Global High Speed Data Acquisition System for Automotive Market Size, Growth & Revenue 2024-2034

Global High Speed Data Acquisition System for Automotive Market is segmented by Type (Analog Data Acquisition Systems, Digital Data Acquisition Systems, Wireless Data Acquisition Systems, Mixed Signal Data Acquisition Systems, Modular Data Acquisition Systems), Application (Engine Testing, Vehicle Dynamics, Emissions Testing, Safety Testing, Autonomous Vehicle Development), End User (Automotive OEMs, Testing Laboratories, Research & Development Centers, Aftermarket Service Providers), Technology (Real-Time Data Processing, Wireless Data Transmission, Cloud-Based Data Storage, AI-Enabled Analytics), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global High Speed Data Acquisition System for Automotive market includes sophisticated data capture systems designed to collect high-frequency signals from vehicle components and testing setups for real-time analytics and optimization, covering multiple product types and applications.

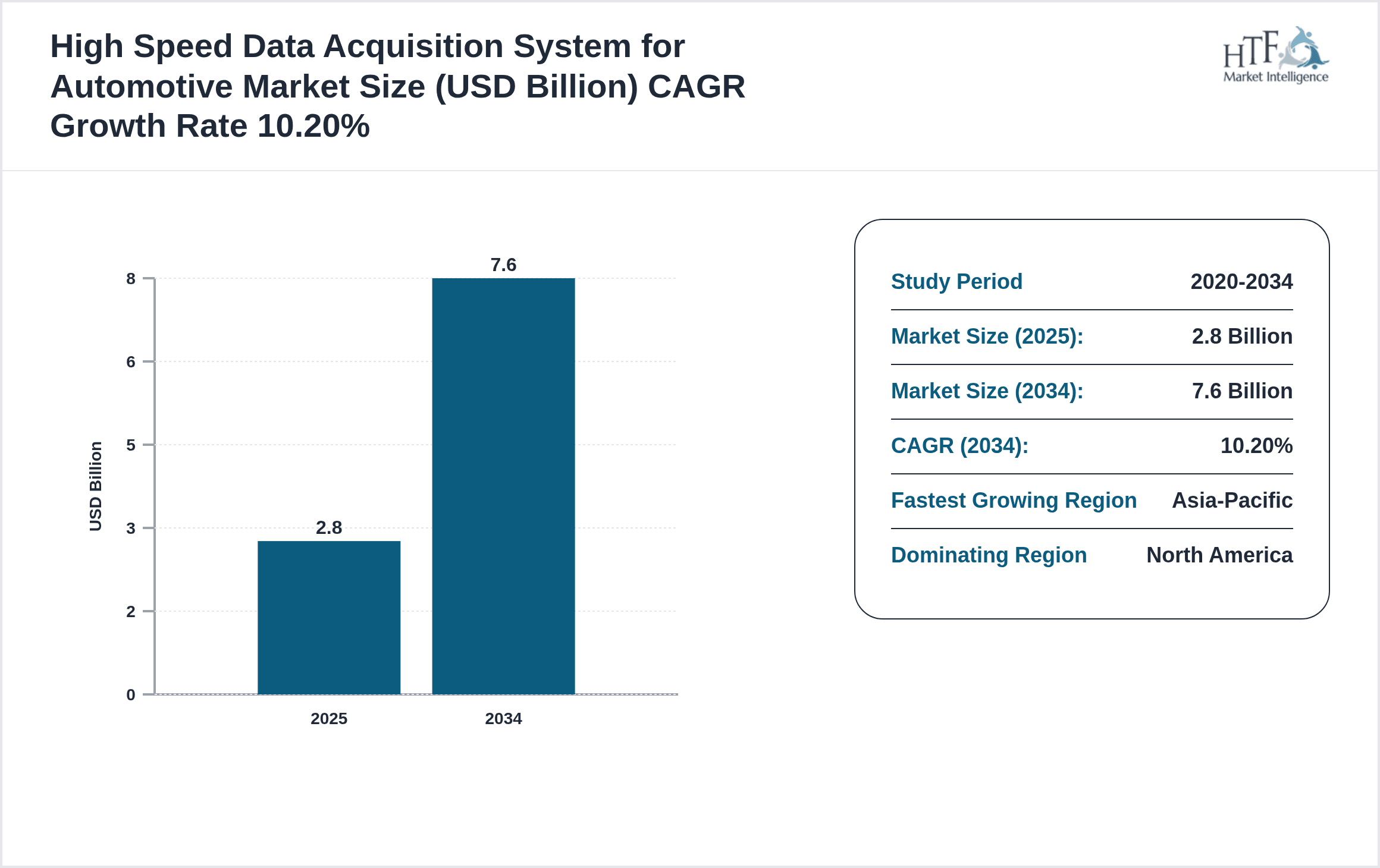

- •Market growth is propelled by stringent vehicle safety and emissions regulations, the rise of autonomous vehicle technologies, and innovations in wireless and digital data acquisition solutions, with the market expected to reach USD 7.6 Billion by 2034.

- •These systems offer strategic value by enabling automotive manufacturers and testing entities to enhance product reliability, comply with regulatory mandates, and accelerate innovation cycles, fostering competitive advantages in a dynamic automotive landscape.

Competitive Landscape

The competitive environment of the Global High Speed Data Acquisition System for Automotive market is marked by intense rivalry among established multinational corporations and emerging innovators. Companies focus on technology differentiation through advanced wireless capabilities, modular designs, and integration with AI-driven analytics. Strategic partnerships and continuous R&D investment are pivotal for maintaining market position, while pricing strategies and global distribution networks influence competitive dynamics. Market entrants face high barriers due to technological complexity and regulatory compliance requirements. Innovation ecosystems, including collaborations with automotive OEMs and research institutions, further shape competitive advantage. Regional market players leverage local expertise to capture specific opportunities, intensifying competition across North America, Europe, and Asia-Pacific. Future competition will likely revolve around enhancing system speed, accuracy, and data security, alongside expanding application breadth into autonomous and electric vehicle testing domains.

Leading Companies in High Speed Data Acquisition System for Automotive Market

- •National Instruments Corporation (United States)

- •Keysight Technologies, Inc. (United States)

- •HBM Test and Measurement (Germany)

- •Kistler Group (Switzerland)

- •DEWESoft (Slovenia)

- •HIOKI E.E. Corporation (Japan)

- •AVL List GmbH (Austria)

- •AMETEK, Inc. (United States)

- •MTS Systems Corporation (United States)

- •Dewesoft d.o.o. (Slovenia)

- •AstroNova, Inc. (United States)

- •Spectris plc (United Kingdom)

- •Yokogawa Electric Corporation (Japan)

- •Rohde & Schwarz GmbH & Co KG (Germany)

- •TE Connectivity Ltd. (Switzerland)

- •LabVIEW (United States)

- •FLIR Systems, Inc. (United States)

- •Tektronix, Inc. (United States)

- •Pico Technology (United Kingdom)

- •Honeywell International Inc. (United States)

- •LXI Consortium (United States)

- •ZETLAB (Russia)

- •HBM Americas, Inc. (United States)

- •Dataforth Corporation (United States)

- •Keysight Technologies India Pvt Ltd (India)

Market Breakdown

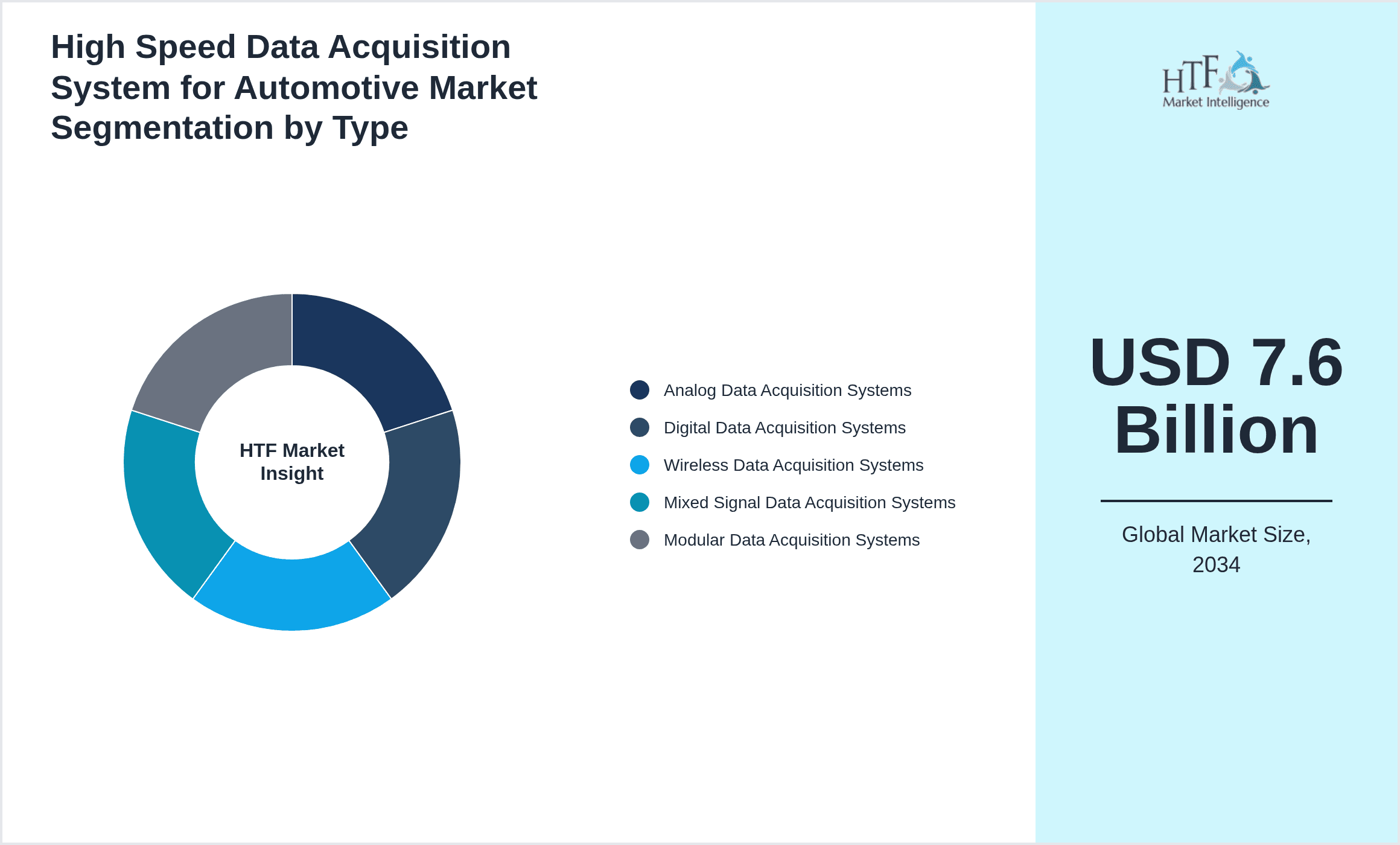

- •By Type

- ◦Analog Data Acquisition Systems

- ◦Digital Data Acquisition Systems

- ◦Wireless Data Acquisition Systems

- ◦Mixed Signal Data Acquisition Systems

- ◦Modular Data Acquisition Systems

- •By Application

- ◦Engine Testing

- ◦Vehicle Dynamics

- ◦Emissions Testing

- ◦Safety Testing

- ◦Autonomous Vehicle Development

- •By End User

- ◦Automotive OEMs

- ◦Testing Laboratories

- ◦Research & Development Centers

- ◦Aftermarket Service Providers

- •By Technology

- ◦Real-Time Data Processing

- ◦Wireless Data Transmission

- ◦Cloud-Based Data Storage

- ◦AI-Enabled Analytics

Growth Drivers

The market's growth is primarily driven by escalating automotive safety and emission regulations worldwide, compelling manufacturers to adopt high speed data acquisition systems for precise testing and compliance verification. Increasing demand for autonomous and electric vehicles necessitates advanced data capture solutions to support complex sensor networks and real-time analytics, boosting system adoption. Technological advancements in wireless and modular data acquisition systems facilitate flexible and scalable testing environments, enhancing market appeal. Additionally, the integration of AI and machine learning in data processing enables predictive maintenance and performance optimization, attracting investment from OEMs and testing labs. Rising vehicle complexity and the need for improved diagnostic accuracy further accelerate demand, establishing these systems as critical for innovation and regulatory adherence in the automotive sector.

Market Trends

The market is witnessing a notable trend towards wireless data acquisition systems, driven by the need for reduced cabling and enhanced mobility in vehicle testing scenarios. Integration with cloud-based platforms enables remote data access and collaborative analysis, improving efficiency. The growing adoption of AI and machine learning for real-time data interpretation is transforming testing methodologies, facilitating faster decision-making. Modular system architectures allow customization to specific testing requirements, reflecting a shift towards flexible solutions. Additionally, the emphasis on emissions testing and environmental compliance has intensified the demand for high precision and high frequency data acquisition capabilities, propelling innovation and market expansion.

Market Opportunities

Emerging opportunities include expansion into electric and autonomous vehicle testing segments, where complex sensor data necessitates advanced acquisition systems. The rise of connected vehicles provides potential for integrated data solutions that combine acquisition with telematics and diagnostics. Growth in developing regions, particularly Asia-Pacific, offers untapped markets due to increasing automotive production and regulatory enforcement. Innovations in AI-driven analytics and cloud computing present avenues for product differentiation and new service models. Collaborations with automotive OEMs and technology providers can accelerate adoption, while aftermarket applications for vehicle health monitoring represent additional growth prospects.

Market Challenges

Challenges include high initial investment costs for advanced data acquisition systems, limiting adoption among smaller manufacturers and testing entities. Complex integration with existing vehicle systems and software platforms can delay deployment and increase operational costs. Data security and privacy concerns arise with wireless and cloud-based transmission, requiring robust safeguards. Rapid technological evolution demands continuous R&D, imposing pressure on companies to innovate and maintain competitiveness. Regulatory variations across regions complicate compliance strategies and product standardization. Furthermore, shortage of skilled professionals capable of managing sophisticated data systems poses an operational hurdle, potentially slowing market growth.

Regulatory Framework

Recent regulatory developments from 2020 to 2024 have intensified emission standards and safety testing protocols globally, necessitating precise and high frequency data acquisition capabilities. Regions such as North America and Europe have introduced stricter vehicle emissions limits and mandatory autonomous vehicle safety validations, directly impacting system requirements. Compliance mandates now demand real-time data capture accuracy and traceability, driving adoption of advanced acquisition technologies. Additionally, data protection regulations influence wireless data handling and storage practices. Governments have also initiated incentives for electric and autonomous vehicle testing infrastructure, indirectly supporting market growth. These evolving regulations necessitate continuous updates in system design and functionality to maintain compliance and market relevance.

Industry Insights

Recent industry developments reflect increasing emphasis on integrating AI capabilities within data acquisition systems to enhance real-time analytics and predictive diagnostics. In June 2023, National Instruments Corporation launched a new modular digital data acquisition system tailored for autonomous vehicle testing, featuring enhanced wireless connectivity and cloud integration, significantly improving data processing speeds and flexibility. Similarly, in November 2022, Keysight Technologies introduced a next-generation high-frequency analog data acquisition platform with advanced signal integrity and multi-channel synchronization, designed to meet stringent emission testing requirements. These innovations underscore the market’s trajectory towards smarter, more connected testing solutions, addressing the complex demands of modern automotive development and regulatory compliance.

Mergers & Acquisitions

- •In March 2023, Keysight Technologies completed the acquisition of a European-based wireless data acquisition technology firm, enhancing its portfolio with cutting-edge wireless modules designed for automotive applications. This strategic move strengthens Keysight’s position in the high speed automotive data acquisition segment, enabling expanded offerings in autonomous vehicle testing and emissions monitoring. The acquisition facilitates integration of advanced wireless capabilities and cloud analytics, positioning the company for growth in emerging markets. It also broadens their geographic footprint across Europe and Asia-Pacific, supporting global expansion strategies.

- •In September 2022, National Instruments Corporation merged with a leading AI analytics startup specializing in real-time data processing for automotive testing. This merger combines National Instruments’ hardware expertise with advanced AI-driven software solutions, fostering innovation in predictive maintenance and autonomous vehicle development. The collaboration accelerates product development cycles and enhances system intelligence, providing a competitive edge in the rapidly evolving automotive testing market. The combined entity gains a stronger foothold in North America and Asia-Pacific regions, aligning with increasing demand for sophisticated data acquisition and analytics platforms.

Recent Industry News

- •15th June 2024, National Instruments Corporation unveiled an advanced wireless modular data acquisition system designed for electric and autonomous vehicle testing. Featuring enhanced cloud integration and AI-powered analytics, this product aims to streamline real-time data processing and improve testing accuracy. The launch marks a strategic expansion into emerging vehicle segments, highlighting National Instruments’ commitment to innovation and market leadership. Source: National Instruments Official Press Release

- •22nd November 2023, Keysight Technologies introduced a high-frequency analog data acquisition platform optimized for stringent emissions testing standards. The platform integrates multi-channel synchronization and advanced signal integrity features, enabling automotive manufacturers to comply efficiently with evolving regulations. Keysight’s innovation addresses critical market needs for precision and regulatory compliance in global automotive testing. Source: Keysight Technologies Press Statement

- •10th March 2024, HBM Test and Measurement announced a strategic partnership with a leading automotive OEM to co-develop next-generation data acquisition systems focusing on vehicle dynamics and safety testing. This collaboration aims to accelerate development cycles and enhance testing capabilities through integrated hardware-software solutions. Source: HBM Corporate Announcement

- •5th July 2022, DEWESoft launched a cloud-based data acquisition and analytics platform tailored for autonomous vehicle development. The solution offers scalable data storage and real-time AI analytics, facilitating faster decision-making and predictive diagnostics in automotive R&D. This launch underscores DEWESoft’s focus on digital transformation within the automotive testing landscape. Source: DEWESoft Official News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.8 Billion |

| Forecast Year Market Size | USD 7.6 Billion |

| CAGR | 10.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Scope of Report | Market is segmented by Type (Analog Data Acquisition Systems, Digital Data Acquisition Systems, Wireless Data Acquisition Systems, Mixed Signal Data Acquisition Systems, Modular Data Acquisition Systems), Application (Engine Testing, Vehicle Dynamics, Emissions Testing, Safety Testing, Autonomous Vehicle Development), End User (Automotive OEMs, Testing Laboratories, Research & Development Centers, Aftermarket Service Providers), Technology (Real-Time Data Processing, Wireless Data Transmission, Cloud-Based Data Storage, AI-Enabled Analytics) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | National Instruments Corporation (United States), Keysight Technologies, Inc. (United States), HBM Test and Measurement (Germany), Kistler Group (Switzerland), DEWESoft (Slovenia), HIOKI E.E. Corporation (Japan), AVL List GmbH (Austria), AMETEK, Inc. (United States), MTS Systems Corporation (United States), Dewesoft d.o.o. (Slovenia), AstroNova, Inc. (United States), Spectris plc (United Kingdom), Yokogawa Electric Corporation (Japan), Rohde & Schwarz GmbH & Co KG (Germany), TE Connectivity Ltd. (Switzerland), LabVIEW (United States), FLIR Systems, Inc. (United States), Tektronix, Inc. (United States), Pico Technology (United Kingdom), Honeywell International Inc. (United States), LXI Consortium (United States), ZETLAB (Russia), HBM Americas, Inc. (United States), Dataforth Corporation (United States), Keysight Technologies India Pvt Ltd (India) |

Global High Speed Data Acquisition System for Automotive Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.