EMEA Leather Goods Market Size, Growth & Revenue 2024-2034

EMEA Leather Goods Market is segmented by Type (Genuine Leather, Synthetic Leather, Nubuck & Suede Leather, Patent Leather, Exotic Leather), Application (Handbags, Wallets & Small Leather Goods, Footwear, Belts & Accessories, Travel & Luggage), Distribution Channel (Department Stores, Specialty Retailers, Online Retail, Luxury Boutiques), End User (Men, Women, Unisex), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Leather Goods market includes a wide range of products such as handbags, wallets, footwear, belts, accessories, and travel goods made from genuine, synthetic, and specialty leathers. It serves fashion-conscious consumers across Europe, Middle East, and Africa, combining luxury and utilitarian value.

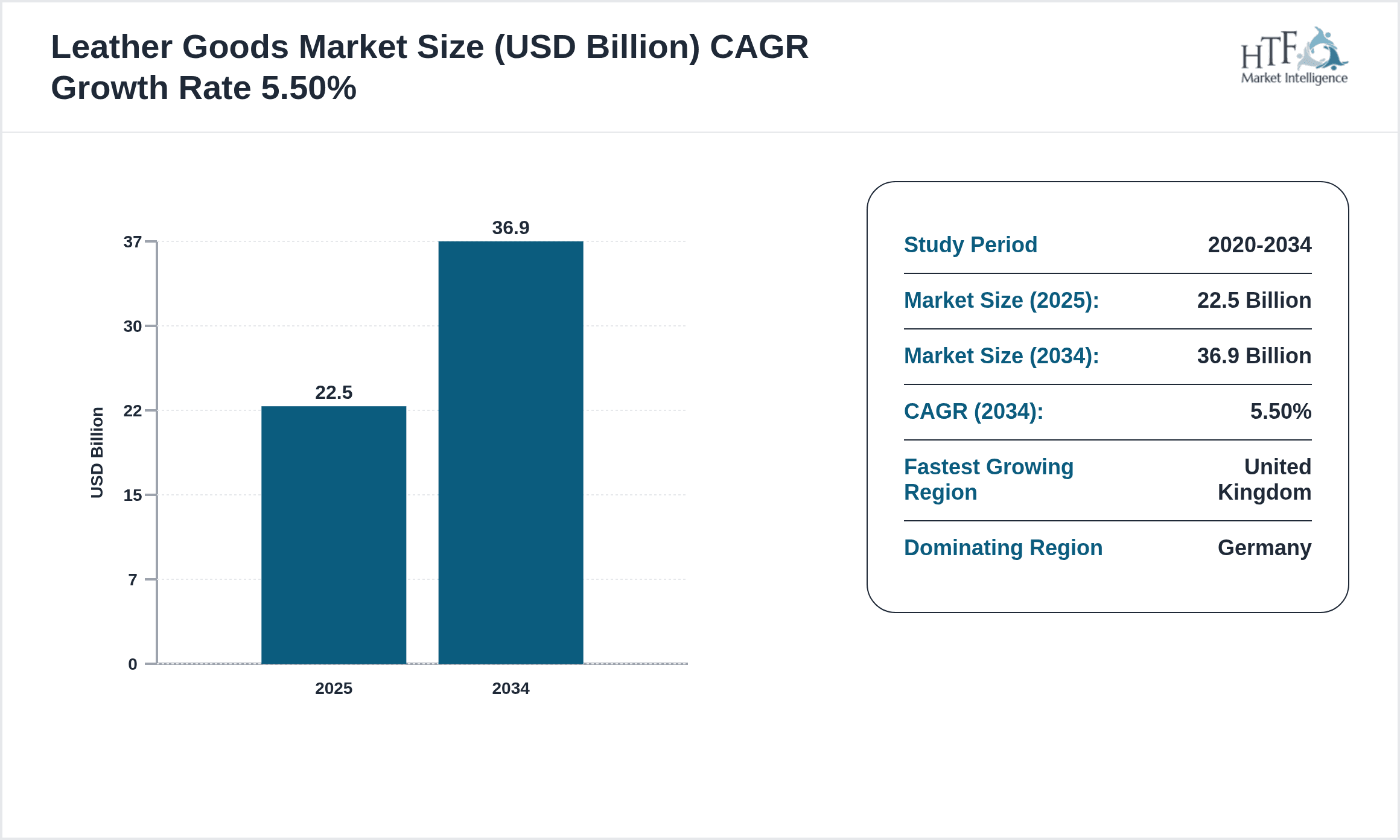

- •The market is currently valued at USD 22.5 Billion in 2024 and is forecasted to reach USD 36.9 Billion by 2034, growing at a CAGR of 5.5%, driven by rising disposable incomes, fashion trends, and increased demand for sustainable leather alternatives.

- •Key stakeholders benefit from innovation in synthetic leather and expanding e-commerce channels, while the market faces challenges related to environmental regulations and raw material costs, emphasizing opportunities in eco-friendly product segments.

Competitive Landscape

Competition in the EMEA Leather Goods market is intense with established luxury brands and emerging sustainable product manufacturers vying for market share. Key strategies include product innovation, brand heritage reinforcement, and expanding multi-channel retail presence. Companies invest heavily in R&D to develop eco-friendly leather alternatives and leverage digital marketing to engage younger demographics. Rivalry is marked by collaborations between designers and manufacturers to create exclusive collections. Pricing strategies balance premium positioning with accessibility in emerging markets. Distribution channels span brick-and-mortar stores, online platforms, and wholesale partnerships. Market entrants face high barriers due to brand loyalty and established supply chains. Future competitive dynamics will revolve around sustainability credentials and technological integration in product design and customer experience.

Leading Companies in EMEA Leather Goods Market

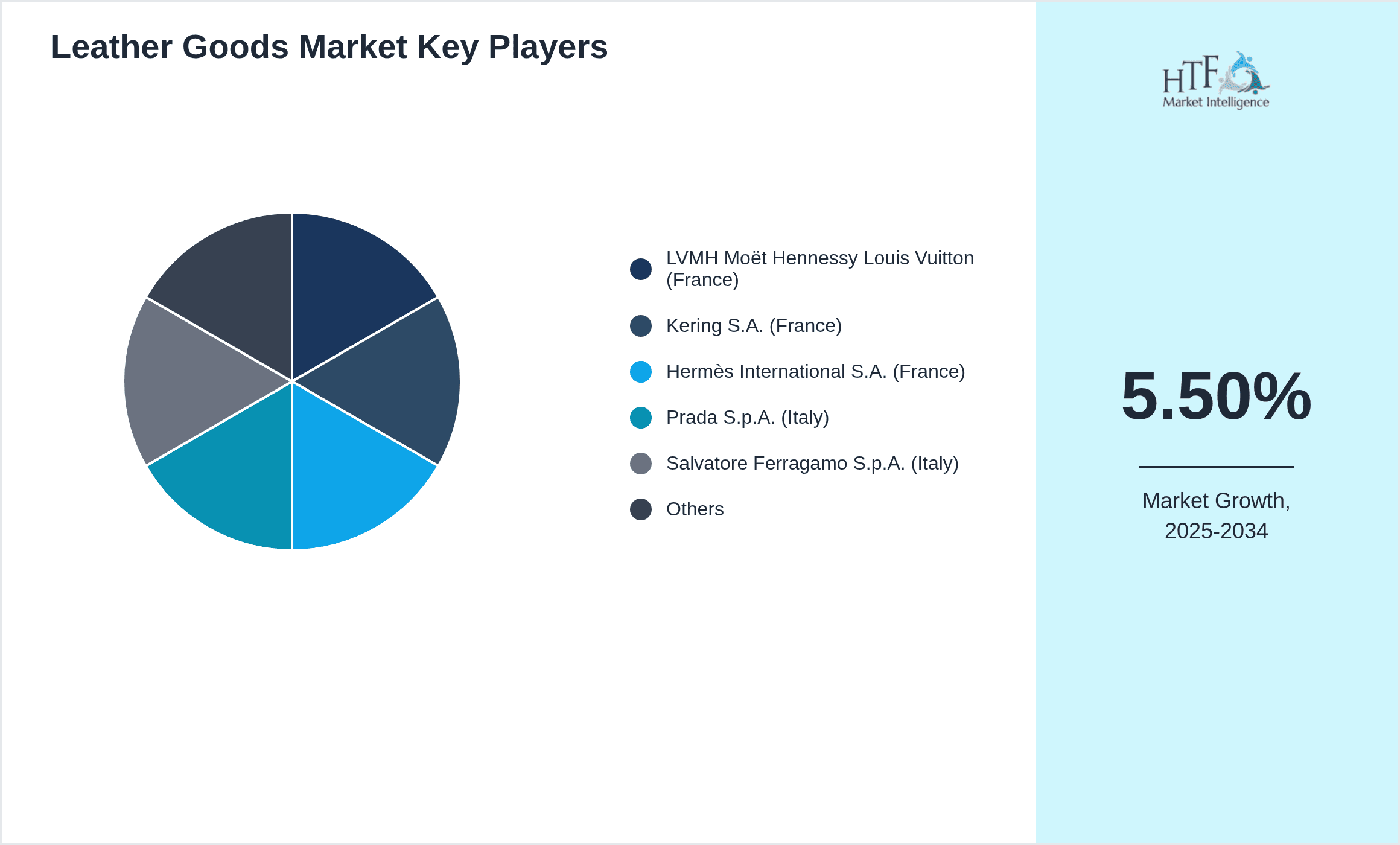

- •LVMH Moët Hennessy Louis Vuitton (France)

- •Kering S.A. (France)

- •Hermès International S.A. (France)

- •Prada S.p.A. (Italy)

- •Salvatore Ferragamo S.p.A. (Italy)

- •Tod's S.p.A. (Italy)

- •Burberry Group plc (United Kingdom)

- •Coach, Inc. (United Kingdom)

- •Smythson of Bond Street (United Kingdom)

- •Hugo Boss AG (Germany)

- •Braun Büffel (Germany)

- •Aspinal of London (United Kingdom)

- •Mulberry Group plc (United Kingdom)

- •MCM Worldwide (Germany)

- •Montblanc International GmbH (Germany)

- •Fossil Group, Inc. (United Kingdom)

- •Longchamp (France)

- •Ghurka (United Kingdom)

- •Lancel (France)

- •Asprey & Garrard (United Kingdom)

- •Valextra (Italy)

- •Etro S.p.A. (Italy)

- •Coccinelle S.p.A. (Italy)

- •Loewe (Spain)

- •Bally International AG (Switzerland)

Market Breakdown

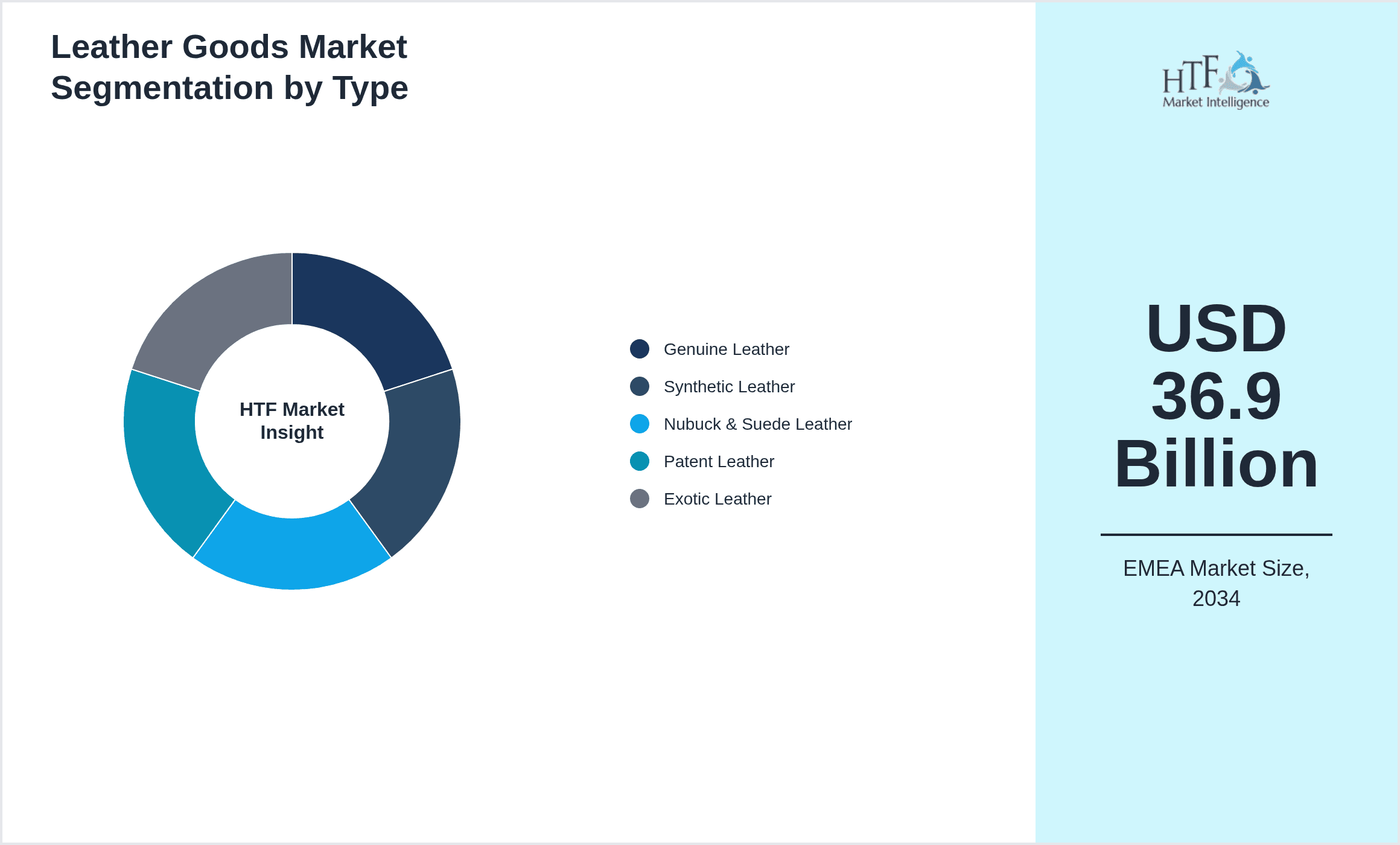

- •By Type

- ◦Genuine Leather

- ◦Synthetic Leather

- ◦Nubuck & Suede Leather

- ◦Patent Leather

- ◦Exotic Leather

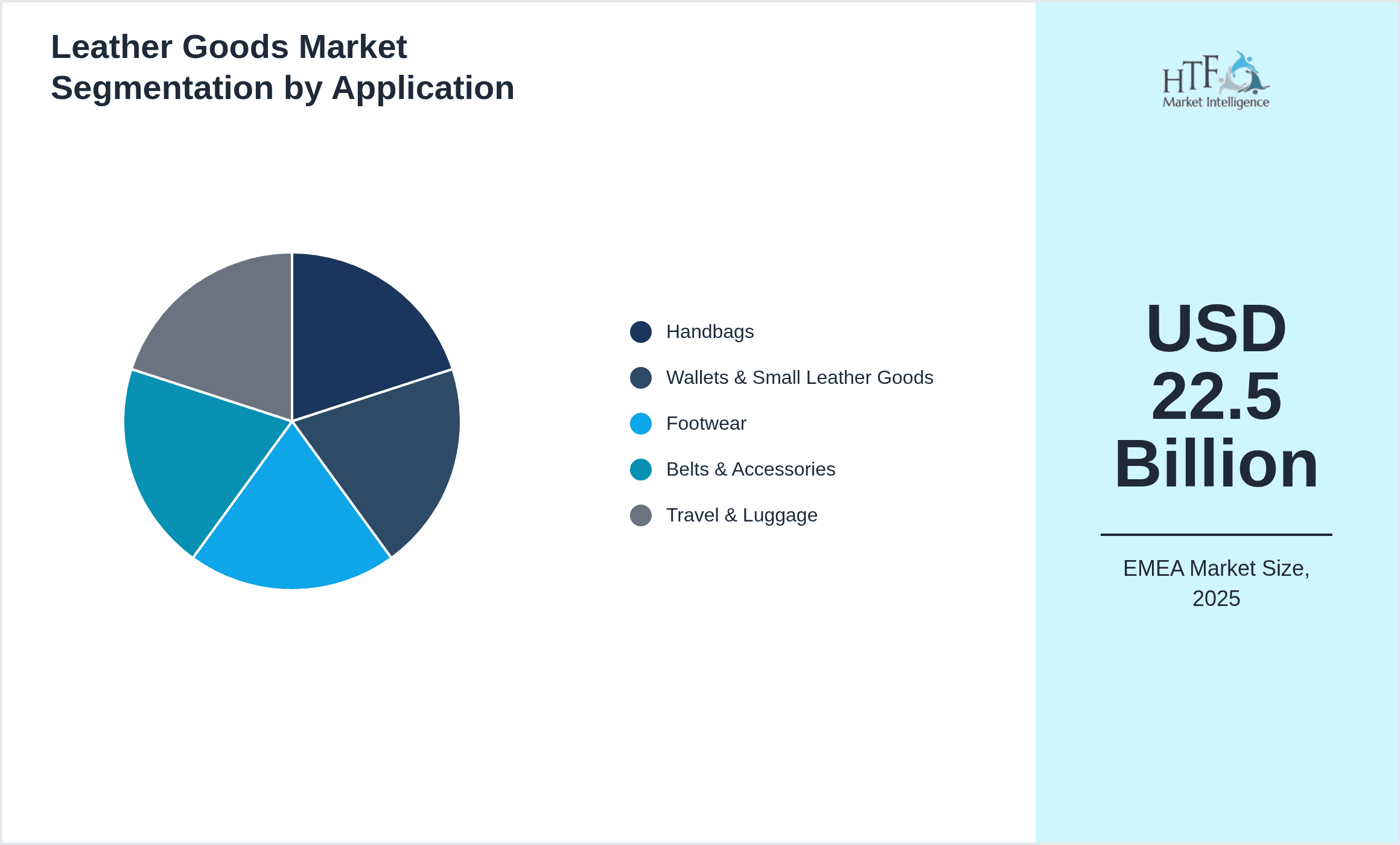

- •By Application

- ◦Handbags

- ◦Wallets & Small Leather Goods

- ◦Footwear

- ◦Belts & Accessories

- ◦Travel & Luggage

- •By Distribution Channel

- ◦Department Stores

- ◦Specialty Retailers

- ◦Online Retail

- ◦Luxury Boutiques

- •By End User

- ◦Men

- ◦Women

- ◦Unisex

Growth Drivers

- •Increasing disposable incomes across major EMEA countries such as Germany, France, and the UK fuel demand for premium and luxury leather goods, enhancing market growth prospects.

- •Growing popularity of synthetic leather driven by sustainability concerns and technological advances is expanding the accessible consumer base and creating new product categories.

- •Rising e-commerce penetration across Europe and the Middle East facilitates broader market reach and convenience, boosting sales volumes especially among younger consumers.

- •Expanding tourism and travel in EMEA increases demand for travel and luggage leather goods, contributing positively to market expansion.

- •Collaborations between luxury brands and designers create exclusive collections, attracting affluent customers and reinforcing brand loyalty.

Market Trends

- •Sustainability is a key trend with brands adopting eco-friendly tanning processes and biodegradable synthetic leathers to meet consumer expectations and regulatory standards.

- •Digital transformation drives personalized shopping experiences and augmented reality try-ons, enhancing consumer engagement and satisfaction within the leather goods market.

- •Minimalist and functional design trends influence product development, especially in wallets and small leather goods, aligning with modern consumer preferences.

- •Resurgence of vintage and heritage-inspired collections reflects consumer desire for timeless style and craftsmanship, boosting demand for genuine leather goods.

- •Increased cross-border collaborations between EMEA and emerging markets stimulate innovation and broaden market appeal.

Market Opportunities

- •Rising demand for sustainable and cruelty-free leather alternatives presents significant growth opportunities for synthetic leather manufacturers and innovators in EMEA.

- •Expansion of online luxury retail platforms enables brands to tap into underserved markets in Middle East and Africa offering customized leather goods.

- •Emerging consumer segments such as millennials and Gen Z show increased interest in premium yet eco-conscious leather products, driving product diversification.

- •Technological integration such as blockchain for supply chain transparency offers brands a competitive edge and builds consumer trust.

- •Collaborations with local artisans across EMEA can enhance authenticity and support regional craftsmanship, attracting niche luxury consumers.

Market Challenges

- •Volatility in raw material prices, especially for genuine leather, increases production costs and pressures profit margins for manufacturers and retailers.

- •Stringent environmental regulations in Europe related to tanning and chemical use require costly compliance investments, impacting smaller players disproportionately.

- •Counterfeit products and grey market imports dilute brand value and hinder growth prospects for established EMEA leather goods companies.

- •Supply chain disruptions due to geopolitical uncertainties in the Middle East and Africa affect timely delivery and inventory management.

- •Changing consumer preferences towards non-leather alternatives challenge traditional leather goods manufacturers to innovate rapidly to remain relevant.

Regulatory Framework

- •From 2023 to 2024, the EU imposed stricter regulations on chemical usage in leather tanning processes to reduce environmental pollution, mandating safer alternatives and increased supplier audits.

- •New labeling requirements introduced in 2023 require transparency regarding leather origin and sustainability certifications, impacting product packaging and marketing strategies.

- •The Middle East has enhanced import regulations for leather goods, focusing on quality control and compliance with regional standards effective since early 2024.

- •Anti-counterfeiting laws across EMEA have been strengthened between 2022 and 2024, increasing penalties and enforcement actions to protect brand integrity.

- •Trade agreements within EMEA countries facilitate tariff reductions on raw leather imports, promoting regional manufacturing and impacting pricing dynamics.

Industry Insights

In March 2024, a leading French luxury brand launched a new line of sustainable synthetic leather handbags featuring innovative biodegradable materials, marking a significant step towards greener fashion in EMEA. This launch received strong consumer interest, highlighting shifting market preferences towards eco-conscious products. Additionally, in September 2023, an Italian footwear manufacturer introduced an advanced leather tanning technology that reduces water consumption by 40%, setting new industry standards for environmental responsibility in leather processing within the region.

Mergers & Acquisitions

- •In June 2023, a prominent German leather goods manufacturer acquired a UK-based sustainable leather startup to enhance its portfolio of eco-friendly products. This strategic move aims to expand the company’s presence in the synthetic leather segment and capitalize on growing consumer demand for environmentally responsible goods across EMEA, leveraging the startup’s innovative material technology and agile market approach to accelerate growth.

- •In November 2024, a major French luxury conglomerate completed the acquisition of an Italian artisanal leather brand, reinforcing its foothold in the premium handcrafted segment. The acquisition enables the group to diversify its product range while preserving heritage craftsmanship, catering to affluent customers seeking exclusivity and authenticity within the EMEA leather goods market.

Recent Industry News

- •15th January 2025, Kering S.A. announced a strategic partnership with a leading Dutch technology firm to develop next-generation sustainable leather alternatives. The collaboration focuses on biofabrication techniques aimed at reducing environmental impact while maintaining luxury standards. This initiative positions Kering at the forefront of innovation in the EMEA leather goods sector. Source: Official Kering Press Release.

- •22nd March 2025, Hermès International unveiled a limited-edition collection featuring exotic leather goods sourced through new traceability programs ensuring ethical supply chains. The launch was accompanied by a digital campaign highlighting sustainability efforts, attracting strong consumer interest in Europe and the Middle East. Source: Hermès Corporate Website.

- •10th June 2025, Prada S.p.A. expanded its e-commerce platform to include personalized leather goods customization options, utilizing 3D visualization technology. This enhancement improves customer engagement and broadens market reach across EMEA, especially targeting millennial and Gen Z demographics. Source: Industry Fashion News.

- •5th September 2025, Burberry Group plc opened a new flagship boutique in Dubai, featuring immersive retail experiences and exclusive leather goods collections. This expansion underscores Burberry’s commitment to growth in the Middle East market and reinforces its luxury brand presence across EMEA. Source: Burberry Official Announcement.

Market Statistics

- •CAGR by 2034: 5.5%

- •Market Size by 2034: USD 36.9 Billion

- •Market Size in 2025: USD 23.8 Billion

- •Dominating Type: Genuine Leather

- •Next-Following Type: Synthetic Leather

- •Dominating Application: Handbags

- •Next-Following Application: Wallets & Small Leather Goods

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: United Kingdom

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Genuine Leather: 60%

- ◦Synthetic Leather: 25%

- •Market Share (%) of Dominating vs Followed Application

- ◦Handbags: 40%

- ◦Wallets & Small Leather Goods: 22%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Genuine Leather: 4.8%

- ◦Synthetic Leather: 8.9%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Handbags: 5.2%

- ◦Wallets & Small Leather Goods: 6.7%

Top Companies Profiled in EMEA Leather Goods Market

- •LVMH Moët Hennessy Louis Vuitton (France)

- •Kering S.A. (France)

- •Hermès International S.A. (France)

- •Prada S.p.A. (Italy)

- •Burberry Group plc (United Kingdom)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Kingdom is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 22.5 Billion |

| Forecast Year Market Size | USD 36.9 Billion |

| CAGR | 5.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 5.4% |

| Scope of Report | Market is segmented by Type (Genuine Leather, Synthetic Leather, Nubuck & Suede Leather, Patent Leather, Exotic Leather), Application (Handbags, Wallets & Small Leather Goods, Footwear, Belts & Accessories, Travel & Luggage), Distribution Channel (Department Stores, Specialty Retailers, Online Retail, Luxury Boutiques), End User (Men, Women, Unisex) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | LVMH Moët Hennessy Louis Vuitton (France), Kering S.A. (France), Hermès International S.A. (France), Prada S.p.A. (Italy), Salvatore Ferragamo S.p.A. (Italy), Tod's S.p.A. (Italy), Burberry Group plc (United Kingdom), Coach, Inc. (United Kingdom), Smythson of Bond Street (United Kingdom), Hugo Boss AG (Germany), Braun Büffel (Germany), Aspinal of London (United Kingdom), Mulberry Group plc (United Kingdom), MCM Worldwide (Germany), Montblanc International GmbH (Germany), Fossil Group, Inc. (United Kingdom), Longchamp (France), Ghurka (United Kingdom), Lancel (France), Asprey & Garrard (United Kingdom), Valextra (Italy), Etro S.p.A. (Italy), Coccinelle S.p.A. (Italy), Loewe (Spain), Bally International AG (Switzerland) |

EMEA Leather Goods Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.