GCC Refined Functional Carbohydrates Market Size, Growth & Revenue 2024-2034

GCC Refined Functional Carbohydrates Market is segmented by Type (Oligosaccharides, Polysaccharides, Sugar Alcohols, Resistant Starches, Functional Fibers), Application (Food & Beverage, Pharmaceuticals, Nutraceuticals, Animal Feed, Cosmetics), End User (Manufacturers, Retailers, Healthcare Providers, Animal Nutrition Companies), Distribution Channel (Direct Sales, Distributors, Online Platforms, Wholesale), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

- •The GCC Refined Functional Carbohydrates market involves the manufacture and application of specialized carbohydrates such as oligosaccharides, polysaccharides, sugar alcohols, resistant starches, and functional fibers. These ingredients are pivotal for health-focused products in food & beverage, pharmaceuticals, nutraceuticals, animal feed, and cosmetics sectors across GCC countries. The market is driven by rising health consciousness and the demand for functional ingredients that promote digestive health, immunity, and metabolic balance. Advanced refining technologies and strict quality standards define the production scope, with increasing investments targeting innovation and customization. This market's boundaries cover extraction, purification, and application of refined carbohydrates tailored for regional consumer preferences and regulatory frameworks, highlighting its strategic importance within GCC's growing health and wellness industries.

- •Key market highlights include a base market size of USD 0.45 Billion in 2024, forecasted to reach USD 1.32 Billion by 2034, exhibiting a robust CAGR of 11.5%. Saudi Arabia dominates the regional market with a 38% share, while the UAE shows the fastest growth at 14.8% CAGR. Oligosaccharides lead product types, followed by resistant starches showing the highest growth momentum. Food & beverage and pharmaceuticals remain the largest application segments, reflecting consumer demand for functional foods and health supplements.

- •The GCC refined functional carbohydrates market offers significant value propositions through its contribution to healthier food options, enhanced pharmaceutical formulations, and innovative nutraceutical products. Stakeholders benefit from expanding health awareness, growing regulatory support, and evolving consumer preferences, driving market expansion and technological advancements. This market plays a strategic role in GCC’s push toward wellness-oriented industries, fostering opportunities for manufacturers, distributors, and research entities.

Competitive Landscape

Competition in the GCC Refined Functional Carbohydrates market is intense and shaped by innovation, quality differentiation, and strategic partnerships. Leading companies focus on advanced refining technologies and proprietary formulations to meet stringent health and safety standards. Market rivalry is driven by product differentiation in functional benefits and application versatility across food, pharma, and nutraceutical sectors. Companies adopt competitive pricing strategies, invest in R&D to enhance nutritional efficacy, and expand regional distribution networks. Strategic collaborations and localized production facilities further bolster competitive positioning. The market also experiences moderate entry barriers due to regulatory compliance and capital-intensive refinement processes. Overall, competition fosters continuous product innovation, improved supply chain efficiencies, and customer-centric solutions, shaping a dynamic and evolving marketplace within the GCC.

Leading Companies in GCC Refined Functional Carbohydrates Market

- •Kerry Group (Ireland)

- •Ingredion Incorporated (United States)

- •Beneo GmbH (Germany)

- •Tate & Lyle PLC (United Kingdom)

- •Cargill, Incorporated (United States)

- •Roquette Frères (France)

- •DuPont Nutrition & Health (United States)

- •Südzucker AG (Germany)

- •Meghmani Organics Limited (India)

- •DSM Nutritional Products (Netherlands)

- •Archer Daniels Midland Company (United States)

- •SunOpta Inc. (Canada)

- •Zhengzhou Alpha Biotechnology Co., Ltd. (China)

- •Meiji Holdings Co., Ltd. (Japan)

- •Tereos S.A. (France)

- •Naturex (France)

- •CNP Ingredients Limited (India)

- •Ingredion Middle East (United Arab Emirates)

- •Al Dahra Agricultural Company (United Arab Emirates)

- •Gulf Corporation for Industrial Projects (Saudi Arabia)

- •Almarai Company (Saudi Arabia)

- •National Food Company (Qatar)

- •Oryx Stainless Steel (Qatar)

- •Agthia Group PJSC (United Arab Emirates)

- •Emirates Industrial Fibers Company (United Arab Emirates)

Market Breakdown

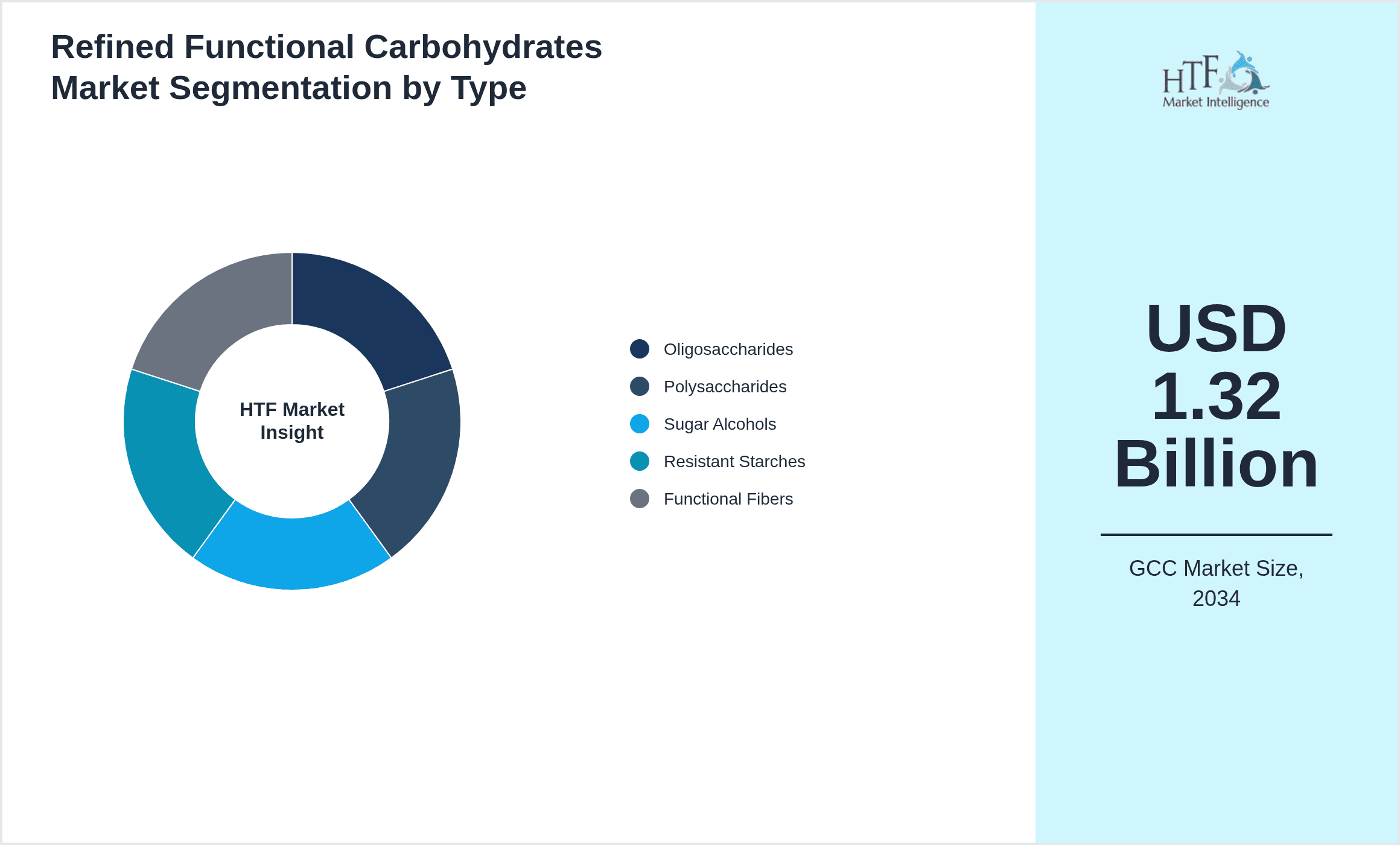

- •By Type

- ◦Oligosaccharides

- ◦Polysaccharides

- ◦Sugar Alcohols

- ◦Resistant Starches

- ◦Functional Fibers

- •By Application

- ◦Food & Beverage

- ◦Pharmaceuticals

- ◦Nutraceuticals

- ◦Animal Feed

- ◦Cosmetics

- •By End User

- ◦Manufacturers

- ◦Retailers

- ◦Healthcare Providers

- ◦Animal Nutrition Companies

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

- ◦Wholesale

Growth Drivers

The GCC refined functional carbohydrates market growth is propelled by increasing health consciousness among consumers emphasizing digestive health and immune support. Rising prevalence of lifestyle diseases encourages demand for functional foods and supplements enriched with prebiotic carbohydrates. Government initiatives promoting healthy nutrition and wellness further stimulate market expansion. Additionally, growing pharmaceutical and nutraceutical sectors in GCC countries drive integration of refined carbohydrates as excipients and active ingredients. The influx of expatriates and urbanization intensify demand for convenient health products. Technological advancements in carbohydrate refinement enhance product quality and application diversity, attracting food manufacturers and healthcare companies. Strategic collaborations between ingredient suppliers and end-product manufacturers accelerate market penetration. Furthermore, rising disposable incomes and evolving consumer preferences toward natural and clean-label ingredients amplify market growth, positioning refined functional carbohydrates as essential components in GCC’s health and wellness landscape.

Market Trends

The GCC refined functional carbohydrates market exhibits trends such as increased adoption of clean-label and plant-based ingredients, reflecting consumer preference for natural health solutions. Manufacturers are leveraging biotechnology to develop novel prebiotic fibers and resistant starches with enhanced functional benefits. There is a growing trend toward personalized nutrition and fortified food products integrating refined carbohydrates for targeted health outcomes. Sustainability initiatives encourage sourcing from renewable raw materials and eco-friendly processing methods. Digitalization in supply chain management optimizes distribution and traceability, improving product transparency. Partnerships between food companies and research institutions foster innovation pipelines. Additionally, the cosmetics industry is incorporating functional carbohydrates for skin health, expanding application horizons. These trends collectively drive product diversification and strengthen market competitiveness within the GCC region.

Market Restraints

Market growth faces challenges including high production costs due to advanced refining technologies and raw material sourcing complexities. Regulatory hurdles and stringent quality compliance across GCC countries create entry barriers for new manufacturers. Limited consumer awareness about functional carbohydrates in certain GCC segments restricts market penetration. Competition from alternative functional ingredients like probiotics and synthetic additives poses substitution threats. Supply chain disruptions and reliance on imports for raw materials impact consistent product availability. Additionally, fluctuations in raw material prices and currency volatility affect profitability. The relatively nascent stage of functional carbohydrate applications in traditional sectors slows adoption rates. These restraints necessitate strategic investments in education, cost optimization, and regulatory navigation to sustain market growth.

Market Opportunities

Emerging opportunities in the GCC refined functional carbohydrates market include expansion into untapped segments such as personalized nutrition and functional cosmetics. Growing demand for natural and organic health products opens avenues for novel carbohydrate formulations. Investment in R&D to develop multi-functional carbohydrates with enhanced prebiotic and metabolic benefits can capture new consumer bases. Geographical expansion within GCC countries with increasing urbanization and health awareness presents growth potential. Collaborations with local food manufacturers and pharmaceutical firms facilitate tailored product development. Additionally, leveraging digital marketing and e-commerce platforms enhances consumer outreach. Government support for food innovation and wellness industries further incentivizes market entry and expansion. These opportunities align with global health trends, positioning the GCC market for dynamic future growth.

Market Challenges

Key challenges confronting the GCC refined functional carbohydrates market include navigating diverse regulatory frameworks across member countries, which complicates product registration and compliance. The fragmented supply chain and dependence on imported raw materials increase vulnerability to geopolitical and logistical disruptions. Limited local manufacturing infrastructure hinders scalability and cost efficiency. Consumer skepticism toward novel functional ingredients requires robust education and marketing efforts. Intense competition from established global ingredient suppliers demands continuous innovation and competitive pricing. Additionally, balancing functional benefits with taste and texture in end products remains technically challenging. These challenges necessitate strategic partnerships, investment in local production capabilities, and focused consumer engagement to sustain competitive advantage and market growth.

Regulatory Overview

The GCC refined functional carbohydrates market is influenced by evolving regulatory frameworks emphasizing food safety, ingredient transparency, and health claims validation. From 2020 to 2024, GCC authorities, including the Saudi Food and Drug Authority (SFDA) and Emirates Authority for Standardization and Metrology (ESMA), implemented stricter guidelines on functional ingredient approvals, labeling, and permissible health claims. Compliance with Gulf Technical Regulations (GSO standards) ensures harmonization across member states. Recent updates focus on allergen declarations, permissible additive limits, and certification requirements for nutraceuticals and food supplements containing functional carbohydrates. These regulations enhance consumer protection and market credibility but require manufacturers to invest in quality assurance and documentation. Ongoing regulatory dialogue supports innovation while safeguarding public health, fostering a balanced environment for market development within the GCC.

Market Intelligence

- •March 2024, Ingredion Middle East launched a new line of oligosaccharide-based prebiotic fibers tailored for GCC food manufacturers, emphasizing digestive health benefits and clean-label formulations. The product features enhanced solubility and stability suited for beverage and dairy applications, aiming to meet rising consumer demand for functional foods. The launch strengthens Ingredion’s regional portfolio and distribution network, supporting industry growth in the GCC. Source: Official Company Website

- •November 2023, Roquette Frères announced expansion of its functional carbohydrates production facility in the United Arab Emirates, integrating cutting-edge refining technologies to increase output capacity by 30%. The expansion targets rising demand from pharmaceutical and nutraceutical sectors within GCC countries, enhancing supply chain efficiency and product innovation capabilities. This strategic move aligns with Roquette’s commitment to regional market growth and sustainability. Source: Industry Publication

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •August 2023 saw Cargill Incorporated acquire a regional functional carbohydrate producer based in Saudi Arabia, aiming to strengthen its GCC market presence and broaden its product portfolio with specialized oligosaccharides and resistant starches. This acquisition enhances Cargill’s supply chain capabilities and allows for localized innovation and faster time-to-market within the GCC food and pharmaceutical sectors. The strategic move supports Cargill’s long-term growth ambitions in the Middle East’s expanding health and wellness industries.

- •February 2022, Ingredion Incorporated completed the acquisition of a nutraceutical ingredient manufacturer in the UAE, expanding its footprint in the GCC refined functional carbohydrates market. This deal brings advanced refining technologies and a diversified product range, enabling Ingredion to cater to increasing demand from food, beverage, and pharmaceutical companies. The integration aims to improve regional operational efficiencies and accelerate innovation pipelines tailored to GCC consumer preferences.

Recent Industry News

- •April 2024, DSM Nutritional Products partnered with a leading GCC food manufacturer to develop prebiotic-enriched dairy products incorporating advanced oligosaccharides. This collaboration aims to enhance gut health benefits and meet consumer demand for functional foods in the region. The partnership includes joint R&D initiatives and marketing campaigns targeting health-conscious GCC consumers. Source: Official DSM Press Release

- •July 2023, Roquette Frères expanded its distribution network in Saudi Arabia through a strategic alliance with Gulf Corporation for Industrial Projects, enhancing availability of functional fibers and sugar alcohols across multiple GCC countries. The alliance focuses on optimizing supply chain logistics and providing tailored ingredient solutions to regional food and pharmaceutical companies, supporting market growth and consumer accessibility. Source: Industry Publication

- •September 2022, Al Dahra Agricultural Company announced the launch of a new resistant starch product line designed for animal feed applications within the GCC. This innovation addresses nutritional optimization and digestive health in livestock, aligning with regional agricultural modernization efforts. The product launch supports sustainable animal husbandry practices and expands Al Dahra’s functional carbohydrate offerings. Source: Company Announcement

- •December 2021, Ingredion Middle East introduced a digital platform for GCC manufacturers aimed at facilitating customized formulation of functional carbohydrates for food and pharmaceutical applications. This platform leverages AI-driven analytics to optimize ingredient selection and product development, enhancing efficiency and innovation. The initiative reflects growing digital transformation trends in the regional ingredients market. Source: Industry News Portal

Market Statistics

- •CAGR by 2034: 11.5%

- •Market Size by 2034: USD 1.32 Billion

- •Market Size in 2025: USD 0.50 Billion

- •Dominating Type: Oligosaccharides; Next-Following Type: Resistant Starches

- •Dominating Application: Food & Beverage; Next-Following Application: Pharmaceuticals

- •Dominating Region: Saudi Arabia; Second-Leading Region: United Arab Emirates

- •Region with Highest Growth Rate: United Arab Emirates

- •Dominating Country: Saudi Arabia

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: Oligosaccharides 42%, Resistant Starches 25%

- •Market Share (%) of Dominating vs Followed Application: Food & Beverage 45%, Pharmaceuticals 28%

- •Growth Rate (%) of Dominating vs Followed Type: Oligosaccharides 10.2%, Resistant Starches 14.1%

- •Growth Rate (%) of Dominating vs Followed Application: Food & Beverage 9.8%, Pharmaceuticals 12.4%

Top 5 Global Players

- •Ingredion Incorporated (United States)

- •Kerry Group (Ireland)

- •Roquette Frères (France)

- •Tate & Lyle PLC (United Kingdom)

- •Cargill, Incorporated (United States)

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.45 Billion |

| Forecast Year Market Size | USD 1.32 Billion |

| CAGR | 11.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Kerry Group (Ireland), Ingredion Incorporated (United States), Beneo GmbH (Germany), Tate & Lyle PLC (United Kingdom), Cargill, Incorporated (United States), Roquette Frères (France), DuPont Nutrition & Health (United States), Südzucker AG (Germany), Meghmani Organics Limited (India), DSM Nutritional Products (Netherlands), Archer Daniels Midland Company (United States), SunOpta Inc. (Canada), Zhengzhou Alpha Biotechnology Co., Ltd. (China), Meiji Holdings Co., Ltd. (Japan), Tereos S.A. (France), Naturex (France), CNP Ingredients Limited (India), Ingredion Middle East (United Arab Emirates), Al Dahra Agricultural Company (United Arab Emirates), Gulf Corporation for Industrial Projects (Saudi Arabia), Almarai Company (Saudi Arabia), National Food Company (Qatar), Oryx Stainless Steel (Qatar), Agthia Group PJSC (United Arab Emirates), Emirates Industrial Fibers Company (United Arab Emirates) |

GCC Refined Functional Carbohydrates Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.