Europe Commercial Curtain Wall System Market Scope & Changing Dynamics 2024-2034

Europe Commercial Curtain Wall System Market is segmented by Application (Office Buildings, Shopping Malls, Airports, Hospitals, Educational Institutions), Type (Stick System, Unitized System, Structural Glazing, Semi-Unitized System, Panel System), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Commercial Curtain Wall System market focuses on exterior cladding solutions designed for commercial buildings, including office towers, shopping centers, airports, and healthcare institutions. These systems provide structural protection, aesthetic appeal, and energy efficiency by using materials like glass and aluminum in various configurations such as stick and unitized systems. The market boundaries include manufacturing, engineering, installation, and maintenance services across the European region, addressing diverse climatic and architectural requirements.

- •Key highlights include a projected market size growth from USD 3.8 billion in 2024 to USD 8.6 billion by 2034, reflecting a CAGR of 8.3%. The dominant product type is the unitized system, favored for its efficiency and performance, while structural glazing is the fastest growing due to its modern aesthetic and technological advancements. Germany holds the leading market share, with Spain emerging as the fastest-growing country driven by infrastructure investments.

- •This market holds strategic importance in supporting sustainable construction initiatives and urban modernization across Europe. It enables architects and builders to meet energy codes and enhance building longevity while offering innovative design flexibility. Stakeholders including manufacturers, contractors, and end-users benefit from evolving technologies and regulatory frameworks promoting green building practices.

Competitive Landscape

The Europe Commercial Curtain Wall System market is characterized by intense competition among global manufacturers and regional fabricators focusing on innovation, quality, and customization. Leading companies leverage advanced R&D to develop energy-efficient and sustainable solutions that comply with stringent European standards. Competition revolves around product differentiation, integration of smart technologies, and cost optimization. Strategic partnerships and localized production enhance market positioning, while rivalry drives continuous improvement in installation methodologies and after-sales services. The market exhibits moderate entry barriers due to capital intensity and technical expertise requirements, encouraging consolidation through mergers and acquisitions. Regional players maintain a competitive edge by tailoring solutions to specific climatic and regulatory contexts, whereas multinational firms emphasize scalability and global supply chain efficiencies. Future competitive trends indicate a shift towards digitalization, modular systems, and eco-friendly materials to meet evolving customer demands.

Leading Companies in Europe Commercial Curtain Wall System Market

- •Schüco International KG (Germany)

- •Saint-Gobain S.A. (France)

- •AluK Group Ltd. (United Kingdom)

- •Hunter Douglas N.V. (Netherlands)

- •Reynaers Aluminium (Belgium)

- •WICONA, a part of Hydro (Germany)

- •Technal, a subsidiary of Hydro (France)

- •SAPA Building System (Norway)

- •Kawneer Europe (United Kingdom)

- •Cortizo S.A. (Spain)

- •FunderMax GmbH (Austria)

- •Alcoa Corporation (Germany)

- •Aliplast Group (Belgium)

- •Etem Bulgaria (Bulgaria)

- •SAPAL S.A. (Poland)

- •Alumil S.A. (Greece)

- •Sapa AS (Norway)

- •Schlegel International (United Kingdom)

- •Aluhaus (Germany)

- •Wicona GmbH (Germany)

- •Alucobond Europe Ltd. (Switzerland)

- •Aluminium Systems & Services GmbH (Austria)

- •Aluminium Design Group Ltd. (United Kingdom)

- •Aluron Sp. z o.o. (Poland)

- •Sapa Building System (Norway)

Commercial Curtain Wall System Market Segmentation

- •By Type

- ◦Stick System

- ◦Unitized System

- ◦Structural Glazing

- ◦Semi-Unitized System

- ◦Panel System

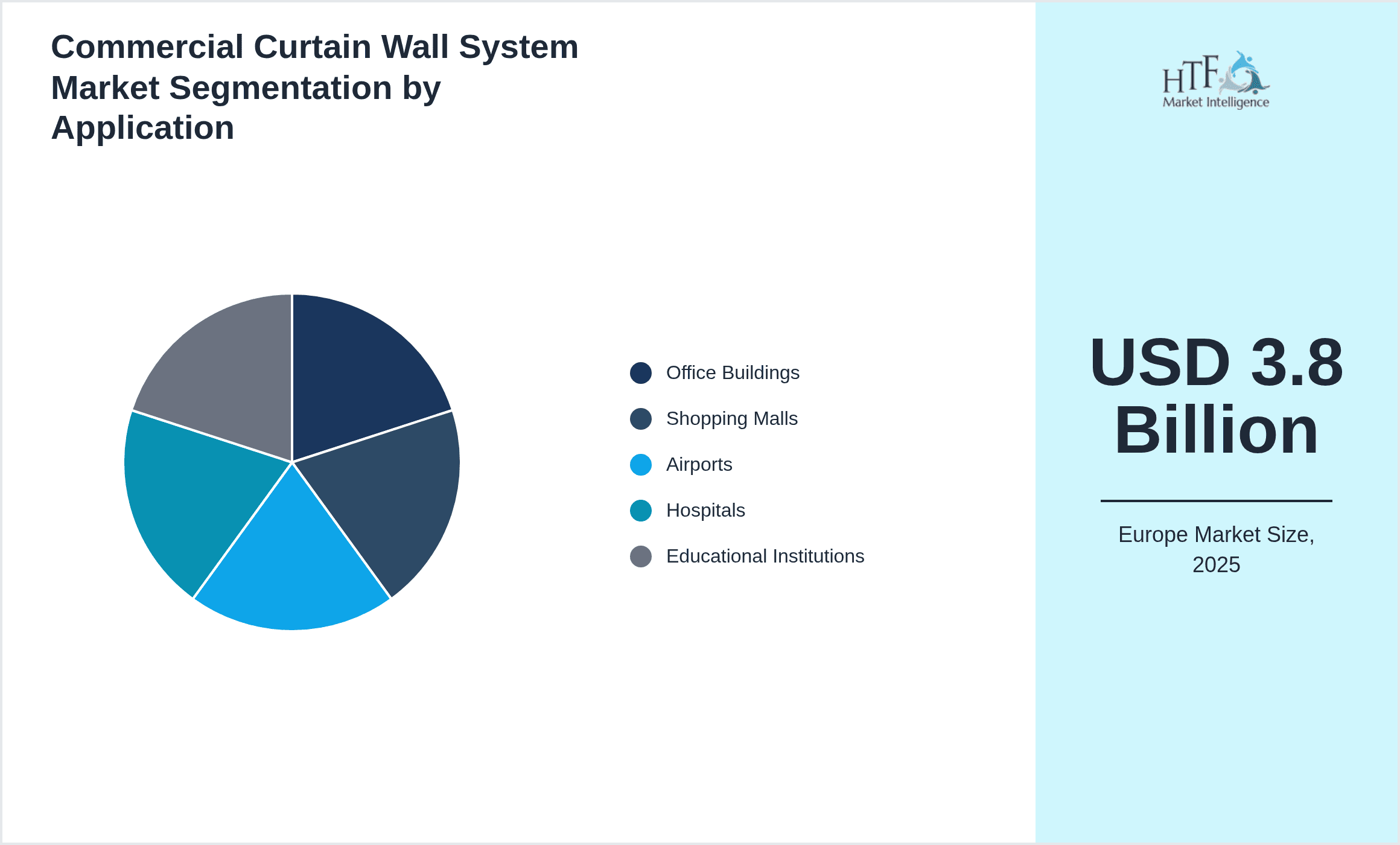

- •By Application

- ◦Office Buildings

- ◦Shopping Malls

- ◦Airports

- ◦Hospitals

- ◦Educational Institutions

- •By End User

- ◦Construction Companies

- ◦Architectural Firms

- ◦Real Estate Developers

- ◦Government Institutions

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Drivers

The Europe Commercial Curtain Wall System market growth is driven by increasing urbanization and demand for modern, sustainable commercial infrastructure. Governments across Europe enforce stringent energy efficiency regulations, encouraging adoption of advanced curtain wall systems with superior thermal insulation. Technological innovations like structural glazing and unitized systems improve construction speed and reduce costs, attracting developers. Additionally, rising investments in airport expansions, shopping malls, and office complexes bolster market demand. Green building certifications such as BREEAM and LEED further propel the market by mandating eco-friendly facade solutions. The trend toward retrofit and renovation of aging commercial buildings also stimulates demand, as property owners seek to improve facade performance and aesthetics while complying with evolving standards. These factors collectively foster robust market expansion and technological advancement in the European commercial curtain wall sector.

Market Trends

A significant trend in the Europe Commercial Curtain Wall System market is the rising incorporation of smart glass technologies, enabling dynamic control over light transmission and thermal properties. Prefabrication and modular construction are gaining traction to reduce on-site installation time and labor costs. Sustainability remains a core focus, with increased use of recyclable materials and low-emissivity coatings. Integration of Building Information Modeling (BIM) enhances design accuracy and collaboration among stakeholders. Moreover, growing interest in biophilic design principles encourages transparent and natural light-permitting facades. These trends reflect an industry-wide shift towards technologically advanced, eco-conscious, and user-centric curtain wall solutions across Europe’s commercial construction projects.

Market Restraints

High initial capital investment and complex installation processes restrict the widespread adoption of advanced commercial curtain wall systems in certain segments of the European market. Variability in regional building codes and certification requirements creates compliance challenges for manufacturers and installers. Additionally, supply chain disruptions and rising raw material costs, particularly aluminum and glass, impact profitability. Limited availability of skilled labor hampers efficient installation and maintenance, leading to project delays. Furthermore, the market faces competition from traditional facade systems that may be preferred for low-budget projects, constraining growth opportunities. These restraints necessitate strategic cost management and innovation to balance quality with affordability.

Market Opportunities

Emerging opportunities in the Europe Commercial Curtain Wall System market include expanding infrastructure projects in Eastern Europe and renovated urban centers requiring modern facades. Increasing adoption of energy-efficient and smart curtain wall solutions presents prospects for technology providers. The growing trend of green buildings opens avenues for eco-friendly materials and system integrations. Digitalization through BIM and IoT-enabled monitoring systems offers value-added services for lifecycle management. Additionally, collaborations between manufacturers and construction firms to develop customized, rapid-installation systems can capture niche market segments. Expansion into retrofit and refurbishment projects also provides untapped revenue streams, especially in heritage city zones balancing preservation with modernization.

Market Challenges

The Europe Commercial Curtain Wall System market faces challenges such as fluctuating raw material prices, particularly for aluminum and specialized glass, which affect manufacturing costs and pricing stability. Regulatory fragmentation across European countries complicates product standardization and certification processes, increasing time-to-market. The shortage of skilled labor for precise installation and maintenance limits scalability and quality assurance. Moreover, the complexity of integrating curtain wall systems with building automation and other facade elements demands advanced technical expertise. Competition from cost-effective local manufacturers and alternative facade technologies also pressures established players. Addressing these challenges requires innovation in materials, streamlined compliance strategies, and workforce development initiatives.

Regulatory Overview

Recent regulatory updates in Europe impacting the Commercial Curtain Wall System market emphasize energy efficiency and environmental sustainability. The EU’s Energy Performance of Buildings Directive (EPBD) revisions mandate higher thermal insulation standards and encourage use of low-emissivity glass and recyclable materials. Additionally, stricter fire safety regulations require enhanced facade fire resistance testing and certification. The Construction Products Regulation (CPR) enforces harmonized standards for curtain wall components across member states, facilitating market transparency but requiring compliance adaptation. National mandates in countries like Germany and France introduce localized environmental impact assessments and lifecycle analysis requirements. These regulations collectively drive innovation in curtain wall design while heightening compliance costs and complexity for manufacturers and contractors.

Industry Insights

In April 2023, Schüco International KG launched a next-generation curtain wall system featuring integrated photovoltaic panels, enabling energy generation while maintaining high transparency and insulation. This innovation aligns with the EU’s renewable energy goals and offers architects new design possibilities. In September 2022, Reynaers Aluminium expanded its modular unitized system portfolio with enhanced thermal breaks and prefabricated components, reducing installation time and improving sustainability credentials. These developments underscore the market’s shift towards multifunctional, eco-friendly systems that address both aesthetic and environmental demands in Europe’s commercial construction sector.

Mergers & Acquisitions

- •In July 2023, Saint-Gobain S.A. completed the acquisition of a leading German facade engineering company specializing in unitized curtain wall systems. This strategic move strengthened Saint-Gobain’s position in the premium commercial facade segment across Europe, enabling enhanced R&D collaboration and expanded manufacturing capabilities. The acquisition supports integration of sustainable technologies aligned with EU building codes, positioning Saint-Gobain for accelerated growth in energy-efficient construction solutions.

- •In November 2022, Hydro ASA finalized the merger of its aluminum building systems division with a prominent Belgian architectural systems manufacturer. The consolidation aimed to combine technical expertise and broaden product offerings in the structural glazing and stick systems categories. This merger enhances competitive advantage by optimizing supply chains and fostering innovation in lightweight, sustainable curtain wall components tailored for the European market.

Recent Industry News

- •On 15th March 2024, AluK Group Ltd. announced the launch of its new high-performance curtain wall system designed for cold climates, featuring triple-glazed panels and advanced thermal breaks. The system targets Northern European commercial projects focused on energy conservation and reduced carbon footprints. This launch reflects AluK’s commitment to innovating sustainable facade solutions in response to evolving regional regulations. Source: AluK Official Press Release.

- •On 22nd June 2023, Hunter Douglas N.V. entered a strategic partnership with a leading glass manufacturer to co-develop smart glass curtain wall systems incorporating dynamic tinting and solar control technologies. The collaboration aims to accelerate deployment of energy-efficient commercial facades across Europe, leveraging combined expertise in materials science and architectural engineering. Source: Hunter Douglas Corporate News.

- •On 5th October 2022, Technal, a Hydro subsidiary, inaugurated a new manufacturing facility in Spain dedicated to prefabricated unitized curtain wall components. The facility enhances production capacity by 30%, supporting growing demand in Southern European commercial construction markets. This expansion underscores the company’s focus on reducing lead times and improving sustainability through localized operations. Source: Technal Corporate Announcement.

- •On 18th January 2021, Reynaers Aluminium launched a digital design platform enabling architects and engineers to customize curtain wall systems with real-time performance simulations. This innovative tool streamlines project workflows and optimizes facade performance, fostering greater adoption of advanced commercial curtain walls in Europe. Source: Reynaers Aluminium Industry Update.

Market Statistics

- •CAGR by 2034: 8.3%

- •Market Size by 2034: USD 8.6 Billion

- •Market Size in 2025: USD 4.1 Billion

- •Dominating Type: Unitized System

- •Next-Following Type: Structural Glazing

- •Dominating Application: Office Buildings

- •Next-Following Application: Shopping Malls

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: Spain

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) Comparison

- ◦Unitized System: 45%

- ◦Structural Glazing: 25%

- •Application Market Share (%) Comparison

- ◦Office Buildings: 40%

- ◦Shopping Malls: 30%

- •Growth Rate (%) Comparison by Type

- ◦Unitized System: 7.8%

- ◦Structural Glazing: 10.2%

- •Growth Rate (%) Comparison by Application

- ◦Office Buildings: 8.0%

- ◦Shopping Malls: 7.2%

Top 5 Global Players

- •Schüco International KG (Germany)

- •Saint-Gobain S.A. (France)

- •AluK Group Ltd. (United Kingdom)

- •Hunter Douglas N.V. (Netherlands)

- •Reynaers Aluminium (Belgium)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Spain is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 8.6 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Schüco International KG (Germany), Saint-Gobain S.A. (France), AluK Group Ltd. (United Kingdom), Hunter Douglas N.V. (Netherlands), Reynaers Aluminium (Belgium), WICONA, a part of Hydro (Germany), Technal, a subsidiary of Hydro (France), SAPA Building System (Norway), Kawneer Europe (United Kingdom), Cortizo S.A. (Spain), FunderMax GmbH (Austria), Alcoa Corporation (Germany), Aliplast Group (Belgium), Etem Bulgaria (Bulgaria), SAPAL S.A. (Poland), Alumil S.A. (Greece), Sapa AS (Norway), Schlegel International (United Kingdom), Aluhaus (Germany), Wicona GmbH (Germany), Alucobond Europe Ltd. (Switzerland), Aluminium Systems & Services GmbH (Austria), Aluminium Design Group Ltd. (United Kingdom), Aluron Sp. z o.o. (Poland), Sapa Building System (Norway) |

Europe Commercial Curtain Wall System Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.