GCC Scaffold Material Market - Middle East Size & Outlook 2020-2034

GCC Scaffold Material Market is segmented by Type (Steel Scaffold, Aluminum Scaffold, Timber Scaffold, System Scaffold, Tube and Coupler Scaffold), Application (Commercial Construction, Residential Construction, Industrial Construction, Infrastructure Projects, Maintenance and Repair), Service Type (Sales, Rental, Installation Services, Inspection and Maintenance), End-User Industry (Oil & Gas, Real Estate Development, Transportation, Utilities, Manufacturing), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

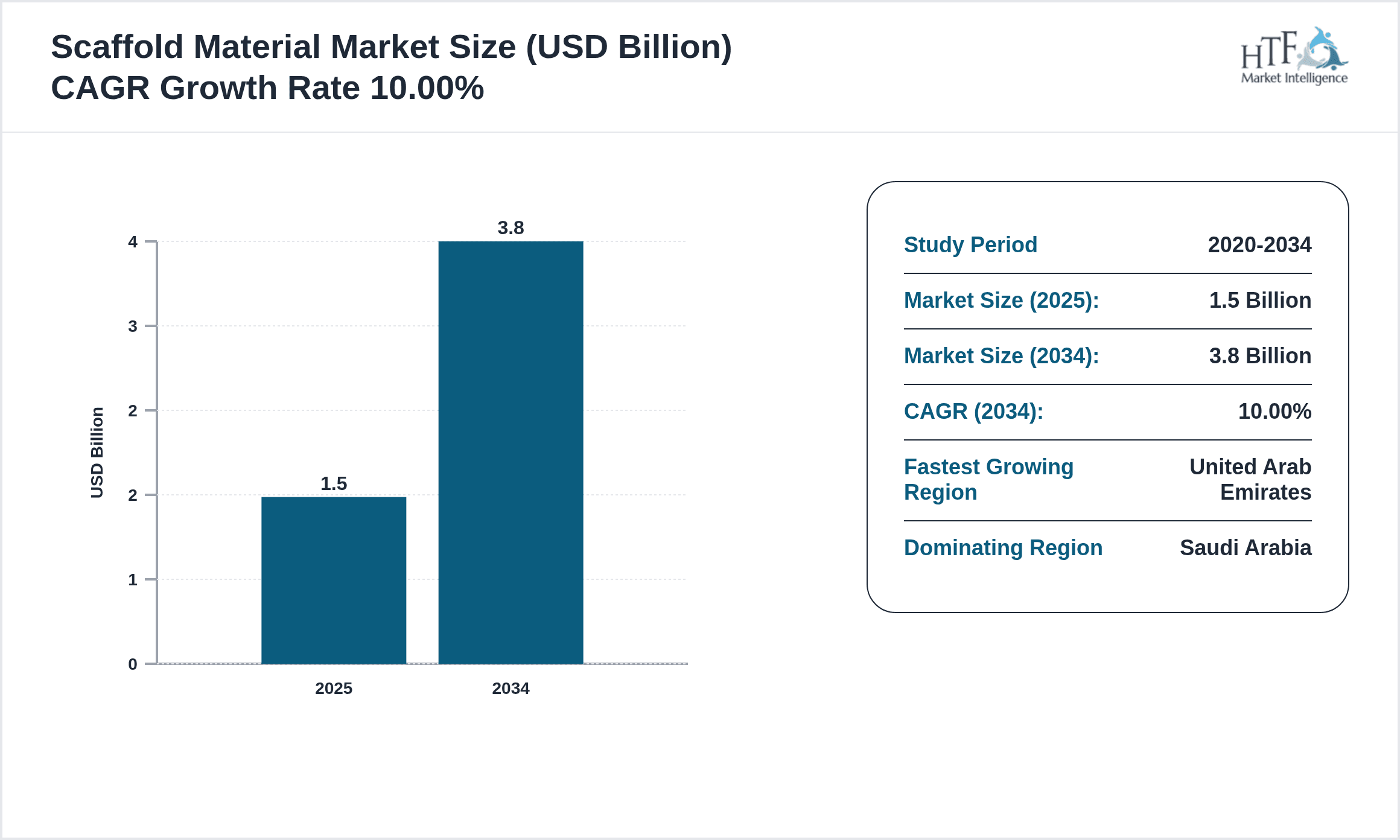

- •The GCC Scaffold Material market includes a variety of scaffolding products essential for supporting construction and maintenance activities across the region. The market features types such as steel, aluminum, timber, system scaffold, and tube and coupler scaffold. These materials are used extensively in commercial, residential, industrial, infrastructure, and maintenance projects. Driven by rapid urbanization, infrastructure development, and strong industrial growth, the market is forecasted to expand significantly from 2025 to 2034, underpinning the region's construction sector ambitions.

- •Key market highlights include a base market size of USD 1.5 Billion in 2025, expected to reach USD 3.8 Billion by 2034, exhibiting a CAGR of approximately 10%. Saudi Arabia dominates the market with a 35% share, while the UAE is the fastest growing country at a CAGR of 12.5%, reflecting robust construction activity and investment inflows.

- •The market offers strategic value to construction companies, scaffold manufacturers, rental service providers, and investors by enabling safer, efficient, and compliant construction practices. Innovations in lightweight and modular scaffolding, coupled with stringent regulatory standards, are enhancing market attractiveness and operational efficiency across the GCC.

Competitive Landscape

The competitive environment in the GCC Scaffold Material market is characterized by a mix of multinational corporations and regional manufacturers focusing on product innovation, safety compliance, and strategic partnerships. Companies compete through differentiation in material quality, modular system offerings, and rental services. Market players invest in advanced manufacturing technologies to improve scaffold durability and reduce assembly time. The landscape also sees mergers and acquisitions aimed at consolidating market share and expanding regional footprints. Pricing strategies are influenced by raw material costs and regional demand fluctuations. Distribution channels include direct sales, distributors, and rental services, with increasing emphasis on digital platforms to enhance customer reach. Regional competition is intense, particularly among Saudi Arabia and UAE-based companies, driven by large-scale infrastructure and industrial projects. Future trends suggest increasing adoption of lightweight aluminum systems and digital monitoring solutions to ensure scaffold safety and compliance.

Leading Companies in GCC Scaffold Material Market

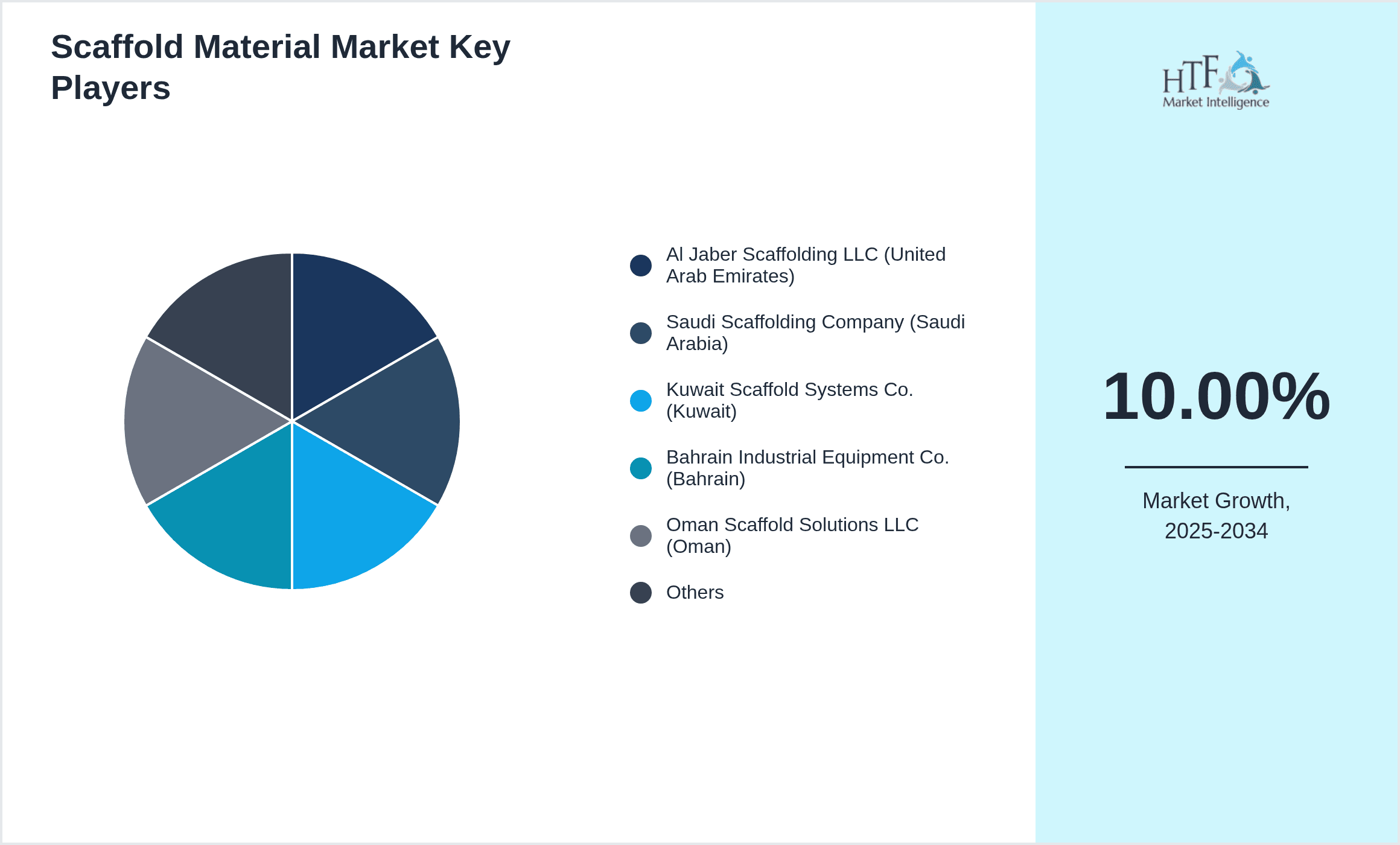

- •Al Jaber Scaffolding LLC (United Arab Emirates)

- •Saudi Scaffolding Company (Saudi Arabia)

- •Kuwait Scaffold Systems Co. (Kuwait)

- •Bahrain Industrial Equipment Co. (Bahrain)

- •Oman Scaffold Solutions LLC (Oman)

- •Qatar Scaffolding Services (Qatar)

- •Gulf Scaffold Supplies (United Arab Emirates)

- •Middle East Scaffold Trading Ltd. (Saudi Arabia)

- •Emirates Scaffold Manufacturing (United Arab Emirates)

- •Kuwait Industrial Scaffolding (Kuwait)

- •Bahrain Scaffold Equipment (Bahrain)

- •Oman Construction Supplies (Oman)

- •Qatar Building Materials Co. (Qatar)

- •Saudi Arabian Scaffold Solutions (Saudi Arabia)

- •Gulf Construction Materials (United Arab Emirates)

- •Al Zayani Scaffolding (Bahrain)

- •Al Suwaidi Scaffolding LLC (United Arab Emirates)

- •National Scaffold Co. (Saudi Arabia)

- •Kuwait Technical Scaffolding (Kuwait)

- •Oman Scaffold Services (Oman)

- •Qatar Scaffolding Equipment (Qatar)

- •Emirates Engineering Supplies (United Arab Emirates)

- •Saudi Scaffold Rental Services (Saudi Arabia)

- •Bahrain Scaffolding Solutions (Bahrain)

- •GCC Scaffold Systems Ltd. (United Arab Emirates)

Market Breakdown

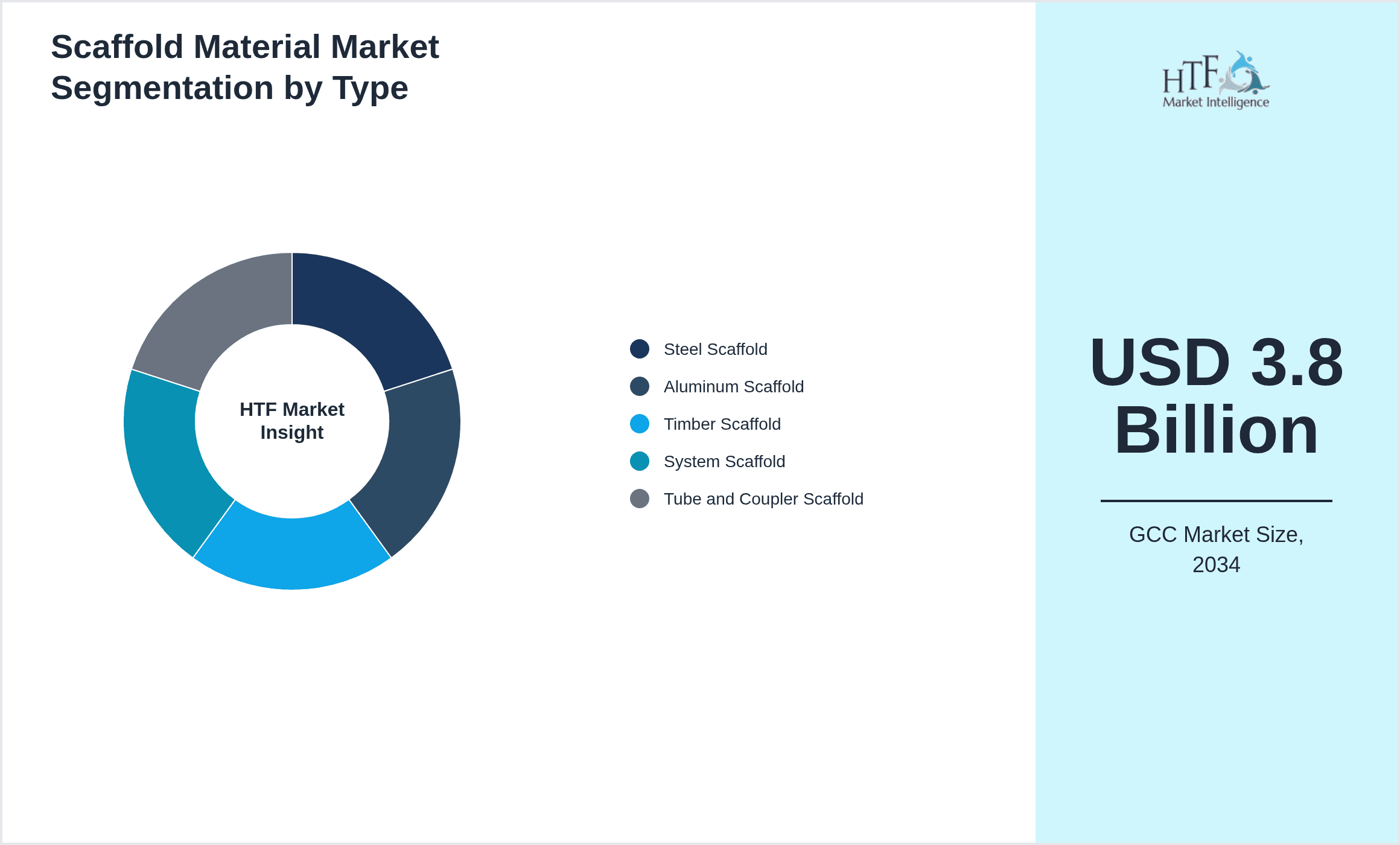

- •By Type

- ◦Steel Scaffold

- ◦Aluminum Scaffold

- ◦Timber Scaffold

- ◦System Scaffold

- ◦Tube and Coupler Scaffold

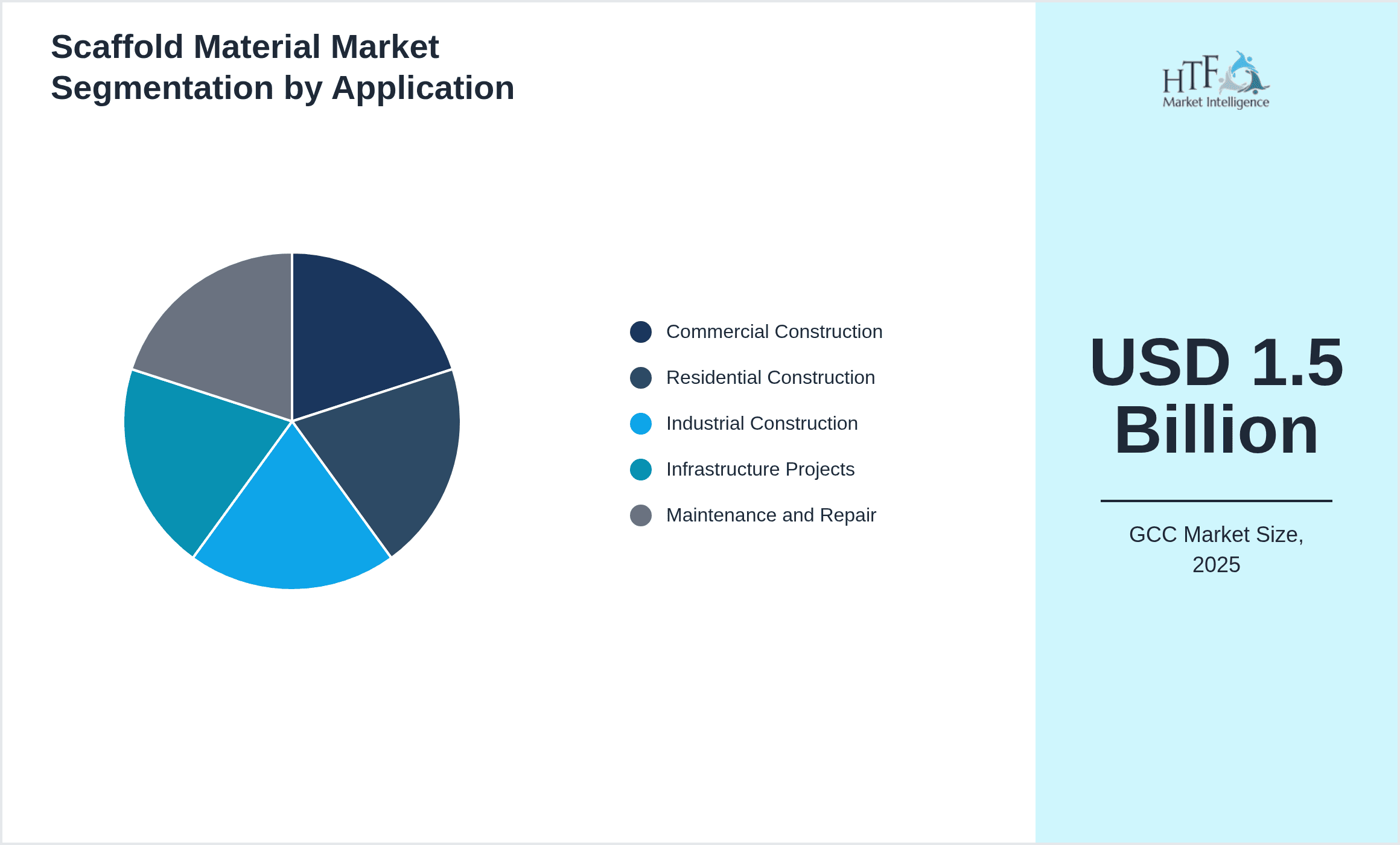

- •By Application

- ◦Commercial Construction

- ◦Residential Construction

- ◦Industrial Construction

- ◦Infrastructure Projects

- ◦Maintenance and Repair

- •By Service Type

- ◦Sales

- ◦Rental

- ◦Installation Services

- ◦Inspection and Maintenance

- •By End-User Industry

- ◦Oil & Gas

- ◦Real Estate Development

- ◦Transportation

- ◦Utilities

- ◦Manufacturing

Growth Dynamics

The GCC Scaffold Material market growth is primarily driven by the surge in large-scale infrastructure and urban development projects, particularly in Saudi Arabia and the UAE. Government initiatives such as Saudi Vision 2030 and Expo 2020 Dubai have accelerated construction demand, necessitating high-quality scaffolding solutions that ensure safety and efficiency. Increasing investments in oil & gas sector maintenance further augment demand for durable scaffold materials. Additionally, technological advancements in modular and lightweight scaffolding systems enhance on-site assembly speed and worker safety, fostering adoption across the region. The growing emphasis on compliance with stringent safety regulations also compels companies to invest in superior scaffold materials, contributing to market expansion.

Market Trends

A significant trend in the GCC scaffold market is the adoption of aluminum scaffold systems due to their lightweight nature and ease of handling, which reduces labor costs and assembly time. Digitalization is influencing safety management through IoT-enabled scaffold monitoring devices that detect structural integrity in real-time. Increasing rental services are gaining popularity as cost-efficient alternatives to outright purchases for temporary projects. Sustainability is becoming a focus, with companies exploring recyclable and eco-friendly scaffold materials. Furthermore, the integration of Building Information Modeling (BIM) with scaffold planning enhances project precision and safety compliance, reflecting broader digital transformation trends in construction.

Market Opportunities

The GCC scaffold material market presents vast opportunities driven by the region's expanding construction and industrial sectors. Emerging demand for lightweight and modular scaffolding systems offers potential for manufacturers to innovate and capture market share. Infrastructure development, including transport networks and smart city projects, creates new application segments. Opportunities also exist in providing integrated scaffold rental and inspection services capitalizing on increasing safety regulations. Geographic expansion into underpenetrated GCC countries such as Bahrain and Oman can further boost growth. Collaborations with technology providers for digital monitoring solutions represent a promising avenue to enhance product offerings and differentiate in a competitive market.

Market Challenges

Despite growth prospects, the GCC scaffold material market faces challenges including fluctuating raw material prices, which impact cost structures and pricing strategies. The high capital investment required for advanced scaffold manufacturing limits entry for smaller players. Regulatory compliance across multiple GCC countries can be complex due to varying safety standards and inspection requirements, increasing operational burdens. Additionally, the market contends with occasional supply chain disruptions that affect timely delivery. Skilled labor shortages for scaffold assembly and maintenance further constrain operational efficiency. The prevalence of cheaper, low-quality imports poses risks to market stability and safety standards, necessitating stringent quality controls and enforcement.

Regulatory Framework

The GCC scaffold material market operates under comprehensive regulatory frameworks established between 2020 and 2025 to enhance construction site safety and scaffold quality. Saudi Arabia’s Ministry of Labor and Social Development enforces strict scaffold safety codes requiring regular inspections and certification. The UAE’s Occupational Safety and Health Center mandates compliance with international scaffold standards such as OSHA and BS EN 12811. Qatar and Kuwait have introduced scaffold licensing procedures and mandatory training programs for scaffold erectors. These regulations emphasize material quality, load capacity, and worker safety measures. Compliance is monitored through frequent audits, with penalties for violations. The regulatory landscape encourages adoption of standardized scaffold materials and promotes integration of digital safety monitoring tools to reduce accidents and enhance operational oversight across GCC construction sites.

Market Intelligence

- •15th January 2025, Al Jaber Scaffolding LLC launched a new line of lightweight aluminum scaffolding systems targeting the UAE and Saudi Arabian construction markets. These systems feature modular design for rapid assembly and enhanced worker safety, aligning with regional regulatory requirements. The launch aims to capitalize on growing infrastructure projects and government initiatives promoting sustainable construction practices. The product line includes IoT-enabled sensors for real-time structural health monitoring, improving safety compliance and reducing inspection costs. Al Jaber’s strategic focus on innovation and digital integration positions it as a key market player driving scaffold technology advancement in the GCC. Source: Al Jaber Official Press Release

- •30th March 2025, Saudi Scaffolding Company announced a partnership with a European manufacturer to introduce high-strength steel scaffold materials in the GCC region. This collaboration enhances product quality and broadens the company’s portfolio to serve mega construction and oil & gas maintenance projects. The alliance supports Saudi Arabia’s Vision 2030 construction boom by providing durable scaffolding solutions that meet stringent safety standards. The partnership includes knowledge transfer and localized manufacturing initiatives to reduce lead times and costs. This strategic move strengthens Saudi Scaffolding’s competitive position and contributes to regional market consolidation. Source: Saudi Scaffolding Company Website

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.5 Billion |

| Forecast Year Market Size | USD 3.8 Billion |

| CAGR | 10% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.6% |

| Scope of Report | Market is segmented by Type (Steel Scaffold, Aluminum Scaffold, Timber Scaffold, System Scaffold, Tube and Coupler Scaffold), Application (Commercial Construction, Residential Construction, Industrial Construction, Infrastructure Projects, Maintenance and Repair), Service Type (Sales, Rental, Installation Services, Inspection and Maintenance), End-User Industry (Oil & Gas, Real Estate Development, Transportation, Utilities, Manufacturing) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Al Jaber Scaffolding LLC (United Arab Emirates), Saudi Scaffolding Company (Saudi Arabia), Kuwait Scaffold Systems Co. (Kuwait), Bahrain Industrial Equipment Co. (Bahrain), Oman Scaffold Solutions LLC (Oman), Qatar Scaffolding Services (Qatar), Gulf Scaffold Supplies (United Arab Emirates), Middle East Scaffold Trading Ltd. (Saudi Arabia), Emirates Scaffold Manufacturing (United Arab Emirates), Kuwait Industrial Scaffolding (Kuwait), Bahrain Scaffold Equipment (Bahrain), Oman Construction Supplies (Oman), Qatar Building Materials Co. (Qatar), Saudi Arabian Scaffold Solutions (Saudi Arabia), Gulf Construction Materials (United Arab Emirates), Al Zayani Scaffolding (Bahrain), Al Suwaidi Scaffolding LLC (United Arab Emirates), National Scaffold Co. (Saudi Arabia), Kuwait Technical Scaffolding (Kuwait), Oman Scaffold Services (Oman), Qatar Scaffolding Equipment (Qatar), Emirates Engineering Supplies (United Arab Emirates), Saudi Scaffold Rental Services (Saudi Arabia), Bahrain Scaffolding Solutions (Bahrain), GCC Scaffold Systems Ltd. (United Arab Emirates) |

GCC Scaffold Material Market - Middle East Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.