Europe Frozen Food Packaging Bag Market Size, Growth & Revenue 2024-2034

Europe Frozen Food Packaging Bag Market is segmented by Type (Polyethylene Bags, Polypropylene Bags, Laminated Bags, Biodegradable Bags, Vacuum Sealed Bags), Application (Frozen Meat, Frozen Seafood, Frozen Vegetables, Frozen Ready Meals, Frozen Bakery), End User (Food Processing Companies, Retail Chains, Foodservice Providers, Household Consumers), Distribution Channel (Direct Sales, Distributors, Online Retail, Wholesale), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Frozen Food Packaging Bag market includes packaging solutions designed to preserve frozen foods such as meat, seafood, vegetables, ready meals, and bakery items. Materials range from polyethylene and polypropylene to biodegradable options, emphasizing product protection and sustainability.

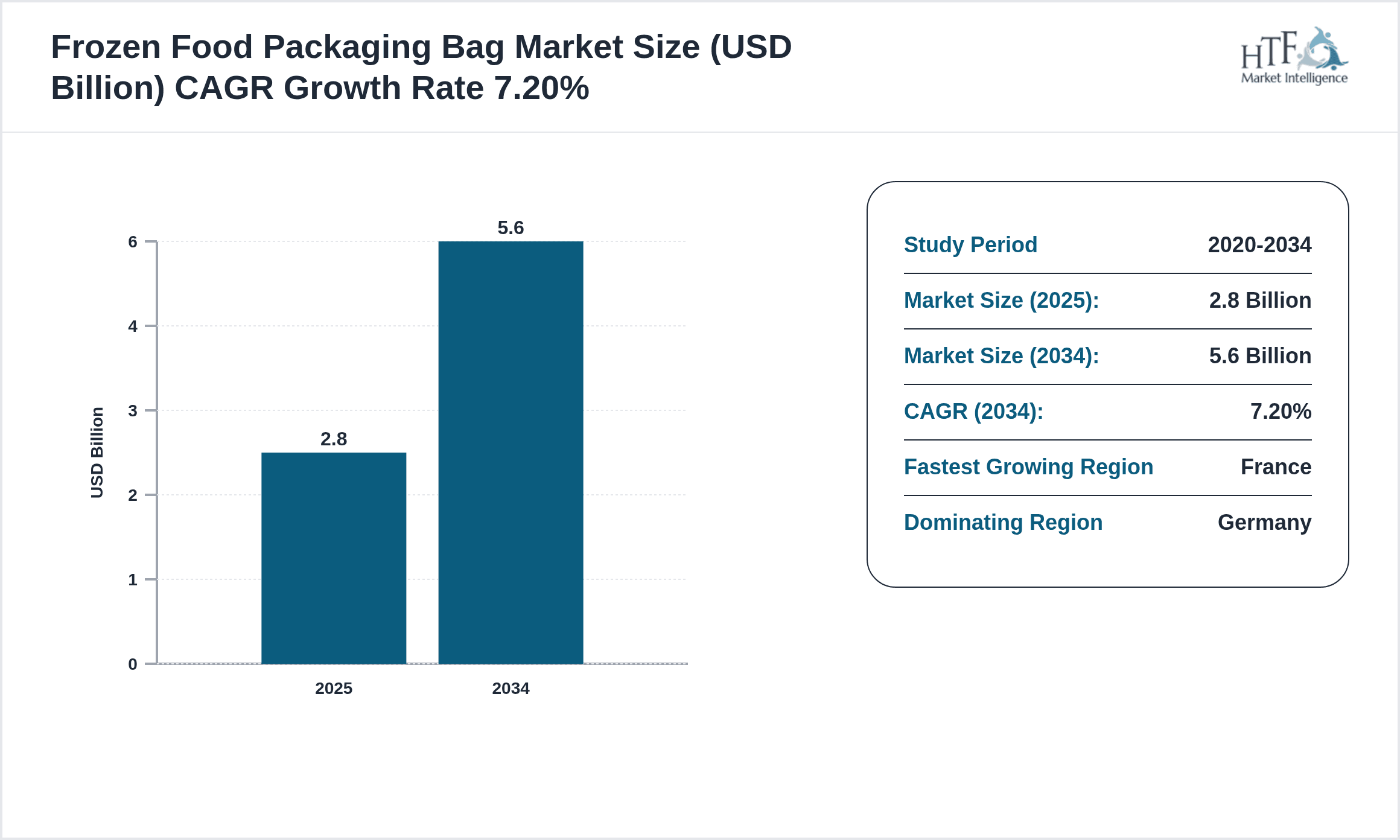

- •Key market highlights show a projected CAGR of 7.2% from 2024 to 2034, driven by rising demand for frozen convenience foods, sustainability initiatives, and innovations in packaging technology across major European countries.

- •This market offers strategic value by supporting the frozen food supply chain with protective, eco-friendly packaging that meets regulatory standards, catering to evolving consumer preferences and retail sector growth.

Competitive Landscape

Competition in the Europe Frozen Food Packaging Bag market is characterized by intense rivalry among established packaging manufacturers leveraging innovation in sustainable materials and barrier technologies. Market players focus on product differentiation through biodegradable and vacuum-sealed bag offerings to meet stringent environmental regulations. Strategic partnerships and regional customization enhance market positioning. The competitive environment encourages continuous R&D investment and expansion into emerging applications to capture growing frozen food segments. Pricing strategies balance cost-effectiveness with quality assurance, while strong distribution networks across Europe reinforce company footprints. Barriers to entry include compliance with EU packaging directives and high capital requirements for advanced film technologies. Overall, the landscape is marked by collaborative innovation and dynamic market responsiveness to consumer and regulatory demands.

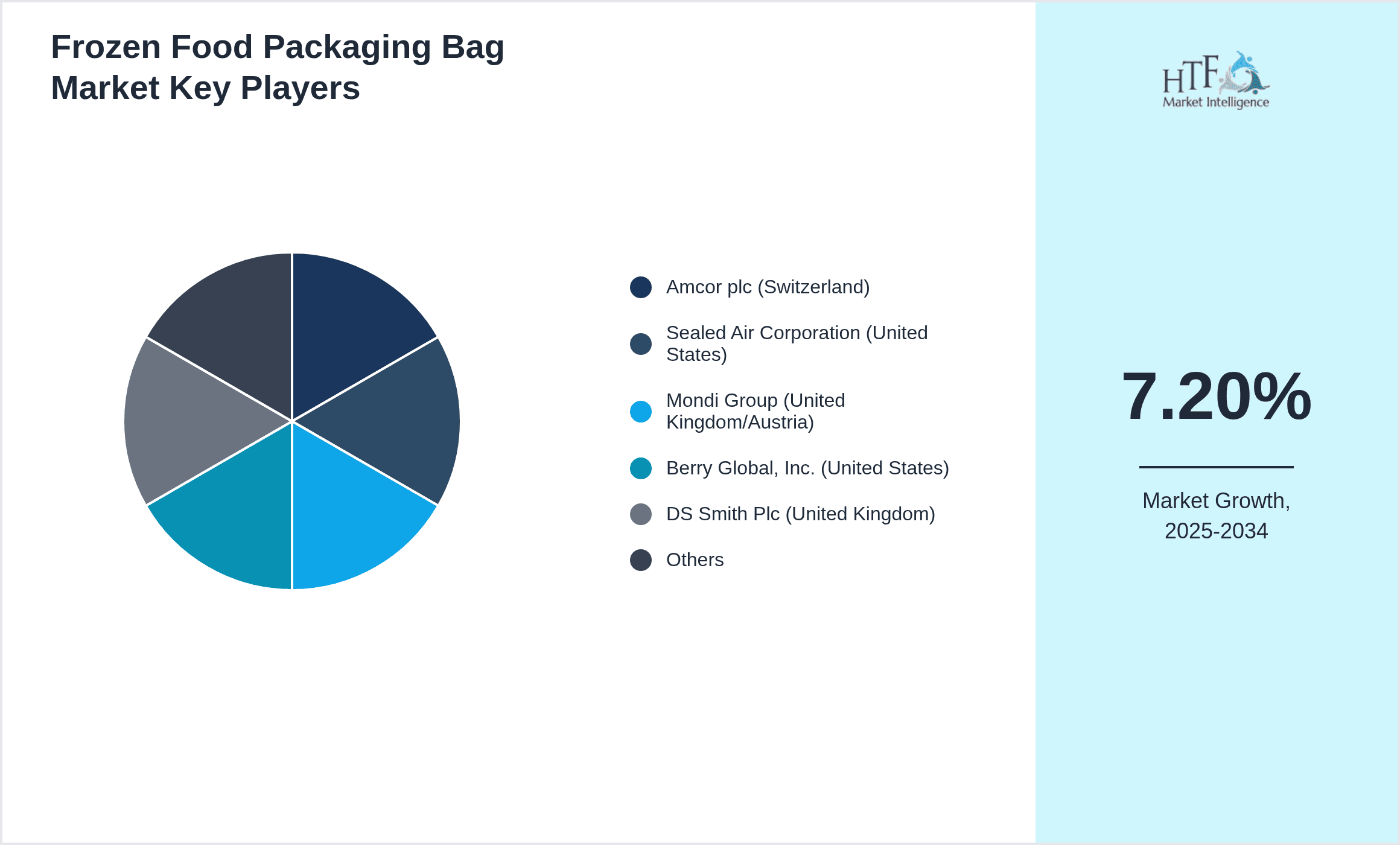

Leading Companies in Europe Frozen Food Packaging Bag Market

- •Amcor plc (Switzerland)

- •Sealed Air Corporation (United States)

- •Mondi Group (United Kingdom/Austria)

- •Berry Global, Inc. (United States)

- •DS Smith Plc (United Kingdom)

- •Coveris Holdings S.A. (Austria)

- •Bemis Company, Inc. (United States)

- •Huhtamaki Oyj (Finland)

- •Klöckner Pentaplast Group (Germany)

- •Winpak Ltd. (Canada)

- •Constantia Flexibles Group GmbH (Austria)

- •Sonoco Products Company (United States)

- •Novolex Holdings, LLC (United States)

- •LINPAC Packaging Limited (United Kingdom)

- •ProAmpac (United States)

- •Printpack Inc. (United States)

- •Coveris Europe (Austria)

- •Südzucker AG (Germany)

- •RKW Group (Germany)

- •Toppan Printing Co., Ltd. (Japan)

- •WestRock Company (United States)

- •MJS Packaging (United Kingdom)

- •Plastipak Holdings, Inc. (United States)

- •Uflex Limited (India)

- •Flex Films (India)

Market Breakdown

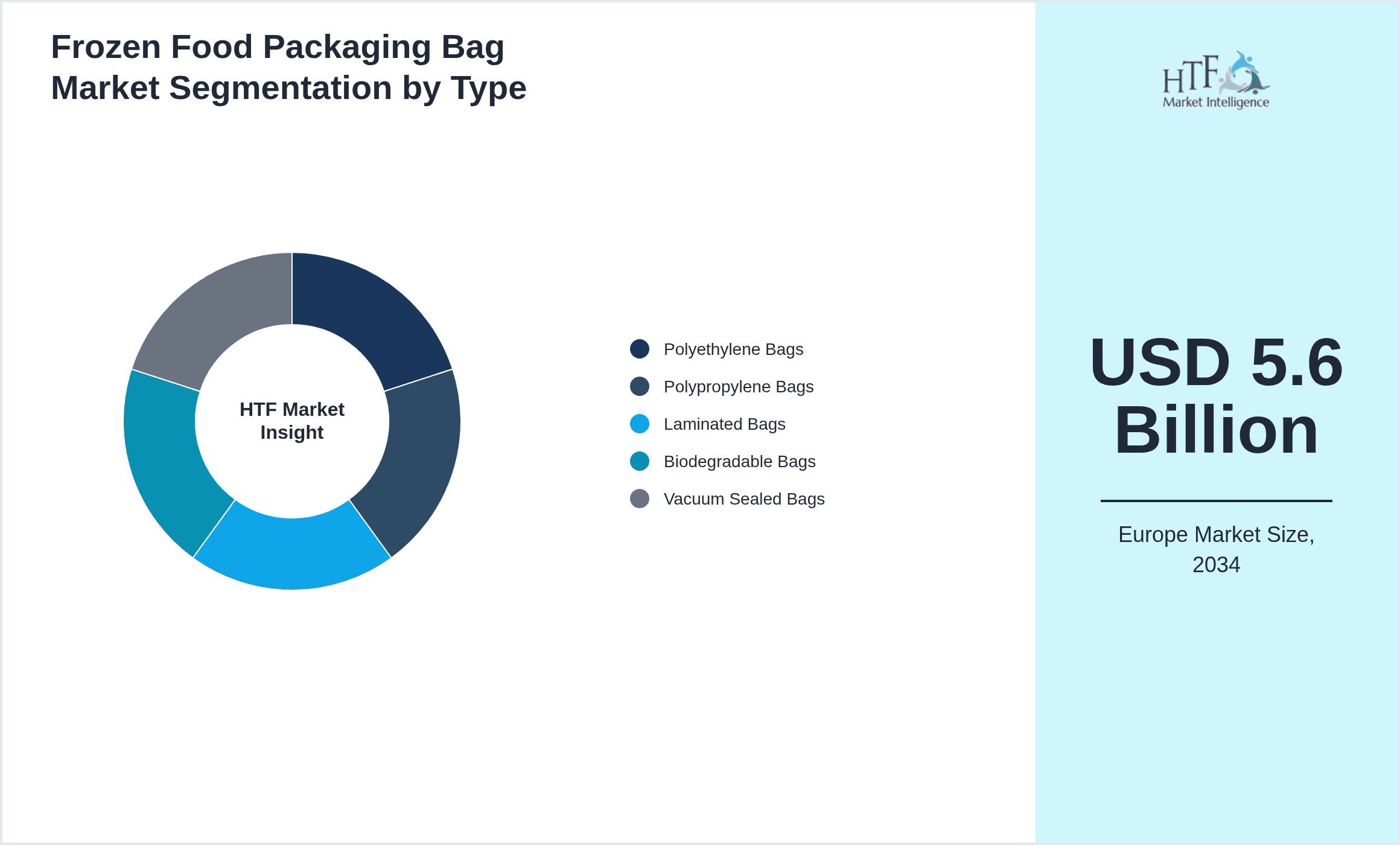

- •By Type

- ◦Polyethylene Bags

- ◦Polypropylene Bags

- ◦Laminated Bags

- ◦Biodegradable Bags

- ◦Vacuum Sealed Bags

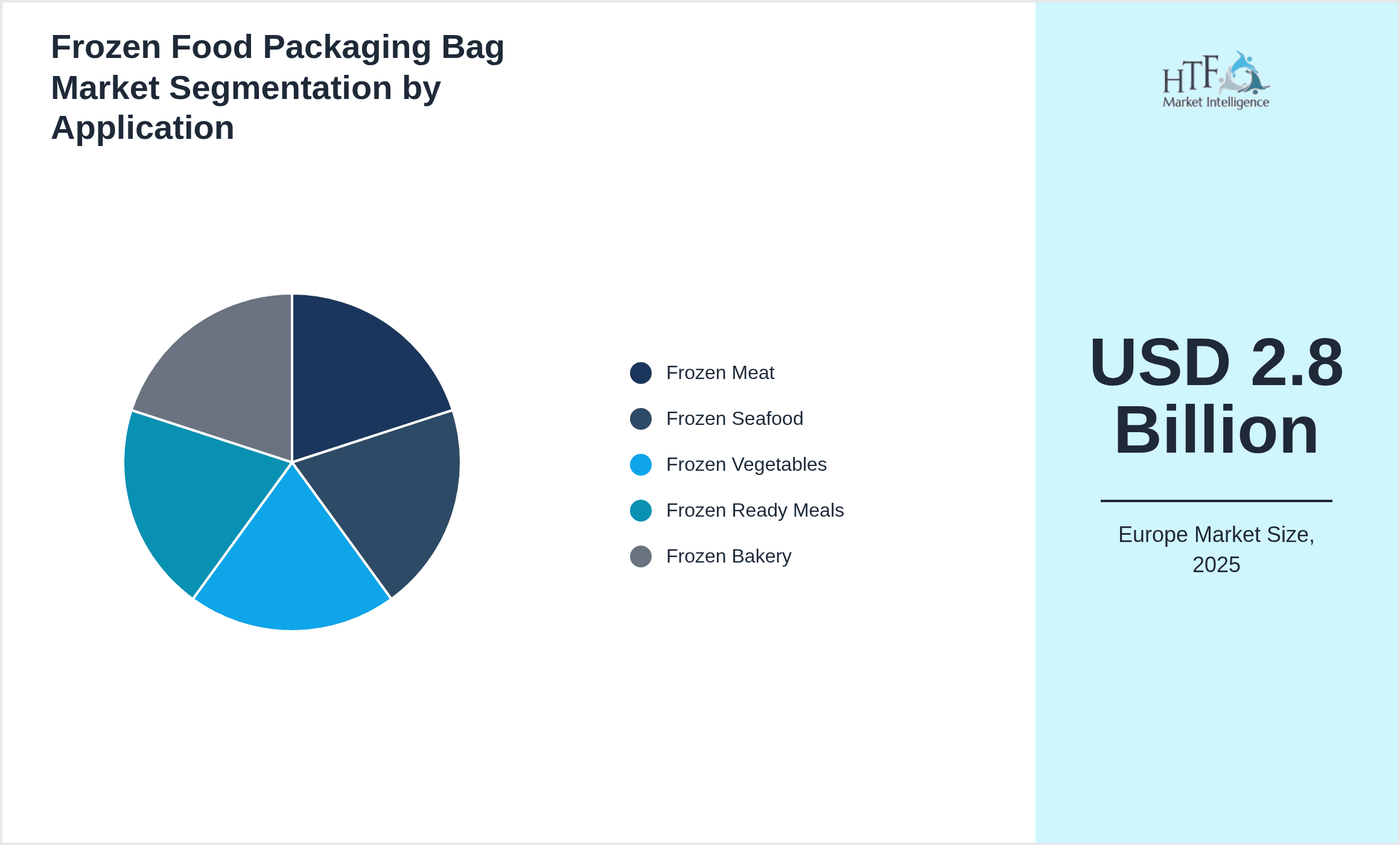

- •By Application

- ◦Frozen Meat

- ◦Frozen Seafood

- ◦Frozen Vegetables

- ◦Frozen Ready Meals

- ◦Frozen Bakery

- •By End User

- ◦Food Processing Companies

- ◦Retail Chains

- ◦Foodservice Providers

- ◦Household Consumers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Retail

- ◦Wholesale

Growth Drivers

- •Increasing consumer demand for convenient frozen food options across Europe fuels the adoption of advanced frozen food packaging bags that extend product shelf life and maintain quality during transportation.

- •Strict European Union regulations promoting sustainable packaging materials drive innovation and investment in biodegradable and recyclable frozen food packaging bags.

- •Expansion of organized retail and supermarket chains across Germany, France, and the UK supports market growth by facilitating widespread distribution of frozen food products requiring specialized packaging.

- •Technological advances in barrier films and vacuum sealing methods enhance packaging performance, reducing food wastage and appealing to environmentally conscious consumers.

- •Rising exports of frozen food products within Europe and to global markets necessitate robust packaging solutions to ensure product integrity during long-distance logistics.

Market Trends

- •The adoption of biodegradable and compostable frozen food packaging bags is accelerating, reflecting broader sustainability trends and consumer preferences for eco-friendly products.

- •Smart packaging technologies incorporating QR codes and temperature indicators are emerging to enhance traceability and consumer engagement in frozen food retailing.

- •Increasing use of multilayer laminated bags that combine barrier properties with mechanical strength is becoming prevalent among premium frozen food brands.

- •Collaborations between packaging manufacturers and frozen food producers are fostering co-development of customized packaging solutions tailored to specific product categories.

- •Digital printing on frozen food packaging bags is gaining traction for flexible branding and faster time-to-market in response to dynamic consumer trends.

Market Restraints

- •High production costs for biodegradable and advanced laminated packaging materials limit adoption among price-sensitive frozen food manufacturers and retailers.

- •Complex recycling and waste management infrastructure variations across European countries pose challenges for standardizing sustainable packaging practices.

- •Stringent regulatory compliance requirements increase operational costs and delay product launches, especially for smaller packaging firms.

- •Limited consumer awareness on packaging recyclability sometimes leads to improper disposal, reducing environmental benefits of sustainable packaging.

- •Supply chain disruptions impacting raw material availability can cause price volatility and affect timely delivery of frozen food packaging bags.

Market Opportunities

- •Rising demand for plant-based and organic frozen food products creates opportunities for specialized biodegradable packaging solutions that appeal to health-conscious consumers.

- •Expansion into Eastern European countries with growing frozen food consumption offers untapped market potential for packaging manufacturers.

- •Integration of antimicrobial coatings in frozen food packaging bags to prolong freshness and enhance food safety is an emerging innovation area.

- •Collaborative ventures between packaging firms and technology providers to develop smart, connected packaging can differentiate product offerings.

- •Increasing investment in circular economy initiatives by European governments supports the development and adoption of recyclable frozen food packaging solutions.

Market Challenges

- •Balancing sustainability goals with cost-efficiency remains a critical challenge for packaging manufacturers catering to diverse frozen food segments.

- •Navigating heterogeneous regulatory frameworks across European countries complicates product certification and market entry strategies.

- •Achieving desired barrier properties while maintaining biodegradability standards requires advanced material science and manufacturing capabilities.

- •Intense competition from low-cost imports pressures regional manufacturers to continuously innovate and optimize operational costs.

- •Consumer skepticism regarding the performance of eco-friendly packaging may slow adoption rates without effective education campaigns.

Regulatory Overview

- •The European Union's Single-Use Plastics Directive (enforced since 2021) restricts certain plastic packaging materials, compelling frozen food packaging manufacturers to adopt recyclable or biodegradable alternatives.

- •REACH regulations require comprehensive chemical safety assessments for packaging materials placed on the market, impacting product formulation and supplier selection.

- •The EU Packaging and Packaging Waste Directive mandates minimum recycled content percentages and encourages eco-design, influencing innovation in frozen food packaging bags.

- •National-level regulations in Germany, France, and the UK complement EU directives with extended producer responsibility schemes, increasing accountability for packaging waste management.

- •Ongoing updates to labeling and traceability standards require packaging to incorporate clear recyclability information, affecting design and printing processes.

Industry Insights

- •In March 2024, Mondi Group launched a new line of fully recyclable frozen food packaging bags combining barrier performance with enhanced sustainability credentials, targeting leading European frozen food brands. This innovation addresses growing regulatory pressures and consumer demand for eco-friendly packaging solutions, positioning Mondi as a frontrunner in sustainable packaging technology within the region.

- •In September 2023, Amcor plc announced a strategic partnership with a major food retailer to co-develop biodegradable frozen food packaging bags customized for frozen seafood products, aligning with the retailer's sustainability goals and enhancing brand differentiation in competitive markets.

Mergers & Acquisitions

- •In July 2024, Sealed Air Corporation acquired a European biodegradable film producer to enhance its sustainable packaging portfolio in frozen food applications. This acquisition strengthens Sealed Air's market position by integrating advanced eco-friendly materials and expanding its customer base across key European countries, enabling accelerated innovation and compliance with evolving regulatory requirements.

- •In November 2023, Berry Global, Inc. completed the acquisition of a specialized laminated bag manufacturer based in Germany, aiming to broaden its product offerings for frozen ready meals packaging. This strategic move reinforces Berry Global's footprint in Europe and supports its commitment to delivering high-barrier, performance-driven packaging solutions.

Recent Industry News

- •15th January 2025, Huhtamaki Oyj expanded its manufacturing capacity in Finland by commissioning a new production line dedicated to biodegradable frozen food packaging bags. The expansion responds to surging demand from European frozen food producers seeking sustainable packaging alternatives. This strategic investment aims to reduce lead times and improve supply chain responsiveness within the region. Source: Huhtamaki Official Press Release

- •20th March 2025, Mondi Group announced a collaboration with a leading European frozen seafood brand to develop smart packaging integrating freshness indicators and QR codes. This initiative enhances consumer trust and transparency while promoting digital engagement. The pilot project is set to launch across multiple countries in Europe by mid-2025. Source: Industry Packaging News

- •10th May 2025, Coveris Holdings S.A. launched a new range of laminated frozen food packaging bags with improved recyclability and mechanical strength. The product line targets frozen bakery and ready meal segments, supporting clients’ sustainability targets while maintaining packaging durability standards. Source: Coveris Corporate Announcement

- •5th August 2025, DS Smith Plc entered a strategic partnership with a retail conglomerate in the UK to supply recyclable polyethylene frozen food packaging bags. This agreement is expected to drive significant volume growth and accelerate adoption of circular economy packaging practices in European retail chains. Source: DS Smith Annual Report

Market Statistics

- •CAGR by 2034: 7.2%

- •Market Size by 2034: USD 5.6 Billion

- •Market Size in 2025: USD 3.0 Billion

- •Dominating Type: Polyethylene Bags

- •Next-Following Type: Biodegradable Bags

- •Dominating Application: Frozen Meat

- •Next-Following Application: Frozen Vegetables

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: France

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Polyethylene Bags: 45%

- ◦Biodegradable Bags: 20%

- •Market Share (%) of Dominating vs Followed Application

- ◦Frozen Meat: 38%

- ◦Frozen Vegetables: 25%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Polyethylene Bags: 6.5%

- ◦Biodegradable Bags: 12.0%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Frozen Meat: 5.8%

- ◦Frozen Vegetables: 8.5%

Top 5 Global Players

- •Amcor plc (Switzerland)

- •Sealed Air Corporation (United States)

- •Mondi Group (United Kingdom/Austria)

- •Berry Global, Inc. (United States)

- •DS Smith Plc (United Kingdom)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.8 Billion |

| Forecast Year Market Size | USD 5.6 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Type (Polyethylene Bags, Polypropylene Bags, Laminated Bags, Biodegradable Bags, Vacuum Sealed Bags), Application (Frozen Meat, Frozen Seafood, Frozen Vegetables, Frozen Ready Meals, Frozen Bakery), End User (Food Processing Companies, Retail Chains, Foodservice Providers, Household Consumers), Distribution Channel (Direct Sales, Distributors, Online Retail, Wholesale) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Amcor plc (Switzerland), Sealed Air Corporation (United States), Mondi Group (United Kingdom/Austria), Berry Global, Inc. (United States), DS Smith Plc (United Kingdom), Coveris Holdings S.A. (Austria), Bemis Company, Inc. (United States), Huhtamaki Oyj (Finland), Klöckner Pentaplast Group (Germany), Winpak Ltd. (Canada), Constantia Flexibles Group GmbH (Austria), Sonoco Products Company (United States), Novolex Holdings, LLC (United States), LINPAC Packaging Limited (United Kingdom), ProAmpac (United States), Printpack Inc. (United States), Coveris Europe (Austria), Südzucker AG (Germany), RKW Group (Germany), Toppan Printing Co., Ltd. (Japan), WestRock Company (United States), MJS Packaging (United Kingdom), Plastipak Holdings, Inc. (United States), Uflex Limited (India), Flex Films (India) |

Europe Frozen Food Packaging Bag Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.