope & Changing Dynamics 2024-2034

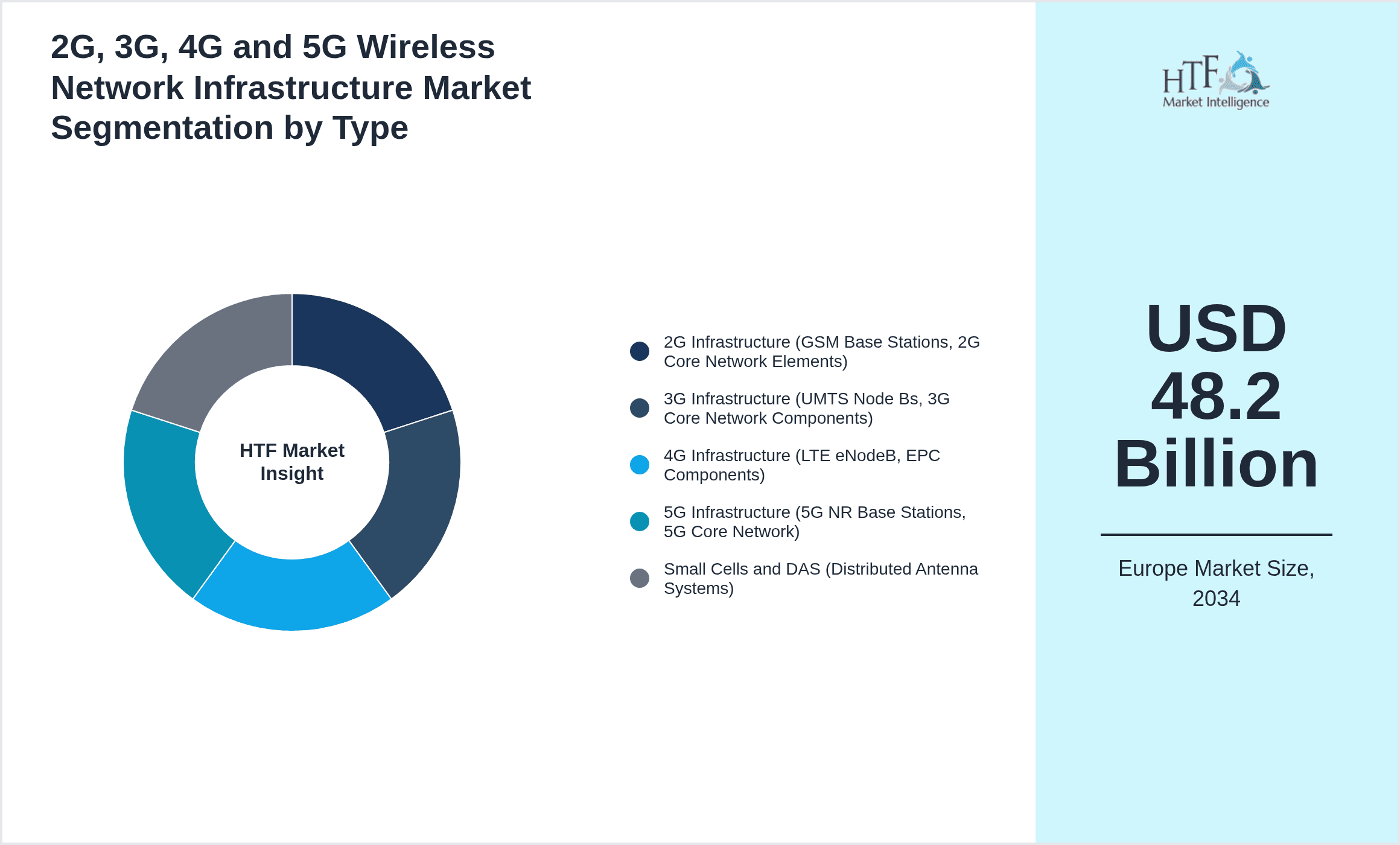

Europe 2G, 3G, 4G and 5G Wireless Network Infrastructure Market is segmented by Type (2G Infrastructure (GSM Base Stations, 2G Core Network Elements), 3G Infrastructure (UMTS Node Bs, 3G Core Network Components), 4G Infrastructure (LTE eNodeB, EPC Components), 5G Infrastructure (5G NR Base Stations, 5G Core Network), Small Cells and DAS (Distributed Antenna Systems)), Application (Mobile Broadband, Fixed Wireless Access, IoT Connectivity, Enterprise Networks, Public Safety Communications), End User (Telecom Operators, Government and Public Sector, Enterprises, Industrial and Manufacturing, Healthcare), Technology (Macro Cell Networks, Small Cell Networks, Cloud RAN, Network Slicing), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe 2G, 3G, 4G and 5G Wireless Network Infrastructure market includes the deployment and management of wireless communication technologies across European countries. It covers legacy 2G and 3G networks supporting voice and low-speed data, as well as advanced 4G LTE and 5G infrastructures facilitating high-speed internet, IoT, and enterprise connectivity. This market is critical for enabling mobile broadband, fixed wireless access, IoT applications, and public safety communications across diverse sectors.

- •Key market highlights include a base market size of USD 18.5 Billion in 2024, with forecasted growth to USD 48.2 Billion by 2034 at a CAGR of 10.5%. 5G infrastructure leads the market, driven by increasing data traffic, government initiatives, and technological advancements. Germany dominates the regional market with 23% share, while France is the fastest-growing country at a 12.3% CAGR.

- •This market holds strategic importance for telecommunications operators, equipment manufacturers, and end-users by enabling enhanced connectivity, supporting digital transformation, and fostering innovation in IoT and smart city initiatives within Europe.

Competitive Landscape

The Europe wireless network infrastructure market is highly competitive, dominated by established global players and innovative regional companies. Competition revolves around technological innovation, extensive R&D investments, and strategic partnerships to expand network coverage and capacity. Companies focus on differentiating through advanced 5G solutions, energy-efficient equipment, and integrated software platforms. Market rivalry intensifies with new entrants and increasing demand for network modernization. Strategic alliances and mergers are common to gain market share and address evolving customer needs. Pricing strategies and service quality are key competitive levers. Regional nuances influence market positioning, with companies tailoring offerings to country-specific regulatory and technological landscapes. Overall, the competitive environment drives continuous improvement in infrastructure capabilities, fostering rapid adoption of 5G and preparation for future wireless technologies.

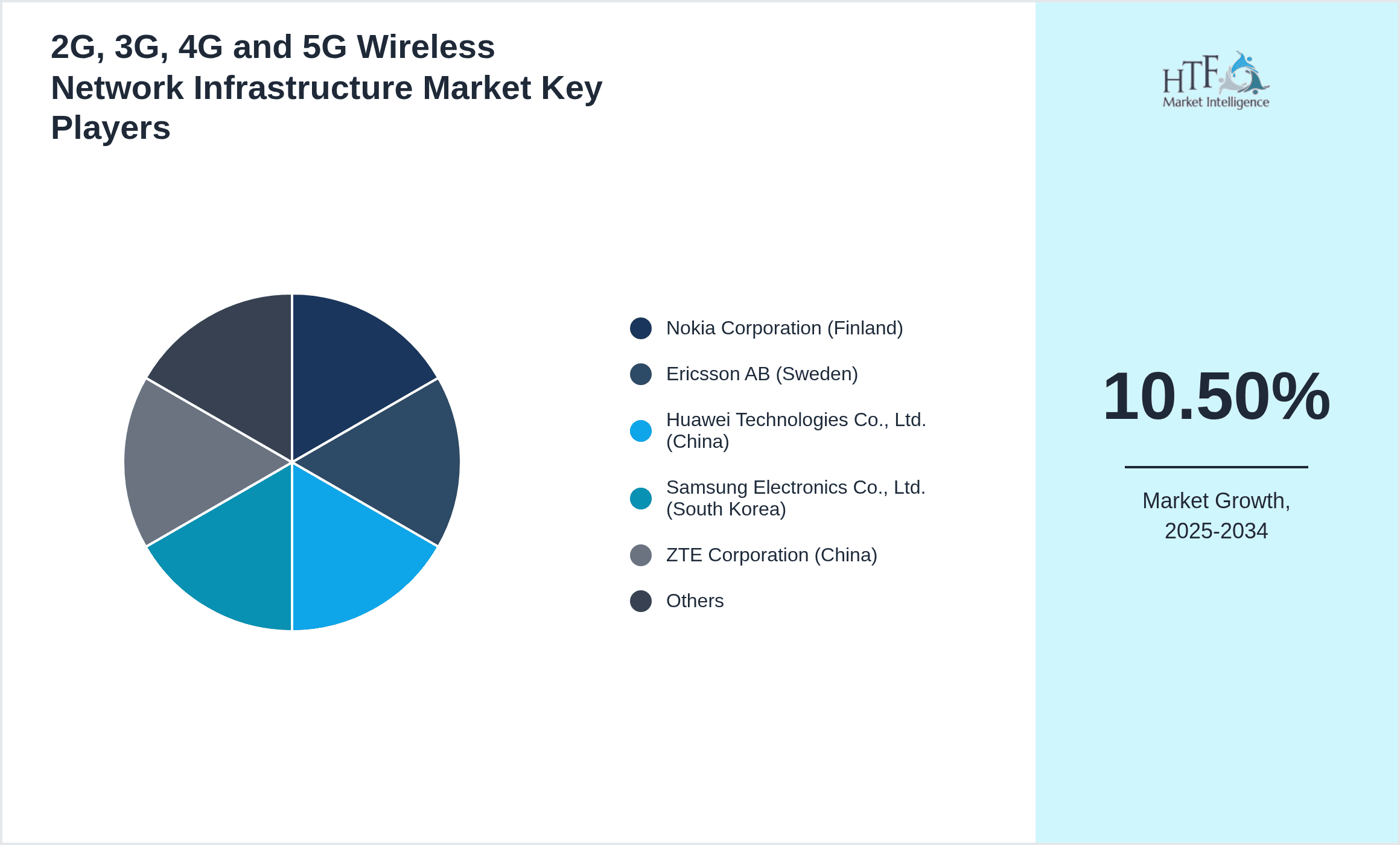

Leading Companies in Europe 2G, 3G, 4G and 5G Wireless Network Infrastructure Market

- •Nokia Corporation (Finland)

- •Ericsson AB (Sweden)

- •Huawei Technologies Co., Ltd. (China)

- •Samsung Electronics Co., Ltd. (South Korea)

- •ZTE Corporation (China)

- •NEC Corporation (Japan)

- •Cisco Systems, Inc. (United States)

- •Fujitsu Limited (Japan)

- •Alcatel-Lucent (France)

- •CommScope Holding Company, Inc. (United States)

- •Juniper Networks, Inc. (United States)

- •Infinera Corporation (United States)

- •Mavenir Systems, Inc. (United States)

- •Telefonaktiebolaget LM Ericsson (Sweden)

- •Ciena Corporation (United States)

- •Juniper Networks, Inc. (United States)

- •Samsung Networks Europe (United Kingdom)

- •Ericsson AB (Germany)

- •Nokia Solutions and Networks GmbH & Co. KG (Germany)

- •ZTE Europe GmbH (Germany)

- •NEC Europe Ltd. (United Kingdom)

- •Cisco Systems Europe (Germany)

- •Fujitsu Europe Ltd. (United Kingdom)

- •CommScope Europe GmbH (Germany)

- •Mavenir Europe Ltd. (United Kingdom)

Market Breakdown

- •By Type

- ◦2G Infrastructure (GSM Base Stations, 2G Core Network Elements)

- ◦3G Infrastructure (UMTS Node Bs, 3G Core Network Components)

- ◦4G Infrastructure (LTE eNodeB, EPC Components)

- ◦5G Infrastructure (5G NR Base Stations, 5G Core Network)

- ◦Small Cells and DAS (Distributed Antenna Systems)

- •By Application

- ◦Mobile Broadband

- ◦Fixed Wireless Access

- ◦IoT Connectivity

- ◦Enterprise Networks

- ◦Public Safety Communications

- •By End User

- ◦Telecom Operators

- ◦Government and Public Sector

- ◦Enterprises

- ◦Industrial and Manufacturing

- ◦Healthcare

- •By Technology

- ◦Macro Cell Networks

- ◦Small Cell Networks

- ◦Cloud RAN

- ◦Network Slicing

Growth Drivers

The Europe wireless network infrastructure market is propelled by growing demand for high-speed mobile broadband and data-intensive applications, accelerating deployment of 5G networks across major economies. Government initiatives promoting digital transformation and spectrum allocation facilitate infrastructure expansion. Increasing adoption of IoT devices in industries such as manufacturing, healthcare, and automotive drives infrastructure investments. Telecom operators are upgrading legacy 2G and 3G networks to support advanced 4G and 5G services, improving coverage and capacity. The push for smart cities and connected devices further fuels demand, supported by technological advancements in small cells and cloud RAN architectures. Together, these factors stimulate robust market growth and innovation in wireless network infrastructure throughout Europe.

Market Trends

Europe’s wireless network infrastructure market witnesses rapid adoption of 5G standalone (SA) architectures enabling ultra-low latency and network slicing capabilities tailored for enterprise and industrial applications. Operators increasingly integrate cloud-native solutions and virtualization technologies to enhance network flexibility and reduce operational costs. Edge computing deployments adjacent to wireless infrastructure grow to support real-time data processing, enhancing IoT use cases. Sustainability trends prompt equipment manufacturers to develop energy-efficient hardware. Collaborative partnerships among telecom providers and technology firms accelerate innovation and market penetration. Additionally, the gradual phase-out of 2G and 3G networks leads to spectrum re-farming for newer technologies, optimizing resource utilization region-wide.

Market Restraints

The Europe wireless network infrastructure market faces challenges due to high capital expenditure required for 5G deployment and network upgrades, impacting smaller operators’ ability to invest. Regulatory complexities and lengthy approval processes for site acquisition and spectrum licensing can delay infrastructure rollout. Security concerns, including cyber threats targeting new network architectures, necessitate costly protective measures. Legacy 2G and 3G infrastructure phase-out risks service interruptions for certain user segments, complicating transition strategies. Additionally, supply chain disruptions and component shortages can hamper timely equipment delivery, while economic uncertainties may constrain investment budgets, collectively restraining market growth momentum.

Market Opportunities

Emerging opportunities in Europe’s wireless infrastructure market include expansion of private 5G networks tailored for industrial automation, logistics, and healthcare sectors, enabling customized connectivity solutions. Integration of AI and machine learning for network optimization offers potential for enhanced performance and predictive maintenance services. The rise of Fixed Wireless Access (FWA) solutions presents a viable alternative to traditional wired broadband in underserved areas, expanding market reach. Cross-border collaborations and harmonized spectrum policies can accelerate deployment and interoperability. Additionally, increasing demand for green infrastructure encourages investments in sustainable technologies, opening avenues for eco-friendly product innovation and government support programs.

Market Challenges

Key challenges in the Europe wireless network infrastructure market include managing the complex coexistence of multiple generations of wireless technologies, requiring interoperable and backward-compatible solutions. High competition among vendors intensifies pricing pressures, squeezing margins. Rapid technological evolution demands continuous R&D investments to stay competitive. Ensuring consistent quality of service across diverse geographies with varying infrastructure maturity levels is difficult. Regulatory heterogeneity across European countries complicates unified deployment strategies. Furthermore, addressing cybersecurity risks in increasingly virtualized and software-defined networks poses ongoing challenges. These factors collectively require strategic planning and agile execution from market participants.

Regulatory Framework

Between 2020 and 2024, the European Union and national regulatory bodies have advanced spectrum allocation policies supporting 5G deployment, including harmonized mid-band and mmWave frequencies. GDPR enforcement continues influencing data privacy and network security requirements for wireless infrastructure providers. The EU’s Digital Decade strategy outlines targets for gigabit connectivity and 5G coverage by 2030, driving regulatory support and funding. Network security directives mandate stringent cybersecurity measures for telecommunications operators. Additionally, environmental regulations increasingly require adoption of energy efficiency standards and reduction of electromagnetic emissions, shaping equipment manufacturing and deployment practices across Europe.

Industry Insights

In March 2023, Nokia announced the launch of its latest AirScale 5G radio platform in Europe, designed to deliver enhanced network capacity and energy efficiency for operators upgrading to standalone 5G networks. This product integrates advanced Massive MIMO technology and cloud-native software, enabling flexible deployments for urban and rural environments. In July 2024, Ericsson expanded its European footprint through a strategic partnership with a leading telecom operator to accelerate 5G coverage in underserved regions, leveraging edge computing and AI-driven network management solutions. These developments underscore the dynamic innovation landscape and growing investments in next-generation wireless infrastructure across Europe.

Mergers & Acquisitions

- •In September 2023, Ericsson completed the acquisition of a European private network specialist firm to bolster its 5G enterprise solutions portfolio. The deal enhances Ericsson’s capabilities in delivering customized private 5G deployments for industrial clients, expanding its addressable market in Europe. This strategic acquisition aligns with growing demand for dedicated wireless networks supporting manufacturing automation and logistics, strengthening Ericsson’s competitive positioning in the region.

- •In June 2022, Nokia acquired a Germany-based cloud RAN technology startup, aiming to accelerate its development of virtualized and cloud-native 5G infrastructure products. This acquisition supports Nokia’s strategy to offer flexible, scalable wireless network solutions that reduce operational costs and enable rapid service innovation. The integration of cloud RAN capabilities is expected to improve Nokia’s market share in Europe’s evolving telecom infrastructure landscape.

Recent Industry News

- •15th January 2024, Ericsson announced a partnership with Deutsche Telekom to deploy a nationwide standalone 5G network in Germany, focusing on industrial IoT applications and smart city initiatives. The collaboration aims to integrate edge computing and AI-driven network analytics to optimize performance and reliability. This partnership represents a significant milestone in expanding advanced wireless infrastructure capabilities across Europe. Source: Ericsson Official Press Release.

- •22nd November 2023, Nokia unveiled its new energy-efficient 5G base station equipment in Europe, designed to reduce carbon footprint by 30% compared to previous models. The product launch supports EU sustainability targets and offers telecom operators cost savings through lower power consumption. Early trials in France and Italy demonstrated improved network capacity and reduced operational expenses, positioning Nokia as a leader in green telecom infrastructure. Source: Nokia Corporate Website.

- •10th August 2022, Samsung Electronics expanded its European R&D center focusing on 6G and advanced wireless technologies, investing USD 200 million to accelerate innovation. The expansion enhances collaboration with European universities and telecom operators, aiming to solidify Samsung’s competitive edge in upcoming network generations. This move reflects the growing importance of Europe as a hub for telecom technology development and future network infrastructure. Source: Samsung Newsroom.

- •5th April 2021, ZTE Corporation partnered with Vodafone Europe to upgrade existing 4G networks and accelerate 5G deployments across multiple countries. The deal includes supply of radio access network equipment and joint innovation in network slicing technologies. This collaboration strengthens ZTE’s presence in Europe’s competitive wireless infrastructure market and supports Vodafone’s digital transformation goals. Source: Vodafone Corporate Announcements.

Market Statistics

- •CAGR by 2034: 10.5%

- •Market Size by 2034: USD 48.2 Billion

- •Market Size in 2025: USD 20.5 Billion

- •Dominating Type: 5G Infrastructure; Next-Following Type: 4G Infrastructure

- •Dominating Application: Mobile Broadband; Next-Following Application: IoT Connectivity

- •Dominating Region: Germany; Second-Leading Region: United Kingdom

- •Region with Highest Growth Rate: France

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: 5G Infrastructure (45%) vs 4G Infrastructure (30%)

- •Market Share (%) of Dominating vs Followed Application: Mobile Broadband (40%) vs IoT Connectivity (25%)

- •Growth Rate (%) of Dominating vs Followed Type: 5G Infrastructure (12.8%) vs 4G Infrastructure (7.2%)

- •Growth Rate (%) of Dominating vs Followed Application: Mobile Broadband (11.5%) vs IoT Connectivity (9.3%)

Top Companies Profiled in Europe 2G, 3G, 4G and 5G Wireless Network Infrastructure Market

- •Nokia Corporation (Finland)

- •Ericsson AB (Sweden)

- •Huawei Technologies Co., Ltd. (China)

- •Samsung Electronics Co., Ltd. (South Korea)

- •ZTE Corporation (China)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 18.5 Billion |

| Forecast Year Market Size | USD 48.2 Billion |

| CAGR | 10.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10% |

| Scope of Report | Market is segmented by Type (2G Infrastructure (GSM Base Stations, 2G Core Network Elements), 3G Infrastructure (UMTS Node Bs, 3G Core Network Components), 4G Infrastructure (LTE eNodeB, EPC Components), 5G Infrastructure (5G NR Base Stations, 5G Core Network), Small Cells and DAS (Distributed Antenna Systems)), Application (Mobile Broadband, Fixed Wireless Access, IoT Connectivity, Enterprise Networks, Public Safety Communications), End User (Telecom Operators, Government and Public Sector, Enterprises, Industrial and Manufacturing, Healthcare), Technology (Macro Cell Networks, Small Cell Networks, Cloud RAN, Network Slicing) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Nokia Corporation (Finland), Ericsson AB (Sweden), Huawei Technologies Co., Ltd. (China), Samsung Electronics Co., Ltd. (South Korea), ZTE Corporation (China), NEC Corporation (Japan), Cisco Systems, Inc. (United States), Fujitsu Limited (Japan), Alcatel-Lucent (France), CommScope Holding Company, Inc. (United States), Juniper Networks, Inc. (United States), Infinera Corporation (United States), Mavenir Systems, Inc. (United States), Telefonaktiebolaget LM Ericsson (Sweden), Ciena Corporation (United States), Juniper Networks, Inc. (United States), Samsung Networks Europe (United Kingdom), Ericsson AB (Germany), Nokia Solutions and Networks GmbH & Co. KG (Germany), ZTE Europe GmbH (Germany), NEC Europe Ltd. (United Kingdom), Cisco Systems Europe (Germany), Fujitsu Europe Ltd. (United Kingdom), CommScope Europe GmbH (Germany), Mavenir Europe Ltd. (United Kingdom) |

Europe 2G, 3G, 4G and 5G Wireless Network Infrastructure Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.