Europe Stainless Steel Saute Pan Market - Outlook 2024-2034

Europe Stainless Steel Saute Pan Market is segmented by Application (Home Kitchens, Commercial Kitchens, Catering Services, Food Processing Units, Hospitality Sector), Type (Induction Compatible, Non-Induction, With Lid, Without Lid, Non-Stick Coated), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Stainless Steel Saute Pan market covers the production and sale of premium stainless steel pans used in home and commercial kitchens, characterized by features such as induction compatibility and non-stick coatings. This market serves multiple applications including domestic cooking, commercial kitchens, catering, and food processing, with a focus on durability, heat efficiency, and design innovation across European countries.

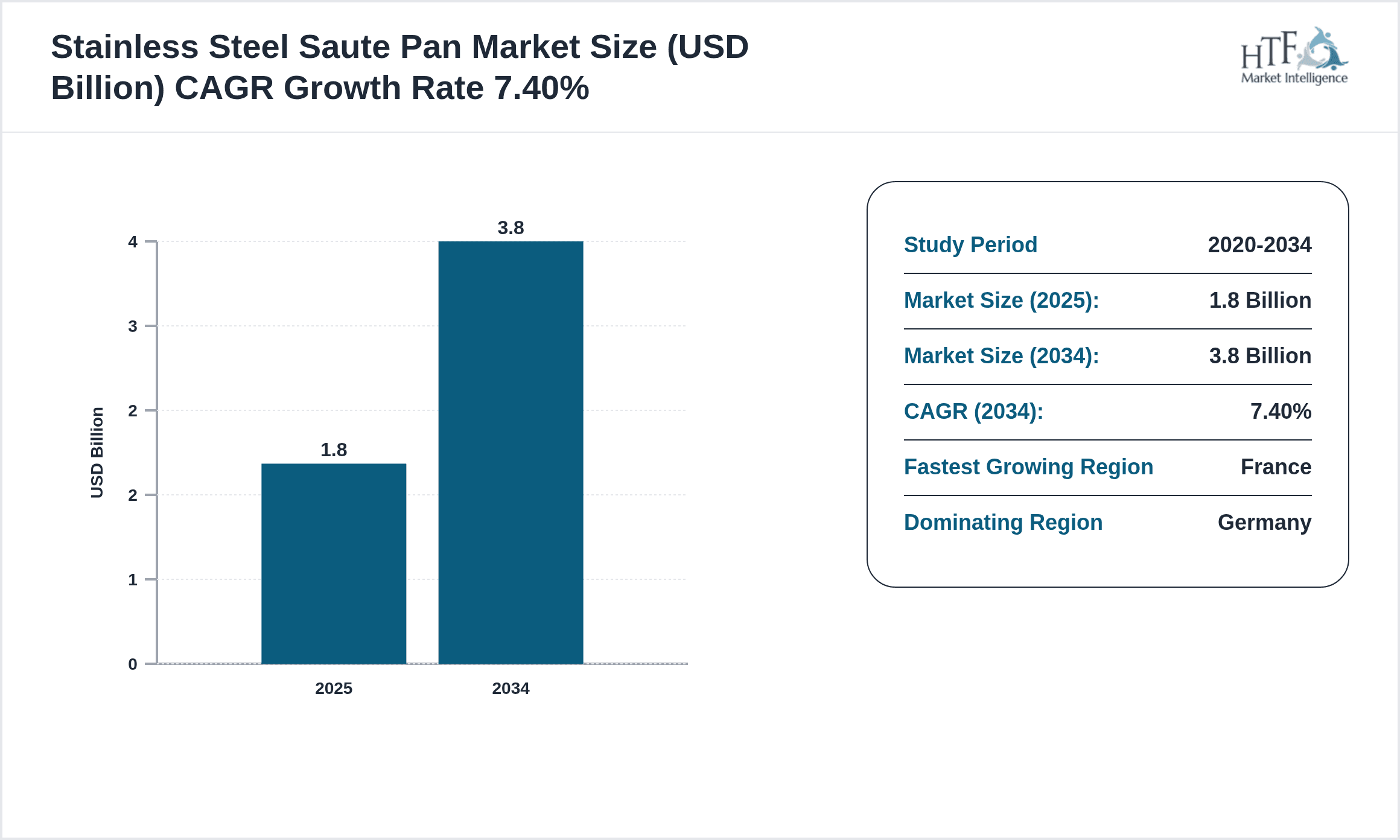

- •Key highlights indicate steady market growth driven by rising consumer interest in durable cookware and expanding hospitality services in Europe. The market is forecasted to grow at a CAGR of 7.4% from 2024 to 2034, reaching USD 3.8 Billion by 2034, up from USD 1.8 Billion in 2024.

- •Strategically, the Europe stainless steel saute pan market is vital for cookware manufacturers, distributors, and hospitality businesses as it caters to increasing demand for high-quality, sustainable cooking solutions. Innovation in product design and compliance with stringent European regulations offer competitive advantages to key players.

Competitive Landscape

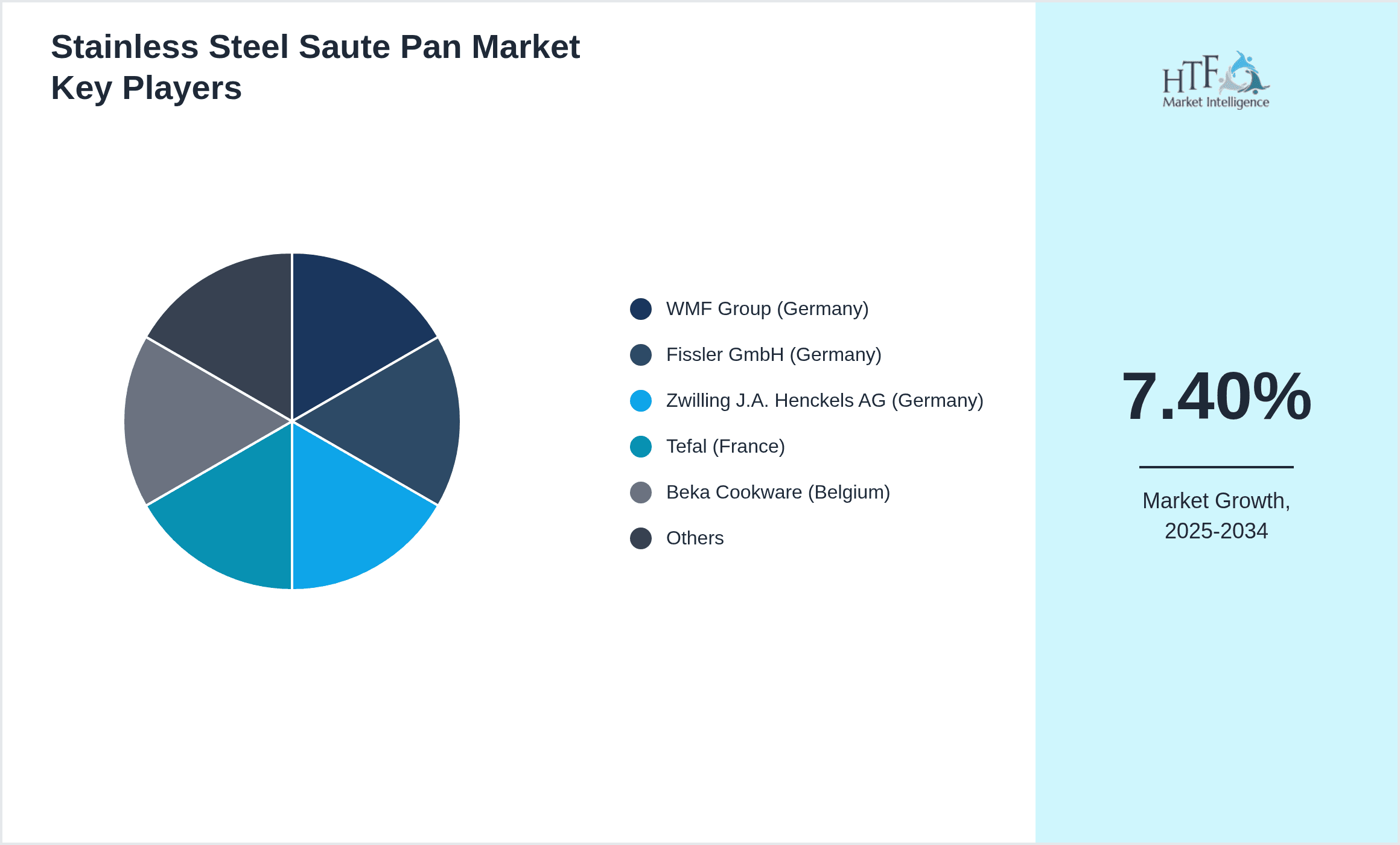

Competition within the Europe Stainless Steel Saute Pan market is intense, with companies focusing on product innovation, quality enhancement, and sustainable manufacturing practices to differentiate themselves. Market leaders leverage advanced stainless steel alloys and ergonomic designs to meet evolving consumer preferences for durable and induction-compatible cookware. Rivalry is also based on expanding distribution networks, including online retail and specialty kitchenware stores, to capture diverse customer segments. Strategic partnerships and collaborations are common to enhance product portfolios and geographic reach. Pricing strategies balance affordability with premium quality, catering to both budget-conscious consumers and high-end commercial clients. The competitive environment is further shaped by regulatory compliance requirements across European countries, encouraging companies to adopt eco-friendly materials and production processes. Future trends suggest increased emphasis on digital marketing and customized cookware solutions to maintain market positioning and drive growth.

Leading Companies in Europe Stainless Steel Saute Pan Market

- •WMF Group (Germany)

- •Fissler GmbH (Germany)

- •Zwilling J.A. Henckels AG (Germany)

- •Tefal (France)

- •Beka Cookware (Belgium)

- •Scanpan A/S (Denmark)

- •Le Creuset (France)

- •Berndes (Germany)

- •De Buyer (France)

- •Silit GmbH (Germany)

- •Sambonet Paderno Industrie S.p.A. (Italy)

- •Ballarini (Italy)

- •Rösle (Germany)

- •Alessi (Italy)

- •Cristel (France)

- •Zwiesel Kristallglas AG (Germany)

- •Kuhn Rikon AG (Switzerland)

- •KitchenAid Europe (Netherlands)

- •Villeroy & Boch AG (Germany)

- •Gastroback GmbH (Germany)

- •Joseph Joseph Ltd (UK)

- •Stelton A/S (Denmark)

- •Lodge Manufacturing Co. (Europe Division) (UK)

- •Bialetti Industrie S.p.A. (Italy)

- •Cuisinox Ltd. (UK)

Europe Stainless Steel Saute Pan Market Segmentation

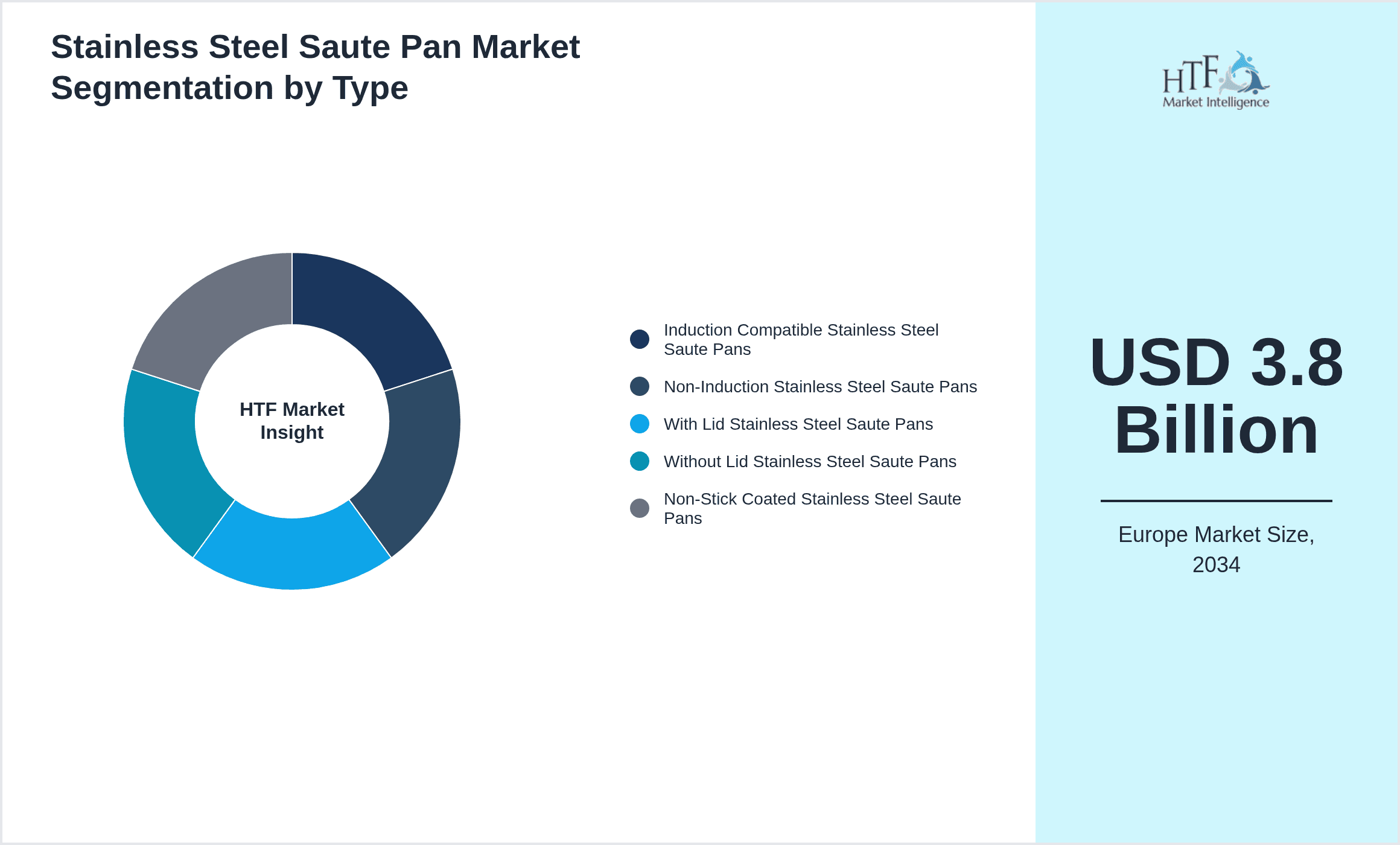

- •By Type

- ◦Induction Compatible Stainless Steel Saute Pans

- ◦Non-Induction Stainless Steel Saute Pans

- ◦With Lid Stainless Steel Saute Pans

- ◦Without Lid Stainless Steel Saute Pans

- ◦Non-Stick Coated Stainless Steel Saute Pans

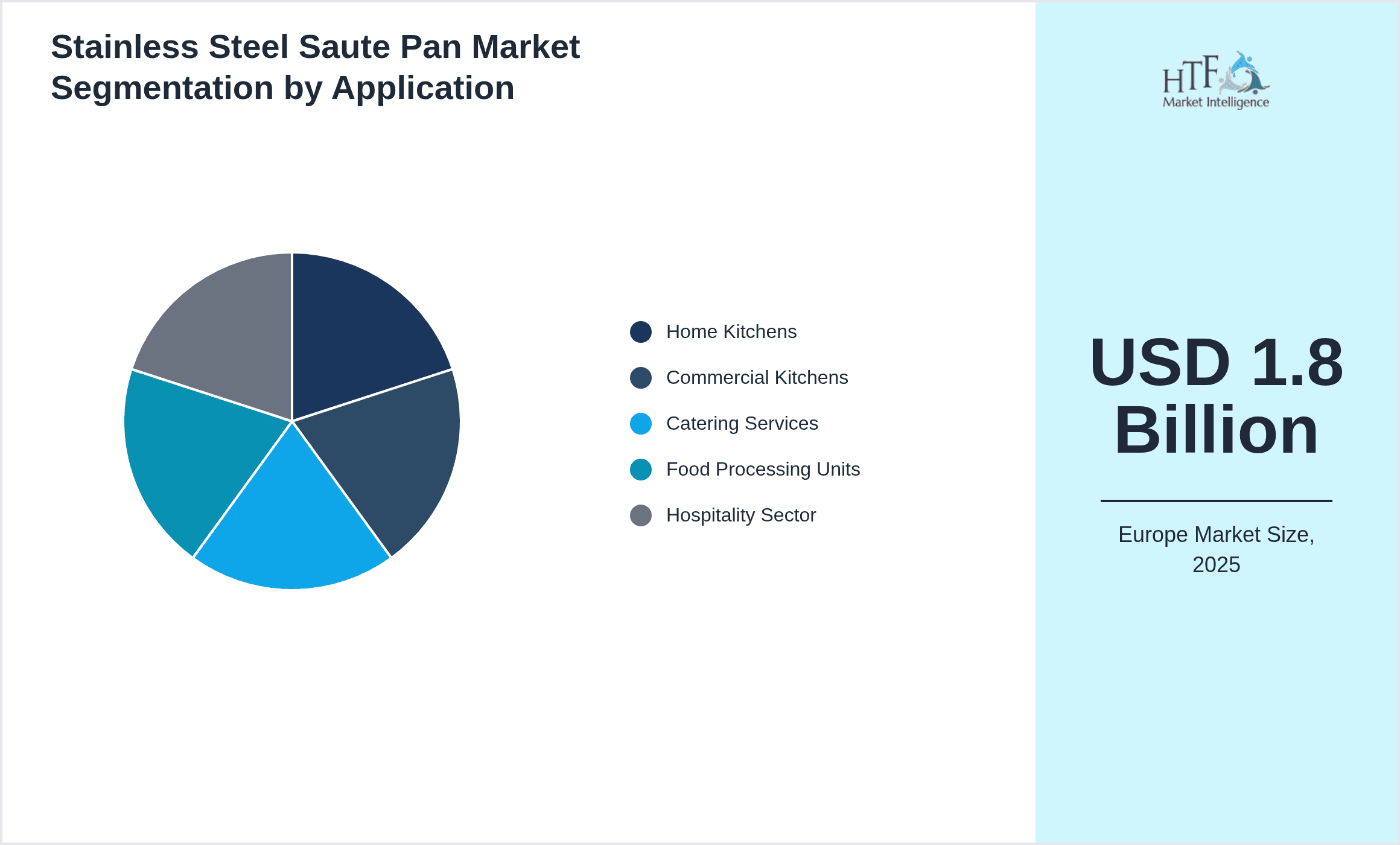

- •By Application

- ◦Home Kitchens

- ◦Commercial Kitchens

- ◦Catering Services

- ◦Food Processing Units

- ◦Hospitality Sector

- •By Distribution Channel

- ◦Retail Stores

- ◦Online Retail

- ◦Specialty Kitchenware Stores

- ◦Wholesale Distributors

- •By Material Technology

- ◦304 Stainless Steel

- ◦316 Stainless Steel

- ◦Mixed Alloy Stainless Steel

- ◦Eco-Friendly Recycled Stainless Steel

Growth Drivers

The Europe Stainless Steel Saute Pan market growth is primarily driven by increasing consumer preference for durable and versatile cookware that supports modern cooking technologies such as induction stovetops. Rising disposable incomes and growing culinary interest among European households fuel demand. The expanding hospitality sector, including restaurants and catering services, further stimulates market expansion. Innovations in non-stick coatings combined with stainless steel enhance cooking efficiency and ease of maintenance, attracting both domestic and commercial buyers. Additionally, stringent European standards encouraging eco-friendly and sustainable cookware production boost market confidence and consumer trust. The shift towards healthy cooking practices, where stainless steel is favored over traditional non-stick pans for chemical-free food preparation, also significantly contributes to market growth. These factors collectively propel the Europe stainless steel saute pan market toward steady expansion through 2034.

Market Trends

A prominent trend in the Europe Stainless Steel Saute Pan market is the integration of advanced multi-layered base technology, enhancing heat distribution and energy efficiency. Manufacturers are increasingly adopting eco-friendly materials and recycling processes to align with Europe’s sustainability goals. The rise of e-commerce platforms is transforming distribution, offering consumers broader access to premium and niche cookware brands. Customization and ergonomic designs tailored to professional chefs and home cooks are gaining popularity. Moreover, collaborations between cookware brands and celebrity chefs or influencers are shaping consumer preferences and driving brand loyalty. These trends reflect a market evolving with technological innovation, sustainability focus, and changing consumer behavior toward premium and functional kitchenware.

Market Restraints

Despite positive growth, the Europe Stainless Steel Saute Pan market faces challenges from the relatively high cost of premium stainless steel products compared to alternative materials like aluminum and cast iron. Price sensitivity in certain consumer segments limits market penetration. Additionally, the complexity of manufacturing induction-compatible and non-stick coated pans increases production costs and affects pricing strategies. The market is also restrained by the availability of counterfeit and low-quality products, which undermine consumer confidence. Furthermore, regulatory compliance with strict European environmental and safety standards imposes additional operational costs on manufacturers. Finally, shifting consumer preferences towards newer cooking technologies and appliances, such as air fryers, may reduce traditional saute pan demand in some segments.

Market Opportunities

Emerging opportunities in the Europe Stainless Steel Saute Pan market include expanding into untapped Eastern European countries where growing urbanization and rising middle-class populations increase cookware demand. Innovations in smart cookware incorporating temperature sensors and app integration present a new frontier for product differentiation. There is potential for growth through collaborations with culinary institutes and professional chefs to co-develop specialized cookware lines. The rising trend of sustainable kitchenware allows companies to capitalize on eco-conscious consumer segments by offering recycled stainless steel products. Additionally, growth in online retail channels facilitates direct-to-consumer sales, reducing dependency on traditional retail and enhancing margins. Expanding customization options and launching limited-edition collections can also attract premium buyers, thus diversifying revenue streams.

Market Challenges

Key challenges for the Europe Stainless Steel Saute Pan market include intense price competition from low-cost imports, which can erode margins for domestic manufacturers. Maintaining product quality while scaling up production poses operational difficulties. The complexity of complying with diverse national regulations across Europe increases administrative burdens. Supply chain disruptions, including fluctuations in raw stainless steel prices, impact cost stability and product availability. Additionally, consumer education about the benefits of stainless steel saute pans compared to other materials remains limited in some regions, hindering adoption. The market also faces challenges in balancing innovation with sustainability, as newer coatings or designs must meet environmental standards without compromising performance. Lastly, shifting consumer cooking habits towards convenience appliances may reduce demand for traditional saute pans over time.

Regulatory Overview

Recent regulatory updates in Europe emphasize sustainability and safety in cookware manufacturing, impacting the stainless steel saute pan market. The European Union’s REACH regulation mandates strict control over chemical substances used in coatings and materials, ensuring consumer safety. Additionally, the EU Eco-Design Directive encourages manufacturers to reduce environmental impacts by promoting resource-efficient production processes and recyclable materials. Several countries have introduced labeling requirements for cookware to inform consumers about material composition and compliance standards. These regulations necessitate that manufacturers implement rigorous quality checks and adopt eco-friendly materials, driving innovation in sustainable product design. Compliance with these evolving standards is critical for market access and consumer trust, influencing product development cycles and cost structures within the Europe stainless steel saute pan industry.

Market Intelligence

- •In March 2023, WMF Group launched its latest line of induction-compatible stainless steel saute pans featuring enhanced thermal conductivity and ergonomic handles designed for professional kitchens and home chefs alike. This innovation supports energy-efficient cooking and aligns with increasing demand for premium cookware in Europe’s expanding hospitality sector. The product line also incorporates recycled stainless steel, reinforcing WMF’s commitment to sustainability and regulatory compliance.

- •In October 2022, Fissler GmbH introduced a smart saute pan integrating temperature sensors linked to a mobile app, providing users with precise cooking control and alerts. This technological advancement positions Fissler at the forefront of smart kitchenware innovation, catering to tech-savvy consumers and professional cooks seeking enhanced cooking experiences in Europe’s competitive cookware market.

Mergers & Acquisitions

- •In August 2023, Zwilling J.A. Henckels AG acquired a majority stake in a European eco-friendly cookware startup specializing in recycled stainless steel products. This strategic acquisition enhances Zwilling’s sustainable product portfolio, enabling access to innovative manufacturing techniques and expanding its footprint in the environmentally conscious segment of the Europe stainless steel saute pan market.

- •In February 2022, Tefal expanded its European market presence by acquiring a premium kitchenware brand known for high-quality stainless steel cookware in the UK and France. This acquisition strengthens Tefal’s distribution network and product offerings, facilitating deeper penetration into commercial and retail channels across Europe.

Recent Industry News

- •In May 2024, Le Creuset expanded its product line with the launch of a new range of stainless steel saute pans featuring improved heat retention and eco-friendly manufacturing processes. The launch received strong market reception in France and Germany, reinforcing Le Creuset’s position in the premium cookware segment. Source: Official Company Press Release

- •In November 2023, Berndes partnered with a leading European kitchen equipment distributor to enhance market reach across Central and Eastern Europe. This strategic collaboration aims to accelerate sales of Berndes’ stainless steel saute pans in emerging markets by leveraging the distributor’s extensive network. Source: Industry Publication

- •In July 2022, Ballarini announced the introduction of a limited edition stainless steel saute pan series incorporating advanced non-stick technology and ergonomic handles, targeting premium customers in Italy and Spain. The line emphasizes durability and cooking performance, aligning with evolving consumer preferences. Source: Company Website

- •In January 2021, Scanpan launched a new online platform dedicated to direct sales of stainless steel cookware, including saute pans, with customized options and fast delivery across Europe. This digital push supports Scanpan’s growth strategy in the competitive online retail space. Source: Official Press Release

Market Statistics

- •CAGR by 2034: 7.4%

- •Market Size by 2034: USD 3.8 Billion

- •Market Size in 2025: USD 1.9 Billion

- •Dominating Type: Induction Compatible Stainless Steel Saute Pans

- •Next-Following Type: Non-Stick Coated Stainless Steel Saute Pans

- •Dominating Application: Home Kitchens

- •Next-Following Application: Commercial Kitchens

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: France

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) by Type: Induction Compatible - 45%, Non-Stick Coated - 25%

- •Market Share (%) by Application: Home Kitchens - 50%, Commercial Kitchens - 30%

- •Growth Rate (%) by Type: Induction Compatible - 6.8%, Non-Stick Coated - 9.1%

- •Growth Rate (%) by Application: Home Kitchens - 7.0%, Commercial Kitchens - 8.3%

Top 5 Global Players

- •WMF Group (Germany)

- •Fissler GmbH (Germany)

- •Zwilling J.A. Henckels AG (Germany)

- •Tefal (France)

- •Le Creuset (France)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 3.8 Billion |

| CAGR | 7.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.1% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | WMF Group (Germany), Fissler GmbH (Germany), Zwilling J.A. Henckels AG (Germany), Tefal (France), Beka Cookware (Belgium), Scanpan A/S (Denmark), Le Creuset (France), Berndes (Germany), De Buyer (France), Silit GmbH (Germany), Sambonet Paderno Industrie S.p.A. (Italy), Ballarini (Italy), Rösle (Germany), Alessi (Italy), Cristel (France), Zwiesel Kristallglas AG (Germany), Kuhn Rikon AG (Switzerland), KitchenAid Europe (Netherlands), Villeroy & Boch AG (Germany), Gastroback GmbH (Germany), Joseph Joseph Ltd (UK), Stelton A/S (Denmark), Lodge Manufacturing Co. (Europe Division) (UK), Bialetti Industrie S.p.A. (Italy), Cuisinox Ltd. (UK) |

Europe Stainless Steel Saute Pan Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.