Europe Industrial Thermoform Packaging Market - Europe Size & Outlook 2020-2034

Europe Industrial Thermoform Packaging Market is segmented by Type (Rigid Thermoform Packaging, Flexible Thermoform Packaging, Semi-Rigid Thermoform Packaging, Vacuum Formed Packaging, Skin Packaging), Application (Food & Beverage, Pharmaceuticals, Consumer Goods, Electronics, Automotive, Industrial Components), Material Type (Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), Polystyrene (PS), Biodegradable Polymers, Polypropylene (PP)), Packaging Process (Vacuum Thermoforming, Pressure Thermoforming, Twin Sheet Thermoforming), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Industrial Thermoform Packaging market includes packaging products manufactured through plastic thermoforming processes tailored for industrial applications including food & beverage, pharmaceuticals, electronics, automotive, and consumer goods sectors. It covers rigid, flexible, semi-rigid, vacuum-formed, and skin packaging types using materials such as PET, PVC, and biodegradable polymers to meet functional and sustainability requirements.

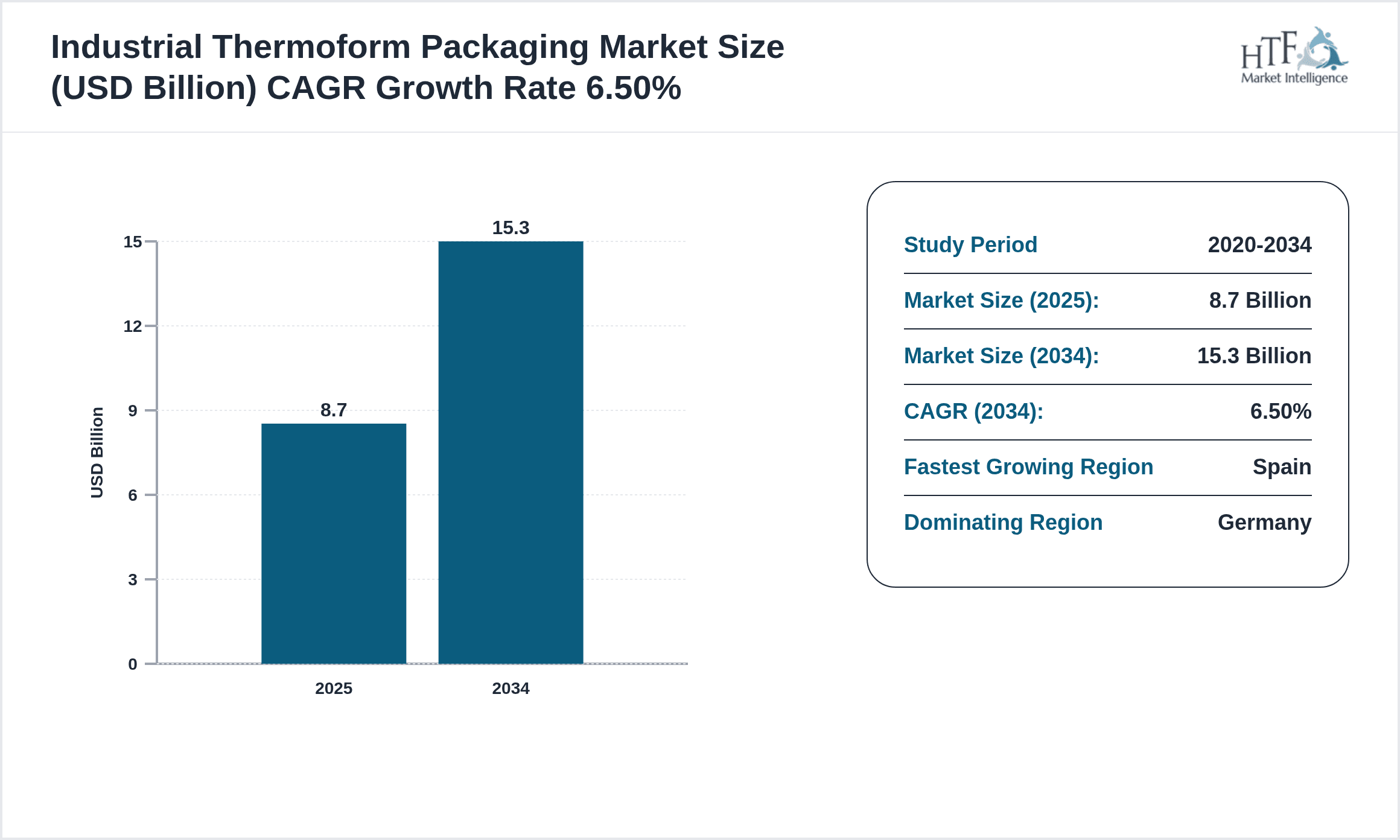

- •Market growth is driven by increasing demand for protective and sustainable packaging solutions across multiple industries, technological advancements in thermoforming processes, and stringent regulatory compliance in Europe aimed at reducing environmental impact. Germany leads the market in size while Spain exhibits the highest CAGR, fueled by expanding manufacturing and packaging activities.

- •This market offers strategic value to manufacturers, suppliers, and end-users by enabling product protection, enhancing shelf life, and optimizing supply chain efficiency. The transition towards eco-friendly materials and customization capabilities further underscore the market's importance in Europe's industrial packaging landscape.

Competitive Landscape

The Europe Industrial Thermoform Packaging market features a competitive environment characterized by established multinational corporations and agile regional players. Companies focus on innovation through advanced thermoforming technologies, sustainable material adoption, and tailored packaging solutions to differentiate themselves. Strategic partnerships and collaborations enhance product offerings and geographic reach. Market players adopt cost-effective manufacturing processes and invest in research and development to meet evolving regulatory standards and customer demands. Pricing strategies are influenced by raw material costs and environmental compliance. Distribution networks leverage both direct sales and third-party logistics providers to optimize market penetration. Barriers to entry include high capital investment, regulatory compliance complexity, and technology expertise requirements. The competitive dynamics are expected to intensify with rising demand for bio-based packaging and digital printing capabilities, driving continuous innovation and consolidation in the sector.

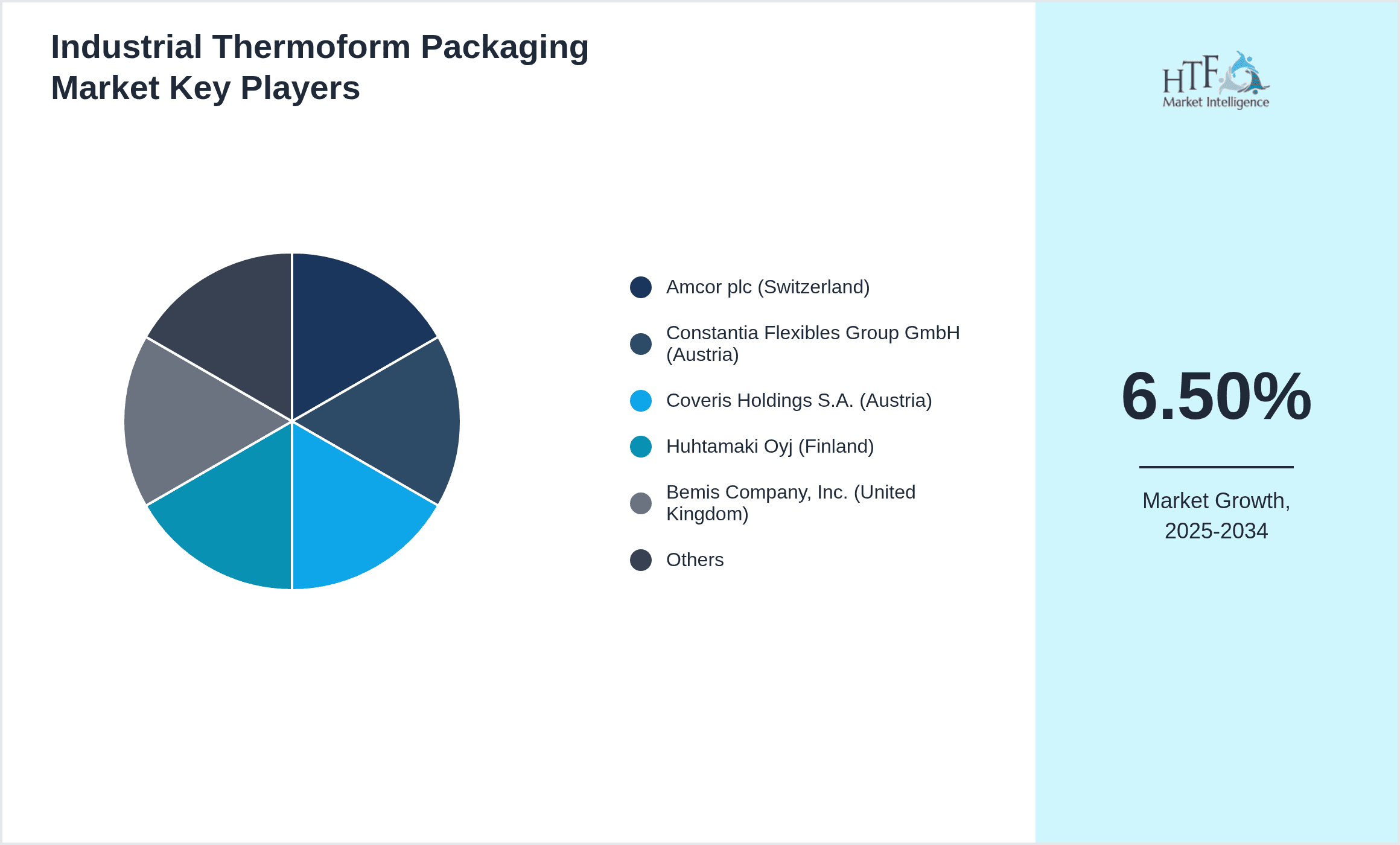

Leading Companies in Europe Industrial Thermoform Packaging Market

- •Amcor plc (Switzerland)

- •Constantia Flexibles Group GmbH (Austria)

- •Coveris Holdings S.A. (Austria)

- •Huhtamaki Oyj (Finland)

- •Bemis Company, Inc. (United Kingdom)

- •Mondi Group (United Kingdom/Austria)

- •Sealed Air Corporation (Ireland)

- •Berry Global, Inc. (United Kingdom)

- •LINPAC Group (United Kingdom)

- •Klöckner Pentaplast Group (Germany)

- •Coveris Rigid (Austria)

- •Schur Flexibles Group (Austria)

- •RPC Group Plc (United Kingdom)

- •Sigma Plastics Group (United Kingdom)

- •Plastopil Ltd. (Israel - European operations)

- •Ineos Styrolution Group GmbH (Germany)

- •Sidel Group (France)

- •Schoeller Allibert (Belgium)

- •Graham Packaging Company (Belgium)

- •Sonoco Products Company (Europe Headquarters - United Kingdom)

- •Constantia Teich GmbH & Co. KG (Germany)

- •Mold-Masters (Europe) Ltd. (United Kingdom)

- •Plastics Capital Plc (United Kingdom)

- •Tekni-Plex, Inc. (Europe) (United Kingdom)

- •DS Smith Plc (United Kingdom)

Market Breakdown

- •By Type

- ◦Rigid Thermoform Packaging

- ◦Flexible Thermoform Packaging

- ◦Semi-Rigid Thermoform Packaging

- ◦Vacuum Formed Packaging

- ◦Skin Packaging

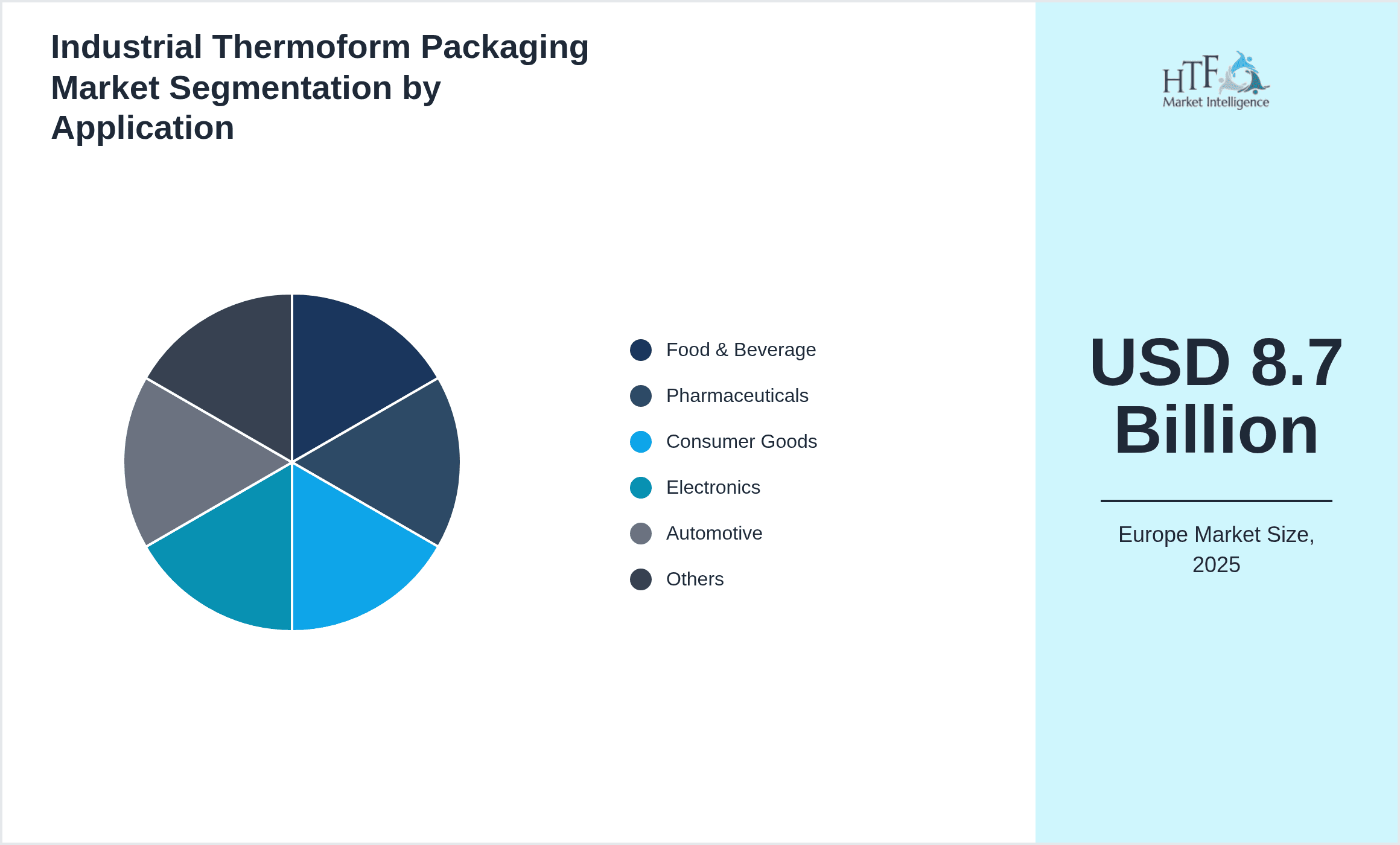

- •By Application

- ◦Food & Beverage

- ◦Pharmaceuticals

- ◦Consumer Goods

- ◦Electronics

- ◦Automotive

- ◦Industrial Components

- •By Material Type

- ◦Polyethylene Terephthalate (PET)

- ◦Polyvinyl Chloride (PVC)

- ◦Polystyrene (PS)

- ◦Biodegradable Polymers

- ◦Polypropylene (PP)

- •By Packaging Process

- ◦Vacuum Thermoforming

- ◦Pressure Thermoforming

- ◦Twin Sheet Thermoforming

Growth Dynamics

- •The Europe Industrial Thermoform Packaging market is propelled by increasing demand for sustainable packaging solutions driven by stringent EU environmental regulations targeting plastic waste reduction. Leading manufacturers invest heavily in biodegradable materials and recyclable packaging designs, which are gaining traction across food, pharmaceutical, and consumer goods sectors, fostering steady market expansion.

- •Technological advancements such as automation in thermoforming processes and integration of digital printing enable customized packaging at scale, enhancing product differentiation and consumer engagement. These innovations reduce production costs and improve turnaround times, increasing adoption among industrial clients seeking efficiency and sustainability.

- •Rising industrialization and urbanization in European countries like Spain and Poland create new opportunities for packaging demand in automotive and electronics industries. The growing e-commerce sector additionally stimulates the need for protective and lightweight thermoform packaging, benefiting market growth through 2034.

- •Government initiatives promoting circular economy principles and increased consumer awareness about plastic pollution further drive demand for eco-friendly thermoform packaging, encouraging manufacturers to adopt green technologies and materials that align with sustainability goals.

- •Supply chain optimizations and strategic partnerships between raw material suppliers and packaging manufacturers enhance material availability and cost-efficiency, contributing positively to market growth and competitive positioning in Europe.

- •Investment in R&D for improving barrier properties and durability of thermoform packaging supports the extension of shelf life for perishable goods, increasing market penetration in food and pharmaceutical applications.

- •The shift towards lightweight packaging to reduce transportation costs and carbon footprint aligns with broader sustainability trends, positioning thermoform packaging as a preferred solution among European industries.

Market Trends

- •Increasing adoption of bio-based and compostable polymers in thermoform packaging reflects a major trend driven by environmental regulations and consumer demand for sustainable products. Companies are innovating to replace conventional plastics with renewable materials without compromising packaging performance.

- •Digital printing technology integration enables high-quality, customizable designs on thermoform packaging, enhancing brand visibility and consumer appeal. This trend is gaining momentum in Europe as manufacturers seek differentiation in competitive markets.

- •The rise of active and intelligent packaging solutions incorporating sensors and freshness indicators within thermoformed packs improves product safety and quality monitoring, particularly in pharmaceuticals and food sectors.

- •Consolidation through strategic mergers and acquisitions among packaging companies is reshaping the competitive landscape to achieve economies of scale, expand product portfolios, and enhance geographic reach within Europe.

- •Sustainability certifications and eco-labeling are increasingly influencing procurement decisions, pushing manufacturers to comply with eco-friendly standards and transparent supply chain practices.

- •Consumer preference for convenience packaging, such as easy-open and resealable thermoform packs, is driving product innovation and adoption across food, beverage, and personal care segments.

- •The integration of Industry 4.0 technologies including IoT and AI in thermoforming manufacturing processes enhances production efficiency, quality control, and predictive maintenance capabilities.

Market Opportunities

- •Expanding demand for sustainable packaging in emerging European markets such as Eastern Europe presents significant growth potential for innovative thermoform packaging solutions that comply with environmental policies and consumer expectations.

- •Development of multi-functional packaging incorporating barrier, antimicrobial, and tamper-evident features opens new avenues in pharmaceuticals and food sectors, addressing safety and shelf life challenges.

- •Investment in automated and flexible manufacturing lines enables customization at scale, allowing manufacturers to cater to niche industrial applications and evolving market needs effectively.

- •Geographical expansion into underserved markets within Europe through strategic partnerships and localized production facilities offers a competitive edge and cost advantages.

- •Leveraging digital printing and smart packaging technologies enhances product differentiation and consumer engagement, facilitating premium pricing and brand loyalty.

- •Collaborations between raw material innovators and thermoform packaging companies to develop bio-based polymers with improved properties represent a promising investment opportunity.

- •Growing e-commerce penetration drives demand for protective and light-weight thermoform packaging solutions, creating opportunities for product innovation and market diversification.

Market Challenges

- •Volatility in raw material prices, particularly petrochemical-based plastics, poses cost pressure on manufacturers, affecting profit margins and pricing strategies in the European market.

- •Compliance with stringent European Union regulations on plastic usage and waste management requires continuous investment in R&D and process adaptation, representing a significant barrier for smaller players.

- •Challenges in recycling and end-of-life management for thermoform packaging materials hinder full adoption of sustainable packaging, necessitating advancements in circular economy solutions.

- •High capital expenditure for advanced thermoforming equipment and automation limits entry and expansion opportunities for new market entrants and SMEs.

- •Balancing performance requirements with sustainability goals remains complex, as bio-based materials may not always match the barrier and durability characteristics of conventional plastics.

- •Supply chain disruptions due to geopolitical factors and pandemic-related constraints impact raw material availability and logistics, affecting timely production and delivery.

- •Consumer skepticism towards plastic packaging despite sustainability claims challenges market acceptance, requiring enhanced transparency and education efforts.

Regulatory Framework

- •The EU Single-Use Plastics Directive, implemented between 2019 and 2025, mandates reduction and replacement of specific single-use plastic products, compelling thermoform packaging manufacturers to innovate sustainable alternatives and improve recyclability.

- •REACH regulation enforces stringent chemical safety assessments and restrictions on hazardous substances in packaging materials, impacting raw material selection and manufacturing processes within Europe.

- •Extended Producer Responsibility (EPR) schemes require manufacturers to manage the end-of-life treatment of packaging waste, stimulating circular economy initiatives and eco-design adoption in thermoform packaging.

- •European Green Deal targets achieving climate neutrality by 2050, influencing packaging regulations with incentives for sustainable product design, material innovation, and waste reduction practices.

- •National regulations across European countries impose varying requirements on packaging labeling, waste collection, and recycling targets, requiring companies to customize compliance strategies regionally.

Market Intelligence

- •15th March 2025, Amcor plc announced the launch of a new line of fully recyclable rigid thermoform packaging solutions designed specifically for the European food industry. These products leverage advanced PET materials with enhanced barrier properties to extend shelf life while meeting EU sustainability mandates. The initiative aims to reduce plastic waste and improve supply chain efficiency across Europe. Amcor plans to expand production capacity at its Germany facilities to meet growing demand. Source: Amcor Official Press Release

- •2nd June 2025, Huhtamaki Oyj introduced smart thermoform packaging integrated with freshness sensors targeting the pharmaceutical sector in Europe. This innovation enables real-time monitoring of product integrity and tamper evidence, enhancing safety standards and regulatory compliance. The technology combines flexible thermoforming with IoT capabilities to support cold chain logistics and patient safety. Huhtamaki expects significant market adoption in countries like France and the UK. Source: Huhtamaki Corporate News

- •10th September 2025, Mondi Group completed the acquisition of a regional thermoform packaging manufacturer in Spain to strengthen its foothold in Southern Europe. This strategic move expands Mondi’s product portfolio in sustainable packaging and supports its long-term growth strategy aligned with circular economy principles. The acquisition enables enhanced local production capabilities and faster delivery to key industrial clients. Source: Mondi Group Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Spain is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.7 Billion |

| Forecast Year Market Size | USD 15.3 Billion |

| CAGR | 6.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.3% |

| Scope of Report | Market is segmented by Type (Rigid Thermoform Packaging, Flexible Thermoform Packaging, Semi-Rigid Thermoform Packaging, Vacuum Formed Packaging, Skin Packaging), Application (Food & Beverage, Pharmaceuticals, Consumer Goods, Electronics, Automotive, Industrial Components), Material Type (Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), Polystyrene (PS), Biodegradable Polymers, Polypropylene (PP)), Packaging Process (Vacuum Thermoforming, Pressure Thermoforming, Twin Sheet Thermoforming) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Amcor plc (Switzerland), Constantia Flexibles Group GmbH (Austria), Coveris Holdings S.A. (Austria), Huhtamaki Oyj (Finland), Bemis Company, Inc. (United Kingdom), Mondi Group (United Kingdom/Austria), Sealed Air Corporation (Ireland), Berry Global, Inc. (United Kingdom), LINPAC Group (United Kingdom), Klöckner Pentaplast Group (Germany), Coveris Rigid (Austria), Schur Flexibles Group (Austria), RPC Group Plc (United Kingdom), Sigma Plastics Group (United Kingdom), Plastopil Ltd. (Israel - European operations), Ineos Styrolution Group GmbH (Germany), Sidel Group (France), Schoeller Allibert (Belgium), Graham Packaging Company (Belgium), Sonoco Products Company (Europe Headquarters - United Kingdom), Constantia Teich GmbH & Co. KG (Germany), Mold-Masters (Europe) Ltd. (United Kingdom), Plastics Capital Plc (United Kingdom), Tekni-Plex, Inc. (Europe) (United Kingdom), DS Smith Plc (United Kingdom) |

Europe Industrial Thermoform Packaging Market - Europe Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.