Europe Diagnostic Nuclear Medicines Market - Europe Size & Outlook 2025-2034

Europe Diagnostic Nuclear Medicines Market is segmented by Application (Oncology Imaging, Cardiology Imaging, Neurology Imaging, Infection and Inflammation, Others), Type (Radiopharmaceuticals, Imaging Equipment, Software Solutions, Consumables, Services), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Diagnostic Nuclear Medicines market includes radiopharmaceuticals, imaging equipment, software, consumables, and services used for non-invasive disease diagnosis across oncology, cardiology, neurology, and infectious diseases. It supports healthcare providers in delivering precise diagnostics via nuclear imaging technologies such as PET and SPECT.

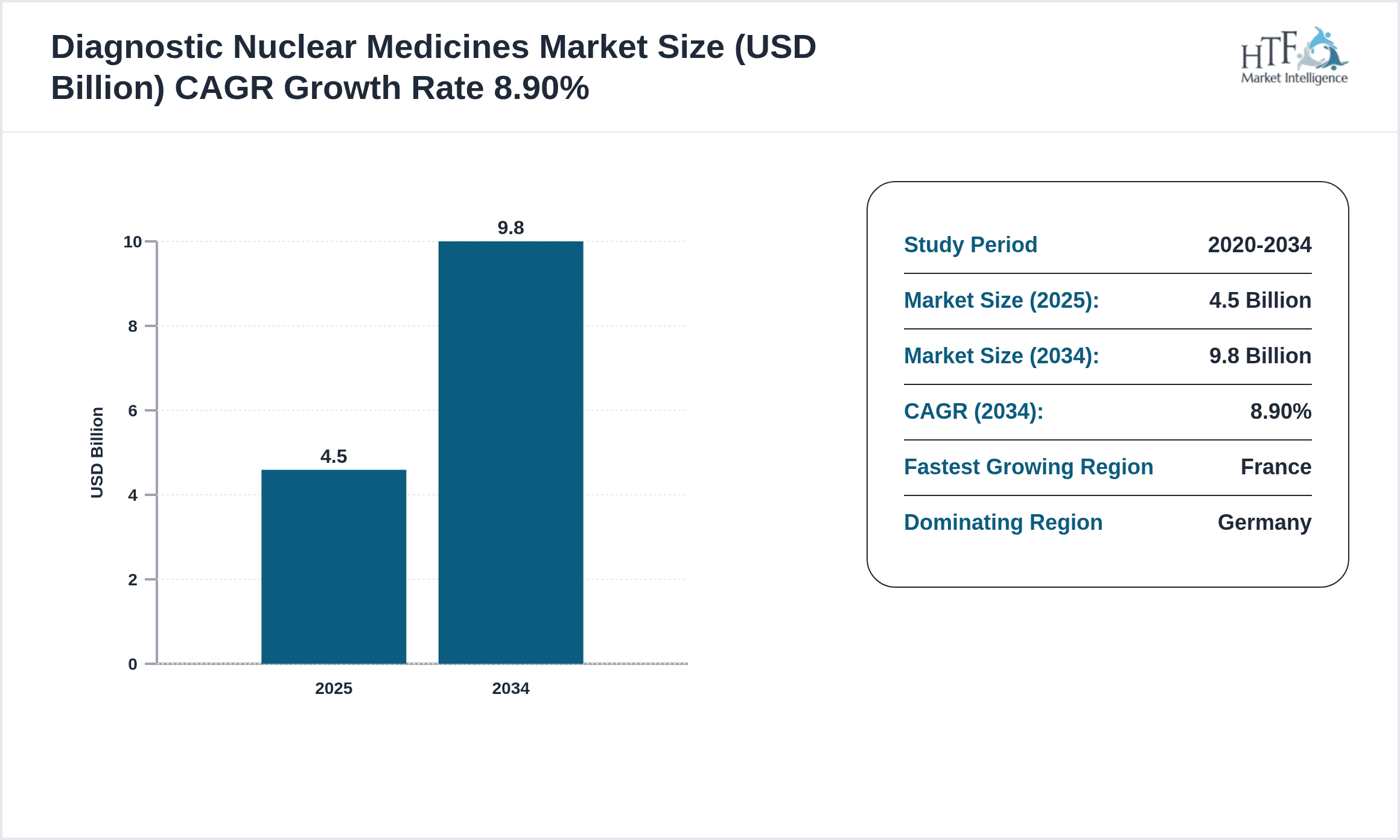

- •Key highlights include a robust CAGR of approximately 8.9% projected through 2034, driven by technological innovations, rising chronic disease prevalence, and expanding healthcare infrastructure across Europe’s major countries.

- •This market holds strategic importance for early disease detection and personalized treatment strategies, thereby enhancing patient outcomes and reducing healthcare costs across European medical facilities.

Competitive Landscape

The Europe Diagnostic Nuclear Medicines market exhibits intense competition characterized by innovation-led product development and strategic partnerships. Market leaders focus on enhancing radiopharmaceutical efficacy and imaging equipment precision to maintain competitive advantage. Companies invest heavily in R&D to advance novel tracers and hybrid imaging technologies, while also leveraging mergers and acquisitions to expand regional presence and product portfolios. The rivalry drives continuous improvements in diagnostic accuracy and operational efficiency. Pricing strategies balance innovation costs with reimbursement policies across European healthcare systems. Distribution and service quality further differentiate competitors. Future competitive trends indicate growing emphasis on personalized diagnostics, integration of AI in image analysis, and sustainability in production processes.

Leading Companies in Europe Diagnostic Nuclear Medicines Market

- •Siemens Healthineers (Germany)

- •GE Healthcare (United Kingdom)

- •Bayer AG (Germany)

- •Philips Healthcare (Netherlands)

- •Curium Pharma (France)

- •Lantheus Holdings (Ireland)

- •Advanced Accelerator Applications (France)

- •Bracco Imaging (Italy)

- •Eckert & Ziegler (Germany)

- •Isotopen Technologien München AG (Germany)

- •Sofie Biosciences (United Kingdom)

- •Nordion (United Kingdom)

- •Mallinckrodt Pharmaceuticals (Ireland)

- •Medi-Radiopharma (France)

- •Telix Pharmaceuticals (Belgium)

- •Nuclear Diagnostics (Netherlands)

- •IBA (Belgium)

- •Sandoz (Germany)

- •Curium US LLC (France)

- •Nordion (France)

- •PETNet Solutions (UK)

- •Nuvia Pharma (Germany)

- •Cyclopharm (Austria)

- •NuclearScan (Italy)

- •RadPharm (Switzerland)

Market Breakdown

- •By Type

- ◦Radiopharmaceuticals

- ◦Imaging Equipment

- ◦Software Solutions

- ◦Consumables

- ◦Services

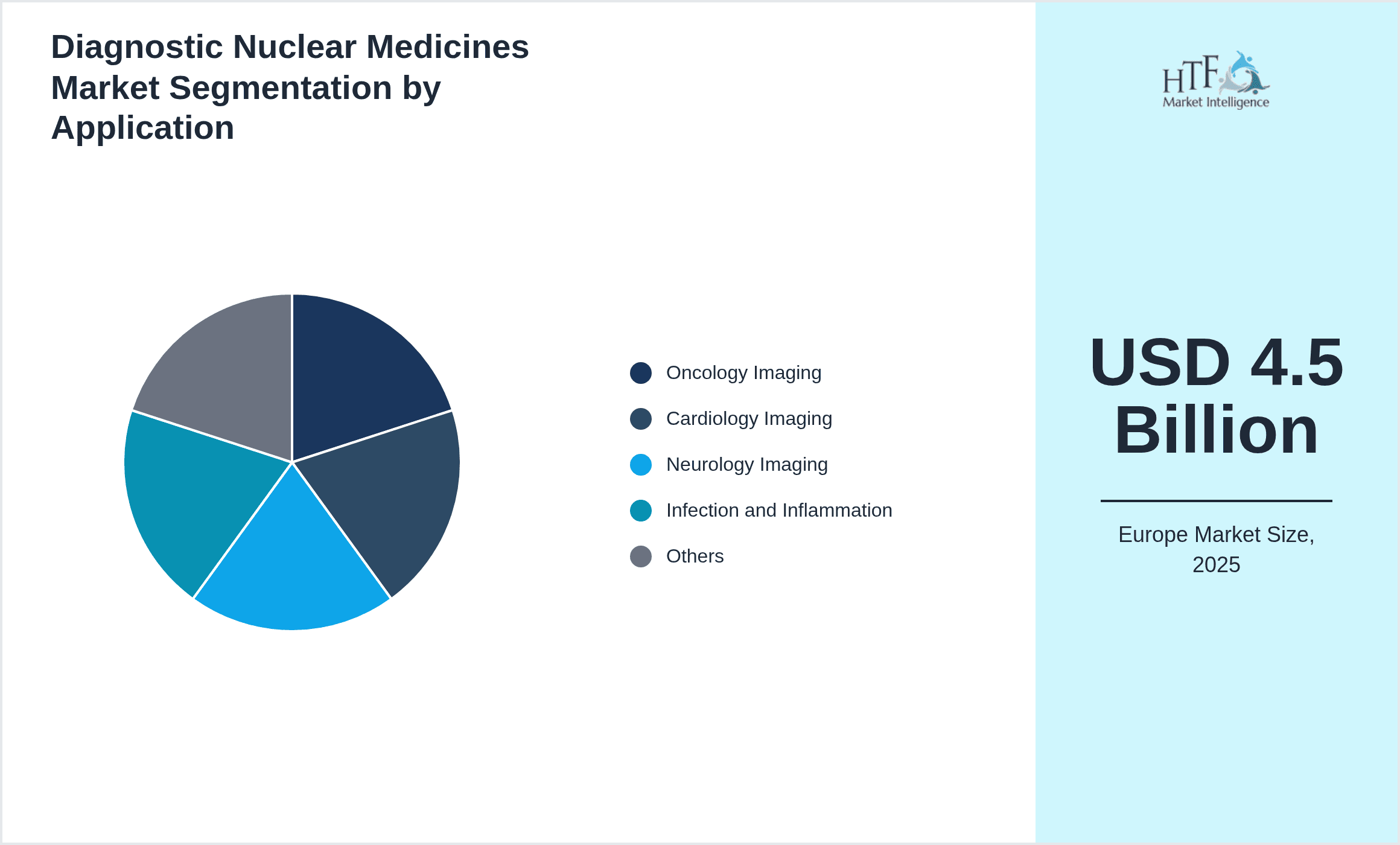

- •By Application

- ◦Oncology Imaging

- ◦Cardiology Imaging

- ◦Neurology Imaging

- ◦Infection and Inflammation

- ◦Others

- •By End User

- ◦Hospitals

- ◦Diagnostic Centers

- ◦Research Institutes

- ◦Outpatient Clinics

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Channels

Growth Drivers

- •Rising prevalence of chronic diseases such as cancer and cardiovascular disorders in Europe fuels demand for precise diagnostic nuclear medicines, enabling early detection and treatment monitoring.

- •Technological advancements in PET and SPECT imaging devices, along with novel radiopharmaceutical development, enhance diagnostic accuracy and patient outcomes, driving market expansion.

- •Increasing government initiatives and funding for nuclear medicine infrastructure and research across European countries improve market accessibility and adoption.

- •Growing preference for personalized medicine encourages integration of nuclear diagnostics to tailor therapies, boosting demand for advanced imaging and tracers.

- •Expansion of nuclear medicine services in emerging European markets such as Eastern Europe creates new growth avenues for market participants.

Market Trends

- •Adoption of hybrid imaging technologies combining PET/CT and SPECT/CT enhances diagnostic capabilities by providing functional and anatomical information simultaneously.

- •Integration of artificial intelligence and machine learning in image processing software improves diagnostic precision and reduces interpretation times.

- •Increased focus on development of theranostic agents that combine diagnostic and therapeutic functions strengthens market positioning.

- •Sustainability initiatives in radiopharmaceutical production reduce environmental impact and align with European regulatory expectations.

- •Collaborative partnerships between pharmaceutical companies and healthcare providers accelerate innovation and market penetration.

Market Opportunities

- •Expansion into underserved Eastern European countries presents significant untapped potential due to rising healthcare investments and infrastructure development.

- •Development of novel radiotracers targeting emerging biomarkers offers opportunities for differentiation and capturing niche markets.

- •Integration of digital health solutions and telemedicine with nuclear diagnostics can enhance remote patient monitoring and follow-up care.

- •Strategic collaborations with academic institutions to accelerate clinical trials and regulatory approvals can expedite product launches.

- •Growing demand for minimally invasive diagnostic methods supports innovation in radiopharmaceutical delivery and imaging techniques.

Market Challenges

- •High costs associated with advanced imaging equipment and radiopharmaceutical production limit accessibility, especially in smaller healthcare facilities.

- •Stringent and complex regulatory requirements across European countries delay product approvals and market entry strategies.

- •Limitations in skilled workforce trained in nuclear medicine hamper wider adoption and operational efficiency.

- •Competition from alternative diagnostic modalities such as MRI and CT scans affects market share for nuclear imaging.

- •Supply chain disruptions for radioisotopes and consumables pose risks to continuous service delivery and patient care.

Regulatory Framework

- •Between 2023 and 2025, the European Medicines Agency (EMA) enhanced guidelines on radiopharmaceutical manufacturing, emphasizing Good Manufacturing Practices (GMP) compliance to ensure safety and quality.

- •New EU directives introduced stricter radiation protection standards for diagnostic nuclear medicine facilities, mandating regular audits and staff training programs.

- •Revised clinical trial protocols require comprehensive pharmacovigilance and patient data transparency, impacting the approval timeline for new diagnostic agents.

- •Several countries adopted harmonized reimbursement policies to facilitate equitable access to nuclear diagnostic services across the region.

- •Government incentives for adopting innovative nuclear medicine technologies aim to boost market growth and improve healthcare outcomes.

Industry Insights

In March 2024, Curium Pharma launched a next-generation PET radiopharmaceutical targeting prostate cancer, featuring enhanced imaging clarity and faster patient throughput, expected to strengthen its competitive position in Europe’s oncology diagnostics segment. The innovation aligns with growing demand for precision diagnostics. Additionally, in November 2023, Siemens Healthineers introduced AI-powered software upgrades for its SPECT/CT scanners, significantly improving diagnostic accuracy and workflow efficiency in cardiology applications, marking a key technological advancement influencing the European market landscape.

Mergers & Acquisitions

- •In July 2023, GE Healthcare completed the acquisition of a leading European radiopharmaceutical manufacturer, expanding its portfolio in diagnostic nuclear medicines and strengthening its foothold in the oncology imaging market. This strategic move enhances GE’s production capabilities and accelerates innovation pipelines within Europe’s competitive landscape.

- •In February 2024, Philips Healthcare acquired a software solutions provider specializing in AI-driven nuclear medicine image analysis. This acquisition facilitates integration of advanced analytics into Philips’ imaging equipment, improving diagnostic accuracy and operational efficiency across European healthcare providers.

Recent Industry News

- •On 15th January 2025, Bracco Imaging announced a partnership with a major German hospital network to deploy its latest SPECT imaging systems across multiple centers, enhancing diagnostic services availability. This collaboration aims to improve early disease detection and patient management, driving growth in the diagnostic nuclear medicines segment. Source: Official Company Press Release

- •On 2nd March 2025, Bayer AG launched a novel radiopharmaceutical for neurology imaging approved across Europe, targeting Alzheimer’s disease biomarkers. The product offers improved brain imaging resolution and faster scan times, expected to capture significant market share in neurological diagnostics. Source: Industry Publication

- •On 20th May 2025, Curium Pharma expanded its production facility in France to increase capacity for PET radiotracers, addressing growing demand in oncology and cardiology applications throughout Europe. The expansion includes advanced automation technologies to enhance manufacturing efficiency. Source: Company Website

- •On 10th September 2025, Siemens Healthineers unveiled a cloud-based nuclear imaging data management platform designed to streamline workflow and facilitate remote diagnostics, supporting telemedicine initiatives in European healthcare systems. The platform integrates AI tools for enhanced image interpretation. Source: Industry Newswire

Market Statistics

- •CAGR by 2034: 8.9%

- •Market Size by 2034: USD 9.8 Billion

- •Market Size in 2025: USD 4.5 Billion

- •Dominating Type: Radiopharmaceuticals

- •Next-Following Type: Imaging Equipment

- •Dominating Application: Oncology Imaging

- •Next-Following Application: Cardiology Imaging

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: France

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: Radiopharmaceuticals 55%, Imaging Equipment 25%

- •Market Share (%) of Dominating vs Followed Application: Oncology Imaging 45%, Cardiology Imaging 30%

- •Growth Rate (%) of Dominating vs Followed Type: Radiopharmaceuticals 7.5%, Imaging Equipment 11.2%

- •Growth Rate (%) of Dominating vs Followed Application: Oncology Imaging 8.3%, Cardiology Imaging 9.5%

Top 5 Global Players

- •Siemens Healthineers (Germany)

- •GE Healthcare (United Kingdom)

- •Bayer AG (Germany)

- •Philips Healthcare (Netherlands)

- •Curium Pharma (France)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 9.8 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.6% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Siemens Healthineers (Germany), GE Healthcare (United Kingdom), Bayer AG (Germany), Philips Healthcare (Netherlands), Curium Pharma (France), Lantheus Holdings (Ireland), Advanced Accelerator Applications (France), Bracco Imaging (Italy), Eckert & Ziegler (Germany), Isotopen Technologien München AG (Germany), Sofie Biosciences (United Kingdom), Nordion (United Kingdom), Mallinckrodt Pharmaceuticals (Ireland), Medi-Radiopharma (France), Telix Pharmaceuticals (Belgium), Nuclear Diagnostics (Netherlands), IBA (Belgium), Sandoz (Germany), Curium US LLC (France), Nordion (France), PETNet Solutions (UK), Nuvia Pharma (Germany), Cyclopharm (Austria), NuclearScan (Italy), RadPharm (Switzerland) |

Europe Diagnostic Nuclear Medicines Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.