Global PH Control Agents And Acidulants Market Size, Growth & Revenue 2024-2034

Global PH Control Agents And Acidulants Market is segmented by Type (Organic Acidulants, Inorganic Acidulants, Buffering Agents, Neutralizing Agents, Others), Application (Food & Beverage, Pharmaceuticals, Water Treatment, Agriculture, Cosmetics), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global PH Control Agents And Acidulants market comprises chemical compounds used to regulate pH levels across diverse industries including food & beverage, pharmaceuticals, water treatment, agriculture, and cosmetics. These agents ensure product integrity, safety, and regulatory compliance by maintaining optimal acidity or alkalinity, thus enhancing shelf-life and efficacy. The market includes organic acidulants like citric and lactic acid, inorganic acidulants such as phosphoric acid, buffering agents that stabilize pH, and neutralizing compounds.

- •Market growth is driven by increasing demand for food preservation, pharmaceutical formulations, and sustainable water treatment solutions globally. Rising health-conscious consumer trends, technological advancements in acidulant formulations, and stringent regulatory frameworks are key growth indicators. The market is forecasted to grow at a CAGR of 7.6% from 2024 to 2034, reaching USD 14.9 Billion.

- •PH control agents and acidulants hold strategic importance across industries for their role in product quality, safety, and environmental compliance. Their applications range from enhancing flavor and shelf-life in food to controlling water quality in treatment plants, making them indispensable for various stakeholders including manufacturers, regulators, and end-users worldwide.

Competitive Landscape

The global PH Control Agents And Acidulants market is characterized by intense competition among established chemical manufacturers and specialty chemical firms. Market players focus on innovation through the development of eco-friendly and high-efficiency acidulant products, strategic partnerships, and capacity expansions to strengthen market positions. Competitive strategies include diversification of product portfolios, advanced R&D for sustainable formulations, and geographic expansion to emerging markets. The rivalry is heightened by the demand for compliance with evolving regulatory standards and the need to address varying industry-specific requirements. Companies leverage technology adoption and quality certifications to differentiate themselves, while pricing strategies and supply chain optimization remain critical for maintaining competitive advantages. Regional competition also plays a role, with North America and Europe hosting leading innovators, while Asia-Pacific's rapid growth attracts new entrants and investments.

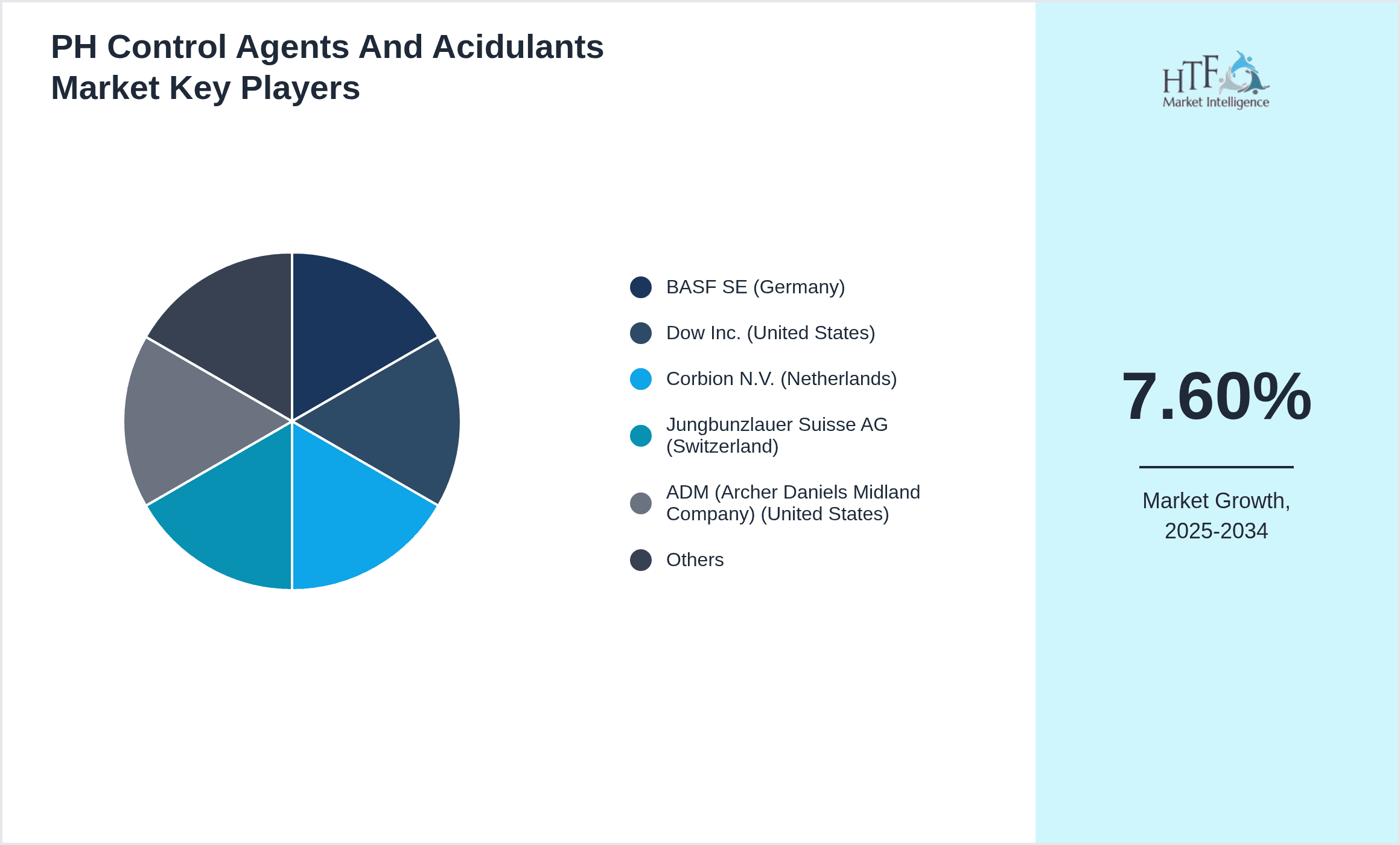

Leading Companies in PH Control Agents And Acidulants Market

- •BASF SE (Germany)

- •Dow Inc. (United States)

- •Corbion N.V. (Netherlands)

- •Jungbunzlauer Suisse AG (Switzerland)

- •ADM (Archer Daniels Midland Company) (United States)

- •Tate & Lyle PLC (United Kingdom)

- •CP Kelco (United States)

- •P&G Chemicals (United States)

- •Ingredion Incorporated (United States)

- •AkzoNobel N.V. (Netherlands)

- •Kerry Group (Ireland)

- •Nouryon (Netherlands)

- •Solvay S.A. (Belgium)

- •Eastman Chemical Company (United States)

- •Celanese Corporation (United States)

- •Solenis LLC (United States)

- •Ashland Global Holdings Inc. (United States)

- •Lanxess AG (Germany)

- •Evonik Industries AG (Germany)

- •Galaxy Surfactants Ltd. (India)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •Tosoh Corporation (Japan)

- •Clariant AG (Switzerland)

- •Solvchem Co., Ltd. (South Korea)

- •Yara International ASA (Norway)

Market Breakdown

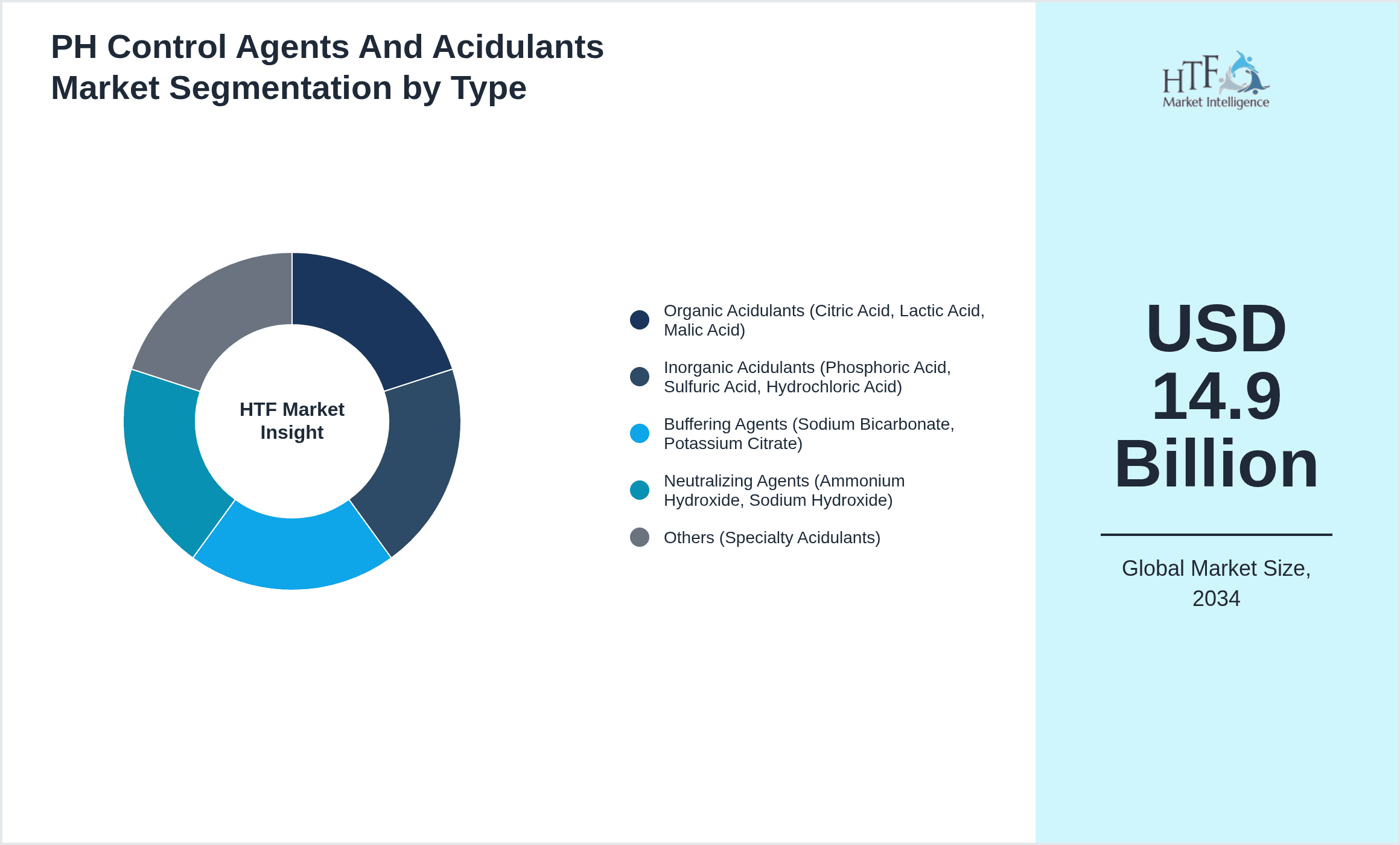

- •By Type

- ◦Organic Acidulants (Citric Acid, Lactic Acid, Malic Acid)

- ◦Inorganic Acidulants (Phosphoric Acid, Sulfuric Acid, Hydrochloric Acid)

- ◦Buffering Agents (Sodium Bicarbonate, Potassium Citrate)

- ◦Neutralizing Agents (Ammonium Hydroxide, Sodium Hydroxide)

- ◦Others (Specialty Acidulants)

- •By Application

- ◦Food & Beverage (Preservation, Flavoring)

- ◦Pharmaceuticals (Formulation, Stability)

- ◦Water Treatment (pH Regulation, Disinfection)

- ◦Agriculture (Soil pH Adjustment, Fertilizers)

- ◦Cosmetics (pH Balancing, Preservation)

- •By End User

- ◦Industrial Manufacturing

- ◦Healthcare & Pharmaceuticals

- ◦Agricultural Sector

- ◦Consumer Goods

- ◦Water Treatment Facilities

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Retail

- ◦Specialty Chemical Suppliers

Growth Drivers

The rapid expansion of the food and beverage industry globally is a primary driver for the PH Control Agents And Acidulants market, as these agents are essential for preserving flavor, texture, and shelf life of consumables. Increasing consumer demand for processed and packaged foods with extended durability fuels the need for effective acidulants. Moreover, the pharmaceutical sector's growth, driven by rising chronic diseases and aging populations, escalates demand for pH control in drug formulations to ensure efficacy and safety. Stringent environmental regulations encouraging eco-friendly water treatment processes also bolster market growth, as acidulants play a vital role in maintaining water quality. Technological advancements in formulation chemistry have enhanced product performance, further supporting adoption. Additionally, growing awareness of sustainable agriculture practices motivates the use of acidulants for soil pH adjustment, improving crop yield and quality across emerging economies.

Market Trends

A significant market trend is the shift towards bio-based and naturally derived PH control agents and acidulants, driven by consumer preference for clean-label products and regulatory pressure to reduce synthetic chemical usage. Companies are investing in R&D to develop organic acidulants sourced from renewable feedstocks. Digitalization and automation in manufacturing processes enable precise pH control and quality consistency, enhancing product reliability. Additionally, there is a growing trend in customization of acidulants tailored to specific industrial applications, such as targeted buffering capacity for pharmaceuticals or optimized flavor profiles in food. Collaborative innovation through partnerships between chemical manufacturers and end users is accelerating. Sustainability initiatives are influencing packaging and supply chain optimization to minimize environmental impact, reflecting evolving market dynamics.

Market Restraints

The PH Control Agents And Acidulants market faces challenges from fluctuating raw material costs, particularly for organic acidulants sourced from agricultural commodities, which may impact pricing stability. Stringent regulatory requirements across regions impose compliance burdens and increase time-to-market for new products. Some acidulants pose handling and storage hazards requiring specialized infrastructure, limiting their adoption in smaller enterprises. Market penetration in less developed regions is constrained by limited awareness and infrastructure. Additionally, the presence of substitutes and alternative pH control technologies like enzymatic systems can restrict market growth. Environmental concerns about chemical runoff and disposal further restrain usage, prompting manufacturers to seek safer and more sustainable alternatives. These factors collectively pose hurdles for consistent market expansion globally.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America offer significant growth opportunities due to expanding food processing industries and increasing pharmaceutical manufacturing capacities. The rising consumer inclination towards organic and natural products opens avenues for bio-based acidulants with premium positioning. Innovations in nanotechnology and encapsulation techniques can enhance acidulant stability and controlled release, creating product differentiation. Growing investments in sustainable water treatment and environmental remediation projects create demand for advanced pH control solutions. Collaborations between chemical producers and end users to develop customized formulations tailored to specific industrial requirements also present lucrative opportunities. Furthermore, digitization in supply chains and smart manufacturing facilitate operational efficiencies and market expansion potential, especially in developing regions.

Market Challenges

Key challenges include navigating complex and evolving regulatory landscapes that vary by country and application, increasing compliance costs and limiting product introductions. Volatility in raw material availability and prices, especially for plant-based acidulants, disrupts supply chains and impacts margins. The necessity for high purity and consistent quality in pharmaceutical and food-grade acidulants demands stringent quality control, adding operational complexity. Intense competition from established chemical giants and emerging local manufacturers constrains pricing power and market share. Additionally, environmental and health concerns about chemical usage necessitate ongoing investments in safer, greener alternatives, imposing research and development expenses. Market education and penetration remain difficult in underdeveloped regions due to infrastructure and knowledge gaps, slowing global adoption rates.

Regulatory Framework

From 2020 to 2024, the Global PH Control Agents And Acidulants market has been affected by tightening regulations focusing on food safety and environmental protection. Regulatory agencies like the FDA, EFSA, and EPA have introduced stricter guidelines for permissible acidulant types and concentration limits in consumables and water treatment. Compliance with REACH regulations in Europe mandates detailed chemical safety assessments, impacting manufacturing and import. Enhanced labeling and traceability requirements have been enforced to ensure consumer awareness and safety. Additionally, emerging regulations encourage the use of bio-based and biodegradable acidulants to reduce environmental impact. These regulatory frameworks have led to increased costs of compliance but have also driven innovation towards safer and sustainable product offerings globally.

Market Intelligence

- •In March 2024, BASF SE launched a new line of bio-based organic acidulants designed for the food and beverage sector, emphasizing sustainability and enhanced biodegradability. These products cater to growing consumer demand for natural additives and comply with stringent global food safety regulations. The launch aims to replace conventional synthetic acidulants and reduce environmental footprint significantly while maintaining product performance. This strategic move positions BASF as a leader in green chemistry innovation within the PH control market.

- •In November 2023, Dow Inc. introduced an advanced buffering agent technology that improves pH stability in pharmaceutical formulations under extreme storage conditions. This innovation enhances drug shelf-life and efficacy, addressing key industry challenges. Dow's proprietary technology integrates seamlessly with existing manufacturing processes, offering cost-effective solutions for pharmaceutical companies seeking to meet regulatory and quality benchmarks. The product launch strengthens Dow’s portfolio in high-value specialty chemicals.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •In July 2023, Corbion N.V. completed the acquisition of a specialty organic acidulant producer based in Southeast Asia, expanding its product portfolio and manufacturing footprint in emerging markets. This strategic acquisition enhances Corbion’s ability to serve the growing food and beverage and pharmaceutical sectors in the Asia-Pacific region with sustainable and high-quality acidulants. The deal also provides access to innovative bio-based technologies and regional distribution networks, strengthening Corbion’s competitive position globally.

- •In January 2024, AkzoNobel N.V. acquired a niche chemical company specializing in buffering and neutralizing agents used in water treatment applications. This acquisition complements AkzoNobel’s existing product range and accelerates its entry into the sustainable water treatment segment. The integration aims to leverage synergies in R&D and supply chain efficiencies, enabling AkzoNobel to provide comprehensive pH control solutions with enhanced environmental compliance. The move reflects industry consolidation trends focused on sustainability and innovation.

Recent Industry News

- •In May 2022, Jungbunzlauer Suisse AG announced a partnership with a leading food processing company to develop customized organic acidulant blends tailored for clean-label beverage formulations. This collaboration focuses on enhancing flavor profiles while meeting strict regulatory and consumer demand for natural ingredients. The joint initiative also involves co-innovation labs aimed at accelerating product development cycles and market adoption. Source: Industry Chemical News Network.

- •In September 2023, Tate & Lyle PLC expanded its manufacturing capacity for citric acid at its flagship facility in Europe to meet rising demand from pharmaceutical and food sectors. The expansion involved installing advanced fermentation technology to boost production efficiency and reduce carbon emissions. This investment supports Tate & Lyle’s sustainability goals and strengthens its market leadership in organic acidulants. Source: Global Food Ingredients Magazine.

- •In February 2024, Solvay S.A. launched a new eco-friendly inorganic acidulant product line designed for industrial water treatment applications. These products comply with updated environmental regulations and offer enhanced corrosion resistance. Solvay’s innovation targets the growing market for sustainable water management solutions across Asia-Pacific and Europe. Source: Chemical Industry Today.

- •In November 2021, Eastman Chemical Company entered into a strategic alliance with a biotechnology firm to co-develop next-generation buffering agents utilizing enzymatic technology. This partnership aims to create high-performance, biodegradable pH control solutions for pharmaceutical and cosmetic applications, addressing environmental and efficacy challenges. Source: Specialty Chemicals Journal.

Market Statistics

- •CAGR by 2034: 7.6%

- •Market Size by 2034: USD 14.9 Billion

- •Market Size in 2025: USD 7.3 Billion

- •Dominating Type: Organic Acidulants; Next-Following Type: Buffering Agents

- •Dominating Application: Food & Beverage; Next-Following Application: Pharmaceuticals

- •Dominating Region: North America; Second-Leading Region: Europe

- •Region with Highest Growth Rate: Asia-Pacific

- •Dominating Country: United States

Market Share Table

- •Market Share (%) - Organic Acidulants: 42%; Buffering Agents: 27%

- •Market Share (%) - Food & Beverage: 38%; Pharmaceuticals: 25%

- •Growth Rate (%) - Organic Acidulants: 6.9%; Buffering Agents: 9.1%

- •Growth Rate (%) - Food & Beverage: 7.2%; Pharmaceuticals: 8.0%

Top 5 Global Players

- •BASF SE (Germany)

- •Dow Inc. (United States)

- •Corbion N.V. (Netherlands)

- •Jungbunzlauer Suisse AG (Switzerland)

- •ADM (Archer Daniels Midland Company) (United States)

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 6.8 Billion |

| Forecast Year Market Size | USD 14.9 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.3% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | BASF SE (Germany), Dow Inc. (United States), Corbion N.V. (Netherlands), Jungbunzlauer Suisse AG (Switzerland), ADM (Archer Daniels Midland Company) (United States), Tate & Lyle PLC (United Kingdom), CP Kelco (United States), P&G Chemicals (United States), Ingredion Incorporated (United States), AkzoNobel N.V. (Netherlands), Kerry Group (Ireland), Nouryon (Netherlands), Solvay S.A. (Belgium), Eastman Chemical Company (United States), Celanese Corporation (United States), Solenis LLC (United States), Ashland Global Holdings Inc. (United States), Lanxess AG (Germany), Evonik Industries AG (Germany), Galaxy Surfactants Ltd. (India), Mitsubishi Chemical Holdings Corporation (Japan), Tosoh Corporation (Japan), Clariant AG (Switzerland), Solvchem Co., Ltd. (South Korea), Yara International ASA (Norway) |

Global PH Control Agents And Acidulants Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.