China Atomic Layer Deposition Equipment for LED Market Size, Growth & Revenue 2025-2034

China Atomic Layer Deposition Equipment for LED Market is segmented by Type (Thermal ALD Equipment, Plasma-Enhanced ALD Equipment, Spatial ALD Equipment, Other ALD Equipment), Application (LED Display Panels, LED Lighting, Automotive LEDs, Optical Sensors, Others), End-User Industry (Consumer Electronics, Automotive, Healthcare Devices, Industrial Lighting, Telecommunications), Technology (Batch ALD Systems, Single Wafer ALD Systems, Roll-to-Roll ALD Systems), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Atomic Layer Deposition Equipment for LED market involves advanced machinery designed for precise thin-film deposition on LED substrates, supporting industries like display panels, automotive lighting, and optical sensors. It covers Thermal, Plasma-Enhanced, and Spatial ALD equipment tailored to enhance LED performance and manufacturing precision.

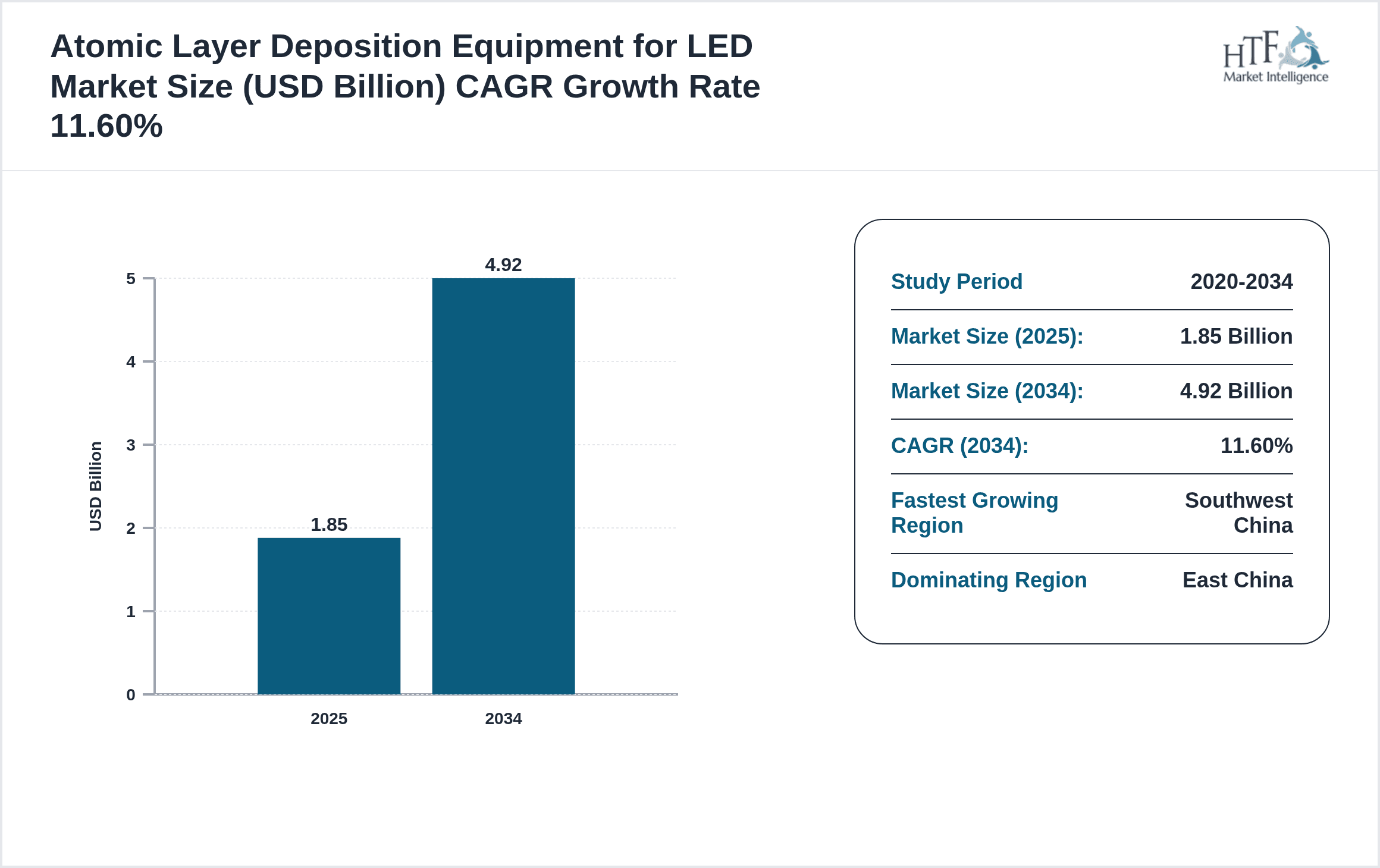

- •Market growth is propelled by China's expanding LED manufacturing sector, rising demand for energy-efficient lighting, and government initiatives promoting semiconductor technologies, resulting in a forecasted CAGR of 11.6% between 2025 and 2034.

- •This market represents a strategic pillar for China's semiconductor equipment industry, enabling manufacturers to meet global standards in LED quality and efficiency, fostering innovation, and bolstering domestic production capabilities.

Competitive Landscape

Competition within the China Atomic Layer Deposition Equipment for LED market is intense, driven by a mix of domestic innovators and international technology providers. Companies emphasize innovation in deposition techniques, equipment precision, and throughput to secure market share. Strategic collaborations and continuous R&D investments are common to enhance product offerings. Market rivalry is characterized by rapid technology upgrades, cost optimization, and service support differentiation. Domestic firms focus on customization for local LED manufacturers, while global players leverage advanced proprietary technologies. Barriers include high capital expenditure and stringent quality requirements, which limit new entrants. Overall, the competitive environment fosters technological advancement and consolidation, positioning key players for long-term growth.

Leading Companies in China Atomic Layer Deposition Equipment for LED Market

- •AMEC (China)

- •Picosun Oy (Finland)

- •Veeco Instruments Inc. (United States)

- •Oxford Instruments (United Kingdom)

- •ASM International (Netherlands)

- •Beneq Oy (Finland)

- •SENTECH Instruments GmbH (Germany)

- •Kurt J. Lesker Company (United States)

- •Hitachi High-Technologies Corporation (Japan)

- •Zhongke AMEC (China)

- •Nanofilm Technologies International (Singapore)

- •Tokyo Electron Limited (Japan)

- •Applied Materials, Inc. (United States)

- •SUSS MicroTec SE (Germany)

- •Kokusai Electric Corporation (Japan)

Market Breakdown

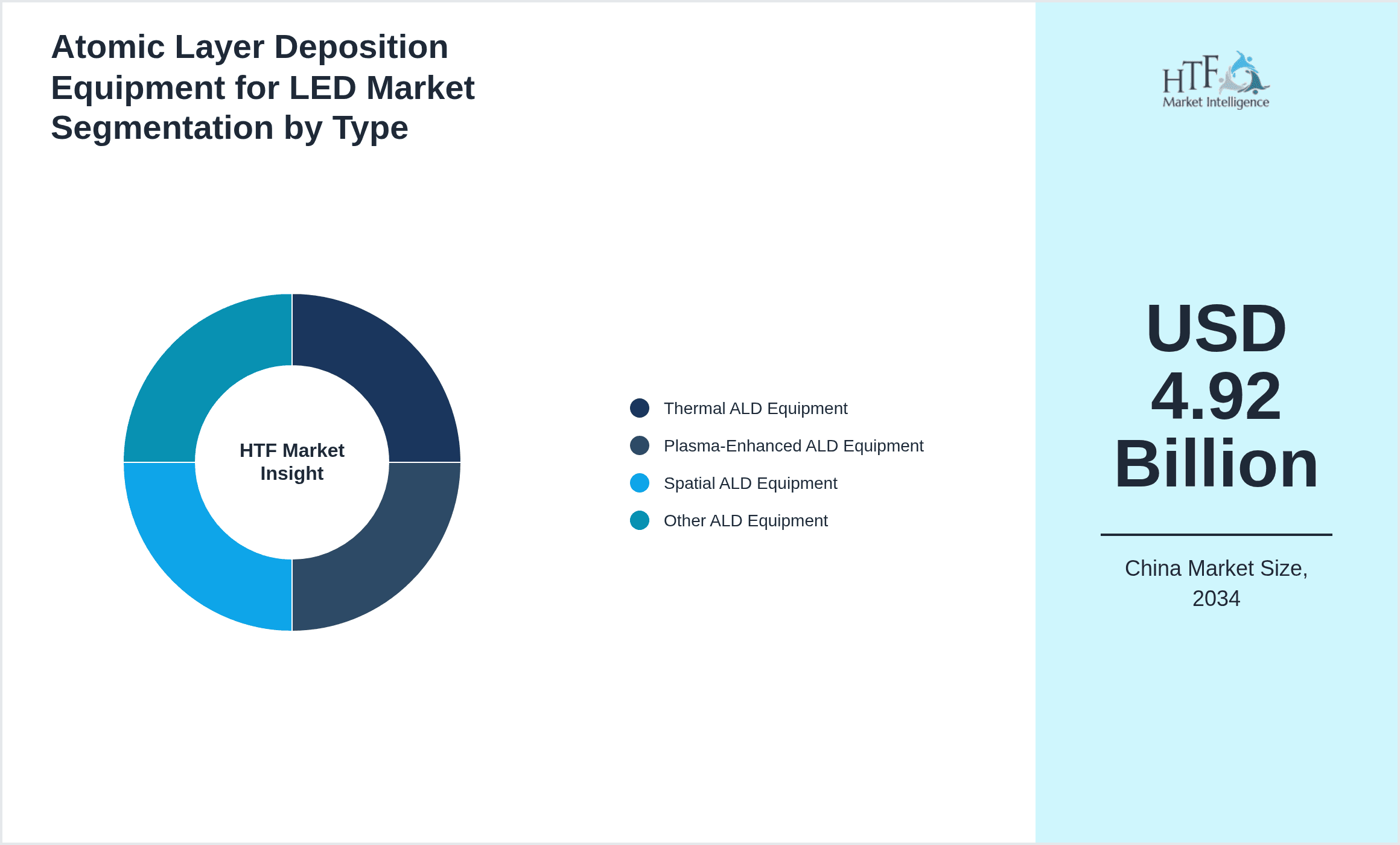

- •By Type

- ◦Thermal ALD Equipment

- ◦Plasma-Enhanced ALD Equipment

- ◦Spatial ALD Equipment

- ◦Other ALD Equipment

- •By Application

- ◦LED Display Panels

- ◦LED Lighting

- ◦Automotive LEDs

- ◦Optical Sensors

- ◦Others

- •By End-User Industry

- ◦Consumer Electronics

- ◦Automotive

- ◦Healthcare Devices

- ◦Industrial Lighting

- ◦Telecommunications

- •By Technology

- ◦Batch ALD Systems

- ◦Single Wafer ALD Systems

- ◦Roll-to-Roll ALD Systems

Growth Drivers

- •Rapid expansion of the LED manufacturing industry in China, driven by demand in consumer electronics and automotive sectors, is fueling increased adoption of advanced ALD equipment for superior product quality and efficiency.

- •Government incentives and policies supporting semiconductor and display technologies promote domestic production capabilities and investments in cutting-edge ALD technologies.

- •Technological advancements such as the development of spatial ALD systems enable higher throughput and lower production costs, attracting LED manufacturers to upgrade existing equipment.

- •Growing emphasis on energy-efficient and environmentally friendly LED lighting solutions is creating demand for precision ALD processes to enhance device performance and lifespan.

- •Increasing integration of ALD equipment with Industry 4.0 and automation technologies improves process control and reduces operational downtime, boosting market growth.

Market Trends

- •Shift towards plasma-enhanced ALD equipment adoption due to its ability to deposit films at lower temperatures, supporting flexible and heat-sensitive LED substrates.

- •Rise in domestic Chinese manufacturers developing indigenous ALD technologies to reduce dependency on imports and cater specifically to local LED production needs.

- •Integration of ALD systems with real-time monitoring and AI-driven process optimization is becoming prevalent to enhance yield and minimize defects.

- •Collaborations between equipment manufacturers and LED producers to co-develop customized ALD solutions tailored for next-generation LED devices.

- •Sustainability focus encouraging the use of eco-friendly precursors and processes in ALD equipment to reduce environmental footprint in LED manufacturing.

Market Opportunities

- •Growing demand for mini-LED and micro-LED technologies opens new avenues for ALD equipment capable of ultra-thin, conformal coatings essential for these advanced displays.

- •Expansion of LED lighting applications in smart cities and IoT devices creates a broader market for deposition equipment with tailored process capabilities.

- •Opportunity exists for equipment providers to develop cost-effective, high-throughput spatial ALD systems to serve mass production requirements in China.

- •Potential for partnerships between global ALD technology leaders and Chinese manufacturers to localize production and enhance service networks.

- •Emerging applications in automotive LED sensors and optical devices provide niche markets requiring specialized ALD equipment customization.

Market Challenges

- •High capital expenditure and complex technology integration pose barriers for small and medium LED manufacturers to adopt advanced ALD equipment.

- •Limited availability of skilled workforce and technical expertise to operate and maintain sophisticated ALD systems restrict market penetration in some regions.

- •Strong competition from established international ALD equipment manufacturers challenges domestic companies in gaining market share.

- •Rapid technology obsolescence requires continuous R&D investment, increasing operational risks for equipment providers and users alike.

- •Supply chain disruptions for critical components and precursor chemicals intermittently affect equipment production and deployment timelines.

Regulatory Framework

- •Between 2023 and 2025, China implemented stricter environmental standards targeting semiconductor manufacturing equipment, mandating reduced emissions and waste from ALD processes, increasing compliance costs.

- •New safety regulations require enhanced operator protections and automated shutdown features in ALD equipment, impacting design and manufacturing specifications.

- •Government subsidies and tax incentives have been introduced to encourage domestic production of semiconductor and LED manufacturing equipment, fostering market growth.

- •Export control policies have tightened on certain high-tech ALD equipment components, affecting global supply chains and encouraging local alternatives.

- •Standards for equipment interoperability and quality assurance have been updated, aligning with international norms to boost export competitiveness.

Industry Insights

- •In March 2024, AMEC launched a new generation of thermal ALD equipment optimized for high-volume LED panel production, featuring enhanced deposition uniformity and reduced cycle times. This innovation addresses the increasing demand for energy-efficient LED displays in China’s consumer electronics sector. The company's strategic focus on automation integration is expected to improve manufacturing scalability and reduce costs.

- •In September 2023, Picosun Oy announced a joint development agreement with a leading Chinese LED manufacturer to customize plasma-enhanced ALD systems for automotive LED applications, aiming to improve film quality on complex geometries. This partnership represents a significant step toward localized ALD technology adaptation in China’s automotive lighting market.

Mergers & Acquisitions

- •In July 2024, AMEC completed the acquisition of a domestic ALD component supplier, enhancing its vertical integration capabilities and accelerating R&D for next-generation LED equipment. This strategic move strengthens AMEC’s position in the China market by securing critical supply chains and expanding its product portfolio to include customized ALD solutions for high-end LED manufacturers.

- •In February 2025, Veeco Instruments Inc. expanded its footprint in China by acquiring a local semiconductor equipment firm specializing in spatial ALD technologies. This acquisition aims to leverage regional expertise and improve service responsiveness, enabling Veeco to capitalize on growing demand for advanced ALD systems in China’s LED sector and reinforce its competitive advantage.

Recent Industry News

- •On 15th January 2025, Oxford Instruments inaugurated a new R&D center in Shanghai focused on developing plasma-enhanced ALD equipment tailored for China’s expanding LED market. The center aims to foster innovation through collaboration with local universities and industries, accelerating the commercialization of next-generation ALD technologies with improved energy efficiency and process speed. Source: Oxford Instruments Official Release

- •On 22nd March 2025, ASM International announced a strategic partnership with a leading Chinese LED manufacturer to co-develop batch ALD systems that optimize throughput and reduce production costs. The collaboration is expected to address the scaling challenges faced by LED producers transitioning to larger panel formats, reinforcing ASM’s commitment to the China market. Source: ASM International News

- •On 10th May 2025, Beneq Oy launched a new spatial ALD platform in Beijing designed specifically for flexible LED applications and wearable devices. The equipment features advanced process control and reduced footprint, aligning with the growing demand for miniaturized and flexible LED solutions in China’s consumer electronics sector. Source: Beneq Oy Press Release

- •On 30th August 2025, Hitachi High-Technologies Corporation expanded its after-sales service network across key Chinese regional zones, including East and South China. This expansion aims to improve equipment uptime and customer support for ALD system users in rapidly growing LED manufacturing hubs. Source: Hitachi High-Technologies Official Statement

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 4.92 Billion |

| CAGR | 11.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | AMEC (China), Picosun Oy (Finland), Veeco Instruments Inc. (United States), Oxford Instruments (United Kingdom), ASM International (Netherlands), Beneq Oy (Finland), SENTECH Instruments GmbH (Germany), Kurt J. Lesker Company (United States), Hitachi High-Technologies Corporation (Japan), Zhongke AMEC (China), Nanofilm Technologies International (Singapore), Tokyo Electron Limited (Japan), Applied Materials, Inc. (United States), SUSS MicroTec SE (Germany), Kokusai Electric Corporation (Japan) |

China Atomic Layer Deposition Equipment for LED Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.