North America Natural Wine Cork Stoppers Market Size, Growth & Revenue 2024-2034

North America Natural Wine Cork Stoppers Market is segmented by Type (Natural Cork Stoppers, Agglomerated Cork Stoppers, Technical Cork Stoppers, Synthetic Cork Stoppers, Composite Cork Stoppers), Application (Wine Bottling, Craft Beverages, Premium Wines, Organic Wines, Others), Distribution Channel (Direct Sales, Distributors, Online Retail, Wholesale Suppliers), End User (Winery, Beverage Manufacturers, Retailers, Exporters), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Natural Wine Cork Stoppers Market involves production and distribution of natural cork closures primarily used in sealing wine bottles, including various cork types and applications across the region.

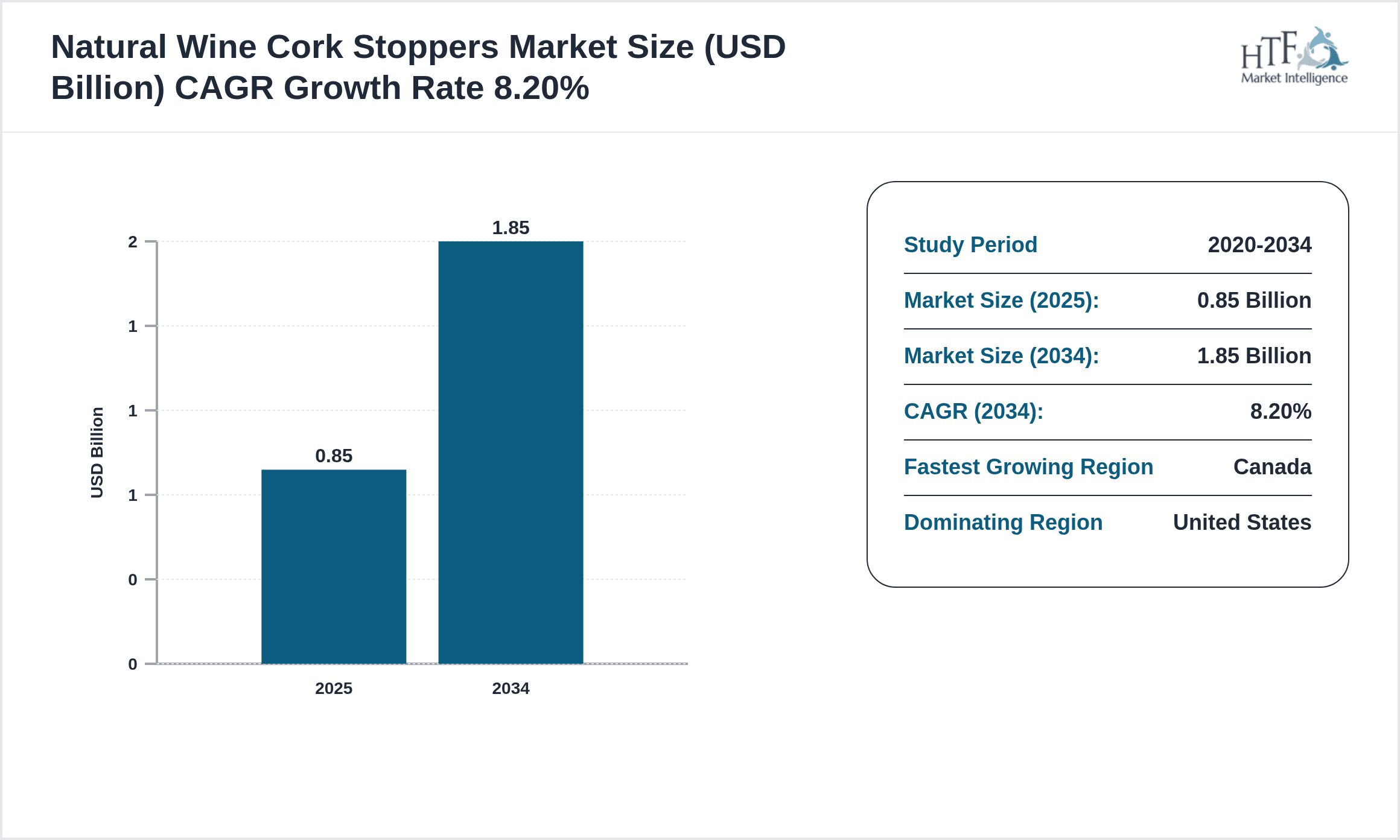

- •The market is projected to grow from USD 0.85 Billion in 2025 to USD 1.85 Billion by 2034, reflecting a CAGR of 8.2%, driven by rising demand for premium and organic wines in the United States and Canada.

- •Sustainability initiatives and consumer preference for natural sealing solutions enhance the strategic importance of cork stoppers, supporting the growth of wine producers and packaging companies across North America.

Competitive Landscape

Competition in the North America Natural Wine Cork Stoppers Market is characterized by a blend of traditional cork manufacturers and innovative entrants focusing on synthetic alternatives. Market leaders emphasize product quality, sustainability, and customization to differentiate themselves. Innovation drives include improved cork treatment technologies and eco-friendly production methods. Rivalry remains intense with companies investing in advanced logistics and partnerships to enhance distribution efficiency. Strategic collaborations with wineries and beverage producers further consolidate market positions. Pricing strategies balance cost competitiveness with quality assurance. Regional competition is influenced by proximity to cork raw material sources and access to premium wine markets, fostering a dynamic landscape emphasizing product innovation, environmental responsibility, and customer-centric approaches to maintain and expand market share.

Leading Companies in North America Natural Wine Cork Stoppers Market

- •Amorim Cork North America (United States)

- •Nomacorc (United States)

- •Cork Supply USA (United States)

- •Oeneo Group (United States)

- •DIAM Bouchage (Canada)

- •Jelinek Cork Group (Canada)

- •Guala Closures North America (United States)

- •M.A. Silva USA (United States)

- •LZ Cork (United States)

- •Corker (United States)

- •Cork Quality Council (United States)

- •Cork Supply Group (United States)

- •Vivari Group (United States)

- •TCA Cork Solutions (Canada)

- •Alfred C. Toepfer International (United States)

- •Innovacork (Canada)

- •Oregon Cork Co. (United States)

- •Sierra Pacific Cork (United States)

- •Canadian Cork Solutions (Canada)

- •EcoCork Innovations (United States)

Market Breakdown

- •By Type

- ◦Natural Cork Stoppers

- ◦Agglomerated Cork Stoppers

- ◦Technical Cork Stoppers

- ◦Synthetic Cork Stoppers

- ◦Composite Cork Stoppers

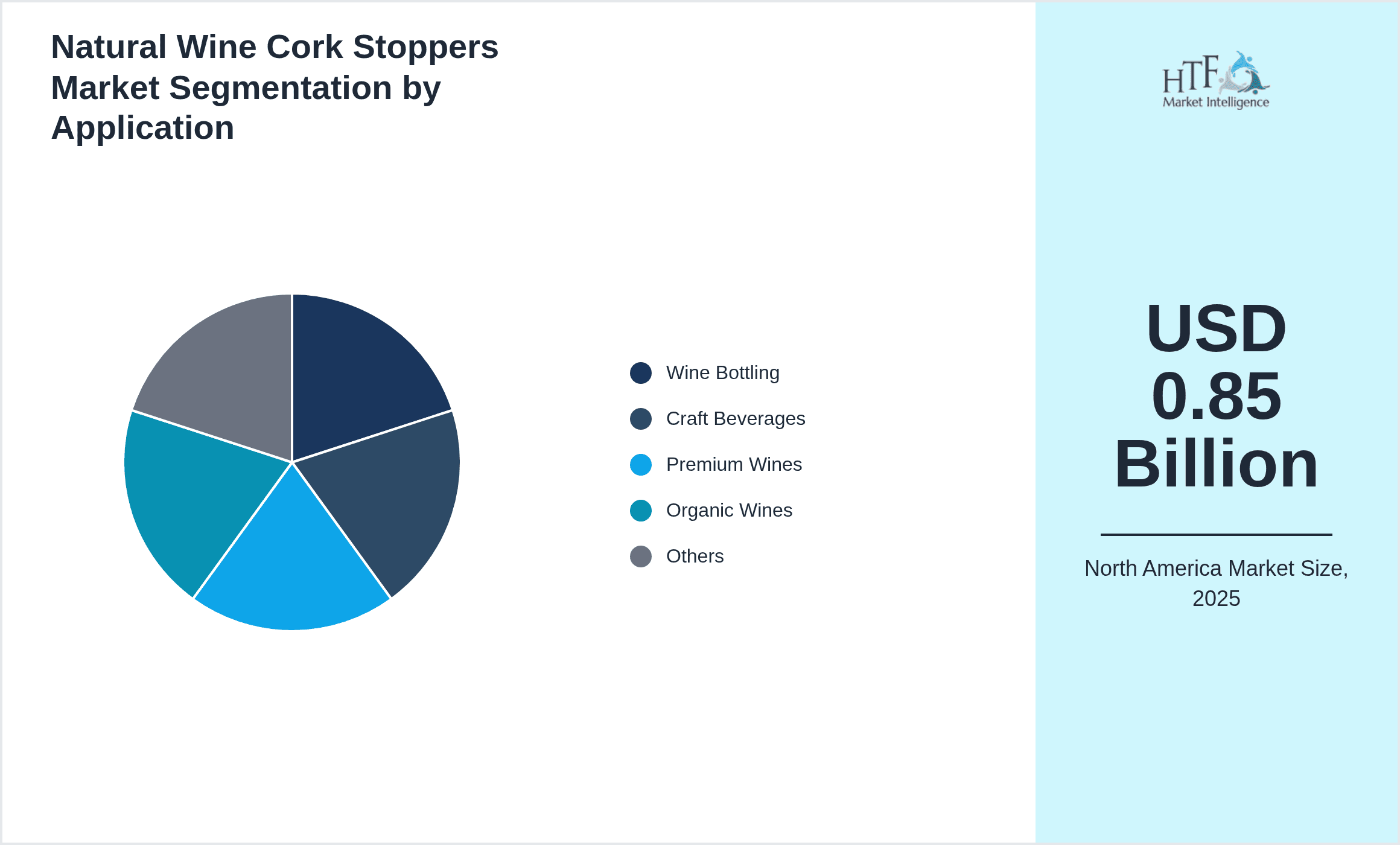

- •By Application

- ◦Wine Bottling

- ◦Craft Beverages

- ◦Premium Wines

- ◦Organic Wines

- ◦Others

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Retail

- ◦Wholesale Suppliers

- •By End User

- ◦Winery

- ◦Beverage Manufacturers

- ◦Retailers

- ◦Exporters

Growth Drivers

The North America market for natural wine cork stoppers is propelled by rising consumer demand for premium and organic wines, which prioritize natural sealing solutions to preserve authenticity and flavor. The increasing wine consumption across the United States and Canada supports growth. Additionally, the sustainability movement strongly favors natural cork due to its renewable and biodegradable nature, attracting eco-conscious wineries and consumers. Technological advancements in cork harvesting and treatment enhance durability and reduce defects, boosting product reliability. Market players’ investments in promoting natural cork benefits and collaborations with wine producers further stimulate demand. The growth is also supported by expanding craft beverage segments adopting natural cork stoppers to align with artisanal branding and quality preservation.

Market Trends

A significant trend in the North America natural wine cork stoppers market is the rise in adoption of synthetic corks, driven by concerns over cork taint and consistent quality. Wineries increasingly blend natural and synthetic options to balance tradition and performance. Furthermore, there is a growing emphasis on sustainable sourcing, with manufacturers investing in environmentally friendly harvesting and recycling programs. Digitalization in supply chain management improves traceability and quality control. The craft and organic wine segments are rapidly expanding, pushing demand for customized and premium cork stopper solutions. Companies are also innovating in cork treatments to enhance oxygen permeability control, supporting wine aging requirements. These trends collectively shape the evolving market landscape.

Market Restraints

Despite growth opportunities, the market faces challenges such as the higher cost of natural cork stoppers compared to synthetic alternatives, limiting adoption among budget-conscious producers. Variability in natural cork quality leads to concerns over cork taint, which affects wine flavor and shelf life, causing some wineries to prefer synthetic options. Supply chain disruptions and limitations in cork oak harvesting regions constrain raw material availability. Additionally, increasing competition from alternative closures like screw caps and synthetic corks impedes market share growth. Regulatory complexities concerning environmental standards and import-export tariffs add operational hurdles. These restraints require manufacturers to innovate and optimize cost-efficiency to remain competitive in North America.

Market Opportunities

The North America natural wine cork stoppers market holds significant opportunities in expanding organic and craft wine segments, as these producers prioritize sustainable and authentic packaging. Innovations in cork treatment technologies offer avenues to address quality inconsistencies and cork taint, attracting more wineries to natural corks. The rising consumer preference for eco-friendly products creates demand for certified sustainable cork stopper solutions. Geographic expansion into emerging wine-producing states in the U.S. and increasing imports from Canada and Mexico present growth potential. Strategic partnerships between cork manufacturers and wineries can enhance product customization and brand differentiation. Moreover, recycling initiatives and circular economy integration offer new business models and regulatory compliance advantages.

Market Challenges

Key challenges in the North America natural wine cork stoppers market include managing the supply-demand imbalance due to limited cork oak forests, primarily located outside North America, resulting in dependency on imports. The threat of cork taint and quality inconsistencies undermines consumer confidence and winery adoption. Additionally, intense competition from alternative closure technologies, such as screw caps and synthetic corks, pressures price points and market share. Regulatory compliance related to environmental standards and import tariffs complicates cross-border trade. Moreover, fluctuating raw material costs impact profitability for manufacturers. Addressing these challenges requires innovation in product quality, supply chain resilience, and strategic market positioning to sustain growth.

Regulatory Framework

Between 2020 and 2025, North America has seen enhanced regulatory focus on sustainable packaging and environmental impact reduction affecting natural wine cork stoppers. The U.S. Environmental Protection Agency and Canadian Environmental Regulations have introduced guidelines promoting biodegradable materials and responsible sourcing. Import regulations have tightened, requiring certifications on cork origin and treatment processes to prevent pest contamination. Additionally, labeling requirements mandate disclosure of closure materials to ensure consumer transparency. These regulations push manufacturers toward eco-certifications and sustainable harvesting practices, influencing market dynamics and compliance costs. Ongoing updates anticipate stricter sustainability and trade policies, encouraging innovation and greener supply chains in the cork stopper industry.

Market Intelligence

- •On 15th March 2024, Amorim Cork North America launched an innovative natural cork stopper line with enhanced oxygen control technology, targeting premium and organic wine producers to improve aging processes and flavor preservation. The product integrates sustainability with performance, meeting rising market demand for high-quality closures. This launch strengthens Amorim’s position in the North American market and supports eco-conscious branding strategies.

- •In October 2023, Nomacorc introduced a new range of eco-friendly synthetic cork stoppers made from renewable materials, designed to offer consistent quality and reduce cork taint risk. This initiative aligns with growing consumer preferences for sustainable alternatives and expands Nomacorc’s footprint in the craft and organic beverage sectors across North America.

Mergers & Acquisitions

- •In July 2024, Cork Supply USA completed the acquisition of EcoCork Innovations, a move aimed at enhancing sustainable product offerings and expanding its portfolio in the natural cork segment. This acquisition strengthens Cork Supply USA’s market presence in the United States and supports its strategic focus on eco-friendly solutions, leveraging EcoCork’s proprietary recycling technologies to meet increasing demand for sustainable wine corks.

- •In January 2025, Jelinek Cork Group acquired a regional synthetic cork manufacturer in Canada, facilitating entry into the growing synthetic cork market and diversifying product lines. This strategic acquisition enables Jelinek to better serve craft and organic beverage producers with innovative closure options, enhancing competitive positioning across North America.

Recent Industry News

- •On 10th February 2025, M.A. Silva USA announced a strategic partnership with a leading organic winery in California to supply 100% natural cork stoppers for its premium wine line. This collaboration highlights the growing preference for sustainable packaging among quality-focused producers and supports M.A. Silva’s expansion in the organic wine segment. Source: Official Company Website

- •In April 2025, DIAM Bouchage launched an advanced cork stopper with patented treatment technology that eliminates cork taint risk, targeting North American wineries focused on high-end and aged wines. The product release is expected to disrupt traditional cork markets by combining natural cork benefits with synthetic closure performance. Source: Industry Press Release

- •On 20th June 2025, Guala Closures North America expanded its manufacturing facility in Mexico to increase production capacity for natural cork stoppers and synthetic alternatives, addressing rising demand from U.S. and Canadian wineries. This expansion reflects the company’s commitment to supply chain resilience and sustainability. Source: Corporate Announcement

- •In August 2025, Amorim Cork North America introduced a cloud-based supply chain tracking system for cork products, enhancing transparency and quality assurance for North American wineries. The initiative supports industry digitalization trends and strengthens customer trust in cork sourcing and treatment processes. Source: Industry News Portal

Market Statistics

- •CAGR by 2034: 8.2%

- •Market Size by 2034: USD 1.85 Billion

- •Market Size in 2025: USD 0.85 Billion

- •Dominating Type: Natural Cork Stoppers

- •Next-following Type: Synthetic Cork Stoppers

- •Dominating Application: Wine Bottling

- •Next-following Application: Premium Wines

- •Dominating Region: United States

- •Second-leading Region with Highest Growth Rate: Canada

- •Dominating Country: United States

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Natural Cork Stoppers: 65%

- ◦Synthetic Cork Stoppers: 20%

- •Market Share (%) of Dominating vs Followed Application

- ◦Wine Bottling: 60%

- ◦Premium Wines: 25%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Natural Cork Stoppers: 7.5%

- ◦Synthetic Cork Stoppers: 11.0%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Wine Bottling: 7.8%

- ◦Premium Wines: 9.5%

Top 5 Global Players

- •Amorim Cork North America (United States)

- •Nomacorc (United States)

- •Cork Supply USA (United States)

- •DIAM Bouchage (Canada)

- •Jelinek Cork Group (Canada)

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 1.85 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Type (Natural Cork Stoppers, Agglomerated Cork Stoppers, Technical Cork Stoppers, Synthetic Cork Stoppers, Composite Cork Stoppers), Application (Wine Bottling, Craft Beverages, Premium Wines, Organic Wines, Others), Distribution Channel (Direct Sales, Distributors, Online Retail, Wholesale Suppliers), End User (Winery, Beverage Manufacturers, Retailers, Exporters) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Amorim Cork North America (United States), Nomacorc (United States), Cork Supply USA (United States), Oeneo Group (United States), DIAM Bouchage (Canada) |

North America Natural Wine Cork Stoppers Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.