Japan Satellite Vehicle Station Market - Japan Size & Outlook 2025-2034

Japan Satellite Vehicle Station Market is segmented by Application (Navigation, Tracking, Telemetry, Communication, Data Relay), Type (Mobile Satellite Vehicle Station, Fixed Satellite Vehicle Station, Transportable Satellite Vehicle Station, Maritime Satellite Vehicle Station, Aerospace Satellite Vehicle Station), and Geography (Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu)

Pricing

Report Overview

Executive Summary

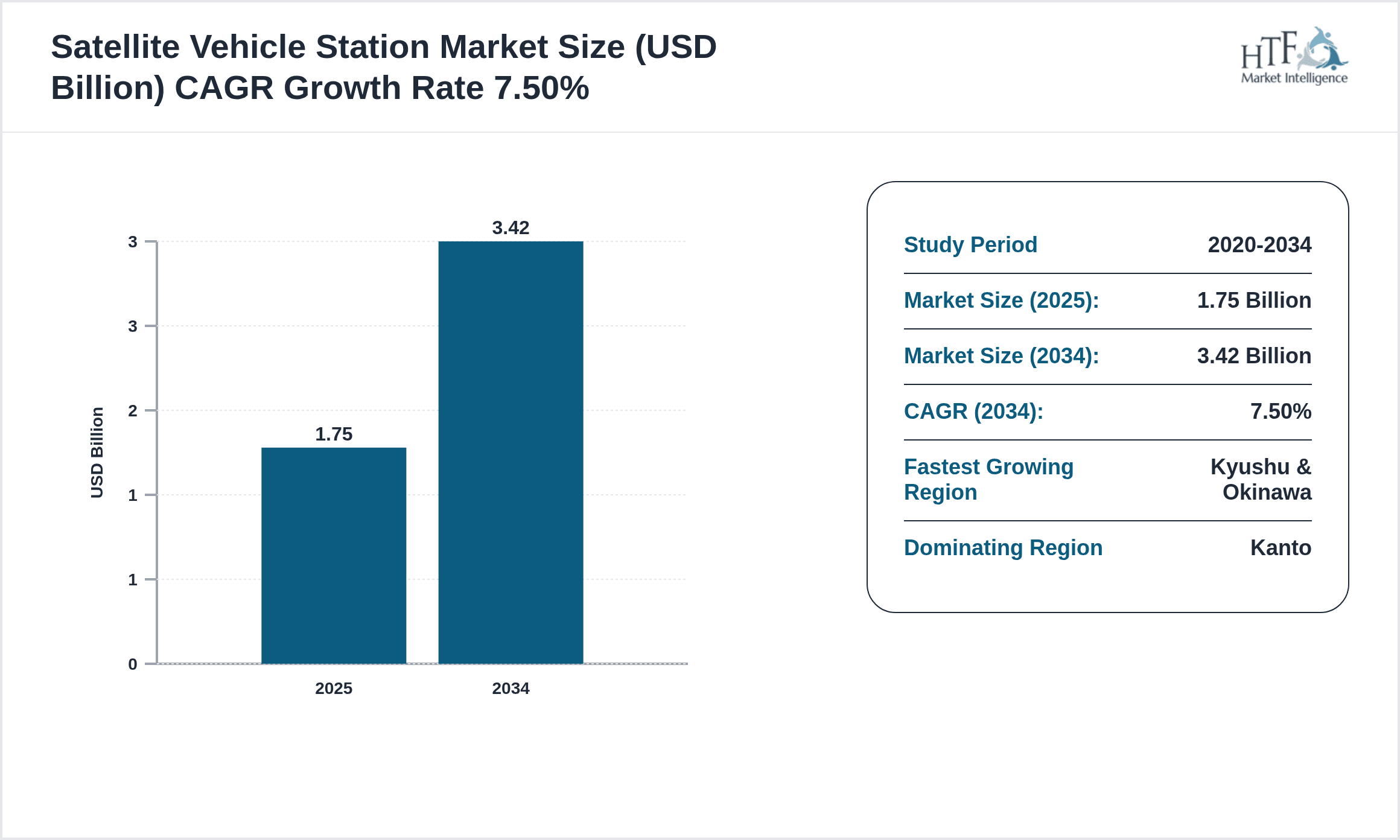

- •The Japan Satellite Vehicle Station market includes various types of satellite stations facilitating communication, navigation, tracking, telemetry, and data relay services to multiple industries such as defense, maritime, aerospace, and transportation within Japan. This market covers mobile, fixed, transportable, maritime, and aerospace satellite vehicle stations tailored to Japan’s unique geographical and technological landscape.

- •Key market highlights include a base market size of USD 1.75 Billion in 2025, projected to reach USD 3.42 Billion by 2034, reflecting a CAGR of 7.5%. Kanto leads with a 38% market share, while Kyushu & Okinawa exhibits the fastest growth rate at 10.3%. Mobile Satellite Vehicle Stations dominate the product segment, with Maritime Satellite Vehicle Stations growing rapidly.

- •The market holds strategic significance for Japan’s communication infrastructure, enabling enhanced connectivity, data relay, and operational efficiency across critical sectors. Ongoing investments in satellite technology and integration with emerging digital networks position the market for sustained growth and innovation.

Competitive Landscape

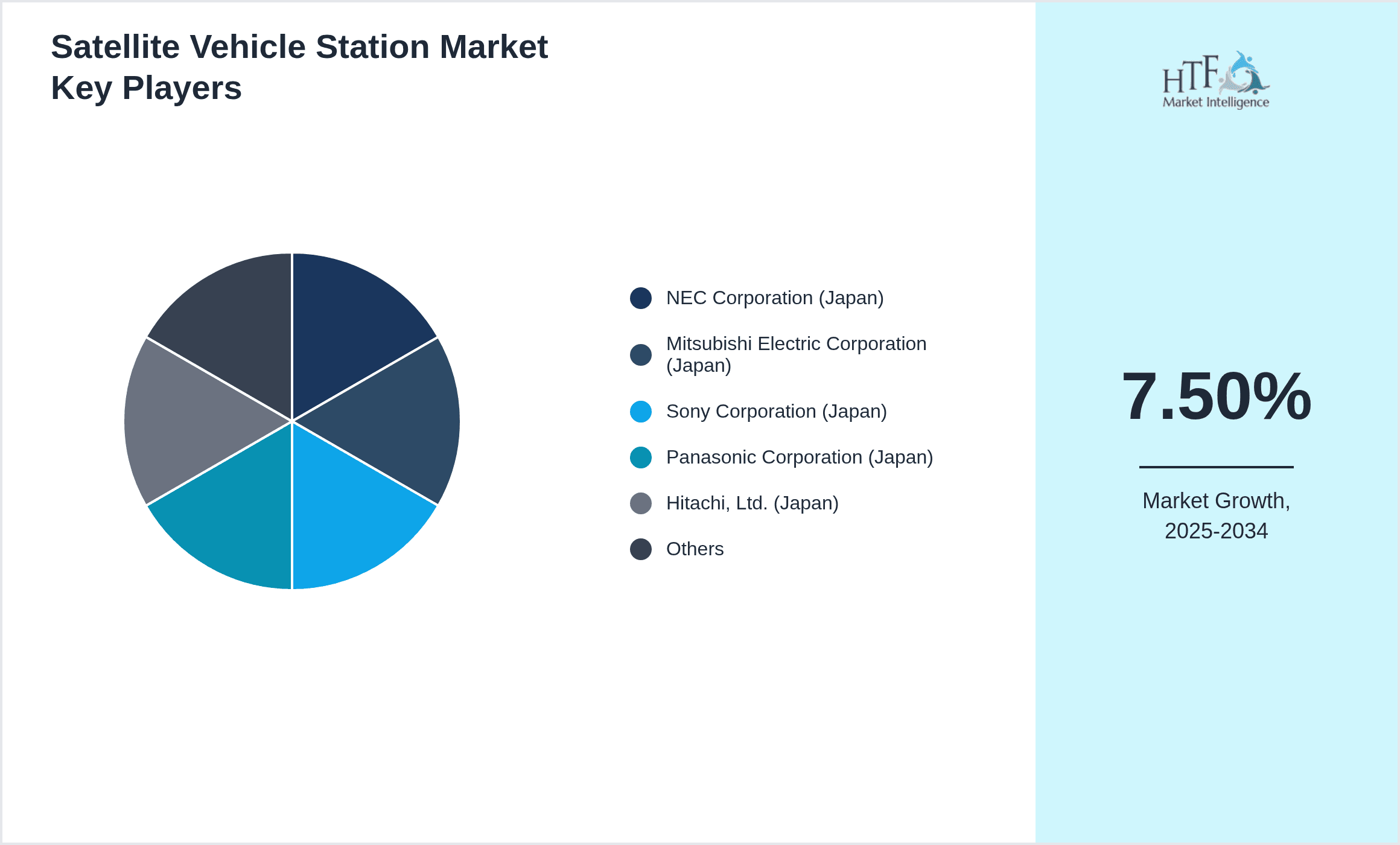

The Japan Satellite Vehicle Station market is highly competitive, featuring a blend of multinational corporations and domestic innovators. Competition revolves around technology innovation, enhanced signal processing, and service reliability. Companies invest heavily in R&D to develop versatile, high-performance satellite stations accommodating Japan’s diverse terrain and maritime zones. Strategic partnerships and collaborations with satellite operators and telecom providers are common to expand service capabilities. Market players differentiate through product customization, network integration, and compliance with stringent Japanese regulatory frameworks. Pricing strategies reflect the balance between advanced technology adoption and cost-efficiency to meet both commercial and governmental needs. The rivalry also drives advancements in mobile and maritime satellite stations to address growing demand from logistics, defense, and emergency response sectors. Overall, the market is expected to see intensified competition fueled by innovation and strategic alliances.

Leading Companies in Japan Satellite Vehicle Station Market

- •NEC Corporation (Japan)

- •Mitsubishi Electric Corporation (Japan)

- •Sony Corporation (Japan)

- •Panasonic Corporation (Japan)

- •Hitachi, Ltd. (Japan)

- •Toshiba Corporation (Japan)

- •Fujitsu Limited (Japan)

- •KDDI Corporation (Japan)

- •SoftBank Group Corp. (Japan)

- •NTT Communications Corporation (Japan)

- •Canon Inc. (Japan)

- •Rakuten Group, Inc. (Japan)

- •IHI Corporation (Japan)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Yokogawa Electric Corporation (Japan)

- •NEC Networks & System Integration Corporation (Japan)

- •Nippon Telegraph and Telephone Corporation (Japan)

- •Mitsubishi Heavy Industries, Ltd. (Japan)

- •Sharp Corporation (Japan)

- •Ricoh Company, Ltd. (Japan)

- •Sumitomo Corporation (Japan)

- •Kawasaki Heavy Industries, Ltd. (Japan)

- •Denso Corporation (Japan)

- •Sony Semiconductor Solutions Corporation (Japan)

- •NEC Space Technologies, Ltd. (Japan)

Market Breakdown

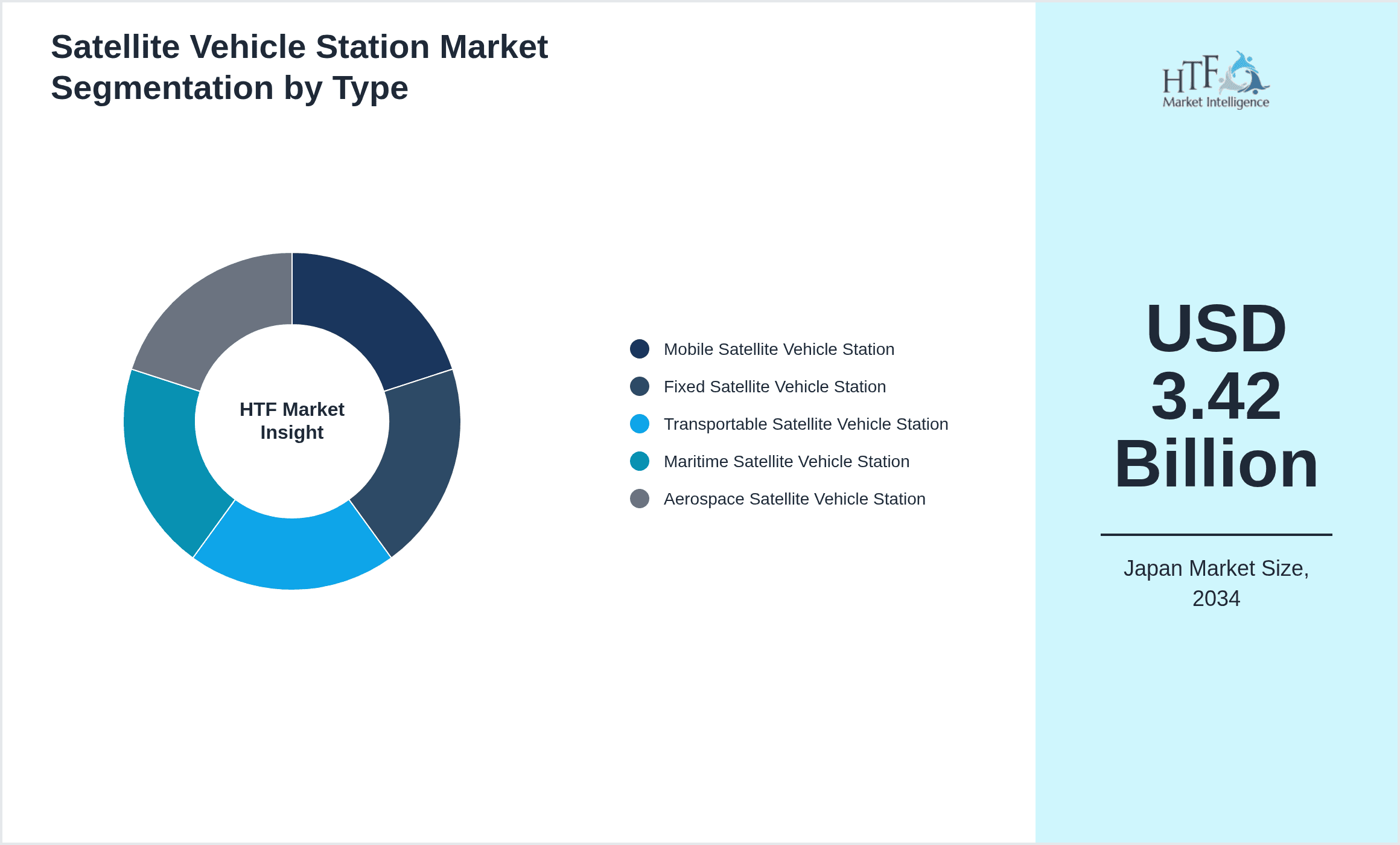

- •By Type

- ◦Mobile Satellite Vehicle Station

- ◦Fixed Satellite Vehicle Station

- ◦Transportable Satellite Vehicle Station

- ◦Maritime Satellite Vehicle Station

- ◦Aerospace Satellite Vehicle Station

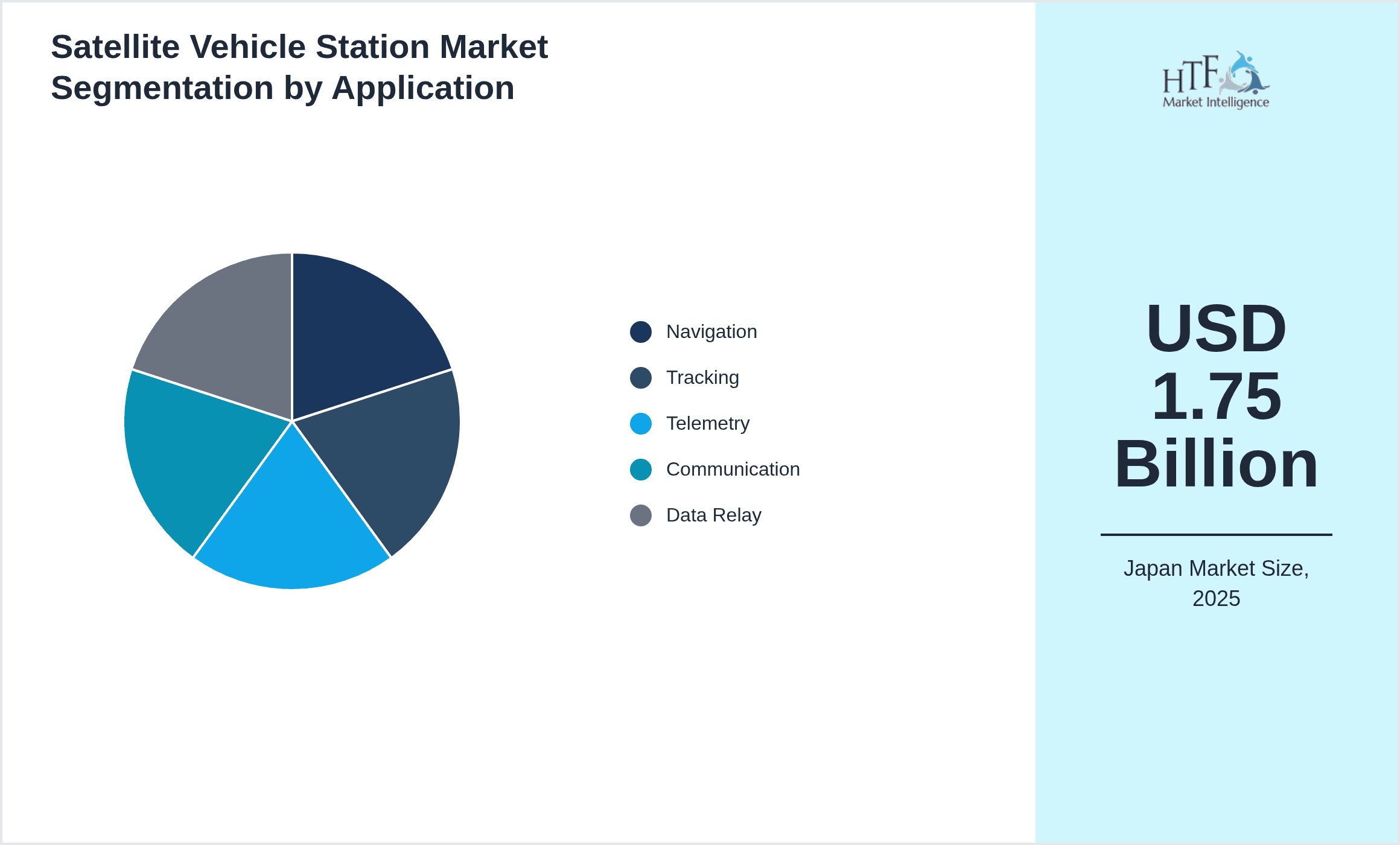

- •By Application

- ◦Navigation

- ◦Tracking

- ◦Telemetry

- ◦Communication

- ◦Data Relay

- •By End User

- ◦Defense & Military

- ◦Maritime Operations

- ◦Aerospace & Aviation

- ◦Telecommunications

- ◦Emergency Services

- •By Technology

- ◦Ku-band Systems

- ◦Ka-band Systems

- ◦L-band Systems

- ◦C-band Systems

Growth Drivers

The Japan Satellite Vehicle Station market is propelled by increasing demand for advanced satellite communication services across transportation, defense, and maritime sectors. Government initiatives to enhance national security and disaster management through robust satellite networks stimulate investment in mobile and fixed stations. Rising adoption of IoT and 5G technologies necessitates reliable satellite data relay infrastructure. Japan’s strategic geographic location drives demand for maritime satellite stations supporting shipping and fisheries. Additionally, growing aerospace activities for satellite launches and space exploration projects further fuel market growth. Technological advancements improving signal quality and station mobility enable broader application adoption. Continuous modernization of Japan’s telecommunication networks to integrate satellite capabilities also acts as a key growth catalyst.

Market Trends

Current trends in the Japan Satellite Vehicle Station market include the proliferation of hybrid satellite-terrestrial communication systems enhancing connectivity in remote regions. Integration of AI and machine learning for predictive maintenance and network optimization is gaining traction. The shift towards miniaturized, transportable satellite vehicle stations supports rapid deployment in disaster zones. Companies are increasingly adopting Ka-band technology for higher bandwidth and lower latency. Collaboration between satellite operators and telecom providers is intensifying to expand service coverage. Environmental sustainability initiatives encourage development of energy-efficient satellite stations. Furthermore, rising investments in maritime satellite communication reflect Japan’s focus on securing sea routes and fisheries management.

Market Restraints

Market growth is hindered by high capital expenditure and complex integration requirements for satellite vehicle stations, limiting adoption among smaller enterprises. Regulatory compliance with Japan’s stringent communication and security standards can delay project timelines. Technical challenges such as signal interference in urban centers and adverse weather impact station reliability. Limited availability of skilled workforce specialized in satellite technologies constrains rapid deployment. Additionally, competition from alternative terrestrial communication technologies reduces immediate demand for satellite-based solutions. Economic uncertainties and fluctuating government budgets for defense and infrastructure projects may further restrain market expansion.

Market Opportunities

Opportunities in the Japan Satellite Vehicle Station market lie in expanding satellite communication services for autonomous vehicles and smart transportation systems. Emerging demand for real-time maritime surveillance and fisheries management presents growth avenues for maritime satellite stations. Integration with 5G networks offers prospects for enhanced data throughput and low latency applications. Japan’s space exploration initiatives and satellite launch programs create need for specialized aerospace satellite vehicle stations. Increasing government focus on disaster resilience and emergency communication infrastructure drives investment. Collaborations with global satellite network providers to enhance coverage and service quality offer strategic growth potential. Innovation in energy-efficient, compact satellite stations also opens new market segments.

Market Challenges

Key challenges include managing the high complexity and cost of deploying satellite vehicle stations compliant with Japan’s regulatory environment. Technical difficulties such as mitigating signal attenuation caused by Japan’s mountainous terrain and dense urban areas affect performance. Ensuring cybersecurity of satellite communication systems against growing threats requires significant investment. The fragmented market with diverse end-user needs complicates standardization and scalability. Supply chain disruptions for critical components, exacerbated by global semiconductor shortages, impact production timelines. Additionally, the rapid evolution of communication technologies demands continuous innovation, posing a challenge for legacy equipment providers. Balancing cost-effectiveness with advanced functionality remains a persistent hurdle.

Regulatory Overview

Japan’s regulatory framework for satellite vehicle stations emphasizes strict licensing, frequency allocation, and compliance with the Ministry of Internal Affairs and Communications (MIC) standards established between 2020 and 2025. Recent updates mandate enhanced security protocols to protect satellite communication networks from cyber threats. Environmental regulations require stations to meet sustainability and electromagnetic emission guidelines. The government promotes harmonization of satellite communications with terrestrial networks under the Radio Act revisions implemented in 2023. Compliance with international treaties on satellite usage and spectrum management also influences market operations. These regulations collectively ensure safe, efficient, and secure deployment of satellite vehicle stations across Japan.

Market Intelligence

- •In March 2024, NEC Corporation launched a next-generation Mobile Satellite Vehicle Station featuring enhanced AI-driven signal processing capabilities designed to improve connectivity in remote and maritime environments. This innovation targets Japan’s growing demand for reliable mobile communication infrastructure in disaster-prone areas and maritime sectors, enabling faster data relay and expanded coverage. NEC’s strategic focus on integrating 5G compatibility positions it competitively within the Japan market.

- •In November 2023, Mitsubishi Electric Corporation unveiled its advanced Ka-band Fixed Satellite Vehicle Station tailored for aerospace communications. The product incorporates energy-efficient components and supports high-bandwidth applications, aligning with Japan’s expanding satellite launch activities. This launch demonstrates Mitsubishi Electric’s commitment to technological leadership and addresses critical market needs in aerospace and defense sectors.

Mergers & Acquisitions

- •In July 2023, Panasonic Corporation acquired a controlling stake in a leading Japanese satellite communication equipment provider specializing in transportable satellite vehicle stations. This acquisition enhances Panasonic’s portfolio in satellite infrastructure and strengthens its position in the mobile and emergency communications segment. The strategic move aims to leverage combined R&D capabilities to accelerate innovation and expand market reach within Japan’s satellite communication ecosystem.

- •In January 2024, SoftBank Group Corp. completed the acquisition of a domestic satellite network operator focusing on maritime satellite services. This deal bolsters SoftBank’s satellite communication offerings and aligns with its vision to expand integrated communication solutions for maritime and logistics industries. The acquisition is expected to drive synergies in technology development and broaden service coverage across Japan’s critical maritime zones.

Recent Industry News

- •In June 2022, KDDI Corporation partnered with a global satellite operator to deploy advanced L-band satellite vehicle stations across Japan’s northern regions including Hokkaido and Tohoku. This strategic collaboration aims to improve communication reliability for remote communities and enhance disaster response capabilities. The rollout supports Japan’s national initiative to bridge the digital divide and strengthen satellite communication infrastructure in underserved areas. Source: KDDI Official Press Release

- •In September 2023, Hitachi, Ltd. expanded its satellite communication product line by launching an AI-enabled telemetry satellite vehicle station designed for aerospace applications. This product enhances real-time data acquisition and processing, critical for Japan’s growing space exploration and satellite monitoring programs. The innovation reflects Hitachi’s commitment to leveraging AI to optimize satellite communication performance. Source: Hitachi Newsroom

- •In February 2024, Toshiba Corporation announced a strategic investment to develop energy-efficient maritime satellite vehicle stations incorporating renewable power technologies. The initiative targets the shipping industry’s need for sustainable communication solutions and aims to reduce operational carbon footprint. This move aligns with Japan’s national environmental policies and growing demand for green technologies in satellite communications. Source: Toshiba Sustainability Report

- •In November 2021, Fujitsu Limited launched a transportable satellite vehicle station optimized for rapid deployment in emergency scenarios such as natural disasters. The system features modular components and enhanced portability, supporting Japan’s disaster resilience framework and emergency communication networks. Fujitsu’s innovation caters to governmental and NGO requirements for reliable satellite connectivity in crisis zones. Source: Fujitsu Corporate Announcements

Market Statistics

- •CAGR by 2034: 7.5%

- •Market Size by 2034: USD 3.42 Billion

- •Market Size in 2025: USD 1.75 Billion

- •Dominating Type: Mobile Satellite Vehicle Station; Next-Following Type: Fixed Satellite Vehicle Station

- •Dominating Application: Communication; Next-Following Application: Navigation

- •Dominating Region: Kanto; Second-Leading Region: Chubu

- •Region with Highest Growth Rate: Kyushu & Okinawa

- •Dominating Country: Japan

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: Mobile Satellite Vehicle Station - 42%, Fixed Satellite Vehicle Station - 28%

- •Market Share (%) of Dominating vs Followed Application: Communication - 35%, Navigation - 25%

- •Growth Rate (%) of Dominating vs Followed Type: Mobile Satellite Vehicle Station - 7.8%, Fixed Satellite Vehicle Station - 6.5%

- •Growth Rate (%) of Dominating vs Followed Application: Communication - 8.0%, Navigation - 6.2%

Top 5 Global Players

- •NEC Corporation (Japan)

- •Mitsubishi Electric Corporation (Japan)

- •Panasonic Corporation (Japan)

- •Hitachi, Ltd. (Japan)

- •SoftBank Group Corp. (Japan)

Regional Outlook

The Kanto currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Kyushu & Okinawa is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Kansai

- Chugoku

- Shikoku

- Kyushu

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.75 Billion |

| Forecast Year Market Size | USD 3.42 Billion |

| CAGR | 7.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.2% |

| Regions Covered | Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu |

| Key Companies | NEC Corporation (Japan), Mitsubishi Electric Corporation (Japan), Sony Corporation (Japan), Panasonic Corporation (Japan), Hitachi, Ltd. (Japan), Toshiba Corporation (Japan), Fujitsu Limited (Japan), KDDI Corporation (Japan), SoftBank Group Corp. (Japan), NTT Communications Corporation (Japan), Canon Inc. (Japan), Rakuten Group, Inc. (Japan), IHI Corporation (Japan), Sumitomo Electric Industries, Ltd. (Japan), Yokogawa Electric Corporation (Japan), NEC Networks & System Integration Corporation (Japan), Nippon Telegraph and Telephone Corporation (Japan), Mitsubishi Heavy Industries, Ltd. (Japan), Sharp Corporation (Japan), Ricoh Company, Ltd. (Japan), Sumitomo Corporation (Japan), Kawasaki Heavy Industries, Ltd. (Japan), Denso Corporation (Japan), Sony Semiconductor Solutions Corporation (Japan), NEC Space Technologies, Ltd. (Japan) |

Japan Satellite Vehicle Station Market - Japan Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.