Japan Ceramic Ball Blanks Market - Japan Size & Outlook 2020-2034

Japan Ceramic Ball Blanks Market is segmented by Type (Silicon Nitride Ceramic Ball Blanks, Zirconia Ceramic Ball Blanks, Alumina Ceramic Ball Blanks, Other Advanced Ceramic Materials), Application (Bearings, Valves, Seals, Medical Devices, Electronics, Automotive, Aerospace), Manufacturing Process (Isostatic Pressing, Slip Casting, Injection Molding, Dry Pressing), Surface Finish (Polished, Unpolished, Coated), and Geography (Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu)

Pricing

Report Overview

Executive Summary

- •The Japan Ceramic Ball Blanks market involves the production of ceramic spheres primarily used in bearings, valves, seals, medical devices, electronics, automotive, and aerospace industries. These blanks are manufactured from high-performance ceramics such as silicon nitride, zirconia, and alumina, offering superior hardness, wear resistance, and thermal stability essential for demanding industrial applications.

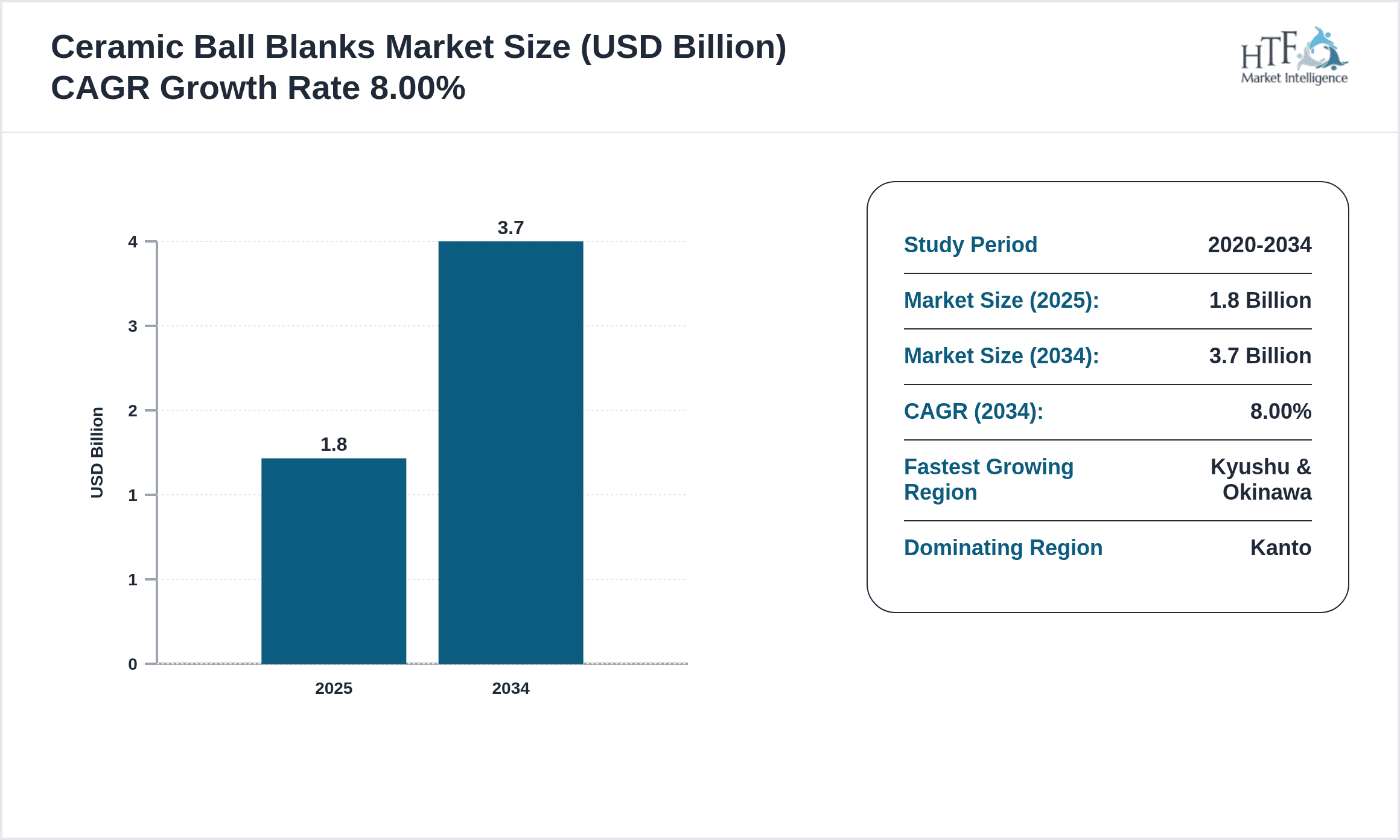

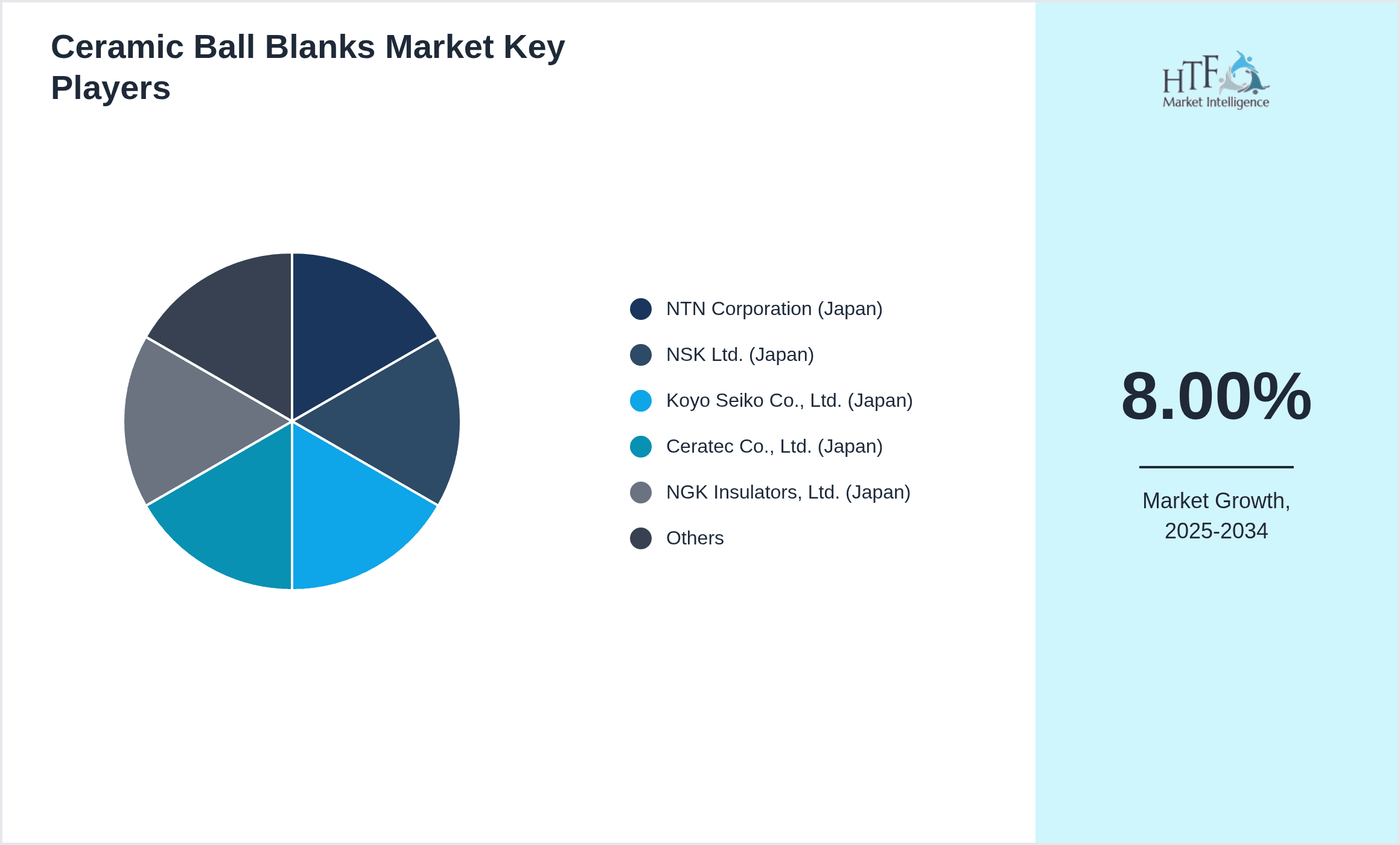

- •The market has shown significant growth from 2020 to 2025, with an estimated CAGR of 8.0%, driven by rising demand for durable and high-precision components in Japan's manufacturing sectors. Silicon nitride ceramic ball blanks dominate the market due to their excellent mechanical properties and broad industrial applicability.

- •Strategic importance of ceramic ball blanks lies in their contribution to enhancing the lifespan and performance of critical machinery components across various industries, positioning Japan as a key hub for advanced ceramic materials manufacturing and innovation.

Competitive Landscape

The Japan Ceramic Ball Blanks market is highly competitive with key players focusing on product innovation, quality enhancement, and strategic partnerships to secure market share. Competitive strategies include advanced ceramic material development, proprietary manufacturing processes, and customization capabilities tailored to industry-specific requirements. Market players emphasize investments in R&D to improve mechanical properties and reduce production costs. The competitive environment is also shaped by stringent quality standards and certifications demanded by automotive, aerospace, and medical sectors. Distribution channels and strong supplier relationships play a crucial role in maintaining competitive advantage. Regional competition within Japan’s industrial zones fosters continuous technological advancements and efficiency improvements, while market entry barriers such as high capital investment and technical expertise limit new entrants, maintaining a consolidated competitive landscape.

Leading Companies in Japan Ceramic Ball Blanks Market

- •NTN Corporation (Japan)

- •NSK Ltd. (Japan)

- •Koyo Seiko Co., Ltd. (Japan)

- •Ceratec Co., Ltd. (Japan)

- •NGK Insulators, Ltd. (Japan)

- •Mitsubishi Materials Corporation (Japan)

- •Kyocera Corporation (Japan)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Ube Industries, Ltd. (Japan)

- •Toho Tenax Co., Ltd. (Japan)

- •Tosoh Corporation (Japan)

- •Hitachi Chemical Company, Ltd. (Japan)

- •Shin-Etsu Chemical Co., Ltd. (Japan)

- •Furukawa Electric Co., Ltd. (Japan)

- •Daido Steel Co., Ltd. (Japan)

- •Muratec Precision Co., Ltd. (Japan)

- •Kyudenko Corporation (Japan)

- •JTEKT Corporation (Japan)

- •NGK Spark Plug Co., Ltd. (Japan)

- •Mikuni Corporation (Japan)

- •Fuji Electric Co., Ltd. (Japan)

- •Asahi Glass Co., Ltd. (Japan)

- •Mitsui Chemicals, Inc. (Japan)

- •Toyo Seikan Group Holdings, Ltd. (Japan)

- •Nippon Steel Corporation (Japan)

Market Breakdown

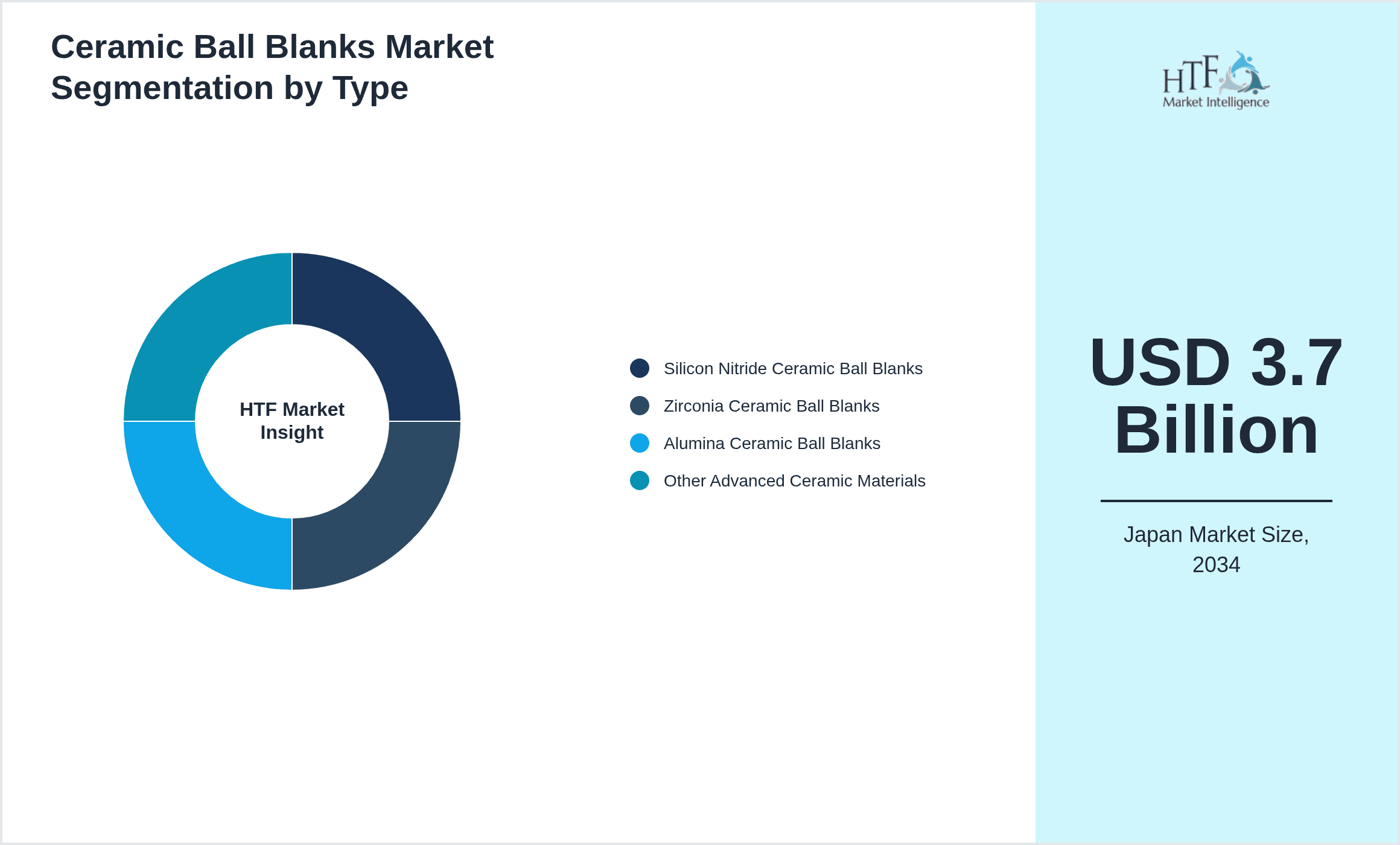

- •By Type

- ◦Silicon Nitride Ceramic Ball Blanks

- ◦Zirconia Ceramic Ball Blanks

- ◦Alumina Ceramic Ball Blanks

- ◦Other Advanced Ceramic Materials

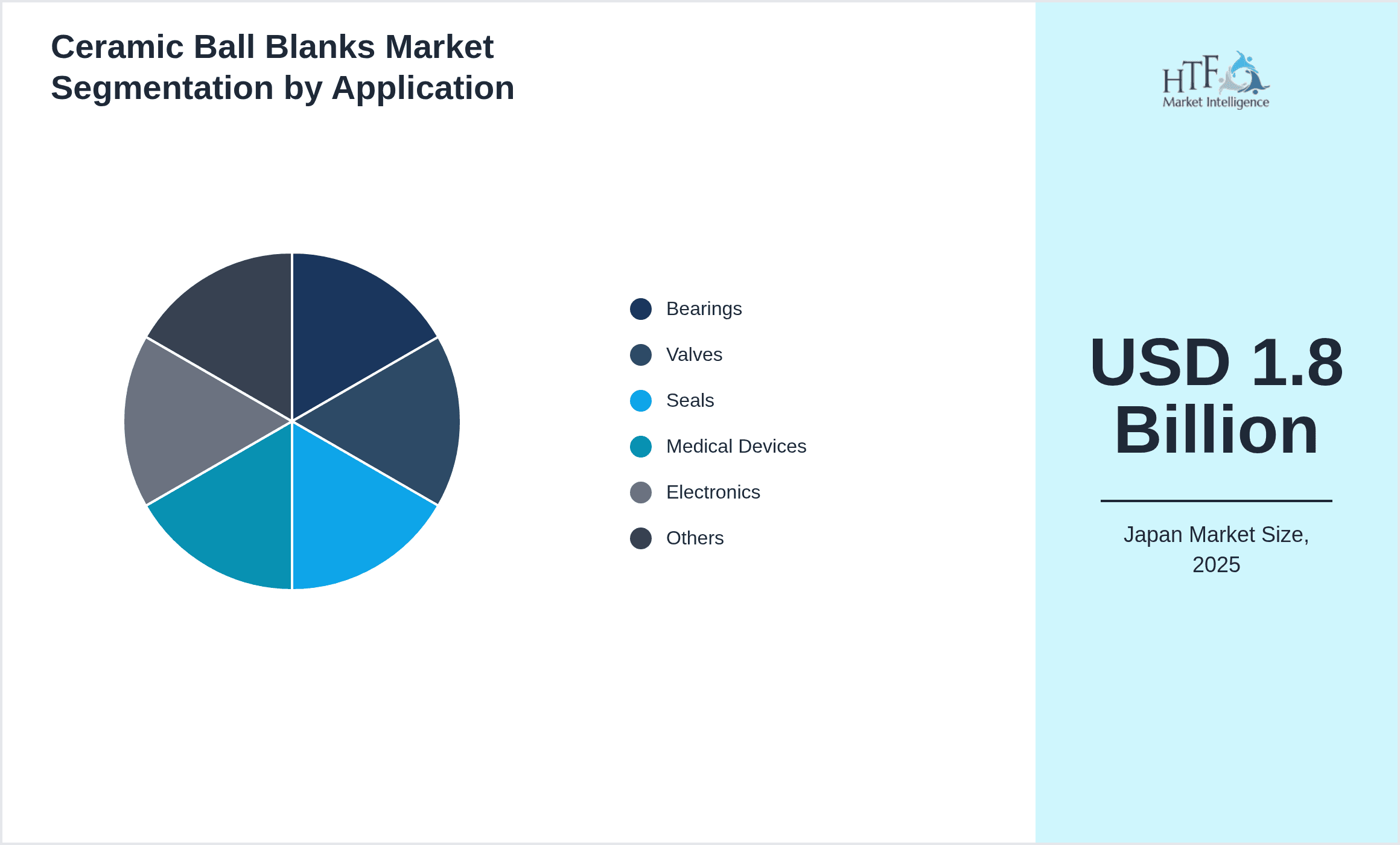

- •By Application

- ◦Bearings

- ◦Valves

- ◦Seals

- ◦Medical Devices

- ◦Electronics

- ◦Automotive

- ◦Aerospace

- •By Manufacturing Process

- ◦Isostatic Pressing

- ◦Slip Casting

- ◦Injection Molding

- ◦Dry Pressing

- •By Surface Finish

- ◦Polished

- ◦Unpolished

- ◦Coated

Growth Dynamics

The growth of the Japan Ceramic Ball Blanks market is primarily driven by increasing demand from automotive and aerospace industries, which require precision-engineered ceramic components for enhanced durability and performance. Technological advancements in ceramic manufacturing, such as improved sintering techniques, enable production of higher quality blanks at scale. Additionally, expanding applications in medical devices and electronics contribute significantly, as these sectors demand biocompatible and electrically insulating materials. The government’s support for advanced materials R&D and rising exports of Japanese precision components further stimulate market expansion. Increased awareness about the benefits of ceramic materials over metals in terms of wear resistance and thermal stability also supports sustained growth.

Market Trends

Emerging trends include adoption of nanotechnology to enhance ceramic ball blank properties, integration of automation in manufacturing processes, and growing use of zirconia ceramics for improved toughness. There is also a notable shift towards environmentally friendly manufacturing practices within the industry. The rise of electric vehicles has increased demand for ceramic components in bearings and sensors, further influencing product innovation and market dynamics.

Market Opportunities

Significant opportunities exist in expanding the use of ceramic ball blanks in emerging sectors such as robotics, renewable energy systems, and next-generation electronics, where material durability and precision are critical. Japan's advanced manufacturing ecosystem provides a strong foundation for collaborative innovation and product development. Additionally, there is potential for export growth to Asia-Pacific and global markets by leveraging Japan’s reputation for quality and technological leadership.

Market Challenges

The market faces challenges including the high cost of raw materials and complex manufacturing processes which limit price competitiveness. Supply chain disruptions and availability of high-purity ceramic powders can hinder production continuity. Moreover, stringent quality standards and certifications required by end-use industries necessitate substantial investment in quality assurance and testing infrastructure. Competition from alternative materials and international manufacturers also poses market entry and expansion difficulties.

Regulatory Framework

Between 2020 and 2025, Japan implemented several regulations impacting the ceramic materials industry, including stricter environmental emission standards related to manufacturing waste and energy consumption. Compliance with the Japan Industrial Standards (JIS) for ceramic components ensures product reliability and safety, especially in automotive and aerospace applications. The Ministry of Economy, Trade and Industry (METI) enforces policies promoting sustainable manufacturing practices and supports innovation grants for advanced ceramics. Additionally, medical device regulations require rigorous testing and certification of ceramic components used in implants and instruments, influencing market dynamics and product development strategies.

Market Intelligence

- •15th January 2025, NSK Ltd. launched a new line of silicon nitride ceramic ball blanks designed for next-generation electric vehicle bearings. These blanks feature enhanced wear resistance and lower weight, targeting improved efficiency and durability in EV drivetrain systems. The launch aligns with growing EV adoption trends in Japan and globally, positioning NSK as a technological leader in advanced ceramic components. The product rollout is supported by integrated digital quality control systems to ensure consistent manufacturing standards. Source: NSK Ltd. official press release.

- •10th March 2025, Kyocera Corporation announced a strategic collaboration with local universities to develop innovative zirconia ceramic ball blanks with improved fracture toughness for aerospace applications. The partnership aims to accelerate research in nanostructured ceramics and expand product applicability in high-stress environments. Kyocera also revealed plans to invest USD 50 million in expanding its ceramic manufacturing facilities in the Kansai region to meet growing domestic and export demands. Source: Kyocera Corporation corporate news.

- •28th May 2024, NGK Insulators, Ltd. completed the acquisition of a smaller ceramic materials firm specializing in alumina powders, enhancing its raw material supply chain and production capabilities for ceramic ball blanks. This move strengthens NGK’s position in the precision ceramics market and supports product portfolio diversification. The acquisition is expected to generate synergies in R&D and reduce production costs through vertical integration. Source: NGK Insulators, Ltd. investor relations.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Kanto currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Kyushu & Okinawa is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Kansai

- Chugoku

- Shikoku

- Kyushu

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 3.7 Billion |

| CAGR | 8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.7% |

| Scope of Report | Market is segmented by Type (Silicon Nitride Ceramic Ball Blanks, Zirconia Ceramic Ball Blanks, Alumina Ceramic Ball Blanks, Other Advanced Ceramic Materials), Application (Bearings, Valves, Seals, Medical Devices, Electronics, Automotive, Aerospace), Manufacturing Process (Isostatic Pressing, Slip Casting, Injection Molding, Dry Pressing), Surface Finish (Polished, Unpolished, Coated) |

| Regions Covered | Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu |

| Key Companies | NTN Corporation (Japan), NSK Ltd. (Japan), Koyo Seiko Co., Ltd. (Japan), Ceratec Co., Ltd. (Japan), NGK Insulators, Ltd. (Japan), Mitsubishi Materials Corporation (Japan), Kyocera Corporation (Japan), Sumitomo Electric Industries, Ltd. (Japan), Ube Industries, Ltd. (Japan), Toho Tenax Co., Ltd. (Japan), Tosoh Corporation (Japan), Hitachi Chemical Company, Ltd. (Japan), Shin-Etsu Chemical Co., Ltd. (Japan), Furukawa Electric Co., Ltd. (Japan), Daido Steel Co., Ltd. (Japan), Muratec Precision Co., Ltd. (Japan), Kyudenko Corporation (Japan), JTEKT Corporation (Japan), NGK Spark Plug Co., Ltd. (Japan), Mikuni Corporation (Japan), Fuji Electric Co., Ltd. (Japan), Asahi Glass Co., Ltd. (Japan), Mitsui Chemicals, Inc. (Japan), Toyo Seikan Group Holdings, Ltd. (Japan), Nippon Steel Corporation (Japan) |

Japan Ceramic Ball Blanks Market - Japan Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.