Europe 3D Design Collaboration Platform Market - Europe Size & Outlook 2024-2034

Europe 3D Design Collaboration Platform Market is segmented by Type (Cloud-based Platforms, On-premise Solutions, Hybrid Platforms, Open Source Tools, Proprietary Software), Application (Product Development, Architectural Design, Engineering Simulation, Virtual Prototyping, Educational Training), End User (Manufacturing Industry, Construction & Architecture, Automotive Sector, Aerospace & Defense, Academic Institutions), Deployment Model (Cloud-based, On-premise, Hybrid), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe 3D Design Collaboration Platform market comprises software enabling real-time, multi-user interaction with 3D models across sectors such as manufacturing, architecture, and education. It covers cloud, on-premise, hybrid, open source, and proprietary tools facilitating synchronized design workflows.

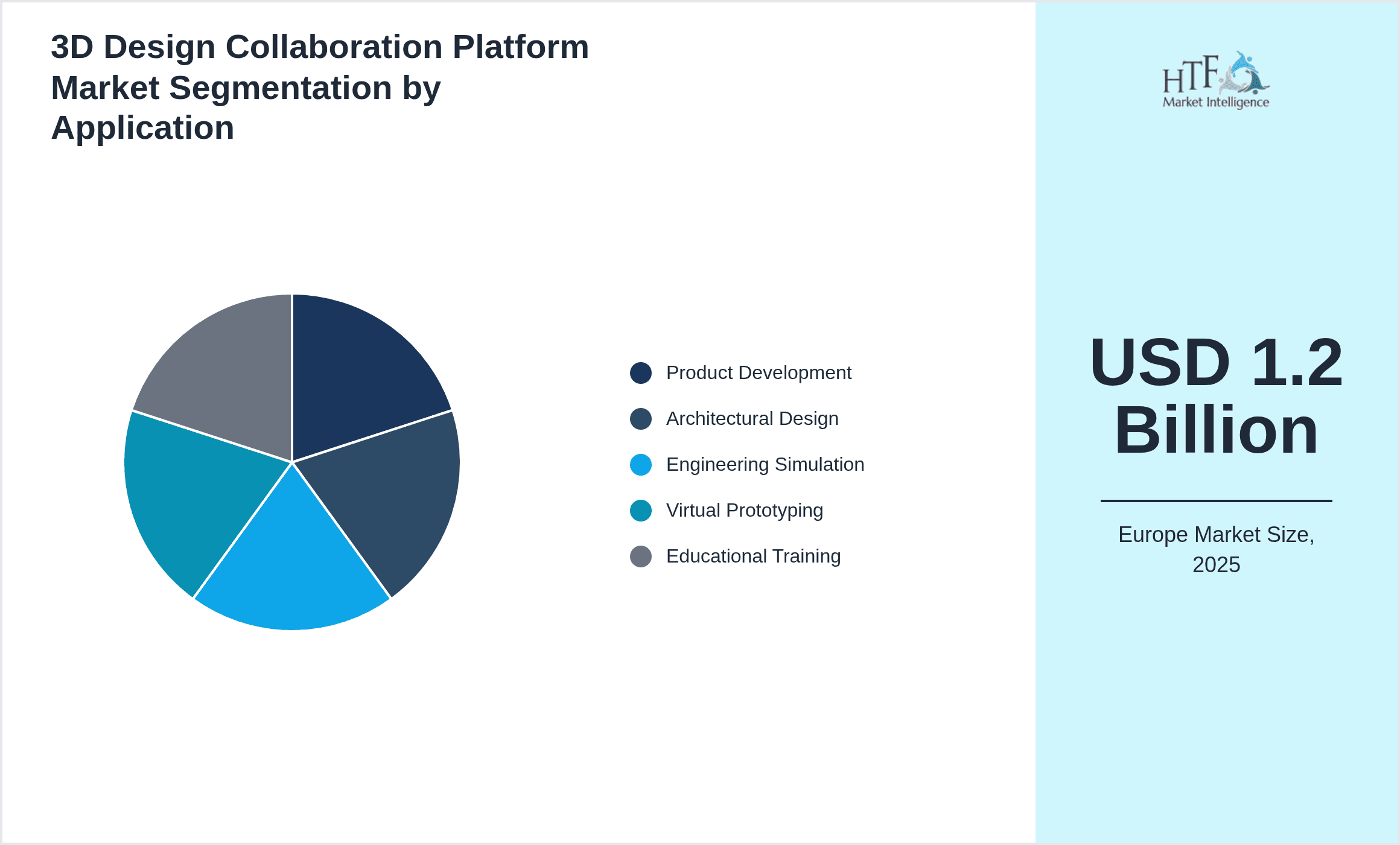

- •The market is projected to grow from USD 1.2 Billion in 2024 to USD 4.5 Billion by 2034, exhibiting a CAGR of 13.1%, driven by rising demand for integrated cloud platforms and remote collaboration solutions in Europe.

- •These platforms enhance product development efficiency and innovation by reducing design cycles, enabling cross-functional collaboration, and supporting digital transformation initiatives in European industries.

Competitive Landscape

The Europe 3D Design Collaboration Platform market features intense competition marked by innovation in cloud integration, user experience, and platform interoperability. Market players focus on strategic partnerships, continuous technology upgrades, and enhancing security features to differentiate offerings. The rivalry is fueled by the need for scalable, customizable solutions catering to diverse industry verticals. Competitive strategies include mergers, acquisitions, and investment in AI-powered collaboration features. Regional players leverage localized expertise, while global firms emphasize comprehensive ecosystem development. The market dynamics reflect a shift toward hybrid deployment models balancing flexibility and data control. Pricing strategies are competitive yet premium for advanced functionalities, with distribution channels expanding through direct sales and channel partnerships. Future competition is expected to center on AI integration, seamless CAD interoperability, and cloud-native innovations, fostering a rapidly evolving landscape.

Leading Companies in 3D Design Collaboration Platform Market

- •Dassault Systèmes (France)

- •Siemens Digital Industries Software (Germany)

- •Autodesk Inc. (United States - European Operations)

- •PTC Inc. (United States - European Operations)

- •Bentley Systems (United States - European Operations)

- •Nemetschek Group (Germany)

- •Graphisoft (Hungary)

- •Altair Engineering (United States - European Operations)

- •Ansys Inc. (United States - European Operations)

- •Trimble Inc. (United States - European Operations)

- •AVEVA Group plc (United Kingdom)

- •Hexagon AB (Sweden)

- •SolidWorks Corporation (France)

- •Bricsys NV (Belgium)

- •Onshape (United States - European Operations)

- •Synopsys, Inc. (United States - European Operations)

- •McNeel Europe (United States - European Operations)

- •Cadac Group (Netherlands)

- •CoreTechnologie GmbH (Germany)

- •Kubotek3D (Japan - European Operations)

- •Cadenas GmbH (Germany)

- •Tech Soft 3D (United States - European Operations)

- •SimScale GmbH (Germany)

- •3YOURMIND GmbH (Germany)

- •CAD Schroer (Germany)

Market Breakdown

- •By Type

- ◦Cloud-based Platforms

- ◦On-premise Solutions

- ◦Hybrid Platforms

- ◦Open Source Tools

- ◦Proprietary Software

- •By Application

- ◦Product Development

- ◦Architectural Design

- ◦Engineering Simulation

- ◦Virtual Prototyping

- ◦Educational Training

- •By End User

- ◦Manufacturing Industry

- ◦Construction & Architecture

- ◦Automotive Sector

- ◦Aerospace & Defense

- ◦Academic Institutions

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

Growth Drivers

- •The Europe 3D Design Collaboration Platform market is propelled by increasing adoption of cloud technologies that facilitate real-time, multi-user access to complex 3D models, enabling geographically dispersed teams to collaborate efficiently and reduce product development cycles.

- •Rising demand for digital transformation in manufacturing and architecture sectors encourages investment in integrated collaboration platforms, enhancing design accuracy and reducing errors through synchronized workflows across Europe.

- •Government incentives promoting Industry 4.0 and smart construction initiatives accelerate platform adoption by fostering innovation ecosystems, particularly in Germany, France, and the UK.

- •The surge in remote working trends post-pandemic has increased reliance on cloud-based 3D collaboration solutions, driving market penetration in SMEs and large enterprises alike.

- •Advancements in AR/VR integration within collaboration platforms enhance visualization capabilities, attracting sectors such as automotive and aerospace to leverage immersive design tools.

Market Trends

- •Hybrid deployment models combining cloud flexibility with on-premise data control are gaining prominence, addressing security concerns while maintaining collaboration efficiency for sensitive European industries.

- •Integration of AI and machine learning algorithms into 3D collaboration platforms is enhancing automated design validation, error detection, and workflow optimization, providing competitive advantages to early adopters.

- •Open-source 3D collaboration tools are emerging as cost-effective alternatives, fostering innovation and customization among startups and academic institutions across Europe.

- •Increased interoperability between CAD software and collaboration platforms is streamlining user experience, enabling seamless import/export and reducing compatibility issues.

- •Sustainability-focused design collaboration is trending, with platforms incorporating tools for lifecycle assessment and energy-efficient modeling to comply with European environmental regulations.

Market Opportunities

- •Growing demand for cloud-based collaboration in small and medium enterprises presents significant expansion opportunities by offering scalable, subscription-based pricing models tailored to European SMEs.

- •The rise of smart cities and infrastructure projects in Europe creates untapped potential for architectural and engineering simulation applications within 3D collaboration platforms.

- •Increasing integration of AR/VR and IoT technologies with 3D design collaboration tools opens avenues for innovative product offerings, enhancing user engagement and real-time data visualization.

- •Strategic partnerships between software providers and hardware manufacturers could deliver end-to-end solutions, driving market growth and customer retention.

- •Expanding educational training applications in universities and technical schools across Europe can foster early adoption and long-term platform loyalty.

Market Challenges

- •Data security and privacy concerns remain critical barriers, particularly in cloud-based platforms, as sensitive intellectual property must be safeguarded under stringent European regulations like GDPR.

- •High initial investment costs and complexity of integration with legacy CAD systems deter some enterprises, especially SMEs, from adopting advanced 3D collaboration platforms.

- •Lack of standardization across different collaboration tools leads to interoperability challenges, causing inefficiencies and limiting seamless cross-platform workflows.

- •Resistance to change within traditional industries slows adoption of digital collaboration tools, necessitating targeted training and change management efforts.

- •Rapid technological advancements require continuous platform updates and skilled workforce, imposing operational challenges on vendors and users alike.

Regulatory Framework

- •The Europe 3D Design Collaboration Platform market is influenced by GDPR policies enacted between 2018-2024, mandating strict data privacy and security compliance for cloud service providers handling personal and proprietary information.

- •Recent updates to the EU Cybersecurity Act (2022) impose certification requirements on software platforms, enhancing trustworthiness and market acceptance across member states.

- •Environmental regulations encouraging sustainable design practices impact platform features, necessitating integration of eco-assessment tools aligning with the EU Green Deal objectives.

- •Intellectual property rights frameworks across Europe reinforce protection of digital models and collaborative outputs, influencing licensing and software usage policies.

- •National digital infrastructure initiatives in countries like Germany and France support adoption of cloud and hybrid collaboration technologies through grants and tax incentives.

Industry Insights

- •In September 2023, Dassault Systèmes launched an advanced cloud-based 3D collaboration suite tailored for the European automotive sector, integrating AI-driven design validation and virtual prototyping, significantly reducing time-to-market. This launch strengthens Dassault’s leadership in Europe by addressing key industry pain points related to remote collaboration and design accuracy.

- •In March 2024, Siemens Digital Industries Software introduced a hybrid collaboration platform combining on-premise security with cloud scalability, targeting manufacturing and aerospace clients in Europe. The platform’s modular architecture allows seamless integration with existing CAD tools, boosting adoption among enterprises seeking flexible deployment options.

Mergers & Acquisitions

- •In July 2023, Hexagon AB completed the acquisition of a European software startup specializing in cloud-based 3D visualization tools, enhancing its portfolio in 3D design collaboration and expanding its footprint in the European construction and manufacturing sectors. This strategic move aims to accelerate innovation and improve cross-platform interoperability.

- •In November 2022, Nemetschek Group acquired a German SaaS provider focused on hybrid 3D collaboration solutions, strengthening its position in the architectural design segment across Europe. The acquisition facilitates integrated cloud services and broadens Nemetschek’s user base in key European markets.

Recent Industry News

- •In January 2024, Autodesk Inc. expanded its European operations by launching an advanced 3D collaboration platform with enhanced cloud security features tailored for the manufacturing sector, aiming to improve cross-border teamwork and reduce product development cycles. Source: Autodesk official press release.

- •In June 2023, Bentley Systems announced a partnership with a leading European aerospace manufacturer to co-develop virtual prototyping tools integrated into Bentley’s 3D collaboration platform, enhancing simulation accuracy and reducing prototyping costs. Source: Bentley Systems news portal.

- •In October 2022, PTC Inc. rolled out an AI-powered design collaboration module for its European clients, facilitating automated error detection and workflow optimization in product development processes, thereby increasing design efficiency. Source: PTC corporate news.

- •In April 2021, Graphisoft introduced a cloud-enabled architectural design solution focusing on sustainable building modeling, enabling European architects to integrate energy efficiency analyses within collaborative workflows. Source: Graphisoft media release.

Market Statistics

- •CAGR by 2034: 13.1%

- •Market Size by 2034: USD 4.5 Billion

- •Market Size in 2025: USD 1.35 Billion

- •Dominating Type: Cloud-based Platforms

- •Next-following Type: Hybrid Platforms

- •Dominating Application: Product Development

- •Next-following Application: Architectural Design

- •Dominating Region: Germany

- •Second-leading Region: United Kingdom

- •Region with Highest Growth Rate: France

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) - Dominating Type (Cloud-based Platforms): 45%, Followed Type (Hybrid Platforms): 30%

- •Market Share (%) - Dominating Application (Product Development): 50%, Followed Application (Architectural Design): 25%

- •Growth Rate (%) - Dominating Type (Cloud-based Platforms): 14.5%, Followed Type (Hybrid Platforms): 16.8%

- •Growth Rate (%) - Dominating Application (Product Development): 13.7%, Followed Application (Architectural Design): 12.9%

Top 5 Global Players

- •Dassault Systèmes (France)

- •Siemens Digital Industries Software (Germany)

- •Autodesk Inc. (United States - European Operations)

- •PTC Inc. (United States - European Operations)

- •Bentley Systems (United States - European Operations)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 4.5 Billion |

| CAGR | 13.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.4% |

| Scope of Report | Market is segmented by Type (Cloud-based Platforms, On-premise Solutions, Hybrid Platforms, Open Source Tools, Proprietary Software), Application (Product Development, Architectural Design, Engineering Simulation, Virtual Prototyping, Educational Training), End User (Manufacturing Industry, Construction & Architecture, Automotive Sector, Aerospace & Defense, Academic Institutions), Deployment Model (Cloud-based, On-premise, Hybrid) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Dassault Systèmes (France), Siemens Digital Industries Software (Germany), Autodesk Inc. (United States - European Operations), PTC Inc. (United States - European Operations), Bentley Systems (United States - European Operations), Nemetschek Group (Germany), Graphisoft (Hungary), Altair Engineering (United States - European Operations), Ansys Inc. (United States - European Operations), Trimble Inc. (United States - European Operations), AVEVA Group plc (United Kingdom), Hexagon AB (Sweden), SolidWorks Corporation (France), Bricsys NV (Belgium), Onshape (United States - European Operations), Synopsys, Inc. (United States - European Operations), McNeel Europe (United States - European Operations), Cadac Group (Netherlands), CoreTechnologie GmbH (Germany), Kubotek3D (Japan - European Operations), Cadenas GmbH (Germany), Tech Soft 3D (United States - European Operations), SimScale GmbH (Germany), 3YOURMIND GmbH (Germany), CAD Schroer (Germany) |

Europe 3D Design Collaboration Platform Market - Europe Size & Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.